Kuaishou’s Strategic Split: Let Kling Shine While Laotie Tills the Fields

05/13 2026

05/13 2026

519

519

Produced by | RoboIsland

When God wanted to watch a movie, He created light. When capital seeks a narrative, Kuaishou has chosen to spin off Kling.

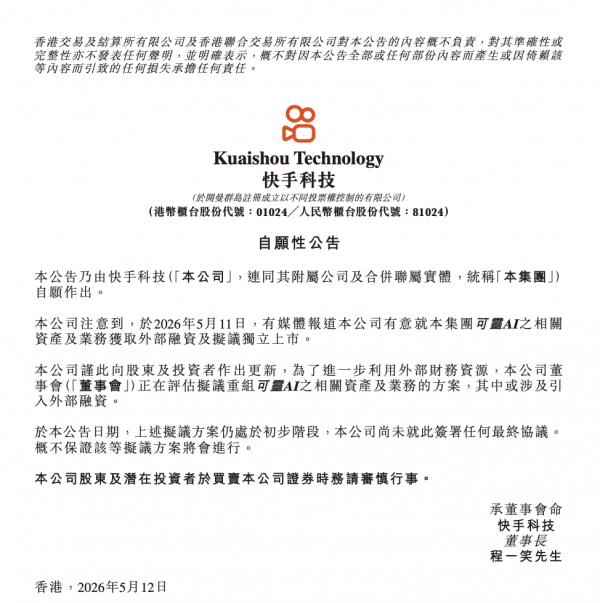

On May 12, a surge in Hong Kong stocks signaled the official commencement of Kuaishou’s strategic split.

A Kuaishou announcement confirmed external rumors: The board is evaluating a plan to restructure Kling AI, potentially introducing external financing with a target valuation of $20 billion.

To ensure clarity, the announcement stressed that the plan is still in its preliminary stages, with no final agreements signed, and “no assurance that such proposed transactions will proceed.”

Prior to this announcement, Kuaishou’s entire group had a market capitalization of less than $29 billion.

It’s as if a diligent father, overseeing a family business worth less than $30 billion, discovers that his two-year-old son, contributing less than 1% of the group’s revenue, is valued at $20 billion by the village—70% of his own net worth.

This isn’t merely a case of a son gaining prestige through his father; it’s the ultimate reversal where the father gains prestige through his son. When the “Laotie economy” collides with the new silicon-based powerhouse, Kuaishou is performing a daring asset reshuffling.

Meanwhile, *LatePost* reported that Kling plans to raise $2 billion in this round, with negotiations underway with investors including Tencent, though the deal has not yet been finalized. If completed, Kling would become the highest-valued independent product in video generation AI globally.

So why is Kling going solo? Is this split advantageous or detrimental for both parties? After divesting its most attractive AI asset, where will Kuaishou’s e-commerce foundation head? RoboIsland attempts to dissect this $20 billion conundrum.

1. In Laotie's Ledger, Silicon’s Price is Unaccountable

Kling’s solo journey may appear to be Kuaishou’s noble act of letting go, but in reality, it’s a desperate move for self-preservation driven by four key constraints: computing power, financial resources, talent, and valuation systems.

Capital markets evaluate Kuaishou based on PE (price-to-earnings), DAU (daily active users), and e-commerce GMV. These metrics are suitable for assessing a mature—or even declining—content platform.

However, for AI companies, especially high-growth entities like Kling with ARR (annual recurring revenue) multiplying severalfold annually, the metrics are PS (price-to-sales), technological edge, and market share.

Buried within Kuaishou, Kling remains a mere footnote in online marketing services or other businesses—a glamorous lace trim hidden beneath the bulky coat of Laotie culture, invisible to the outside world.

Only by extracting, showcasing, and labeling it as China’s Runway or even the OpenAI of video generation can it command a 10x or even 20x PS valuation premium.

This isn’t just a spin-off; it’s a valuation leap.

The valuation mismatch is merely superficial. Behind it lies a harsh reality: Kuaishou can’t afford this “money pit.”

How costly are video generation models? Sora reportedly burns $15 million daily, a cautionary tale. Kuaishou’s own CapEx is staggering: $26 billion planned for 2026, a $11 billion YoY surge, compared to its full-year net profit of just $20.6 billion.

Earnings from a year of hard work aren’t sufficient to fund Kling’s operations. ByteDance vows to invest $200 billion in AI infrastructure—this arms race operates on an entirely different scale.

The solution? Use strategy to overcome challenges. Push Kling to market, let Tencent and other backers foot the bill, and fight the computing war with others’ resources. This is risk socialization and benefit privatization—after all, Kuaishou remains the majority shareholder.

Additionally, Kling’s founder, Zhang Di, defected to Alibaba and launched HappyHorse-1.0, delivering a precise blow to his former employer.

DeepSeek and ByteDance are offering separate stock options to AI teams, with IPO valuations soaring to hundreds of billions. Without dangling a $40 billion IPO carrot, why would top scientists settle for a communal pot?

Kuaishou realized that salaries and group options alone couldn’t retain talent.

Thus, Kling must go solo.

Beside Laotie, Kling is an overqualified son-in-law; alone, it becomes the capital market’s dream dragon slayer.

2. Tencent Smiles, Retail Investors Baffled: Who Profits Most from This Deal?

Kling’s departure from Kuaishou is a reshuffle of power and interests, with no simple winners or losers—only complex bull-bear battles.

Shedding its “Kuaishou’s pride” label, Kling finally breathes freely. It gains independent financing rights, directly accepting dollars from giants like Tencent without bowing to Kuaishou’s budget constraints.

More valuable is its industry neutrality. Independent Kling can transform from a Kuaishou tool into industry infrastructure, earning from all film studios and advertisers.

But Kling loses Kuaishou’s daily feeding of 40 million videos and privileged access to seamlessly integrate ads and e-commerce systems. Henceforth, it must face ByteDance’s Seedance and Alibaba’s HappyHorse head-on, unprotected by its mother.

For Kuaishou, the drama grows more nuanced.

Short-term, the split is a strategic move. $2 billion in external financing alleviates profit pressure from $26 billion in CapEx, instantly beautifying financial reports.

Moreover, Kuaishou retains a large stake in Kling. If Kling IPOs at a $40 billion valuation, this stake could exceed Kuaishou’s current market cap.

Using 1% of its business to leverage 100% of its market cap imagination—this deal pays off.

But long-term, a strategic void emerges.

Kuaishou has stripped away its most imaginative, AI-driven “future story.”

Once markets notice e-commerce growth slowing to 15%, DAUs declining, and the sole high-valuation AI narrative gone, Kuaishou will revert to a “Laotie marketplace” in capital eyes—a slightly outdated one.

This poses a soul-searching question for Kuaishou’s management: Do you guard a profitable but mediocre company, or gamble on a valuable, great future?

In this deal, Tencent likely smiles the broadest. As Kuaishou’s largest external shareholder, it profits from the parent company’s stock surge while securing a strategic stake in Kling’s new rocket—a win-win.

The most injured are small investors lured by Kling’s halo.

They expected “buy Kuaishou, get Kling free,” only to receive “buy Kuaishou, lose Kling”—their stocks collapsing into a pure Laotie economy play.

3. Kuaishou E-commerce in the Post-Kling Era

Kuaishou’s AI choices are deeply ingrained in its DNA. It can’t become a ByteDance-style universal AI empire; it must—and can only—become the ultimate transaction-savvy video AI expert.

Consider this funding round. Kling’s pre-IPO aims to raise $2 billion, with Tencent rumored to participate. But Alibaba, Middle Eastern sovereign funds, and even VC/PE firms reaping AI windfalls may vie for a stake in China’s AI video leader.

This transaction represents Chinese internet capital and global hot money collectively pricing and hunting the most certain AI application-layer assets.

Kuaishou’s e-commerce won’t automatically recover after Kling’s exit, but it sheds baggage, gaining agility to pragmatically save itself.

The answer lies in AI empowerment.

Post-split, Kuaishou can freely procure global top-tier AI capabilities, including Kling’s own APIs, to arm its merchant ecosystem.

From AI product selection and bulk short-video generation to digital human livestreaming and smart customer service, AI will infiltrate every e-commerce pore like electricity and water.

Kuaishou aims to package Laotie’s street-market shopping into an algorithm-driven, personalized immersive experience.

Can this moat hold? Pressure mounts. As RoboIsland analyzed in *Kling's Rise Can't Offset Kuaishou's Weakening Foundations*, Kling accelerates while Kuaishou slows.

In 2026, Kuaishou’s GMV growth fell to 15%, with the company ceasing to disclose the metric—a sign of the boom era’s end.

But Kuaishou isn’t out of options. It holds an unstealable ace: private-domain trust. Its future lies not in replacing hosts with AI but in making AI hosts' ultimate fan-whisperer—helping them select products, reach audiences, and handle after-sales.

Send silicon’s new deity to the front lines while keeping carbon-based Laotie grounded in grassroots precision—this may not be the sexiest narrative, but it's the most pragmatic way to survive.

4. Epilogue

Kuaishou’s split with Kling marks China’s internet sector’s most resolute AI-era asset divestiture.

Kling soars with Kuaishou’s last ambition. Its $20 billion valuation bets on market fantasies of an independent AI video empire—and Kuaishou’s struggle to avoid second-tier internet status.

Kuaishou, left behind, must learn to live without its halo.

As high-growth stories fade, it must prove that a down-to-earth, profitable company still deserves respect.

The higher Kling flies, the more Kuaishou must grip the earth—perhaps the most profound fate in this split.

© RoboIsland. All rights reserved. No reproduction without authorization.

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!

-

![]()

AI Agent Smartphones: The Next Competitive Edge Transcends Large Models

-

![]()

Over 880 Million Yuan Worth of Orders Unveiled, Bidding Launched for Shenzhen Eastern Public Transport

-

![]()

Tesla's Robotaxi Hits the Road: A Monumental Gamble with an Uncertain Future