ZTE: Achieved Scale but Lost Profits, 133.9 Billion Yuan in Revenue Yields Only 5.6 Billion Yuan in Profit

05/13 2026

05/13 2026

458

458

Author | Haishan

Source | Bowang Finance

Standing at a strategic crossroads, ZTE's "report card" is full of contradictions.

According to the financial report, the company's revenue in 2025 was 133.895 billion yuan, a year-on-year increase of 10.38%, reaching a record high. However, behind the impressive revenue figures, net profit fell by 33% year-on-year. The situation did not improve in the first quarter of 2026, with non-recurring net profit falling by 52.16% year-on-year.

The report card of "revenue growth without profit increase" is not only a microcosm of the industry's downturn but also exposes hidden concerns in its profit structure, cash flow, asset quality, and core technologies. It also reflects the growing pains traditional communication giants must endure when transitioning to computing power.

So, what has ZTE experienced behind the scenes, and what does its future hold?

01

The Dilemma of "Revenue Growth Without Profit Increase"

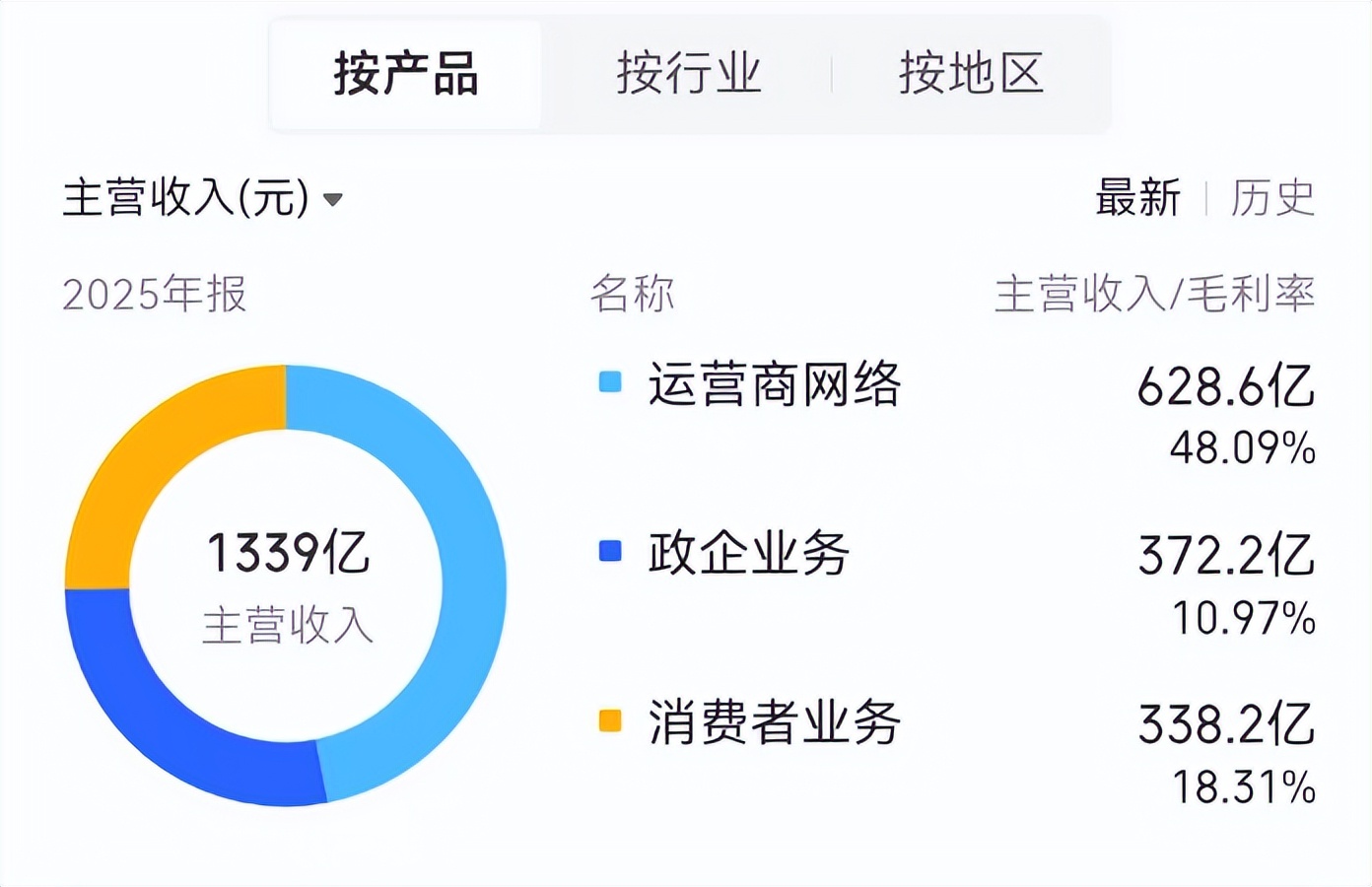

ZTE was listed on the Shanghai Stock Exchange in November 1997, with its main business being to provide customers with satisfactory ICT products and solutions. The company's product categories include operator networks, government and enterprise services, and consumer services.

Source: Tonghuashun

In 2025, ZTE's performance showed a sharp divergence. Financial reports showed that the company's annual revenue reached 133.895 billion yuan, a year-on-year increase of 10.38%, setting a new historical record. However, net profit attributable to shareholders was only 5.618 billion yuan, a year-on-year decline of 33.32%, and non-recurring net profit fell by 45.45% to 3.37 billion yuan.

Source: Company Annual Report

This coexistence of record-high revenue and a profit cliff, signaling "revenue growth without profit increase," reflects that the company is in a critical period of deep business structure adjustment.

The core root of "revenue growth without profit increase" lies in the structural shift between high- and low-margin businesses. In 2025, the company's operator network business revenue fell by 10.62% year-on-year, with its proportion of total revenue dropping to 46.94%. In contrast, government and enterprise business surged by 100.49% year-on-year, with its revenue share rising to 27.80%.

This shift caused the company's comprehensive gross margin to plummet from 41.53% in 2023 to 30.25% in 2025, directly dragging down overall profitability and intensifying the pains of transformation.

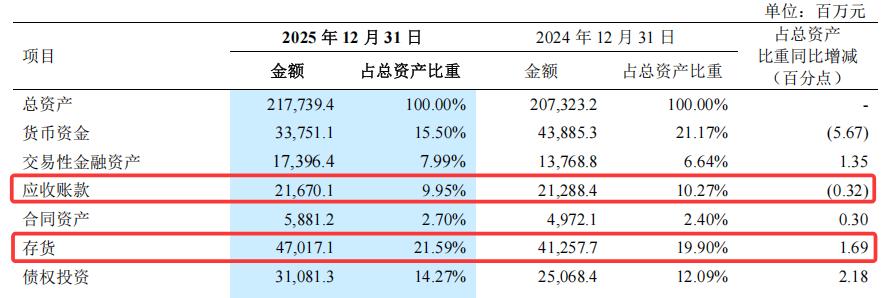

Alarmingly, excessive asset occupation further dragged down profit quality. By the end of 2025, ZTE's inventory had reached 47.017 billion yuan, a year-on-year increase of 1.69%. This asset "precipitation" not only occupied a huge amount of operating capital but also raised market concerns about its composition and liquidity.

Source: Company Annual Report

Meanwhile, by the end of 2025, the company's accounts receivable had reached 21.67 billion yuan, accounting for an astonishing 385.74% of net profit attributable to shareholders. The recovery of these funds directly affects the company's cash flow health and indirectly reflects changes in its bargaining power when dealing with downstream customers.

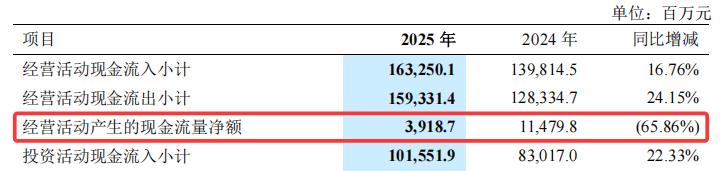

Payment collection pressure directly erodes cash flow health. In 2025, ZTE's net cash flow from operating activities was only 3.919 billion yuan, a staggering year-on-year decline of 65.86%. The ratio of operating cash flow to net profit dropped to 0.7, meaning that the company's book profits were not effectively converted into actual cash inflows, significantly worsening profit quality.

Source: Company Annual Report

Unreasonable capital management also constrained enterprise development. In the past two years, the company has continuously expanded its debt scale, with new bonds payable reaching 7.81 billion yuan. At the same time, its financial management quota was raised to 40 billion yuan, with financial assets accounting for more than 20% of total assets. The model of borrowing while making large financial investments, combined with reduced research and development and personnel investment, resulted in a return on invested capital of only 3.58% in 2025, far below the industry average, indicating low capital efficiency.

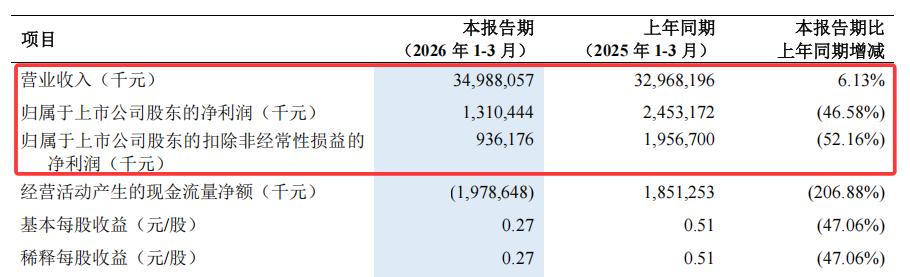

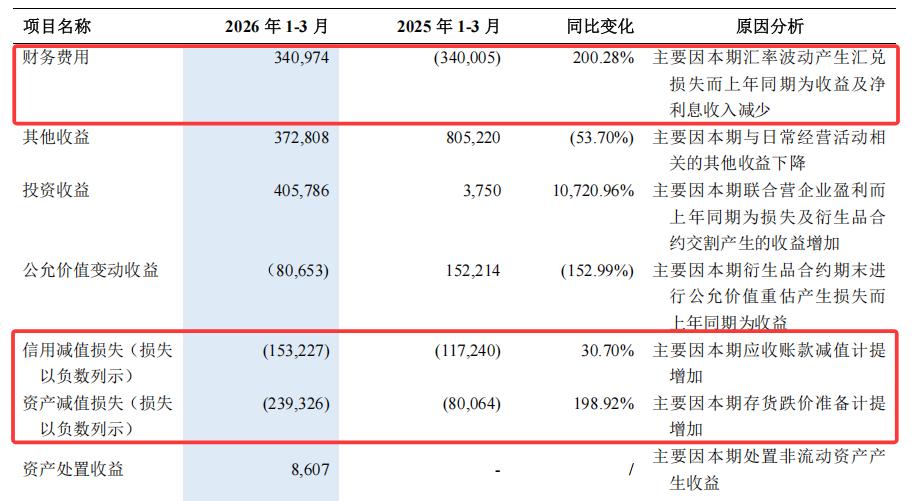

In the first quarter of 2026, operating pressure further amplified. Revenue was 34.988 billion yuan, with a growth rate of only 6.13%. Net profit attributable to shareholders was 1.31 billion yuan, a year-on-year decline of 46.58%, with non-recurring net profit nearly halved. More severe ly, operating cash flow turned negative, with a net outflow of 1.979 billion yuan, significantly weakening the company's ability to generate cash.

Source: Company Quarterly Report

The causes can be traced to the continuous contraction of high-margin communication businesses and the continued expansion of low-margin computing power businesses. In the first quarter, the comprehensive gross margin dropped to 28.3%. Coupled with a 341 million yuan financial loss due to exchange rate fluctuations and a significant increase in credit and asset impairments, multiple negative factors combined to further highlight ZTE's transformation pressure and operational risks.

Source: Company Quarterly Report

02

Growing Pains Under Business Structure Reconstruction

The core reason for ZTE's diverging performance trends lies in the company's critical strategic transformation phase. The company is implementing a "connectivity + computing power" dual-drive strategy, actively reconstructing its business landscape, and forming a differentiated pattern of contraction in traditional main businesses and expansion in emerging businesses. The adjustment of the business structure has brought short-term growing pains and exposed multiple operational structural vulnerabilities.

The operator network business has long been the cornerstone of ZTE's profits, with advantages of high margins and stable payment collection. In 2025, revenue from this business was 62.857 billion yuan, a year-on-year decline of 10.62%, contracting for the second consecutive year. Its revenue share dropped from 66.61% in 2023 to 46.94%, falling below 50% for the first time. Despite the scale decline, the gross margin remained high at 48.09%, still the most profitable segment.

Its contraction is mainly due to the domestic 5G construction entering a stock cycle, with operators reducing capital expenditures, compounded by intensified geopolitical barriers overseas, continuously narrowing the growth space in the traditional communication equipment market.

Source: Company Annual Report

To break through the ceiling, ZTE is fully betting on government and enterprise business, seeking breakthroughs through the computing power track. In 2025, revenue from government and enterprise business was 37.222 billion yuan, surging by 100.49% year-on-year, with its share climbing to 27.80%. Among them, computing power business revenue grew by 150% annually, with servers and storage increasing by more than 200%. Products have entered the supply chains of leading companies such as Alibaba and Tencent, with intelligent computing centers landing in multiple locations.

However, behind the rapid expansion lies a fatal weakness—the business's gross margin was only 10.97%, a further year-on-year decline of 4.36 percentage points, nearly 37 percentage points lower than that of the operator business. The characteristics of heavy capital investment and long payment terms in the computing power industry have trapped the company in an operational vicious circle of "the more it expands, the more cash-strapped it becomes."

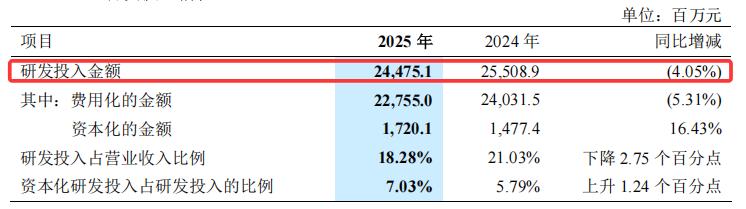

Under profit pressure, ZTE's research and development investment is also contracting. From 2023 to 2025, research and development expenses fell from 26.783 billion yuan to 24.475 billion yuan, with the number of researchers decreasing by more than 3,700. While this has compressed costs in the short term, against the backdrop of accelerated technological iteration, resource contraction may erode long-term technological barriers.

Source: Company Annual Report

Notably, ZTE's independent research and development of core technologies is insufficient. The company still relies heavily on external purchases for high-end chips, with its self-developed NPU computing power lagging behind leading manufacturers by generations, and the mass production of 5nm process ASICs delayed. The high proportion of imported core components poses hidden risks to supply chain stability.

From an industry perspective, ZTE's dilemma is essentially a common challenge during the transformation period of the communication equipment industry. Currently, the industry is undergoing three structural changes: a decline in operator investment, an explosion in computing power demand, and accelerated technological convergence. Companies such as Huawei, Inspur Information, and New H3C are accelerating their layout in the computing power track, with price wars becoming normalized and profit ceilings continuing to decline.

03

Development Game Under Multiple Constraints

Currently, the traditional communication industry has entered a stock adjustment cycle, the computing power track is mired in low-price internal competition, and coupled with core technology limitations, ZTE's transformation process faces significant resistance.

In addition to internal business structure imbalances, industry stock internal competition, accelerated technological iteration, geopolitical suppression, and weak industrial chain bargaining power constitute external bottlenecks for ZTE's long-term development. These constraints stem from the deep-seated changes in the communication and computing power industries, are long-term and complex, and difficult to resolve in the short term.

The traditional communication industry has entered a stock competition phase. Domestic 5G construction is nearing saturation, with 6G still in the research and testing phase. Operators are shifting capital expenditures toward computing power networks, and demand for traditional equipment remains sluggish. Currently, ZTE's domestic base station market share is about 30%, far lower than Huawei's 55%, with insufficient competitiveness in the high-end market. It can only rely on mid-to-low-end products to maintain revenue through volume sales, with weak pricing power. Coupled with the global contraction of the traditional communication equipment market, the growth ceiling continues to lower.

Although the computing power track has broad prospects, fierce internal competition is compressing profit margins. Global AI infrastructure spending is expected to exceed 450 billion US dollars in 2026, but internet vendors, server manufacturers, and chip companies are all crossing into the market, leading to excess low-end capacity and industry gross margins generally below 15%.

Source: Public Reports

ZTE's computing power business mainly focuses on mid-to-low-end servers and general-purpose equipment, with low penetration of high-end AI computing power servers and high-speed optical modules. Compared to leading companies such as Inspur Information and Foxconn Industrial Internet, it lacks technological accumulation and weak brand premium ability. At the same time, the accelerated pace of technological iteration continues to raise industry thresholds, increasing the pressure on ZTE, with limited research and development scale, to catch up technologically.

Geopolitics is the biggest external constraint. Technological sanctions and trade barriers in European and American markets continue to tighten, strictly limiting the company's product exports and technological cooperation, with almost no market share in the high-end European and American markets. Overseas revenue relies heavily on emerging economies such as Asia-Pacific, Middle East, and Latin America, which are prone to political instability, exchange rate fluctuations, and other risks, leading to high operational uncertainty and severely limiting globalization layout .

Weak bargaining power in the industrial chain further squeezes profit margins. ZTE mainly undertakes midstream equipment integration, relying heavily on imports for upstream high-end computing power chips, radio frequency devices, and other core components. Downstream operators engage in centralized procurement and price pressure, placing the company in a "sandwich layer" of "upstream price increases and downstream price pressures." Industrial chain profits are concentrated in upstream segments such as chips, with low added value in midstream manufacturing, making it difficult to share in the industry's high-growth dividends.

Of course, ZTE also has its own advantages. The company has a deep presence in the ICT industry, with its core communication products ranking second globally, mature customer resources, and global channels, giving it strong risk resistance. Under the "connectivity + computing power" strategy, the company possesses rare full-stack self-research capabilities, enabling software and hardware collaboration optimization. Additionally, leveraging the wave of localization, the company is deeply layout in domestic intelligent computing centers, meeting government and enterprise procurement needs. It has the growth ability to navigate industry downturns and improve efficiency and quality.

In the critical period of industry transformation from "connectivity" to "computing power," whether ZTE can break through technological bottlenecks and reshape its industrial chain status will determine whether it can stand firm in fierce competition. What will its future hold? We will continue to monitor.

-

Technology Innovation丨Domestic Native AGI Infra Hits RMB 700 Million Funding Record, Ushering in New Productivity Barriers for AI Infrastructure

-

![]()

Android 17 Update: Google Accelerates AI Implementation on Phones and Releases a High-End PC

-

![]()

DeepSeek Raises 50 Billion Yuan in Funding, but Liang Wenfeng Can't Escape Capital Game

-

![]()

Kuaishou’s Strategic Split: Let Kling Shine While Laotie Tills the Fields

-

![]()

Qianwen Teams Up with Taobao, Doubao Joins Forces with Douyin: Two Distinctive AI-Driven E-commerce Pathways Take Shape

-

Who can defeat DJI?

-

Xiaohongshu’s AI Gains Momentum, but Proceeds with Caution

-

![]()

ZTE: Achieved Scale but Lost Profits, 133.9 Billion Yuan in Revenue Yields Only 5.6 Billion Yuan in Profit