Chen Hang Initiates 'Integration of DingTalk and Wukong': DingTalk Once Again Takes a Backseat

05/17 2026

05/17 2026

476

476

The walk from Building 9 to Building 5 at Haizhi Tower takes no more than five minutes, but Wu Zhao took four years to make this journey.

When Wu Zhao left Alibaba in 2021, the external consensus was that he was unwilling to let DingTalk sacrifice its independence for the 'Cloud-Ding Integration' strategy. DingTalk's mission was to serve small and medium-sized enterprises, while the group required it to serve as a customer acquisition tool for other businesses—two fundamentally conflicting objectives.

Over these four years, Alibaba's AI ledger has advanced to another stage. According to financial reports and management disclosures, Alibaba's annualized recurring revenue (ARR) from AI-related products has surpassed RMB 35.8 billion. The narrower MaaS business is also rapidly growing, with ARR reaching RMB 8 billion, expected to hit RMB 10 billion in June and target RMB 30 billion by year-end.

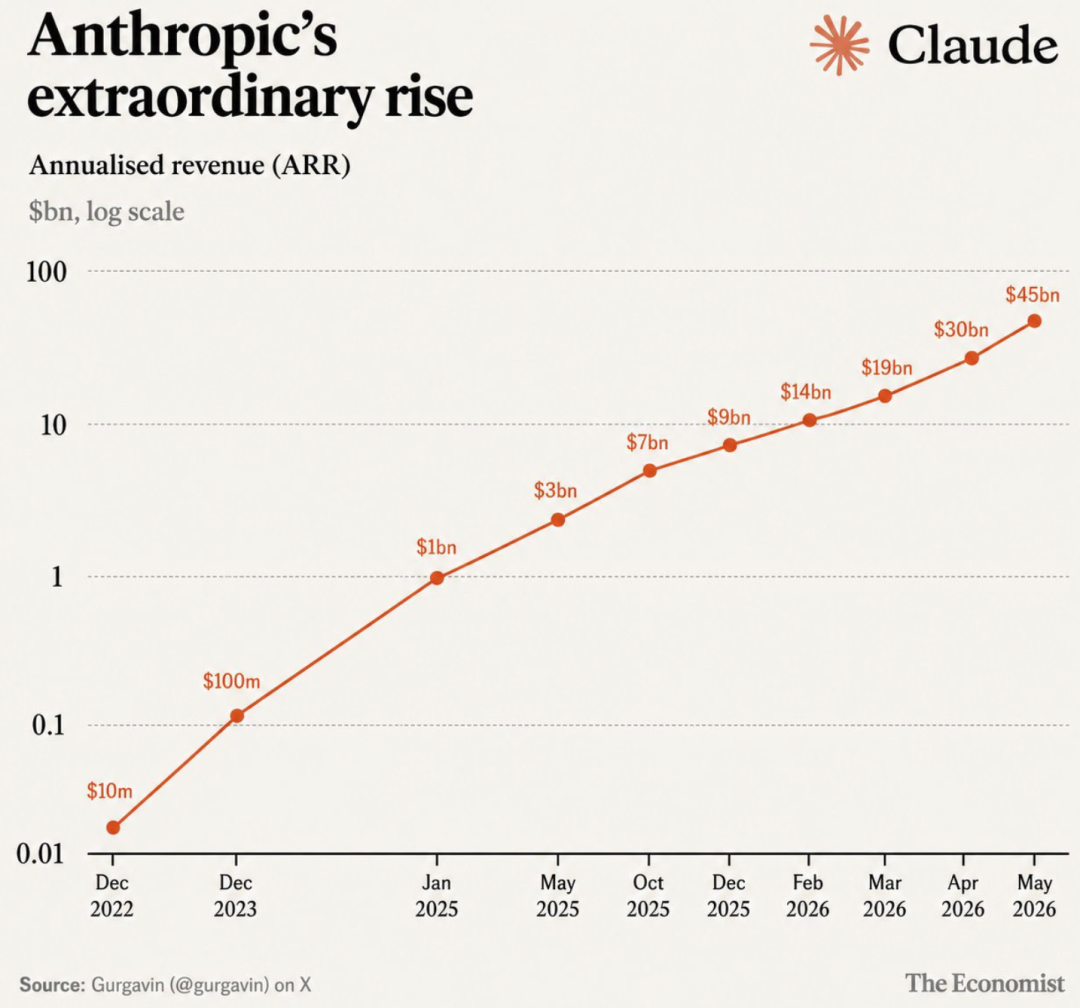

Wu Yongming even offered a more optimistic outlook during the earnings call: 'It should surpass RMB 30 billion in ARR earlier than year-end.' RMB 30 billion, approximately USD 4.4 billion, is comparable to the ARR level of the high-flying AI model company Anthropic as of July last year.

A year after returning to Alibaba, Wu Zhao undertook something even more radical than 'Cloud-Ding Integration.' On March 16, Alibaba announced the establishment of the ATH Business Group; the following day, the B-end-focused AI-native work platform 'Wukong' was officially unveiled at a launch event. Chen Hang stated on stage: 'Today, we shatter DingTalk and rebuild it with AI, forging Wukong.' Wu Yongming sat in the front row, listening from start to finish.

The DingTalk crafted by Chen Hang underwent a systematic self-demotion in the face of Wukong. DingTalk's underlying code was entirely rewritten, its graphical interface replaced by a command-line interface, and the product narrative shifted from DingTalk to Wukong. The boundary he once refused to cross was now effortlessly erased.

This is not difficult to understand. Previously, DingTalk's adjustments stemmed from a larger organizational logic: it needed to be redefined and prove its value within someone else's framework. This time is different. On the surface, the new direction also requires DingTalk to take a step back, but upon closer inspection, it resembles a redivision of labor toward the same goal.

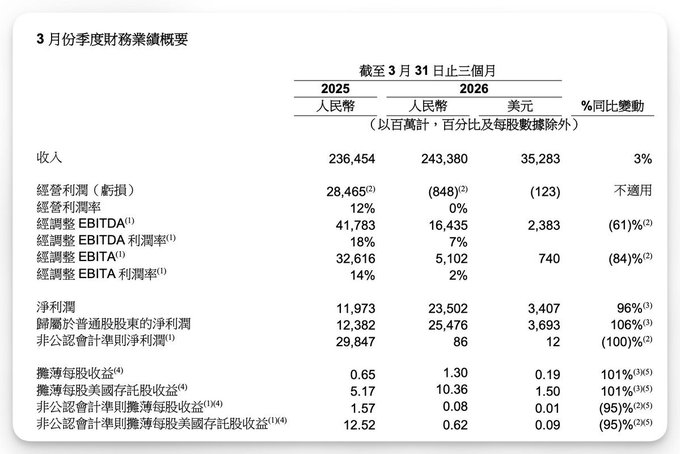

This is also the key to understanding DingTalk's current situation. On May 13, Alibaba released its Q4 financial report for FY2026, declaring—in more certain terms than ever—that AI has entered a 'cycle of large-scale commercial returns.' AI-related product revenue for the quarter reached RMB 8.971 billion, with external cloud commercialization revenue growing 40% year-on-year, surpassing an annualized scale of RMB 35.8 billion. Nearly a decade after the establishment of DAMO Academy, Alibaba's AI investments are beginning to pay off.

The sustainability of these returns hinges on a specific question: who is responsible for creating high-frequency, authentic enterprise-level AI usage scenarios? In the B-end market, the answer undoubtedly lies with DingTalk and Wukong. Yet, the financial report's earnings call offered no corresponding independent figures for 'the answer being DingTalk.'

AI's ledger must be settled by Wukong.

In 2017, Alibaba established DAMO Academy, announcing a RMB 100 billion investment over three years across ten fields, including AI, quantum computing, and chip design. At the time, AI was seen by most companies as a distant promise. Over the next five years, much of this funding was allocated to foundational research and cloud infrastructure.

With the advent of the large model era, the pace accelerated sharply: capital expenditures reached RMB 86 billion in FY2025, nearly tripling the RMB 32.1 billion of the previous fiscal year. Subsequently, Wu Yongming announced an additional RMB 380 billion in investment over the next three years—exceeding the total investment in related fields over the past decade.

In Q4 FY2026, investment intensity continued: quarterly capital expenditures reached RMB 26.887 billion, up 9.24% year-on-year, with RMB 26.588 billion allocated to property and equipment, primarily for GPU server procurement, data center construction, and self-developed chip investments.

Wu Yongming explicitly stated during the latest earnings call that AI infrastructure investment over the next five years will far exceed the previously promised RMB 380 billion, with Alibaba's data center scale expected to grow 'basically tenfold' compared to 2022. This reflects a pragmatic assessment of supply and demand: internal computing resources at Alibaba Cloud are strained, with Wu Yongming straightforward (bluntly stating), 'There is hardly an idle card in our servers.'

Nearly a decade has passed since DAMO Academy's first budget to this quarter's nearly RMB 9 billion in AI-related revenue. This time, Alibaba confidently declared that AI has entered a cycle of large-scale commercial returns. Whether these returns can sustain depends on a critical question: at which layer of the AI commercialization chain does revenue growth truly plateau?

Financial reports show that external cloud commercialization revenue grew 40% year-on-year in Q4, with Gartner reporting that Alibaba Cloud maintained its lead in China's IaaS market, increasing its share to 32.8%. However, cloud revenue comes from computing power and services, model revenue from API calls, and MaaS platform revenue from developers and enterprise applications. The common prerequisite for all three revenue streams is the continuous generation of token consumption through sufficiently numerous and high-frequency enterprise-level AI usage scenarios. Relying solely on selling APIs to developers cannot guarantee sustained enterprise payment behavior.

When AI-to-B target customers expand from developers writing code to employees using DingTalk for approvals, reimbursements, and attendance management, product delivery methods must change: AI capabilities must be triggered within existing enterprise workflows rather than requiring enterprises to adapt to a new tool. This is the logic of 'gateway value'—high-frequency enterprise AI usage depends on embedding into existing workflows rather than starting from scratch.

DingTalk's value in this structure manifests in two dimensions. First, it has scale: according to official public data, DingTalk serves over 20 million enterprise and organizational users, processing over 1 billion messages daily across high-frequency work scenarios such as approval workflows, reporting structures, attendance, and document collaboration. Second, it has depth: DingTalk has accumulated organizational structure data in government agencies, public institutions, and small-to-medium manufacturing enterprises, with approval hierarchies, reporting relationships, and project ownership serving as the skeletal data of organizational operations.

In internal collaboration scenarios at large private enterprises, competition among WeCom, Feishu, and DingTalk is fierce; however, in sectors with more complex organizational structures and heavier processes, such as government affairs and small-to-medium manufacturing, DingTalk's years of accumulated organizational data and approval chains constitute a harder-to-migrate advantage.

If Wukong can truly operate, Alibaba's B-end commercialization closed loop (closed loop) would function as follows: enterprise users initiate tasks on DingTalk, Wukong invokes Skills and models for execution, models run on Alibaba Cloud, token consumption contributes to MaaS and cloud revenue, and results are written back to enterprise workflows. This path offers greater imagination than merely selling cloud services. Technically, this chain is partially connected—DingTalk has integrated the Wukong Agent, and Q4 financial reports show an eightfold year-on-year increase in clients for the Bailian MaaS platform in March 2026.

However, the final link remains open. The Skill ecosystem is currently in invite-only testing, with 'large-scale adoption' lacking quantitative support in official statements. In a Wukong beta test case involving an auto repair shop, the owner paid RMB 5,000 monthly for approximately 100 new customers. While this represents a technically verifiable business model, it remains far from reaching the scale reported in financial narratives.

Two hurdles stand between individual paid cases and disclosable scale: first, whether the Skill ecosystem can effectively cover sufficient industry scenarios; second, the budgeting cycle for enterprise AI expenditures, or how long it takes for trial costs to become fixed operational expenses. No public data exists for these variables, making them uncertainties in the closed-loop narrative.

The Q4 financial report answers whether 'AI can generate revenue.' What DingTalk must answer is whether 'this revenue can be sustained.' However, this question was not explicitly raised during the earnings call. A more practical reason may be that Alibaba has not yet clearly delineated revenue responsibilities between DingTalk and Wukong in external narratives: questions about gateways, products, and commercialization remain difficult to frame stably for outsiders.

After Wu Zhao Shatters DingTalk

In 2026, Wu Zhao finally accomplished—in a manner he approves—what he refused to accept in 2021. The outcome appears similar: DingTalk is once again incorporated into a larger strategic framework. However, the true change lies not in how much DingTalk concedes but in where the value flows afterward. The beneficiary of 'Cloud-Ding Integration' was Zhang Jianfeng and Alibaba Cloud; this time, it is Chen Hang's own Wukong.

The original 2021 decision, 'Cloud-Ding Integration,' aimed to have DingTalk acquire enterprise clients and boost cloud revenue for Alibaba Cloud. Post-event analyses by media outlets such as 36Kr and Southern Metropolis Daily attributed this to the same cause: DingTalk served small-and-medium enterprises, while the group tasked it with targeting large clients and serving as a customer acquisition funnel—two objectives misaligned at the execution level. Chen Hang chose to depart and founded Hydrogen and Oxygen.

A frequently overlooked detail is that Hydrogen and Oxygen's office is in Building 9 of Haizhi Tower, while DingTalk is in Building 5—just a street apart. During Chen Hang's entrepreneurship, one of the investors was Yuanjing Capital, founded by Wu Yongming, who had recruited Chen Hang from Japan to Alibaba in 2010. After leaving DingTalk, Chen Hang's ties to Alibaba's core leadership remained intact.

In early 2025, Alibaba Group proposed acquiring investor stakes in Hydrogen and Oxygen, and Chen Hang subsequently returned as CEO of DingTalk, with former CEO Ye Jun reassigned elsewhere. Prior to this, Wu Yongming had already named DingTalk as one of the group's most critical To B AI application assets during an earnings call.

Wu Zhao's original plan after returning was to spend a year thoroughly reconstructing DingTalk with AI. According to a March report by Guixingren, 70% of Wukong's current form was already finalized by April or May of the previous year. When OpenClaw surged in popularity, Wukong's framework had already been growing internally at DingTalk for over half a year. The sudden shift from 'Computer Use Agent' as a concept to mass-market demand accelerated Wukong's release by a full month.

OpenClaw disrupted the timeline but completed a market education phase before launch. Chen Hang stated at the launch event that seeing knowledge influencers hype OpenClaw daily felt 'irresponsible,' as Wukong aimed to address what OpenClaw lacked: permission management, data security, and auditability in enterprise environments.

To align with Wukong, DingTalk underwent a systematic transfer of agency in technical architecture, organizational positioning, and product narrative. Wu Zhao started from a technical judgment: if AI becomes the executor of work, DingTalk—designed for humans—must be transformed for AI use. This materialized as DingTalk CLI: reconstructing all enterprise-grade capabilities into command-line instructions callable by AI, including IM, documents, approvals, schedules, and business travel. With tens of thousands of CLI commands, AI can complete tasks that once required lengthy graphical interface operations by humans.

Chen Hang described this as 'not merely an interface wrapper but akin to establishing a Unix-like kernel control system.'

The graphical interface is where users perceive a product's existence. You know you're using DingTalk because you open the app and operate within it. After CLI conversion, users issue commands to Wukong, which invokes DingTalk's capabilities to complete tasks—users perceive Wukong. Wu Zhao later defined this shift: 'In the past, humans used DingTalk for work; in the future, AI will use DingTalk for work.' This is both a product manifesto and the concluding statement of DingTalk's narrative as an independent product.

This positioning was confirmed organizationally. On March 16, Alibaba established the ATH Business Group, incorporating the Qianwen and Wukong Business Units. Wukong was positioned to 'create a B-end AI application gateway and deeply integrate model capabilities into enterprise workflows.' DingTalk was not included in ATH but placed under the Wukong Business Unit, with 'DingTalk brand remaining independently operated' as the external statement. Wu Yongming personally oversaw ATH and attended the entire Wukong launch event. Decision-making authority for To B narratives resides with ATH, not DingTalk.

At the product level, Wukong simultaneously launched an AI capability marketplace, aiming to build the 'world's largest toB Skill marketplace.' Multi-platform connectivity is essential to achieve this goal, which does not prioritize protecting DingTalk's gateway status. Thus, Wukong supports integration with mainstream IM platforms like DingTalk, Slack, and WeChat. This 'platform-agnostic' design carries a risk: if Wukong's Skill ecosystem matures to operate efficiently on any IM platform, DingTalk's gateway value could shift from irreplaceable to optional.

Jiazi Guangnian concluded in its retrospective on 'Cloud-Ding Integration' that DingTalk's conversion efficiency in driving traffic to Alibaba Cloud consistently fell short of expectations.

The logic chain of 'enterprises using DingTalk first, then adopting Alibaba Cloud' never materialized in practice. While the problem's form has changed, its essence remains: can DingTalk maintain sufficient conversion efficiency when serving as a tool for another strategic objective?

When juxtaposing Wu Zhao's 2021 departure with today's reconstruction, at least one explanation emerges: what Chen Hang truly could not accept may not have been 'DingTalk being conceded' itself but whether he agreed with the objectives during that concession and whether he held decision-making power.

Epilogue

A DingTalk insider once explained the relationship to media in straightforward terms: 'DingTalk is the foundation; Wukong is the future.' Foundations, however, are often buried underground—unseen and forgotten unless problems arise.

DingTalk has over 20 million enterprise and organizational users, 800 million registered users, and an enterprise-level capability foundation accumulated over 11 years. This is a scale that no ToB product can easily replicate, and it is also the premise that Wukong can claim to be "enterprise-grade" from day one. In Alibaba's Q4 financial report, which prominently announced that AI has entered a commercial return cycle, analysts inquired about the growth rate of Qianwen's Annual Recurring Revenue (ARR), cloud profit margins, and the timeline for achieving break-even in instant retail. No one asked about DingTalk, nor did anyone inquire about Wukong's progress in scaling paid offerings. This silence is a natural outcome of role allocation.

When there is a structural misalignment between an organization's performance goals and the independent value of its product, personnel stability becomes a variable hanging over the narrative. According to Lei Feng Network, around 2019, under Yao Xing's framework of "academic influence and industrial output" at Tencent AI Lab, there was a prolonged tug-of-war between basic research and industrial implementation. The priority of directions was repeatedly adjusted with changes in leadership, eventually leading to a prolonged period of instability after Yao Xing's departure.

The tension within DingTalk lies between product independence and platform dependency. Wu Zhao addressed this tension through "active choice," but such initiative can only delay the moment when the tension resurfaces. When the value of DingTalk as the foundation for Wukong cannot be quantitatively disclosed, and Wukong's platform expansion is not bounded by DingTalk, the issue of aligning interests between the two will inevitably resurface sooner or later.

In 2021, Chen Hang left Alibaba with the intention of protecting DingTalk and spent four years starting a business just a street away. In 2025, Wu Yongming invited him back, reasoning that DingTalk needed to be restructured in the AI era. Chen Hang accepted the offer, returned, and transformed DingTalk into his new product.

Over the past few years, Alibaba has repeatedly attempted to regain its growth narrative through organizational adjustments. The truly difficult part is often getting those who have already left the table to sit back down. Under Wu Yongming's leadership, Alibaba has not only regrown its business lines but also rebuilt some of its relational networks: Jack Ma's several public appearances provided a long-awaited sense of certainty internally, while individuals like Wu Zhao, who had previously left, have also reconnected their next narratives to Alibaba's ecosystem under Wu Yongming's influence.

"The integration of cloud and DingTalk" did not succeed, but "the integration of Wukong and DingTalk" is now underway.

Chen Hang once told a story at a product launch about digging bamboo: a bowl-thick bamboo stake took four people three to four hours to dig up because the real enormity lay in the underground network of rhizomes. He used this imagery to describe the future of DingTalk and Wukong. However, the nature of bamboo rhizomes is precisely that they do not grow in just one direction. The question that follows is: when this root system becomes strong enough, who will ultimately receive its nourishment?

Now, DingTalk has relinquished the spotlight on stage. That position has been left for Wukong—and for Wu Zhao himself.

*The featured image and illustrations in the text are sourced from the internet.

-

![]()

Ford and Geely Forge New Joint Venture in Spain, Sidestepping Changan and JMC

-

![]()

199 RMB! Godox's First Camera Review: Subpar Photography, Transparent Viewfinder Frame is the Highlight

-

![]()

AI Smartphones: A Modern-Day 'Emperor's New Clothes'?

-

![]()

Yonyou Network: A Company Selling 'Transformation' but Struggling in Its Own Transition

-

![]()

Focus | CCCC’s Takeover of Greentown Comes to Fruition: Why Did the 11-Year ‘Control Without Authority’ Era End?

-

![]()

Final Verdict: The 2026 China Auto Forum Shines with Unique Characteristics at a Pivotal Moment

-

![]()

Tencent Maintains Matrix Approach, Alibaba Merges Entry Points: Tech Titans Initiate AI Agent Consolidation

-

![]()

Geely Secures Portion of Ford’s Spanish Production Capacity