Baidu: Nothing Else to Rely On but Kunlunxin

05/19 2026

05/19 2026

406

406

Baidu's Q1 performance was a mixed bag, reflecting significant recent strategic adjustments and business pivots. However, compared to its already struggling advertising business, the key focus for investors is whether Baidu's growth narratives—AI cloud, Kunlunxin, and share buybacks—are unfolding smoothly.

Last quarter, Baidu formally adopted a new reporting structure, dividing results into 'AI Business' and 'Traditional Business.' AI Business includes AI Infrastructure (AI Infra), AI Applications (AI Application), and AI-native Marketing Services.

As most institutions still set expectations based on the old framework, Dolphin Research has merged the old and new frameworks to facilitate comparison while highlighting growth trends in Baidu's new AI business lines.

Detailed breakdown (Baidu Core only, excluding iQIYI):

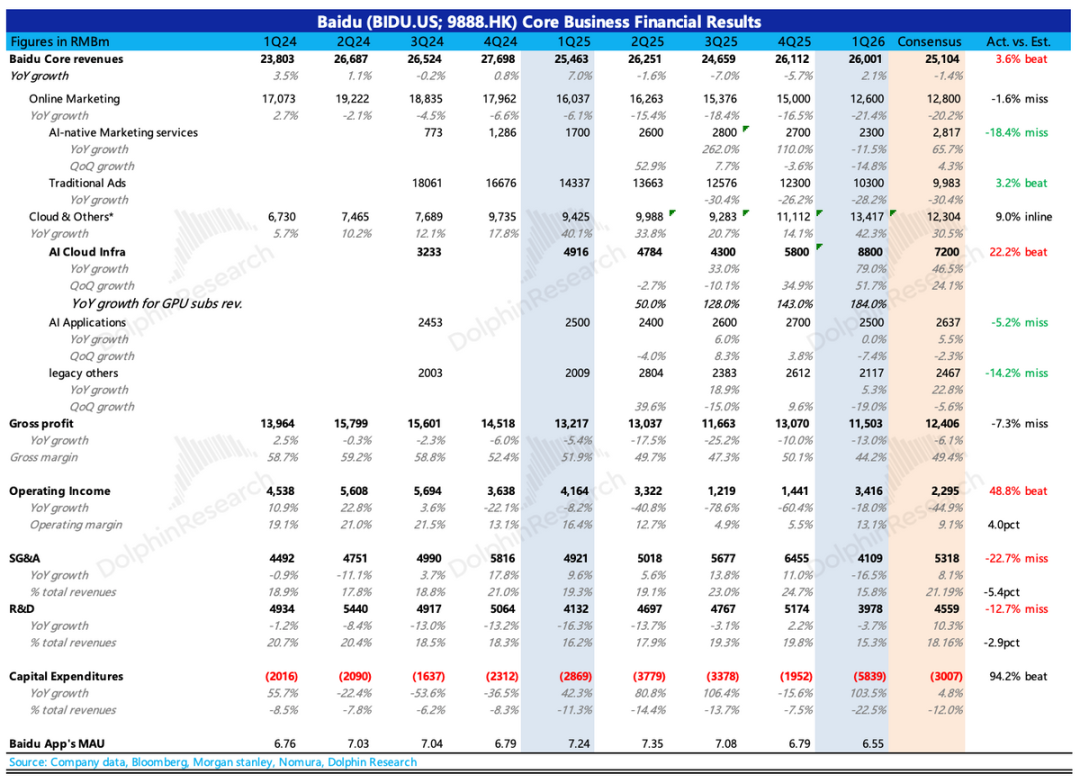

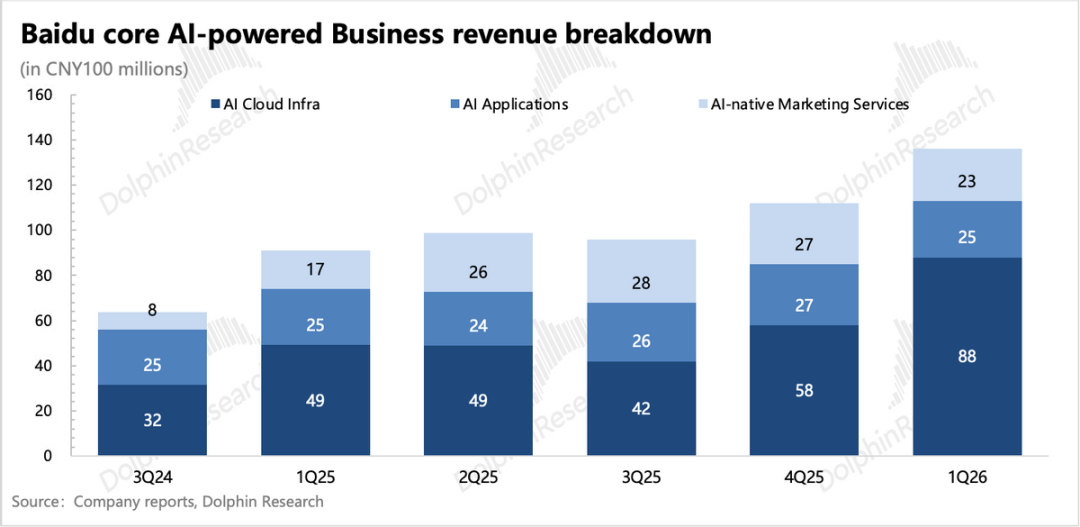

1. AI officially shoulders half the load: In Q1, AI-related revenue reached RMB 13.6 billion, accounting for 52% of total revenue, up from 43% in Q4. Key drivers include:

(1) AI Cloud Infrastructure (including cloud services, large model APIs, and computing power leasing) as the true 'backbone': Revenue hit RMB 8.8 billion, two-thirds of AI business revenue, up 79% YoY, exceeding market expectations. GPU cloud revenue surged 183%, driving AI cloud's high growth.

(2) AI Applications (including Baidu Wenku, Baidu Netdisk, and digital employee products): Trends worsened from last quarter, with a sequential decline. Excluding the drag from Netdisk and other services, growth in pure AI applications (e.g., digital employees) also slowed, mismatched with industry sentiment, raising concerns about intensifying competition.

(3) AI-native Marketing (Agents and digital humans): Continued sequential weakness, likely due to the same competitive pressures faced by digital employee products.

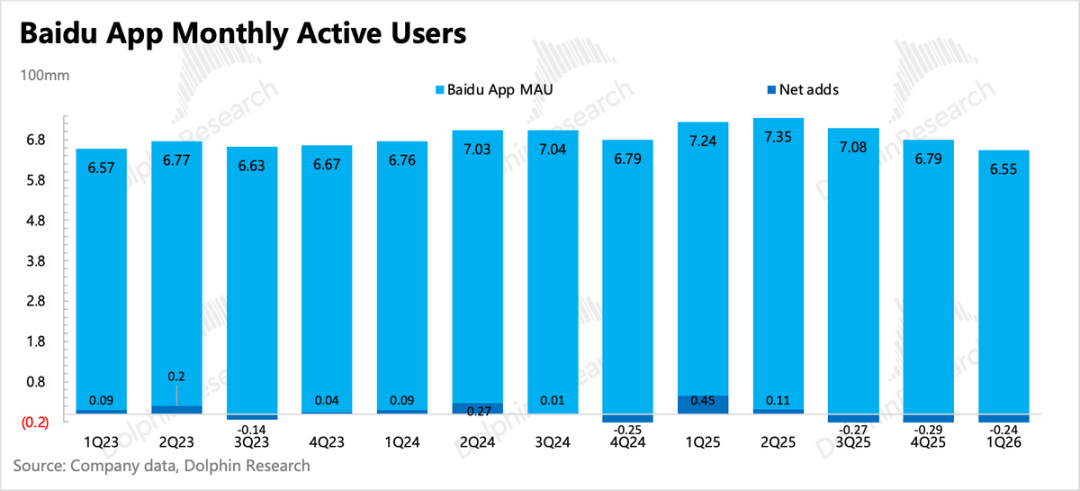

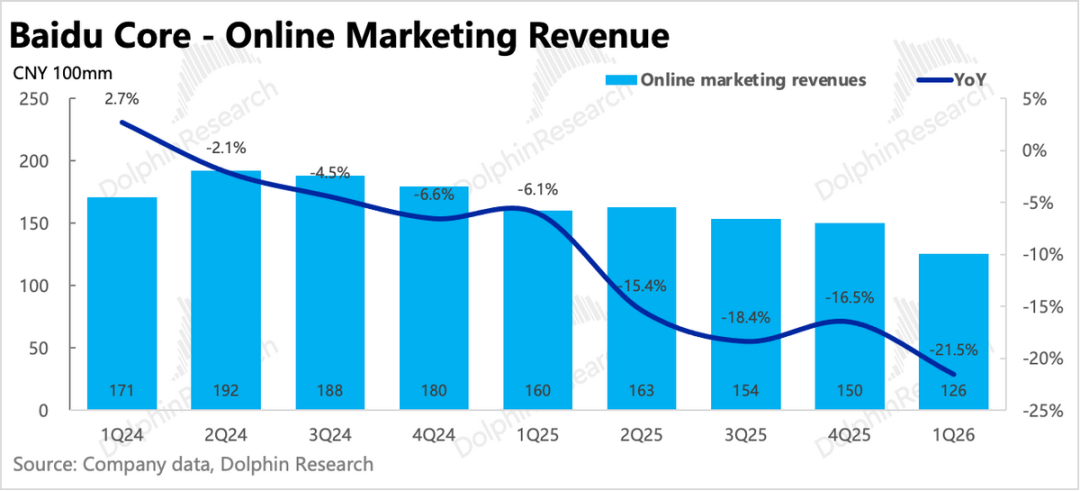

2. Traditional advertising 'hits rock bottom': Split-out traditional advertising (search, feed ads, etc.) fell 28% YoY, worsening from Q4's 26% decline. While Q1 was affected by the Lunar New Year timing shift, broader industry weakness and Baidu's declining competitiveness (MAUs fell 22 million QoQ) make a turnaround unlikely soon.

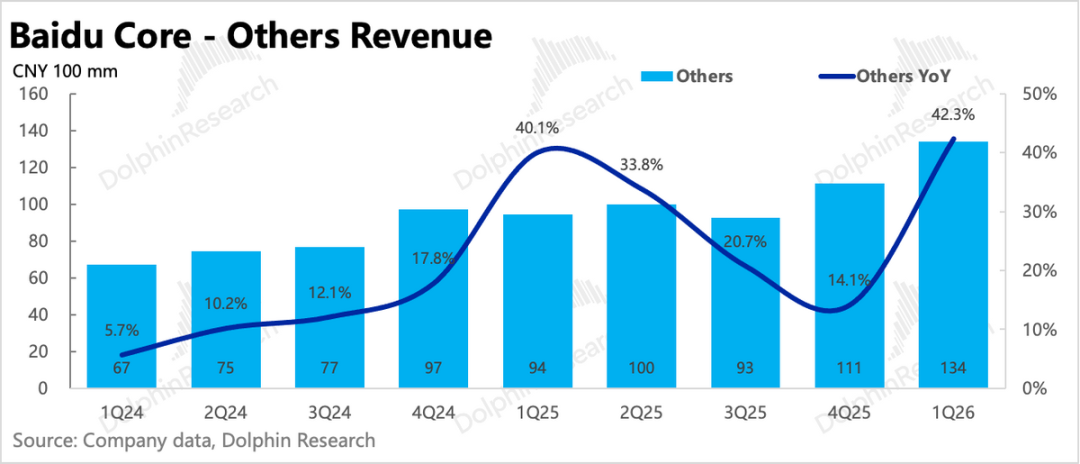

3. Autonomous driving, smart hardware, and others: Revenue from this segment reached RMB 2.1 billion, down sequentially. Autonomous driving orders hit 3.2 million, up 120% YoY.

Due to mainland China's autonomous driving regulatory impacts, Apollo has focused on international expansion since H2 2023. After tests in the Middle East, UK, and South Korea, it recently advanced road testing in Switzerland. The Middle East is progressing fastest, with Dubai operations launched and the Luobo Kuaipao app going live in March.

Apollo now covers 27 cities globally, with potential for future spin-offs and capitalization.

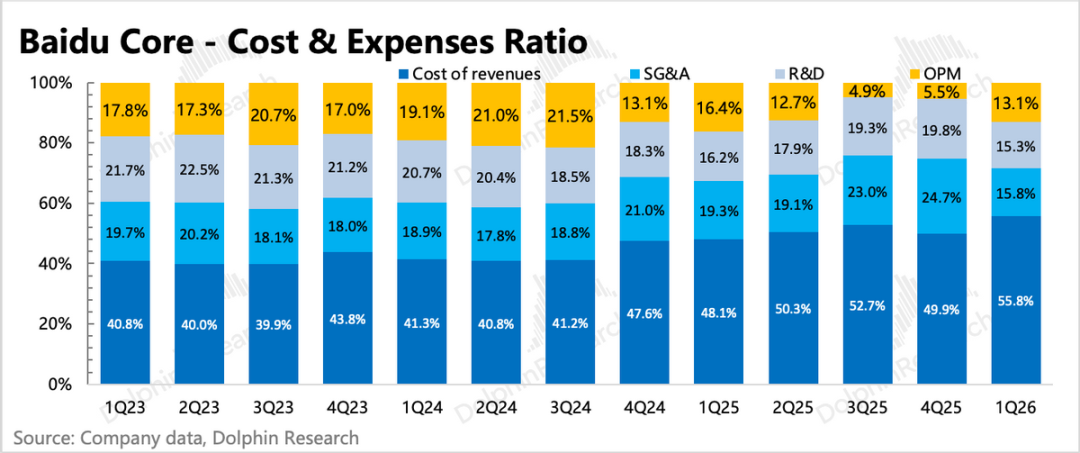

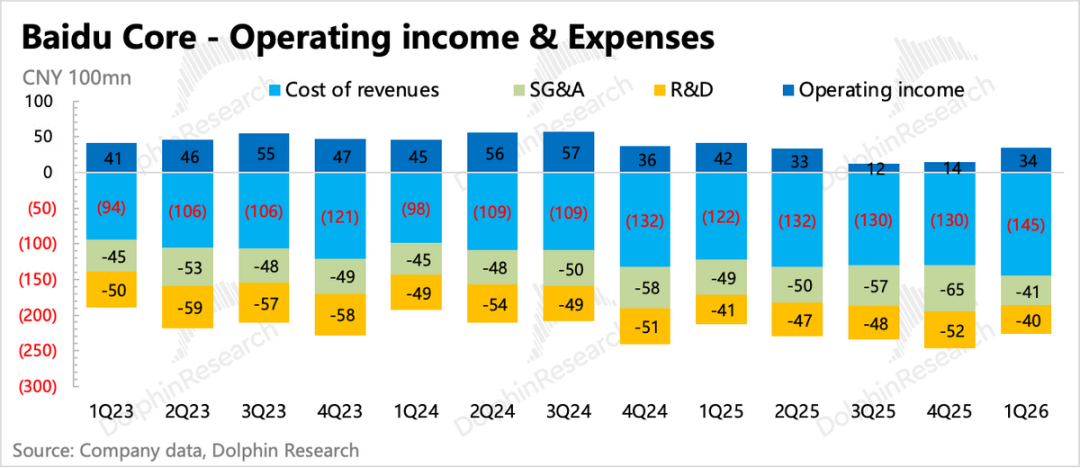

4. Cost reductions and strategic pivot: Last quarter's significant headcount optimizations (nearly RMB 700 million in severance) led to a 10% Q1 operating expense contraction, with expenses as a share of revenue dropping from 45% in Q4 to 31%.

SBC (stock-based compensation) also declined, with Q1 equity incentive expenses down 24% YoY. Despite Baidu's higher market cap in Q1 2024 vs. Q1 2023, this reflects a sharp reduction in incentive recipients.

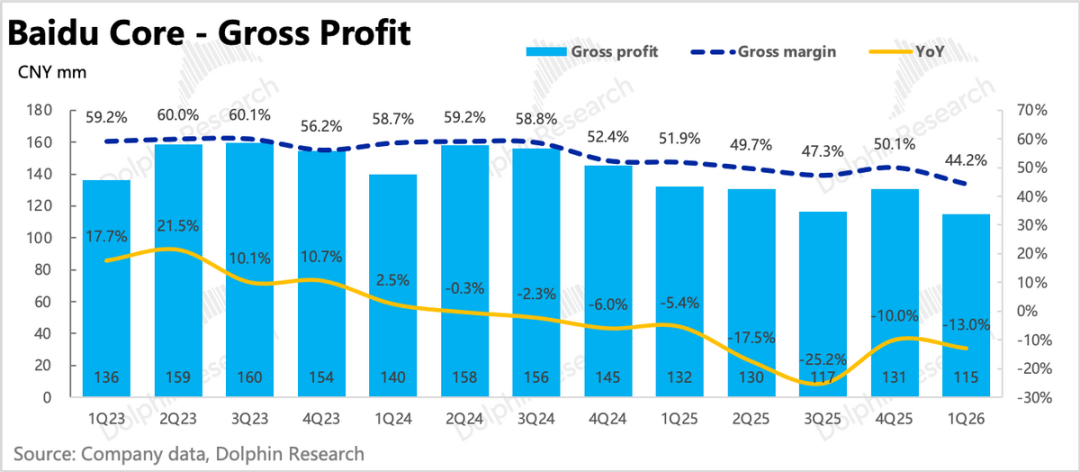

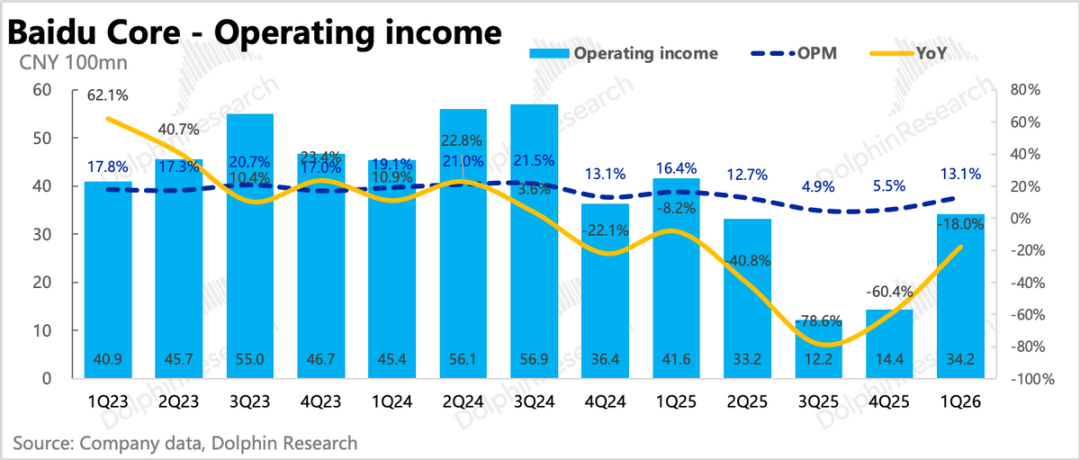

Despite a steep decline in high-margin advertising revenue, operating profit improved sequentially but remained lower YoY. However, costs were cut more aggressively than expected.

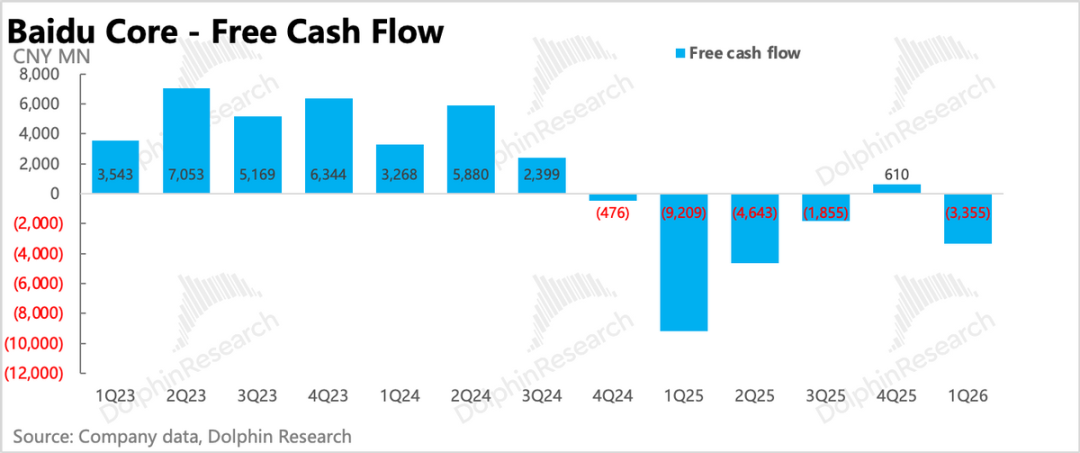

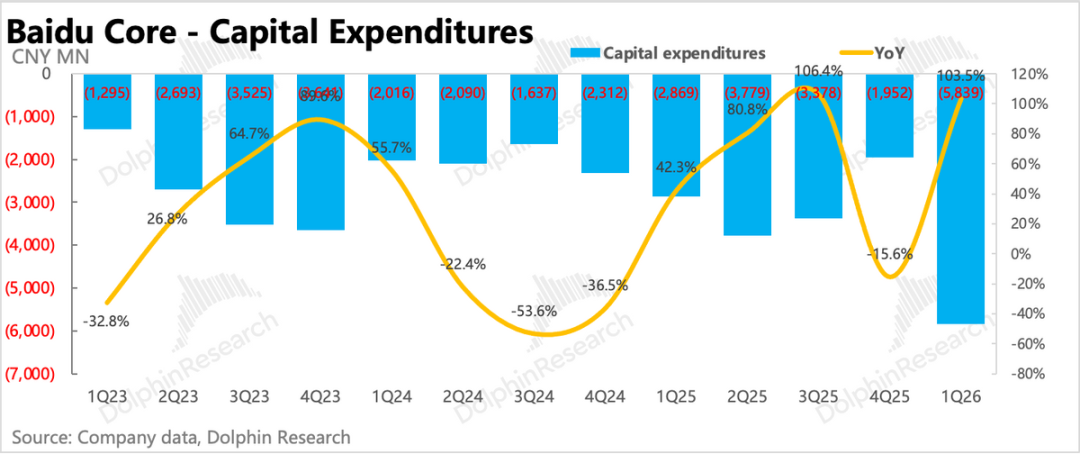

5. Increased CapEx and buybacks proceed as planned: Q1 CapEx nearly doubled YoY to RMB 5.8 billion, still low compared to peers scaling large models and cloud businesses. AI Infra revenue (RMB 8.8 billion) fully covers these expenditures.

The RMB 5 billion two-year buyback plan announced in February saw RMB 172 million in repurchases in Q1 (one month), slightly behind schedule. Management's emphasis on shareholder returns is higher than before, and Baidu's net cash (RMB ~100 billion after short-term debt) supports buybacks and CapEx for the next two years.

Current shareholder yield stands at 5-6%. Excluding dividends, if buybacks proceed at the RMB 2.5 billion annual cap, that's 5.4% of the current RMB 46 billion market cap.

6. Kunlunxin's IPO nears: In early May, Kunlunxin filed for IPO Tutoring registration (pre-IPO counseling registration). Assuming a typical Hong Kong listing timeline, the IPO could occur in July-August. As domestic computing power remains a high-conviction sector, Kunlunxin's listing may catalyze Baidu's valuation in the short term.

7. Financial snapshot

Dolphin Research's View

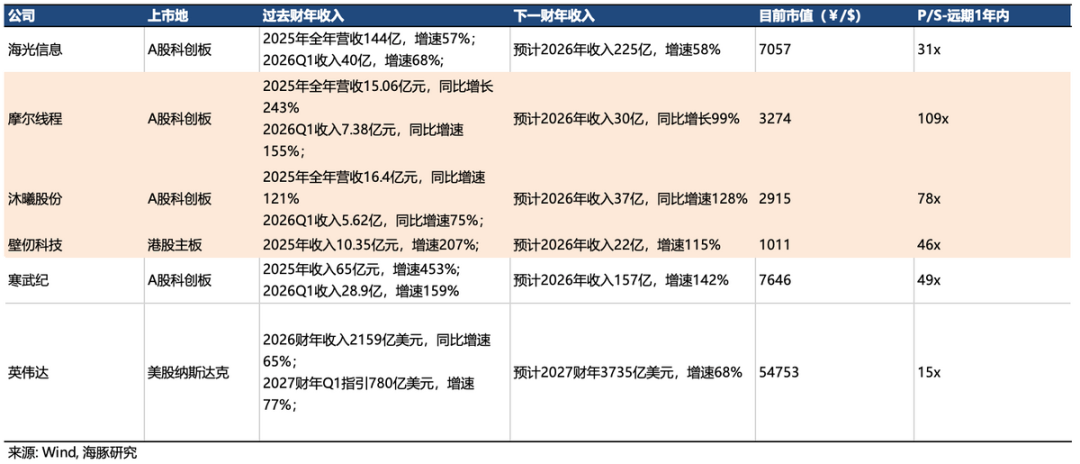

Baidu's immediate growth driver is AI cloud, including large model APIs, computing leasing, and underlying Kunlunxin chips. The sector remains highly buoyant, benefiting all players regardless of product differentiation. Among these, Kunlunxin is the most competitive and promising asset.

What is Kunlunxin worth? In our January note, *Kunlunxin's Accelerated IPO: Baidu's 'Google Moment'?* (see Longbridge App), we estimated:

(1) Financial performance remains largely unchanged, but combining market expectations and channel checks (institutions expect RMB 6-7 billion), our original RMB 8.4 billion revenue forecast may be optimistic. Risks include potential Samsung capacity constraints and post-H2 2024 industry competition leading to price pressure due to performance gaps.

(2) Compared to listed Chinese GPU leaders ('Four Little Dragons'), a 15x P/S valuation appears conservative. While Kunlunxin uses ASIC technology (differing from GPGPU architectures), customer priorities—performance, stability, and price—demand cross-chip benchmarking.

Kunlunxin's R&D capabilities and supply chain resilience are on par with peers, with substantial HBM inventory to support shipments. Current orders come from Baidu (in-house use), Tencent, China Mobile, Geely, State Grid, and CMB. With a sharper focus on AI cloud, Kunlunxin is well-positioned to capture industry tailwinds.

That said, Baidu's valuation increasingly hinges on Kunlunxin's progress. Without milestones or positive news, the stock may drift, pulled back by traditional business logic.

For detailed analysis, see our Same name article (same-titled article) in the Longbridge App's 'Insights - Deep Dive' section.

However, we believe this justifies a premium over peers: Luobo Kuaipao should only be included after a spin-off announcement; iQIYI's damaged fundamentals and volatile equity value make it suitable only for optimistic scenarios; and including all net cash is unreasonable—we cap it at RMB 5 billion (buyback plan) + 5-6% shareholder yield.

While Kunlunxin's early listing (mirroring the 'Four Dragons') could see a short-term rally if market sentiment holds (or Baidu pursues a dual-primary listing), timing is crucial.

Detailed Analysis Below

I. Business Structure

Baidu uniquely splits financials into:

1. Baidu Core: Traditional advertising (search/feed ads), innovative businesses (smart cloud/DuerOS/Apollo), and AI-related revenue (AI Infra, AI Applications, AI-native Marketing).

2. iQIYI: Memberships, advertising, and content licensing.

The split is clear-cut, and as iQIYI is independently listed with detailed disclosures, we analyze both segments separately. Due to ~1% (RMB 200-400 million) in intersegment eliminations, our Baidu Core breakdown may slightly differ from reported figures but does not affect trend analysis.

II. AI Contribution Rises to 52%

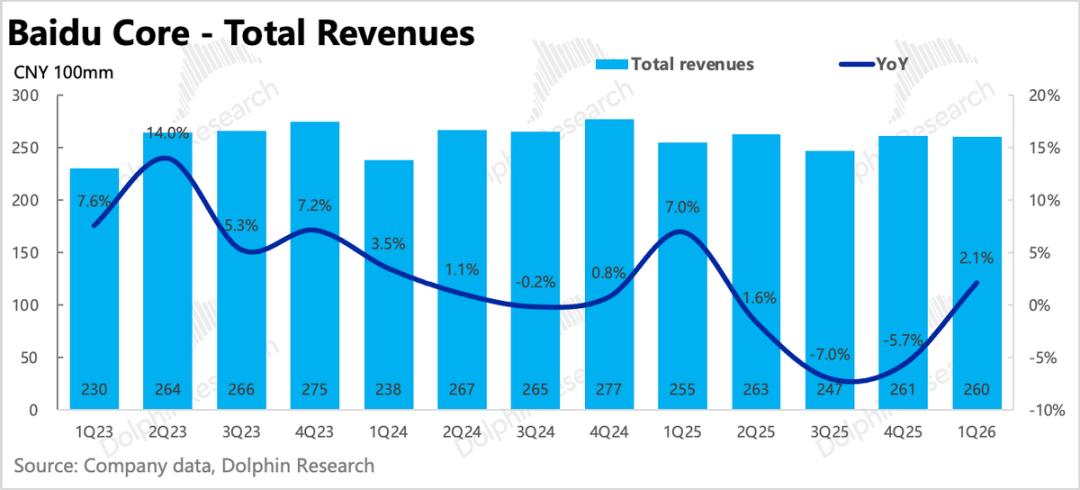

Baidu Core revenue hit RMB 26 billion (+2% YoY), with AI offsetting traditional business declines.

(1) AI Business

Despite three sub-segments, AI Cloud Infrastructure is now the clear pillar, with GPU cloud revenue as the key driver. Demand remains strong for computing power, and Baidu Cloud's full-stack AI and integrated hardware-software capabilities are relatively scarce.

However, AI applications derived from large models appear to have hit a bottleneck. Sequentially, AI applications (Wenku, Netdisk, digital employees) and AI-native ads (Agents, digital humans) flattened.

(2) Traditional Business

Little to say here—the market expects no near-term turnaround, and funds have low expectations. Baidu's MAUs declined in the AI portal wars, even during peak season.

Reverting to the old disclosure framework for comparison:

(1) Advertising: Down 21.5% YoY, with traditional ads falling 28%. The Lunar New Year timing shift contributed, but pressures persist.

(2) Cloud and Other Revenue: Up 42% YoY on a high base, exceeding expectations.

III. Higher CapEx Amid Headcount Optimization

Baidu underwent major organizational changes late last year, integrating traditional businesses, boosting efficiency, and segmenting AI businesses under dedicated teams. Adjustments peaked last quarter, with results visible this quarter.

(1) Core gross margin fell to 44% as advertising pressures offset AI cloud growth.

(2) Core operating profit hit RMB 3.4 billion (13% margin), reflecting layoff effects. Sales & marketing and R&D expenses fell 17% and 4%, respectively.

IV. CapEx Expansion Still Has Room

Q1 free cash flow turned negative due to surging CapEx (up nearly 100% YoY to RMB 5.8 billion). However, this remains low versus peers scaling large models and cloud businesses. AI Infra revenue (RMB 8.8 billion) fully covers CapEx.

Baidu's full-stack AI and in-house chips provide cost advantages, but matching industry growth requires aggressive investment, which its cash reserves support.

- END -

// Reposting for Whitelisting

This article is an original piece from Dolphin Research. Reposting requires authorization.

// Disclaimer and General Disclosure Notice

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or particular needs of any individual receiving this report. Investors must consult with an independent professional advisor before making any investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibility or loss that may arise from the use of the data contained in this report. The information and data contained in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or views expressed in this report shall not, under any jurisdiction, be considered or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall it constitute advice, a quotation, or a recommendation regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability, or use would be contrary to applicable laws or regulations or would subject Dolphin Research and/or its affiliates or associated companies to any registration or licensing requirements within such jurisdiction.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to any other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Focus | CCCC’s Takeover of Greentown Comes to Fruition: Why Did the 11-Year ‘Control Without Authority’ Era End?

-

![]()

Final Verdict: The 2026 China Auto Forum Shines with Unique Characteristics at a Pivotal Moment

-

![]()

Tencent Maintains Matrix Approach, Alibaba Merges Entry Points: Tech Titans Initiate AI Agent Consolidation

-

![]()

Geely Secures Portion of Ford’s Spanish Production Capacity

-

![]()

Tesla Stalls This Second

-

![]()

Elon Musk's 'Money-Burning' Spree: All Car Sales Profits Poured into AI

-

![]()

Why Did Tesla’s Profits Drop and Cash Flow Go Negative?

-

![]()

AI Titans Are All in the Red: Time for Intelligent Driving Car Buyers to Reassess?