Joint Venture Electric Vehicles: Stuck at the 150,000 Yuan Mark?

05/19 2026

05/19 2026

462

462

Introduction

Introduction

With the erosion of brand premium, can joint venture brands still craft compelling new narratives in China's premium market?

After years of development, the overall landscape of the Chinese auto market has been turned upside down, ushering in a complete reconstruction. The collective rise of Chinese brands has not only led to a rapid increase in market share, rapid evolution of the new energy industry, and a value reconstruction that far exceeds market transformation expectations, but it has also compelled once-dominant foreign automakers to learn from us and systematically understand how to navigate the new era.

During this phase, Chinese cars are indeed becoming more expensive. Interestingly, thanks to technological advancements and the high value proposition of the products themselves, a new generation of consumers has set aside their prejudices and is increasingly becoming enthusiastic supporters. In just two years, emerging Chinese auto brands such as Xiaomi, Huawei's "Five Realms," and the NIO ecosystem have demonstrated the potential to surpass BBA (BMW, Mercedes-Benz, Audi).

Faced with this situation, joint venture automakers, under pressure from all sides, are well aware that inaction could make survival a daunting challenge.

Since the beginning of last year, Toyota and Nissan have launched an Electrification 2.0 offensive, making significant moves in the Chinese market. The introduction of localized new models such as the bZ3X and N7 has indeed showcased the joint ventures' unwillingness to remain stagnant.

As we enter 2026, with General Motors and Volkswagen also stepping up their game, aiming to regain market influence from Chinese automakers, we can increasingly sense the determination of joint venture brands to avoid being marginalized.

But does effort necessarily guarantee corresponding rewards? Compared to the golden years of the past, given the current market situation, it's not just that Chinese brands have completely dominated the direction of the Chinese auto market's development; on a broader trend, Chinese users' trust in Chinese brands has reached an unprecedented level.

When the scenario of "high-priced Chinese cars selling well for an extended period" is not just a flash in the pan but truly poses a crisis for other market participants, it signifies that the filter (aura) surrounding joint venture brands has not only been shattered by reality but, in many cases, they no longer enjoy brand premium in most market segments.

In today's context of soaring fuel prices, the notion that "pure electric is the future" is no longer an ambiguous proposition. Regardless of consumer attitudes toward joint ventures or their own assessments of the era's development, abandoning past status and seeking breakthroughs amidst the onslaught of Chinese brands seem to be the critical options for overseas giants to survive in China.

01 Ideals Clash with Reality

Several months into 2026, numerous events indicate that joint venture automakers have already played their trump cards in the process of electrification transformation. Volkswagen has unveiled several pure electric models, including the ID.ERA 9X, Shine 08/09, and ID.AURA T6, while BMW has introduced the new-generation iX3 and i3 to the domestic market. Nissan has launched the NX8, and Buick has introduced the Electra E7, among others...

Even for onlookers who may not favor the working styles of joint ventures, there's little to criticize about this series of moves.

However, the Chinese auto market has always been quick to change. As joint venture brands gradually regain their composure and face off against the now-lofty Chinese brands, their focus has shifted from "how to keep up with industry transformation" to the more fundamental question of "how to earn basic respect from new energy vehicle users."

In other words, as the end-user market clearly judges the development status of new and old forces and no longer evaluates each new model using traditional car-buying logic, it will not be easy for joint ventures to reclaim their original territory from Chinese automakers.

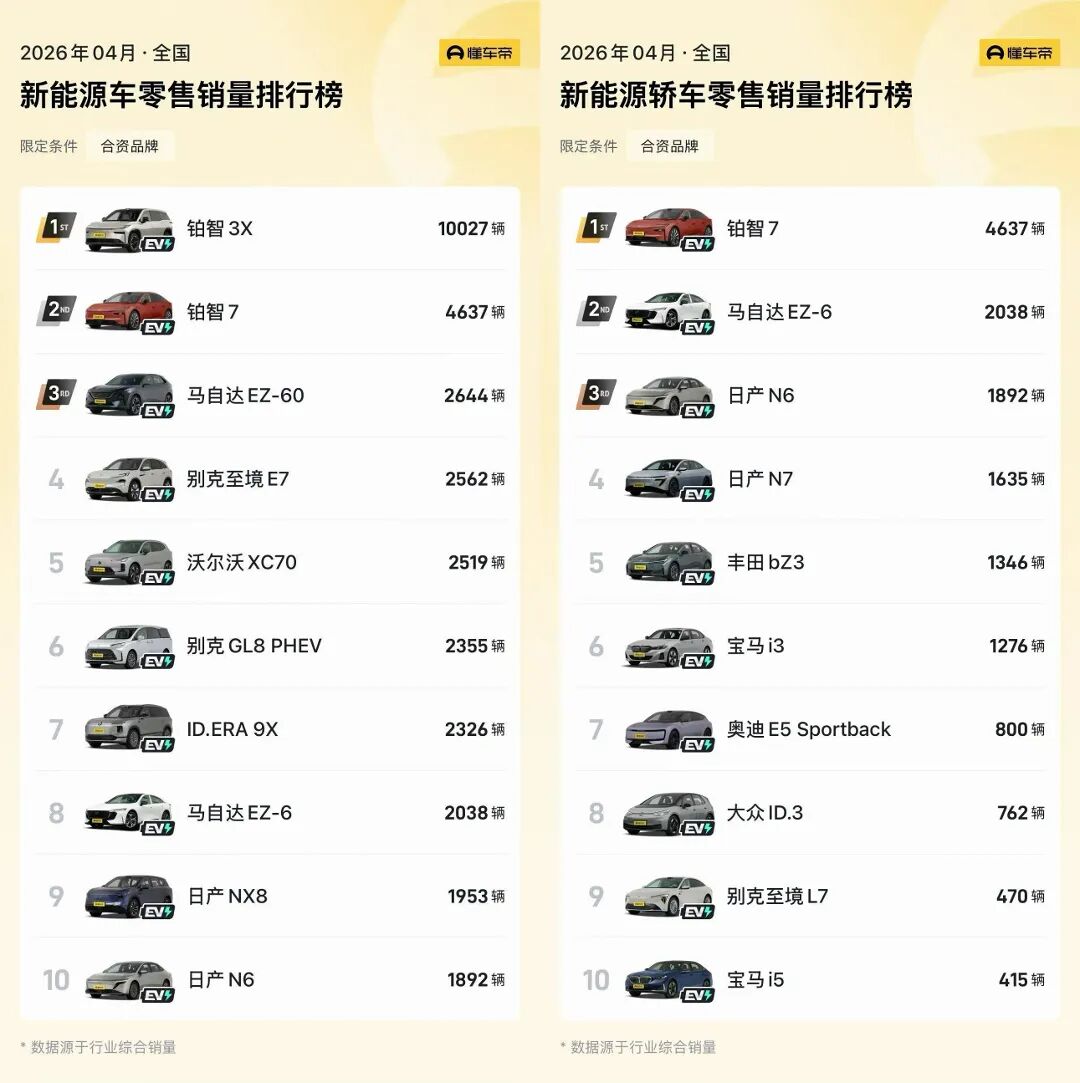

Over the past year, leveraging an absolutely localized R&D approach, joint venture new models like the bZ3X have enjoyed a period of high visibility, maintaining monthly sales of over 10,000 units and finally shedding the shadow of poor sales that plagued previous new models. However, it cannot be ignored that, except for the bZ3X, the freshness period of similar products has significantly shortened.

The Nissan N7 was launched less than half a year ago, and the N6 had to step in to save the day; the Buick Electra E5 has lost its momentum, with the Electra L7's monthly sales quickly dropping below a thousand units; the Mazda EZ-60 hovers around 2,000 units per month; the Honda P7/S7 are powerless to turn the tide; the Hyundai EO was a flop from the start; even the Mercedes-Benz pure electric CLA didn't sell well...

With abundant realities Placed in front of you (before us), to be honest, it's hard to say how much of an improvement the new round of awakening among joint ventures has brought about.

When the Beijing Auto Show in April concluded, everyone was saying that there were too many new models to remember, leading to increased consumer hesitation. But will the electric vehicle offensive from Chinese brands subside because of this? Obviously not.

The past two years have seen a large-scale influx of new models in the MPV market; last year was marked by a collective outbreak (outbreak) of mid-to-large SUV models; this year, the fires of competition in these segments have not died down, and niche markets like station wagons have also witnessed a surge of new models. Chinese automakers, each a "war god," are truly hard to resist.

Looking at monthly sales data, the numbers don't lie. Without any qualifiers, among the top performers in various pure electric vehicle market segments, except for Tesla, there are basically no joint venture models.

A couple of days ago, at the pre-sale launch of a new model from a joint venture luxury brand, corporate executives criticized the industry for some who use pure electric new models to set lap records for online attention, viewing the practice of achieving such records with specially tuned vehicles (changing tires, modifying suspensions, writing separate software) as a show detached from actual user experience.

From an industry standpoint, regardless of the facts, it's difficult to make an objective assessment of such criticism. However, from the perspective of continuous advancements in pure electric technology, the hysteria from joint venture automakers is unnecessary.

In this new era where cars are becoming increasingly linked to consumer electronics, while the reality of "business is war" remains unchanged, any maneuver that can make consumers willingly open their wallets is a subject worthy of scrutiny.

Today, as brands lose their former glory, every step taken by joint ventures must be based on maintaining corporate bottom line (bottom lines) while demonstrating product determination and strategic resolve on par with Chinese automakers.

Since last year, among all new energy vehicle models produced by joint venture automakers, has there been a single one that is just a filler or a transitional product detached from the needs of the times? I don't think so. But the problem is glaring: behind the lack of consumer recognition must lie a lack of clarity among joint venture companies during their transformation about their current position in the Chinese auto market.

02 Wrong Approaches Lead Nowhere

Just after May Day, reports of a sharp sales decline at GAC Honda flooded in. There were also those who pronounced a death sentence on the company's future. What could GAC Honda do in response?

Remaining silent was not an option; it couldn't just let outsiders speculate based on fragmented information. But actively responding didn't seem feasible either, as the reality of poor sales was like a steel nail (nail) locking down all attempts at explanation.

Ultimately, the Chinese market is that ruthless. A sales surge can trigger multi-faceted interpretations, let alone the Public opinion storm (public opinion backlash) that poor sales can bring.

The window of opportunity for joint ventures is narrowing, and time is running out. While this is undoubtedly true, the future market landscape has not yet been fully determined. As long as they adopt the right posture and attitude, opportunities always exist.

This year, we occasionally see GAC Toyota prominently displaying the sales performance of the bZ3X in its promotional materials. Its approach to product iteration cycles and updates adheres to a single principle: to fully align with Chinese brands. Price reductions are acceptable, configurations can be enhanced, and software can be frequently updated via OTA. Profitability and potential impacts on existing fuel-powered products are not its primary concerns.

As the pure electric era accelerates, we must be clear that for joint venture automakers, there is no brand premium. On the surface, everyone promotes product localization and technological adaptation as a sign of their heightened attention to the Chinese market. In reality, this is no longer within the realm of proactive change but a necessity for survival.

In the 100,000-yuan vehicle market segment, we never deny that due to ingrained perceptions in lower-tier markets or long-standing user reputations, models like the Sylphy and Lavida can still stand at the forefront of the market. Thus, as long as prices do not exceed those of competing models, whether for fuel-powered or electric vehicles, joint ventures can naturally gain consumer recognition.

In recent years, Chinese brands have long surpassed the 200,000-yuan price barrier, not relying on luck or timing but on remarkable product advancements. As this trend becomes irreversible and joint venture brands increasingly penetrate lower market segments, it reflects the exchange of market dominance. In the pure electric era, the 150,000-yuan mark has instead become a barrier for joint ventures to break through upwards.

In the mainstream new energy market above 150,000 yuan, where products abound, the competitiveness of joint venture new models is no longer a concern for consumers but a subject for automakers themselves to explore.

Like the bZ3X, GAC Toyota is highly attentive to the market feedback of the bZ7. While monthly sales of over 4,000 units may not be a remarkable achievement to boast about, in terms of understanding China's mid-to-high-end pure electric sedans, GAC Toyota should be pleased from top to bottom. Even without the Toyota logo, the bZ7 is a Chinese-style pure electric new model that meets the needs of potential users.

In contrast, whether in the pure electric sedan market dominated by the Tesla Model 3 and Xiaomi SU7 or the premium market filled with large-sized SUVs, finding another competitive new model in the joint venture product lineup seems challenging.

Either the price lacks appeal, the configurations are not class-leading, or the level of intelligence is not in the top tier. Without a unique advantage in all-around development, the final outcome can only be monthly sales hovering around a thousand units.",

-

![]()

Should Extra-Large New Energy Vehicles Go on a 'Diet'? A Proposal for a Special Consumption Tax

-

![]()

Outpacing JD.com, Tmall Youpin Ramps Up Offline Mega-Store Expansion This Year

-

![]()

Hundreds of Brands Struggle to Hit 10,000 Monthly Sales: Despite a Surge in Orders, Maintaining 10,000 Monthly Sales Remains Tough | MINGJINGpro

-

![]()

97.41 Billion RMB in Revenue, 6 Billion RMB Market: Insta360's Dilemma in Growth Limits

-

![]()

Xi'an 'Places Its Bets' on 2030: 1,500 Autonomous Vehicles Set to Hit the Roads, with an Annual Production Target of 1.55 Million New Energy Vehicles! Is This Historic City Taking a 'Gamble on Future

-

Trump's Exit: A Catalyst for the Global Surge of Chinese Automobiles

-

![]()

Joint Venture Electric Vehicles: Stuck at the 150,000 Yuan Mark?

-

![]()

Baidu: Nothing Else to Rely On but Kunlunxin