97.41 Billion RMB in Revenue, 6 Billion RMB Market: Insta360's Dilemma in Growth Limits

05/19 2026

05/19 2026

470

470

Author | Chuan Chuan

Editor | Da Feng

Insta360 has reported a seemingly remarkable performance, with total revenue reaching 9.741 billion RMB in 2025, marking a 74.76% year-on-year increase.

Judging solely by the growth rate, Insta360 appears to be a hardware tech company still in a high-expansion phase. As a company primarily focused on panoramic cameras and branded as a "leading global seller of panoramic cameras," it seems to meet capital market expectations for its growth potential.

However, the challenge lies in the fact that Insta360's growth story cannot be assessed solely by its own trajectory; it must also be re-evaluated within the context of the market it operates in. According to a recent report by Jiuqian Consulting, Insta360's core market is not a trillion-yuan or multi-trillion-yuan mainstream consumer electronics segment but a niche market valued at approximately 6 billion RMB (Note: This figure is estimated based on Jiuqian's report data).

In other words, behind the 9.7 billion RMB in revenue lies not a vast, untapped new market but a segmented (niche) market with a clearly defined ceiling, growing competition, and increasing margin pressures.

The 6 Billion RMB Market: How Low Is the Ceiling According to Jiuqian's Data?

The first major challenge Insta360 faces is the inherent capacity of the market.

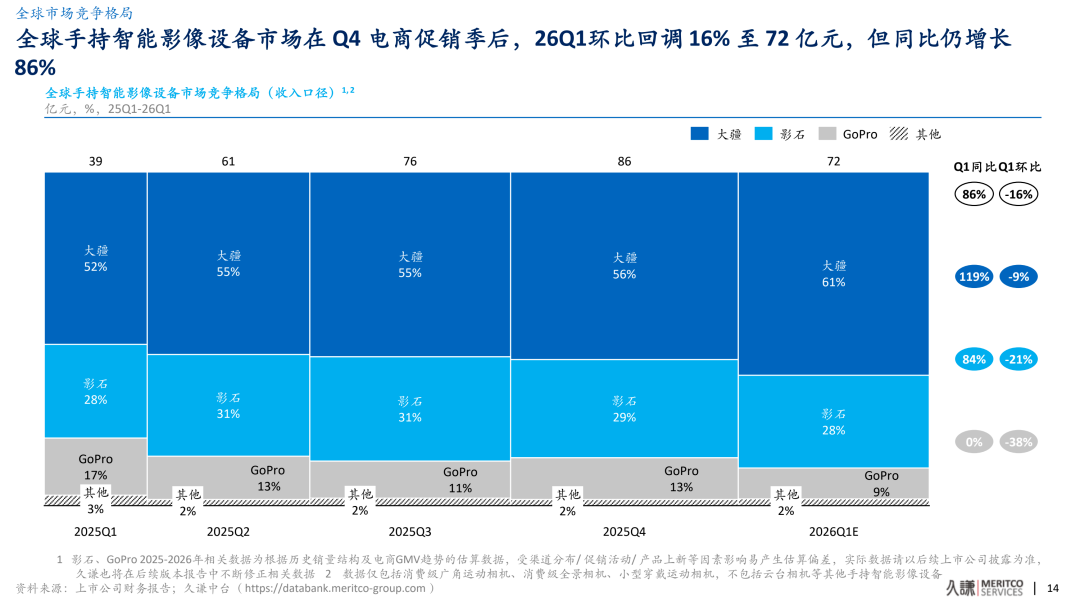

According to Jiuqian Consulting's May 2026 research on the handheld smart imaging industry, the global market size for the core category of handheld smart imaging devices—panoramic cameras—was approximately 7.2 billion RMB in Q1 2026. This figure is relatively modest within the broader consumer electronics sector.

For comparison, China's smartphone market exceeds 800 billion RMB, the global action camera market is around 20 billion RMB, and even the earphone market, dominated by Apple's AirPods, is a multi-hundred-billion-yuan segment. In contrast, 6 billion RMB is not a "hidden champion" market but a highly typical niche hardware segment.

More importantly, Insta360 is not the only player in this small market.

Competitors include DJI, GoPro, EZVIZ, and other brands. Jiuqian's report on the competitive landscape shows that in global revenue from handheld smart imaging devices, the market size in Q1 2026 contracted by 16% quarter-on-quarter to 7.2 billion RMB after the Q4 e-commerce promotion season but still grew 86% year-on-year. Meanwhile, DJI's market share further increased to 61%, widening its lead, while Insta360 held 28%, GoPro 9%, and other brands 2%.

This indicates that even as the industry continues to grow year-on-year, the gains are not evenly distributed to Insta360. DJI is emerging as a stronger absorber of market share.

From this perspective, Insta360's 9.7 billion RMB in revenue does not automatically equate to sustained high growth in a massive market.

Instead, it reflects income generated across multiple product lines, including panoramic cameras, action cameras, small wearable devices, and accessories, all within a niche market. The issue is that high growth in niche markets tends to be phased: early-stage market education through new categories, mid-stage expansion through hit products, and late-stage inevitable competition for share, pricing, and ecosystem dominance. Once the market size nears its upper limit, companies must either seize share from rivals or enter larger but more crowded new markets to sustain past growth rates.

How Valuable Is Being "Number One" in a 6 Billion RMB Market?

Insta360's most recognizable label is panoramic cameras.

This label holds value, indicating that Insta360 has accumulated user mindshare and product capabilities in this segmented (niche) category. However, the "number one" status must be evaluated alongside market capacity and competitive dynamics.

Insta360 holds approximately 55–60% of the panoramic camera market share but faces sustained pressure from DJI's Osmo 360 series. Its share has declined from an early dominant position of around 92% to less than 60% today.

Jiuqian's category-specific data further confirms this shift. The global panoramic camera market slightly contracted to 1.5 billion RMB in Q1 2026, with market shares remaining stable: Insta360 at 57%, DJI at 33%, GoPro at 4%, and others at 6%.

In Q1 2025, Insta360 held 90% of the panoramic camera market, rising to 92% in Q2 2025. This means that after DJI entered, panoramic cameras ceased to be a safe zone dominated solely by Insta360 and became a battleground where DJI could quickly gain traction, scale, and reshape the landscape.

The key question is not whether Insta360 remains number one but whether "number one" can still justify a high valuation. A company capturing 50% of a trillion-yuan market has vastly different capital implications than one holding 50% of a multi-billion-yuan market. The former implies significant profit pools and expansion potential, while the latter resembles a segmented (niche) category champion.

Insta360 still holds advantages in panoramic cameras, but these are no longer unassailable monopolistic strengths. Moreover, its 9.7 billion RMB in revenue is not solely driven by panoramic cameras. A substantial portion comes from action cameras, thumb cameras, and accessories—categories with far more intense competition, dominated by stronger players.

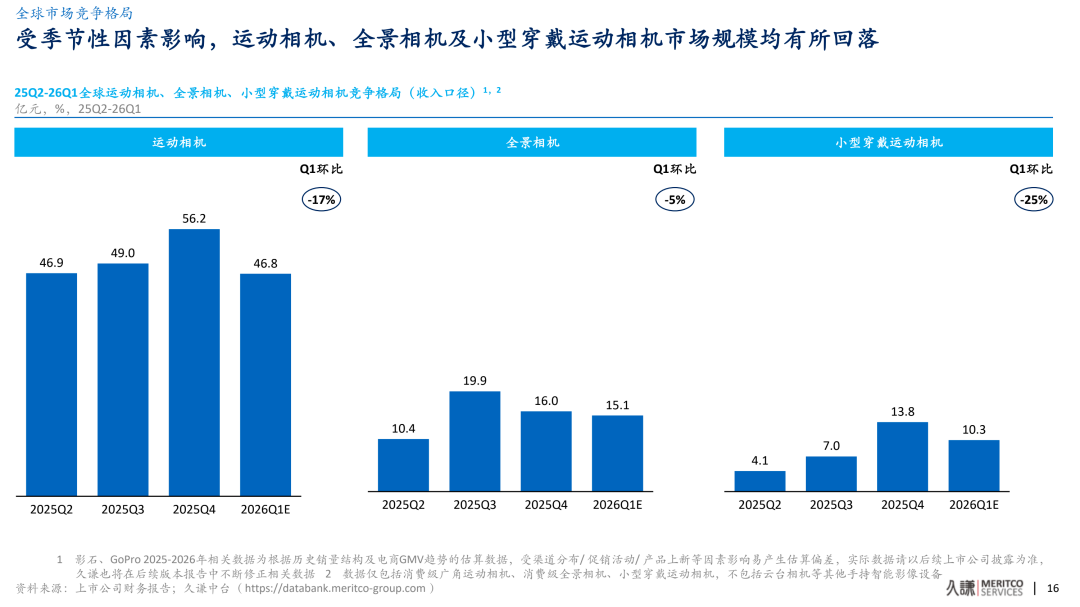

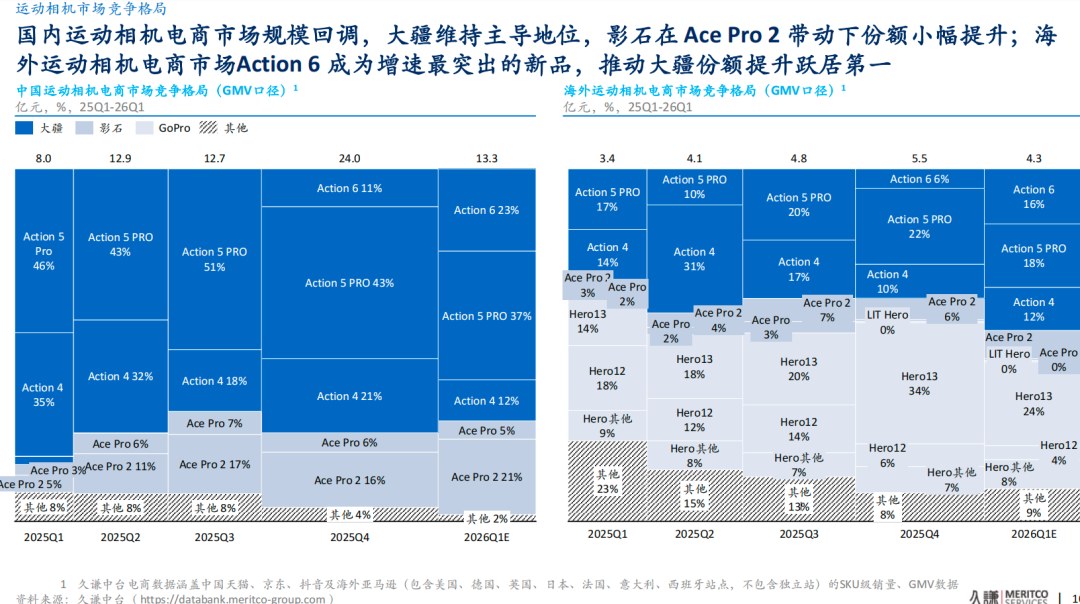

Take action cameras, for example. Jiuqian's report shows that the global action camera market was 4.7 billion RMB in Q1 2026, down 17% quarter-on-quarter. DJI's share rose further to 70% with its Action 6 model, while Insta360 held 16%, GoPro 13%, and others 1%.

This data indicates that Insta360 is a challenger, not a leader, in the larger action camera category. It faces not only GoPro, a legacy action camera player, but also DJI, a formidable competitor with superior product, channel, supply chain, and ecosystem capabilities.

The same applies to small wearable action cameras. Jiuqian's report shows that this market contracted by 26% quarter-on-quarter in Q1 2026 but grew 333% year-on-year due to DJI's entry. In terms of revenue, DJI held 59% of the market share in Q1 2026, while Insta360 held 40%. In Q1 2025, Insta360 had dominated with 93% of the market. Thus, DJI's Osmo Nano rapidly reshaped the market landscape after its launch.

Therefore, Insta360's "number one" status must be re-evaluated. Its advantages have shifted from "absolute leadership" to "partial leadership." While it retains brand mindshare, this is being eroded by stronger competitors. Growth increasingly relies on multi-category expansion, which means entering even more fiercely competitive arenas.

Survival in a Multi-Player Landscape Below the Market Ceiling

More alarming than market size is the relationship between category ceilings and user demand. The imaging device industry exhibits a clear "category ceiling" phenomenon: each segmented (niche) category has a defined upper limit, and users are unlikely to purchase panoramic cameras, action cameras, and thumb cameras simultaneously. Instead, they choose one based on core needs.

This judgment is critical because it means Insta360 cannot simply expand its market share by offering more camera categories.

Jiuqian's report on consumer demographics supports this:

Action cameras are primarily used for extreme sports like cycling, skiing, diving, and mountaineering, as well as outdoor adventures. Panoramic cameras target travel enthusiasts seeking immersive visual experiences. Small wearable action cameras cater to athletes and Vloggers, emphasizing first-person perspective, portability, and quick activation. While these needs overlap, they do not necessarily stack.

For most users, one device suffices for core shooting needs unless they form high-frequency creative habits, limiting the incentive to purchase multiple camera types.

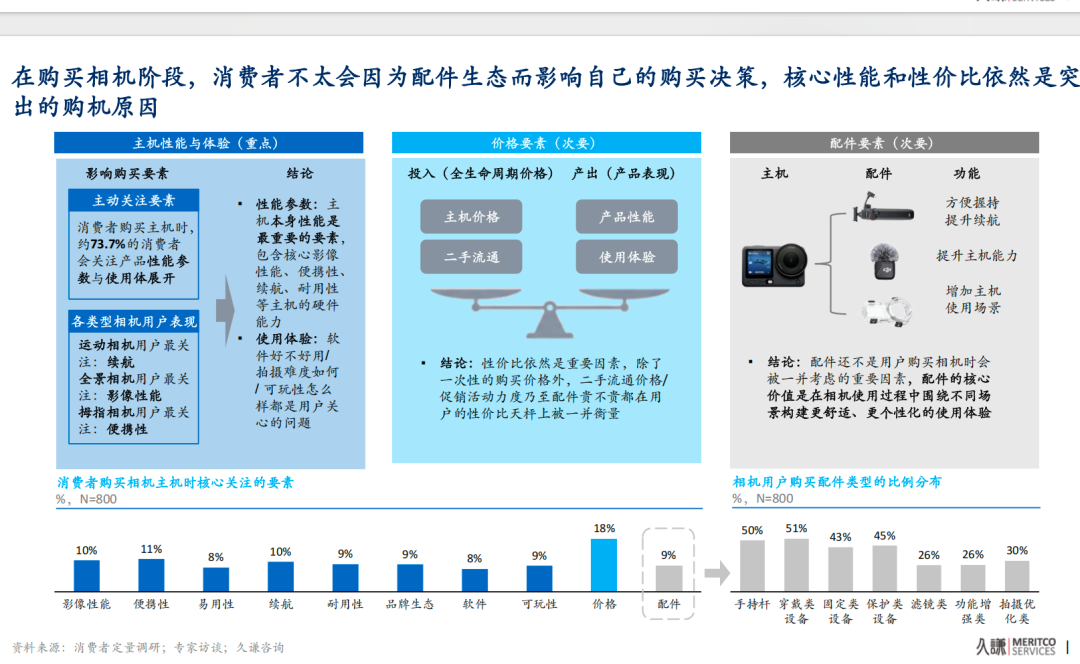

Consumer surveys also show that when buying a primary device, users prioritize performance, experience, and price over accessories.

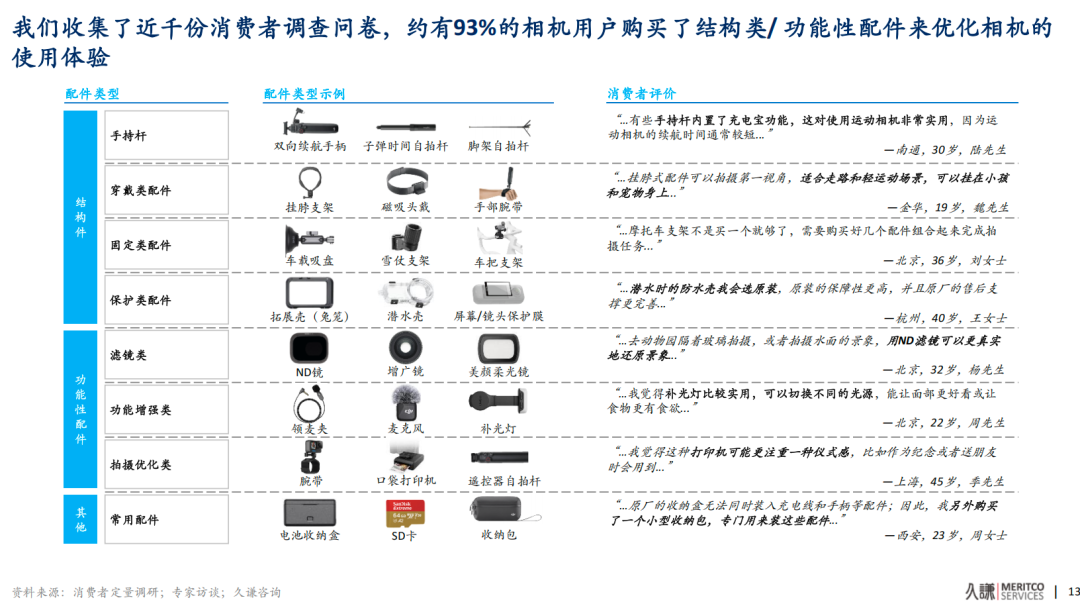

Jiuqian's report reveals that 73.7% of camera buyers focus on product performance parameters and user experience. Action camera users prioritize battery life, panoramic camera users prioritize imaging performance, and thumb camera users prioritize portability. In other words, consumers first judge whether a camera "solves their core shooting problem" rather than whether the brand can sell them additional accessories later.

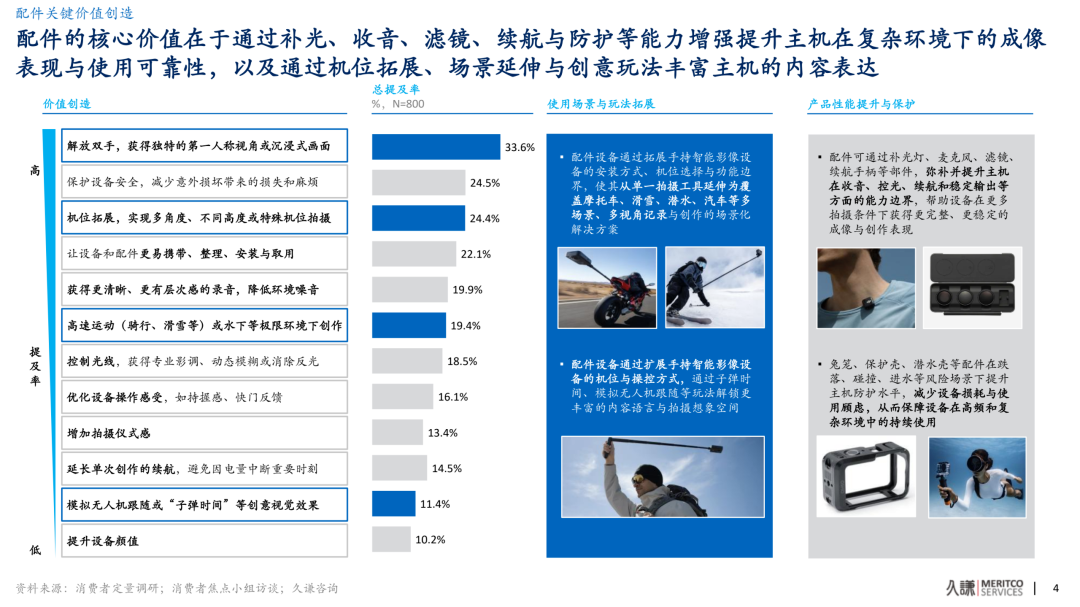

Accessory ecosystems hold value. The report notes that about 93% of camera users purchase structural or functional accessories to enhance their experience. However, accessories are not the primary driver of primary device purchases or repurchases.

DJI, Insta360, and GoPro users who repurchase primary devices from the same brand stand at 94%, 87%, and 90%, respectively. Among them, only 18%, 17%, and 20% cite accessories as the reason for repurchasing. This suggests accessories enhance loyalty but do not solely determine primary device competition.

A more pressing issue is that Insta360 does not dominate the accessory ecosystem.

Jiuqian's report shows that DJI's official website lists 313 accessories covering 12 scenarios, while Insta360 offers 290 accessories across 8 scenarios. GoPro provides 115 accessories but covers 13 scenarios, focusing on niche sports like skiing, mountain biking, surfing, motocross, power sports, fishing, and kayaking.

This means Insta360's accessory volume is competitive, but DJI excels in system completeness and cross-generational compatibility, while GoPro retains professional mindshare in hardcore sports.

DJI's threat is particularly noteworthy. The report highlights that DJI's accessories minimize device-switching costs and time losses across creative scenarios, featuring magnetic quick-release mechanisms, remote/charging contacts, and multi-generational compatibility.

For example, the Osmo Action 1.5-meter extension pole kit is compatible with multiple generations of Osmo Action models (6, 5 Pro, 4, 3, 2, and the original). Such ecosystem design reduces user hesitation about upgrading and increases repurchase certainty.

Insta360 is not without its strategies. Jiuqian's report notes that Insta360 upgrades accessories like dive housings and street-shooting grips from single-function items to scenario-based solutions by combining hardware with software algorithms and filters.

For instance, its dive housing hardware, dive mode algorithm, and AquaVision underwater color restoration address refraction, stitching, and color cast issues in underwater panoramic shooting. This demonstrates that Insta360's true strength lies not in hardware specifications alone but in software-hardware integration and innovative use cases.

However, software-hardware integration cannot eliminate market ceilings. In a multi-player landscape, Insta360's real dilemma is that it faces larger competitors in every category.

Escaping the "small but beautiful" panoramic camera niche is challenging because other categories already have dominant players. It may also be uneconomical, as rising competition costs squeeze profit margins. This judgment is sharper than merely discussing market share: Insta360's issue is not an inability to grow but changing growth quality and costs.

Below the Ceiling: Valuation Logic Needs Re-examination

Ultimately, all industry discussions circle back to valuation. Currently, the STAR Market values Insta360 at approximately 77 billion RMB, with a price-to-earnings (PE) ratio of around 80. This valuation assumes sustained high growth. However, with a clear market ceiling, deteriorating competitive landscape, and margin pressures, the growth narrative supporting this high valuation must be re-examined.

A high valuation is not untenable, but it requires three conditions: a sufficiently large market space, sufficiently strong competitive barriers, and sufficiently strong profit-realization capabilities. The current issue with Insta360 is that doubts have arisen regarding all three conditions.

First, the core market segment is worth approximately 6 billion yuan, which is not a large market; second, its share of the panoramic camera market has dropped from over 90% to less than 60%, while its market share in action cameras and small wearable cameras is being continuously squeezed by DJI; third, its current net profit margin has fallen to 3.41%, and there is no sign of a reversal in the trend of intensifying competition. also offers a valuable window for analysis: In the first quarter of 2026, the global e-commerce market for handheld smart imaging devices contracted to 2.8 billion yuan, marking a 35% quarter-on-quarter decline. The report notes that market growth—previously propelled by the entry of )

Consequently, Insta360’s valuation logic may now be confined to two potential pathways.

The first pathway involves digesting its valuation through profit growth, maintaining a strong market share within a constrained market segment while enhancing net profit margins. However, with net profit margins already reduced to 3.41% and competitors intensifying their efforts, this approach presents significant challenges. The second pathway entails recalibrating the valuation to a more reasonable range through a decline in stock price. For investors, this is not an emotional assessment but a revaluation influenced by the interplay of market size, competitive dynamics, and profitability.

Insta360 Innovation remains a company characterized by robust product capabilities, strong brand recognition, and an innovative spirit. It has established a distinctive position in the panoramic camera market and continues to diversify shooting styles through integrated software and hardware solutions. Nevertheless, capital markets evaluate not just "good companies" but also the speed, scale, and profitability of their sustained growth.

As the narrative shifts from "high-speed expansion" to "competition for market share within a limited segment," the valuation logic must transition from the speculative allure of a growth stock to the pragmatic realities of a hardware-focused enterprise.

Insta360’s true challenge lies not in the fact that its 9.7 billion yuan in revenue is unimpressive, but rather that the market underpinning that revenue is too small. It is not that achieving the top position in the panoramic camera market lacks value, but that the market itself is limited in size and its share is under pressure. Nor is it that product innovation has ceased, but rather that innovation now faces systematic competition from formidable rivals like DJI and GoPro.

The 7 billion yuan revenue ceiling, multi-player competition in a niche market segment, and the strain of a 3.41% net profit margin are the realities Insta360 Innovation must confront.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle