The Business Logic Behind Tokens

05/25 2026

05/25 2026

589

589

Recently, the three major telecom operators in China have collectively started selling tokens.

China Telecom has launched a series of trial commercial token packages. Individual users can get 10 million tokens per month for RMB 9.9, while enterprise developers can purchase starting from 15 million tokens per month for RMB 39.9. Shanghai Mobile has also announced the large-scale commercialization of its 5G-A super uplink network capabilities, introducing a general token service where users can purchase 400,000 tokens for RMB 1, supporting payment via phone bills and compatibility with multiple models, thereby initiating a new paradigm for AI-powered office life. China Unicom Shanghai Branch has released a fully domestically produced security foundation featuring 'domestic chips, domestic models, and domestic clouds,' offering diversified computing power services, multi-tiered token products, and integrated packages.

The three major telecom operators in China have officially incorporated 'token operations' into their strategic priorities for 2026. When tokens, charged 'by the word,' become commodities, they are not simply supported by servers in data centers but by a vast infrastructure network spanning models, data centers, domestic chips, edge computing, and computing power IoT.

01 Operators Shift from 'Selling Bandwidth' to 'Selling Tokens'

Over the past two decades, the core business model of telecom operators has been 'selling connectivity'—charging based on bandwidth, duration, and data volume. In the 5G era, this logic has reached a bottleneck: while data traffic grows, ARPU (Average Revenue Per User) stagnates, reducing operators to mere 'pipeline workers.'

The emergence of the token economy offers operators a unique opportunity to transform from 'bit transporters' to 'computing power operators.' China Telecom's packages integrate the Xingchen large model and DeepSeek V3.2 for individual users, and Xingchen + GLM5 for enterprise users, while consolidating proprietary and third-party computing power resources. This means Telecom is not just selling computing power but offering an integrated service of 'model + computing power + connectivity + security.'

More notably, 'Tianyi Token Coins'—defined by China Telecom as a unified metric for token operation and circulation—allow users to redeem token packages and AI applications with points. This constructs a 'monetary system' in the computing power domain, laying the foundation for future computing power trading, futures, and scheduling.

McKinsey's February 2026 research report points out that AI infrastructure requires diverse assets such as data centers, fiber optics, edge computing, power supply, and GPU computing power, all of which are naturally controlled by telecom operators in abundance. While cloud providers are still competing over large model parameters, operators have quietly 'commoditized' computing power.

02 'Token Factories': The Industrial Revolution in Computing Power Production

Token factories refer to data centers transforming into token production facilities in the AI inference era. This concept was first proposed by NVIDIA CEO Jensen Huang at the 2024 GTC Conference and systematically elaborated as 'Token Factory Economics' at the GTC 2026 Conference on March 16, 2026. Huang introduced a five-tier commercial framework for AI services—free, intermediate, premium, high-speed, and ultra-high-speed layers—and emphasized that higher token throughput per watt under fixed power conditions reduces production costs.

If token packages represent the 'retail end,' then 'token factories' are the 'production end.' On May 15, Hongxin Electronics partnered with the Wuxi High-Tech Zone to establish the province's first Huawei super-node computing cluster in Wuxi. This 'token factory' will initially deploy four Huawei Ascend 384 super-node servers (each with 384-card computing power), forming a super cluster. Earlier, China Telecom Ningxia Branch's 2026 'Token Factory' generation capacity service centralized procurement project had an estimated scale of RMB 16.451 billion (excluding tax), marking the first hundred-billion-yuan centralized procurement project named after a token factory among the three major operators.

The essence of a 'token factory' is upgrading computing power production from 'artisanal workshops' to 'industrial assembly lines': first, scalability, with clusters of ten thousand or even one hundred thousand cards continuously outputting tokens; second, standardization, with unified metrics, interfaces, and billing; and finally, orchestration, enabling cross-regional and cross-architecture token production and distribution through computing power networks. Currently, China Telecom's one-stop token service platform, unveiled at the 9th Digital China Construction Summit, covers the entire industrial chain of token mass production, orchestration, distribution, and value realization.

03 The Computing Power Strengths of the Three Major Operators

Behind the token business lies the computing power empire built by the three major operators through hundreds of billions in capital expenditures over the years.

China Telecom

In 2025, China Telecom upgraded its corporate strategy from 'cloud transformation and digital transformation' to 'cloud transformation, digital transformation, intelligence, and affordability,' fully embracing artificial intelligence. It constructed and continuously deepened an integrated intelligent cloud system of 'computing power, platforms, data, models, and applications,' leveraging its core technology 'Xirang' to capitalize on cloud-network integration advantages.

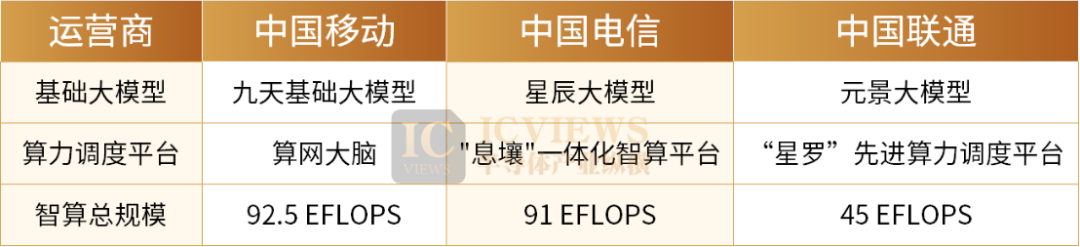

By the end of 2025, its proprietary and accessed intelligent computing power reached a total scale of 91 EFLOPS, aggregating over 10 trillion tokens of general-purpose large model corpus data and high-quality datasets covering more than 14 industries, totaling over 500TB. China Telecom also developed over 110 industry-specific large models and over 350 industry intelligent agents, serving over 37,000 clients, with an 85% AI penetration rate among central enterprises.

China Mobile

China Mobile's computing power network strategy is the most aggressive, with a total intelligent computing power scale of 92.5 EFLOPS (FP16), achieving full-specification computing capabilities from hundreds to tens of thousands of cards. In early 2026, China Mobile Guangdong won a RMB 155 million bid for the Shenzhen Guangming Large-Scale Device Computing Power Service Support Platform project, fully adopting Huawei Ascend 910C chips to build a domestically produced intelligent computing power system, entirely 'rejecting imports.'

In 2025, China Mobile's Jiutian foundational large model upgraded to version 3.0, launching over 100 AI+ products and application solutions, 29 vertical intelligent agents, and over 50 industry-specific large models, achieving rapid growth in data algorithm and digital culture revenues.

From a layout perspective, China Mobile built ten thousand-card-level intelligent computing centers in Hohhot and Harbin in 2024 and further strengthened its 'AIDC + network + computing power + operations and maintenance' integrated service capabilities in 2025, enabling intelligent scheduling of general-purpose, intelligent, supercomputing, and quantum computing power. This 'computing power network' model differentiates it from leading vendors like Alibaba Cloud and Huawei Cloud, particularly showcasing unique advantages in customized services for government and enterprise clients.

China Unicom

Unicom Cloud is accelerating its evolution into an AI cloud, deepening ultra-large-scale intelligent cloud-native practices, enhancing unified orchestration and scheduling capabilities, and constructing a new computing power operation model of 'applications + models + resources,' serving the digital transformation of over 180 provincial and municipal government clouds and nearly 400,000 enterprise clients. It established the National AI Application Pilot Base, launching the 'Wanxiang' data engineering platform, 'Yuanjing' MaaS platform, and 'Wanwu' intelligent agent platform, accumulating over 400TB of high-quality datasets, providing over 140 mainstream industry models, and gathering over 10,000 developers to help clients rapidly build intelligent agent applications.

At the infrastructure level, Unicom proposed a '4+4+31+X+0' intelligent computing infrastructure layout and AINet computing power smart internet, enabling efficient cross-regional computing power scheduling through the 'New Eight Verticals and Eight Horizontals' backbone optical cable network—deploying ultra-large-scale training resource pools at national hub nodes, providing hundred-card-scale training and inference services at provincial nodes, and achieving 'millisecond computing' for edge inference at local nodes.

China Unicom's intelligent computing power scale has reached 45 EFLOPS, with over 1.1 million standard rack units and seven 100-megawatt-class AIDC parks built.

04 Domestic Computing Power Supports the Token Economy

Although token prices have significantly declined, the demand for low-cost, 'abundant' tokens continues to surge with the rise of AI agents. Further reductions in token prices will ultimately depend on the large-scale production and cost optimization of domestic AI chips.

In 2025, China's AI accelerator card market shipped approximately 4 million units, with domestic vendors accounting for 1.65 million units, marking a market share breakthrough of over 40%. NVIDIA's share dropped from around 70% in 2024 to 55%.

Huawei Ascend is the undisputed domestic leader: shipping approximately 812,000 units in 2025, accounting for nearly 50% of domestic shipments. In Q1 2026, the Ascend 950PR officially entered mass production.

Cambricon followed closely: reporting a net profit of RMB 2.059 billion in 2025 and RMB 1.013 billion in Q1 2026, a year-on-year surge of 185%. Its ThinkForce 590 chip is widely used by the three major operators, financial institutions, and major internet companies.

Operators' intelligent computing centers are becoming 'training grounds' for domestic chips. China Mobile and China Telecom have built multiple ten thousand-card-level intelligent computing centers using domestic chips like Ascend or Cambricon, with cumulative investments exceeding RMB 10 billion. This substitution is not a policy-driven switch but a commercial necessity driven by cost-efficiency in the token economy.

05 Every Device Will Become a Token Consumer

At the farthest end of the token economy lies computing power IoT (AIoT).

For operators, computing power IoT means the 'long-tail market' for token consumption will be fully unlocked. Every camera, every connected vehicle, and every industrial robot is both a token producer (uploading data) and a token consumer (obtaining inference results).

When China Telecom states its 2026 goal of making 'token services the main business line,' it aims not just at C-end RMB 9.9 packages but also at the trillion-yuan B-end IoT device computing power access. Just as electricity evolved from Edison's DC power stations to today's national grid, computing power is undergoing a transformation from 'private generators' to a 'public grid.'

Operators have three irreplaceable advantages in the token business:

First, the network is computing power—fiber optics, 5G, and satellite internet serve as the 'power grid' for computing power transmission, eliminating the need for operators to build additional transmission layers.

Second, nodes are factories—millions of base stations, data centers, and edge computing centers nationwide can be transformed into distributed token production factories with minimal modifications.

Third, clients are users—900 million mobile users, tens of millions of enterprise clients, and billions of IoT devices are all ready-made token consumers. Nodes are factories: millions of base stations, data centers, and edge computing centers nationwide can be converted into distributed token factories with slight modifications.

Of course, operators face numerous challenges on their token journey: industry standards are not yet unified, data center liquid cooling retrofits are daunting, the domestic chip ecosystem still needs improvement, and cross-domain computing power scheduling capabilities require enhancement... However, the overarching business trend is clear: whoever controls token pricing will dominate the 'petrodollar' of the AI era.

The business logic behind tokens ultimately boils down to one sentence: Computing power is no longer a technical capability but a public commodity that can be measured, traded, and circulated like water and electricity. And operators are striving to become the 'State Grid' of this new world.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle