Ningde Is Being ‘Urged’ by Automakers to Invest in DeepSeek

05/25 2026

05/25 2026

426

426

Automakers Are Moving Away from Ningde, While Ningde Is Diversifying Beyond Automakers

DeepSeek’s rumored list of potential investors now includes the battery industry giant.

On May 23, The Information reported that Contemporary Amperex Technology Co. Limited (CATL) is planning to participate in the initial round of financing for DeepSeek, with JD.com and NetEase also in negotiations to invest.

In terms of valuation and financing scale, it was previously reported that DeepSeek aims to raise RMB 50 billion, with its valuation expected to surpass RMB 350 billion post-financing.

Historically, CATL has rarely ventured into such cross-border investment projects. If the investment in DeepSeek materializes, it would signify the company’s first direct equity participation in a general-purpose foundational large model enterprise.

If the news holds true, why is Ningde joining the fray for DeepSeek? As the global leader in power and energy storage batteries, what are Ningde’s underlying motivations?

01 Investing in Hengtong and Acquiring 21Vianet: What Is Ningde’s Grand Strategy?

In fact, Ningde’s ambition to align with AI is not a recent development.

In April, Hengtong Electric announced that CATL would invest RMB 4.1 billion to acquire a 49% stake in its shareholder structure, with plans to deeply engage in the company’s governance.

Who is Hengtong Electric?

Simply put, powering AI Data Centers (AIDCs) is not as straightforward as plugging in a power strip. With thousands of GPUs running simultaneously, power demands fluctuate rapidly, rendering conventional power systems inadequate. Hengtong Electric is a leading enterprise addressing this challenge.

Hengtong Electric possesses two key technologies: High-Voltage Direct Current (HVDC) and Panama Power Systems.

The core function of HVDC is to convert unstable alternating current (AC) power from the grid into safer and more efficient direct current (DC) power for servers, ensuring an uninterrupted power supply for thousands of GPUs during inference tasks. Panama Power Systems, an integrated version of HVDC, combines transformers, rectifier modules, and power distribution units into a standard cabinet. It takes in high-voltage power (tens of thousands of volts) at the input and delivers usable DC power at the output—all in one step.

By 2025, Hengtong Electric is projected to hold a 31% market share in China’s HVDC market for intelligent computing centers, ranking first. It commands about 50% of Alibaba Cloud’s HVDC systems and over 90% of the market for Panama Power Systems.

This means that any expansion of major companies’ data centers would be impossible without Hengtong Electric.

In mid-May, CATL made another strategic move, acquiring a 38.1% stake in 21Vianet Group for RMB 6.4 billion, becoming its largest shareholder.

What role does 21Vianet Group play?

Training and running large models require not just GPUs but also physical space. However, building an AI data center is not as simple as stacking servers in a warehouse.

An intelligent computing center has a power density per cabinet that is 5 to 10 times higher than traditional data centers. Each cabinet starts at 30 to 50 kilowatts, with some exceeding 100 kilowatts. This is equivalent to cramming the electricity consumption of an entire household into a single cabinet—with thousands of cabinets running simultaneously.

Under such high power demands, electricity is just one concern. The power load of a large intelligent computing center is comparable to that of a small county. Any issues with grid access, backup power, or peak shaving could halt tens of thousands of GPUs.

21Vianet Group specializes in the construction and operation of such high-density data centers. By the end of 2025, it will operate over 50 data centers with a total capacity of 889 megawatts.

However, building data centers alone may not have been sufficient to attract CATL to 21Vianet Group. The real driving force behind this deal may be a larger opportunity.

Shortly before CATL’s investment, 21Vianet Group secured a major contract to provide approximately 500 megawatts of computing capacity to ByteDance. This deal more than doubled its operational scale. But the 500 megawatts is just the tip of the iceberg. Over the next few years, ByteDance plans to build intelligent computing centers with a total power load equivalent to several counties. The two biggest pain points for AIDC deployment are electricity and physical space.

CATL can handle the electricity—energy storage, peak shaving, and backup power are its core competencies. For the physical space, someone needs to build the data centers, deploy liquid cooling systems, and manage grid access. That’s where 21Vianet Group comes in.

Most likely, the three parties reached an agreement: ByteDance places orders, 21Vianet Group builds the data centers, and CATL provides energy storage solutions. Once the data centers are ready, ByteDance can install GPUs purchased from Cambricon and Huawei, along with CATL’s batteries, and all parties profit.

CATL’s RMB 6.4 billion investment to become 21Vianet Group’s largest shareholder was not a spontaneous decision. It came after finalizing the deal with ByteDance, ensuring a locked-in partner for physical space. This way, every new intelligent computing center ByteDance builds will include CATL’s energy storage and power systems.

This is not just an investment—it’s about securing a dedicated pathway to ByteDance’s AI ambitions.

Taken together, investing in Hengtong Electric gives CATL the “plug” for AIDC power systems; investing in 21Vianet Group secures the “space” for AIDC data centers; and investing in DeepSeek directly binds the largest power consumer.

CATL is playing a grand game, aiming to become the power supplier for major companies’ AIDCs, offering everything from power equipment to energy storage systems to data center space—a one-stop solution.

However, as large as the AIDC market is, it’s just an incremental growth story for CATL. The real reason behind its urgency to expand into new businesses is that automakers are steadily reducing their reliance on CATL. AI is a battle CATL must win.

02 Automakers Are Cutting Ties—They All Want to Break Free from Ningde

Automakers no longer want to be tied to CATL.

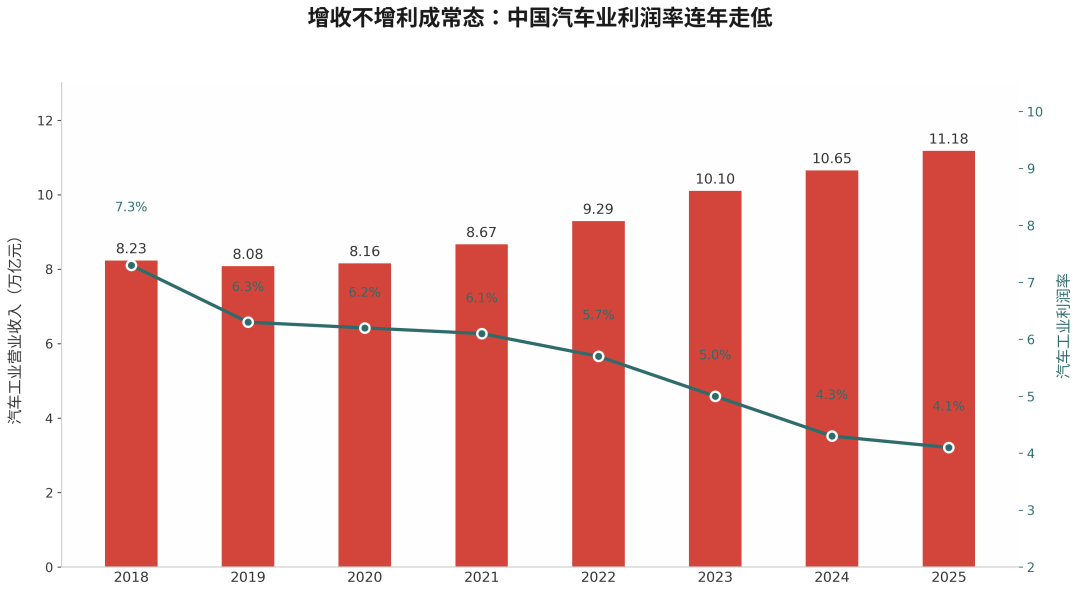

The automotive industry has evolved from its real start in 2020 to intense competition by 2026, with automakers facing increasing challenges. While industry revenue grew from RMB 8.23 trillion in 2018 to RMB 11.18 trillion in 2025, profit margins declined from 7.3% to 4.1%.

With a market size exceeding RMB 11 trillion, profit amounts to just over RMB 400 billion. Costs are rising faster than revenue—the more vehicles sold, the harder it is to turn a profit.

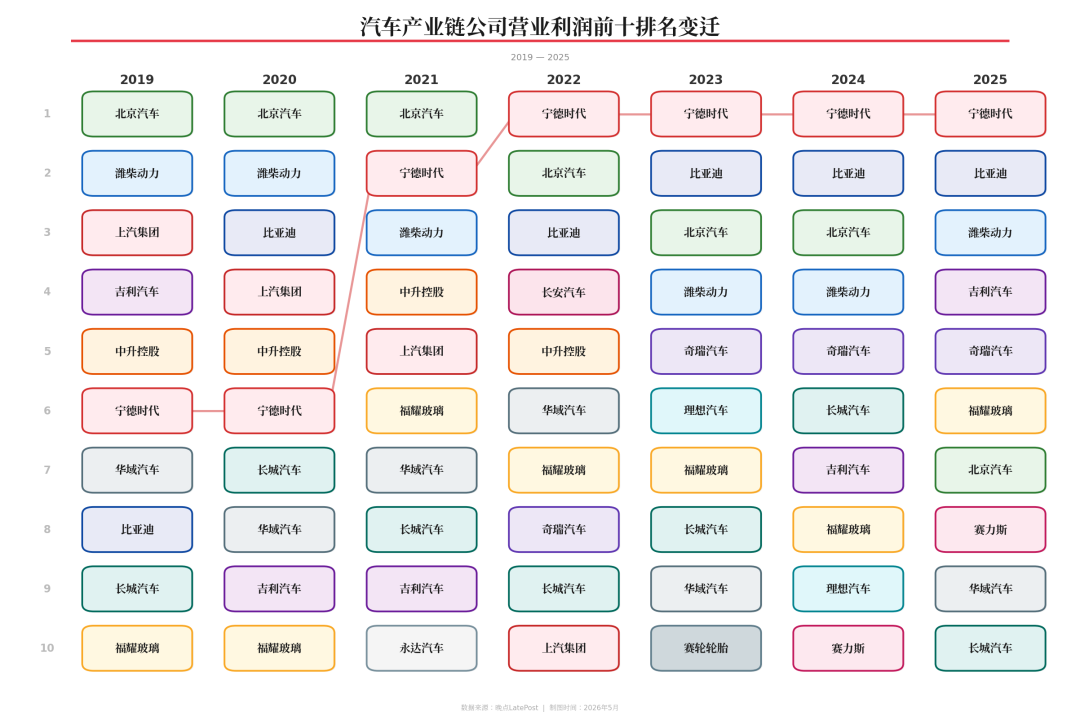

CATL’s 2025 financial report shows: net profit of RMB 72.2 billion, up 42% year-on-year, with a net profit margin of 18.12%. The combined profits of leading automakers like BYD, Geely, Great Wall Motors, SAIC, and Changan are roughly comparable to CATL’s alone.

This has led to an industry saying: automakers fight on the front lines, while CATL counts the money in the background.

This is not because CATL deliberately raises prices. As the absolute leader in battery technology and scale, its business model dictates this outcome. Batteries account for 30%-40% of a vehicle’s cost, yet automakers have little pricing power. Selling an electric vehicle priced around RMB 100,000 might yield less than RMB 10,000 in profit for the automaker, while CATL profits handsomely from each battery.

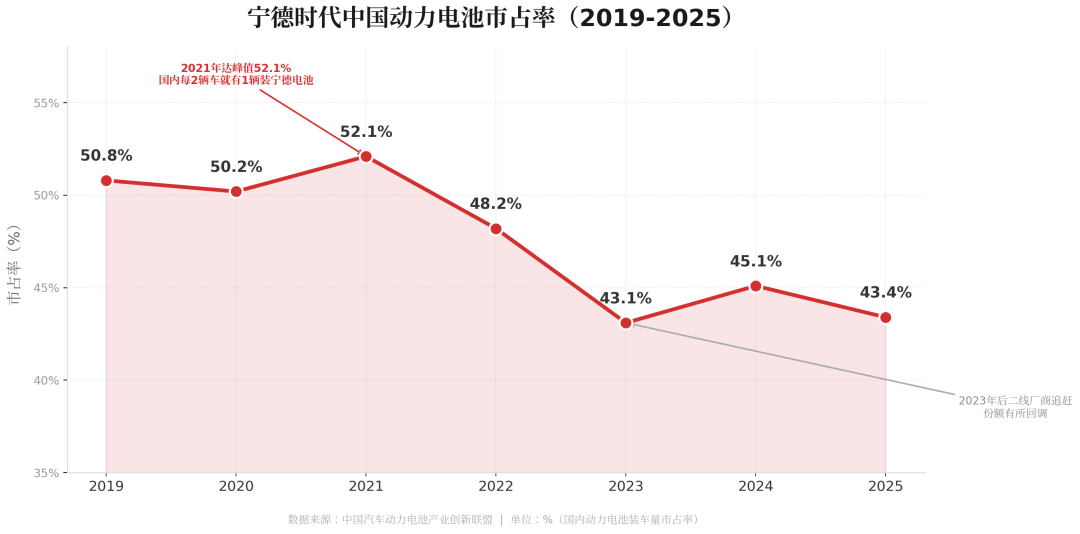

The issue is that automakers previously had no choice. CATL once dominated the market, holding over half of the market share at its peak. Not using CATL’s batteries meant struggling with production capacity. However, rapid industry growth in recent years has provided automakers with more options.

BYD has long produced its own batteries through FinDreams Battery, now the second-largest in China by installation volume, supplying both itself and others. Geely has consolidated Yaoning and Vreo, starting to purchase cells from external battery makers for in-house packaging. Great Wall Motors has SVOLT Energy, which, despite listing challenges, maintains solid production lines and growing volumes. GAC’s Aion brand cooled its relationship with CATL early on, turning to CALB instead.

Among new-energy vehicle startups, NIO, Li Auto, and XPENG are diversifying their suppliers. NIO invested in WeLion New Energy for semi-solid-state batteries, while Li Auto collaborates with Sunwoda and SVOLT. Even the highest-volume newcomer, Leapmotor, adopts a multi-supplier strategy—not entirely abandoning CATL but reducing its share. The message is clear: no single supplier should dominate.

The automakers’ reasoning is simple: costs are unsustainable. CATL’s gross margin consistently exceeds 20%, far higher than automakers. An automaker works hard to build an entire vehicle yet earns less than BYD does from a single battery.

Moreover, the memory of supply shortages two years ago lingers. During that period, having batteries meant shipping vehicles; without them, production lines halted. For instance, XPENG’s P5 460 model faced delayed deliveries due to insufficient LFP battery supplies.

Most importantly, battery technology gaps are narrowing. While CATL once led, second-tier players like CALB, Sunwoda, and SVOLT have caught up, offering comparable performance at lower prices. Automakers have little reason to remain loyal.

The trend is clear: CATL’s market share in power batteries has dropped from a peak of around 55% to just over 40% by 2025, with the decline accelerating.

From a market perspective, this is rational behavior—diversifying supply chains, reducing costs, and minimizing reliance on a single giant. But for CATL, it poses a significant problem.

This forces CATL to take two actions.

The simplest is to retain existing major clients. Whether renewing long-term contracts with Tesla, securing new deals with BMW, or expanding overseas to lock in more automakers, these key accounts are also adopting strategies learned from domestic automakers—buying CATL’s batteries while supporting second and third suppliers. CATL’s share in these contracts is declining yearly.

Beyond “defense,” CATL must find a new, large-scale, and rapidly growing market to sustain its growth.

This explains CATL’s investments in Hengtong Electric, 21Vianet Group, and now DeepSeek. Automakers are unwilling to let CATL profit from vehicle batteries, so CATL is pivoting to AI. Intelligent computing centers have rigid, 24/7 power demands with low price sensitivity. ByteDance needs power for Doubao, Baidu for Wenxin, Tencent for Hunyuan, and DeepSeek for training next-gen models. Behind all this computing power is electricity—CATL’s expertise. Energy storage, peak shaving, backup power, and high-voltage DC power supply align perfectly with CATL’s technical strengths. Investing in Hengtong Electric secured the “plug” for power systems; investing in 21Vianet Group locked in the “socket” for data center space; and investing in DeepSeek directly captures a major, power-hungry client.

DeepSeek’s investment is less about CATL’s proactive offensive and more about being pushed onto the AI playing field by automakers.

- END -

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle