Weekly Stock Review | A-Shares Buck the Trend with a Plunge: Have You Been Caught in the Sell-Off?

05/25 2026

05/25 2026

581

581

This week's stock review delves into the automotive sector, offering insights into the multifaceted auto market.

Many investors felt a pang of anxiety.

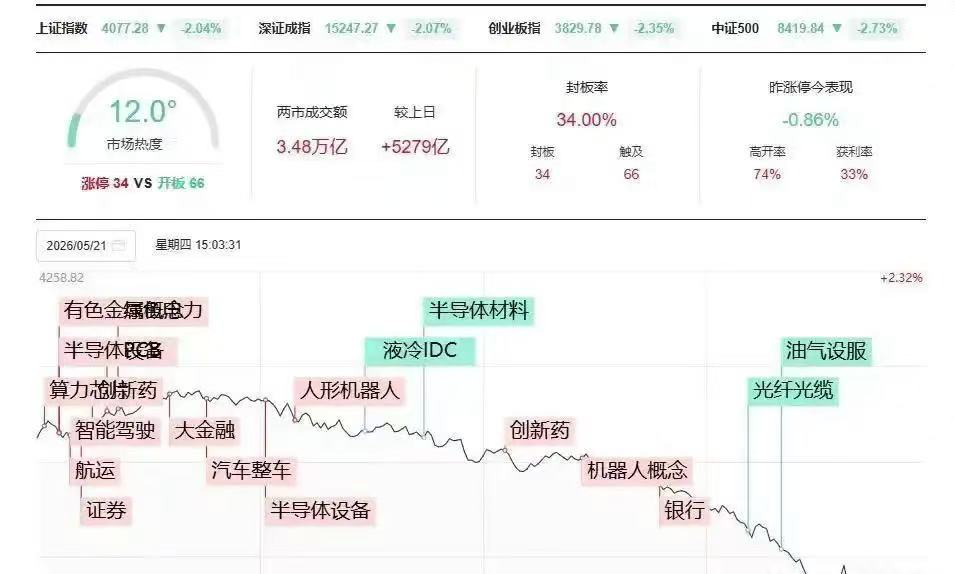

Stock enthusiasts watched helplessly as the Shanghai Composite Index plummeted from 4,199 to 4,077. In the morning session, A-shares surged, with even the securities sector, often seen as a bellwether for bull markets, leading the charge. However, the afternoon brought an abrupt shift to sell-off mode, resulting in a one-sided decline that left bullish investors defenseless.

The Shanghai Composite Index fell below the 4,100-point mark, with the Shenzhen Component Index and ChiNext Index following suit. Over 1.5 trillion yuan in market value vanished in just half a day, while trading volume remained robust above 3 trillion yuan, highlighting intense divergence at high levels.

More than 100 points were wiped out, with 4,800 stocks declining and over 4,300 ending in the red—a scenario that would leave any investor reeling. Most alarmingly, the afternoon sell-off continued unabated, showing no signs of stabilization.

This ruthless 'double whammy' of index and stock declines is a rare sight in recent market history. Yet, investors were left scratching their heads, unsure of the cause behind the sudden plunge. The confusion was palpable: Why did the morning's optimism give way to an afternoon collapse?

In the AI hardware sector, Nvidia's stellar earnings report sparked rallies in U.S. semiconductors and optical communications, providing a boost to Asian tech stocks. There was no external negative news to speak of. Domestically, the IPOs of storage giants and positive market sentiment also pointed towards a bullish outlook.

However, most analysts attributed the core plunge to concentrated profit-taking following a sustained rally.

A-shares had staged a rare independent rally, with the Shanghai Composite Index breaching the 4,200-point mark and hitting an 11-year high since July 2015. The ChiNext Index surpassed its 2015 peak, setting a new record. The STAR 50 surged over 25% in a month, with AI computing power and semiconductor tech stocks amassing massive short-term profits.

As the index approached the 4,190–4,200 range, retail investors, eager to recoup previous losses, sold aggressively, thinking, 'It's enough, time to cash out.'

This plunge heavily impacted AI computing power hardware, with the CPO and memory sectors leading the declines. Former high-flyers like Dongxin Semiconductor and Liyang Chip plummeted over 10%. In the short term, tech stocks had simply risen too much—what goes up must come down. Additionally, heavy selling by large funds ignited the downturn.

Investors also questioned whether the AI supply chain is overvalued. Brokerage strategists argued that earnings growth has digested valuations, which remain reasonable.

JPMorgan stated, 'Current AI supply chain valuations, whether measured by P/E or P/S ratios, are not extreme. Last Q4 exceeded three standard deviations; now it's fallen back to around two. Rolling earnings growth has partially absorbed these valuations.'

However, after Nvidia's better-than-expected earnings, fears of 'peak hype' emerged.

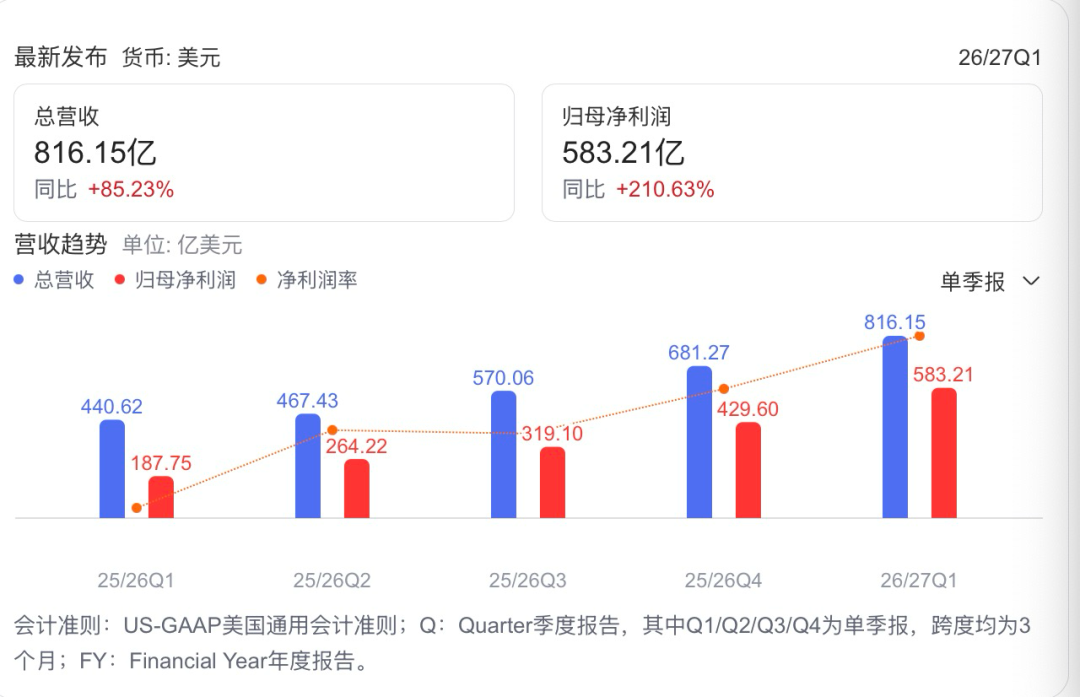

Nvidia reported quarterly revenue of $81.6 billion, reinforcing confidence in sustained AI infrastructure and data center investments, which drove Arm's stock surge. During the earnings call, Jensen Huang declared, 'The age of AI agents is here—computing power equals revenue, equals profit.' Nvidia is positioning its full-stack platform across AI's lifecycle, from training to inference, cloud to edge.

Nvidia's 'blockbuster' earnings ignited AI optimism, triggering a short-term stock rally. But 'peak hype' quickly materialized. Over two days, U.S. chip and memory sectors tanked, with the Philadelphia Semiconductor Index plunging nearly 7%. Leaders like Qualcomm, Intel, and Micron collapsed, halting the year's AI computing power rally.

Facing AI market volatility, Wall Street's titans are deeply divided.

Michael Burry, the 'Big Short' trader who predicted the 2008 subprime crisis, now loudly bets against AI. He argues, 'The AI bubble is on the verge of bursting.' Stocks now defy logic, divorced from economic data or corporate earnings.

Legendary investor Paul Tudor Jones remains bullish, comparing AI to the 1995 internet commercialization and Microsoft's 1980s rise—both disruptive revolutions that drove long-term productivity gains and multi-year bull markets. He asserts, 'This AI bull market is only 50–60% complete, with 1–2 years of upside left.'

Some remain neutral, arguing 'this time is different'—AI is not equivalent to the dot-com bubble. However, they caution that most AI concept stocks are overvalued and lack fundamental support, despite AI's long-term potential.

MIIT data shows China's AI core industry exceeded 900 billion yuan by September 2025, with over 5,300 firms. AI applications are now key to industrial digital transformation. By 2026, AI large models will proliferate, accelerating global penetration across sectors.

Over the past two years, retail investors, lured by the profit potential of AI stocks, have piled into high-valuation AI, chip, and memory stocks, even using leverage. Following the herd at market peaks often leads to getting trapped.

A prevailing trend is the creation of workflow products to replace manual SOPs with AI. This has led to massive homogenization, as models share similar logic, rely on prompt engineering, lack data loops, and struggle to self-iterate.

The root dilemma? 'No clear path to profitability.' Model training and computing center deployment incur huge costs, yet revenues lag. While there is trust in AI capabilities, true productivity gains remain unrealized.

Note: Images sourced from the internet. Please contact us for removal if any infringement is found.

-END-

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle