High Leverage, High Prosperity, High Suspense: Unveiling the True Nature of Computing Power Leasing

05/26 2026

05/26 2026

559

559

In 2026, the expansion of AI applications has fueled a surge in the computing power industry, with the concept of 'computing power leasing' rapidly gaining popularity. As the supply of computing power cards and clusters remains limited, a number of companies specializing in providing such platform services have emerged in the market.

This is a market 'built on money': In May 2026, the spot rental price of NVIDIA's Blackwell series GPUs in cloud data centers reached $4.08 per hour, up 48% from two months earlier. The one-year lease contract price for H100 GPUs rose from $1.7 per card per hour in October 2025 to $2.35 in March 2026, a nearly 40% increase.

It is also an industry crucial for countless innovations: OpenRouter data shows that as of April 2026, the total global invocation volume of AI large model tokens has reached 27 trillion, up 18.9% month-over-month. ByteDance's Doubao consumes 120 trillion tokens daily on average, a 1,000-fold increase since its launch.

China International Capital Corporation (CICC) points out that the average daily token invocation volume in China exceeded 140 trillion in March 2026. 'When the penetration rate of Agents reaches 8%, their total token consumption is already comparable to that of Chatbots.'

But this is just the beginning, as the growth potential remains exponential with the widespread adoption of Agents. The market's focus lies more on the diversification of computing power leasing models—high procurement costs, high debt ratios, scarce channels, and AIDC. Companies labeled as 'computing power leasing' actually rely on different operational models. They must answer three questions:

Who is profiting from the boom itself, who is profiting from barriers, and who is chasing tomorrow with leverage.

1. Why is Computing Power Leased?

Computing power leasing is not a new concept. Since computing power relies on servers, the early model involved subleasing—platforms purchased GPUs and rented them out by the hour, with clients using them on demand, akin to vending machines in the cloud.

However, as AI applications become the primary consumers, the driving force behind the demand for computing power leasing has shifted from training-centric to inference-centric structural migration.

Computing power demand during the training phase is pulsatile. Training a large model may require thousands of GPUs running continuously for months, but demand drops sharply once training is complete. In contrast, demand during the inference phase grows continuously, directly correlated with user scale and invocation frequency. Every API call by OpenAI, Doubao, or DeepSeek consumes tokens. The more tokens are consumed, the greater the demand for inference computing power.

Numerous institutional estimates indicate that the current demand for inference computing power in the AI field is already 10 to 15 times that of the training phase. This multiple will continue to widen, as inference demand follows user growth, while training demand only follows model iteration cycles.

In the past, computing power leasing involved selling GPU runtime, with clients paying by the hour, and actual utilization depending on the client's technical capabilities. Now, the market is shifting toward a Token-sharing model—clients no longer care about how many hours are rented but focus on how many tokens are generated and tasks completed.

As a result, the industry is upgrading. Computing power lessors no longer need to provide only bare-metal computing power but also matching (supporting) scheduling, optimization, and model adaptation capabilities. While the scale of hardware procurement remains important, the output efficiency per unit of hardware has become equally or even more critical. At this point, the sophistication of hardware determines the baseline performance limit, explaining why some high-end GPU models in China sell out instantly upon listing on leasing platforms.

This tension is not a short-term inventory fluctuation but a symptom of rigid constraints on the supply side.

More importantly, the shift from 'selling computing power' to 'selling Tokens' represents a transition from a resource-based business to a service-based business. The moat of a resource-based business lies in who has more cards, while the moat of a service-based business lies in who can generate more Tokens with the same cards. The market remains optimistic about computing power leasing, believing that an 'innovator' will eventually break the conventional model.

2. Diversified Transformations Converge: Short-Term Logic Believable but Not Blindly Trusted

Since 2026, the concept of computing power leasing has surged in popularity. Data from the China Academy of Information and Communications Technology shows that the domestic computing power leasing market reached 68 billion yuan in the first quarter of 2026, up 62% year-over-year. This has prompted many companies to cross over into the field, announcing transformations in various forms.

For example, SiE Information, with a market capitalization of around 13 billion yuan, announced in mid-May plans to invest up to 20 billion yuan in financing leasing for computing power servers. Earlier this year, Yunneng Holding, a thermal power company, entered the data center (IDC) and computing power operations sector by increasing its stake in 'Innate Computing Power (Henan) Technology Co., Ltd.' for 1.1 billion yuan, moving toward 'computing-electricity synergy.'

Many similar cases exist in the market.

Xiechuang Data is a rising player in computing power, having transformed from consumer electronics manufacturing (originally a contract manufacturer of USB drives and cameras). In 2023, it entered server remanufacturing, followed by large-scale procurement of high-end GPUs for computing power leasing. The scale and speed of its transformation have been remarkable.

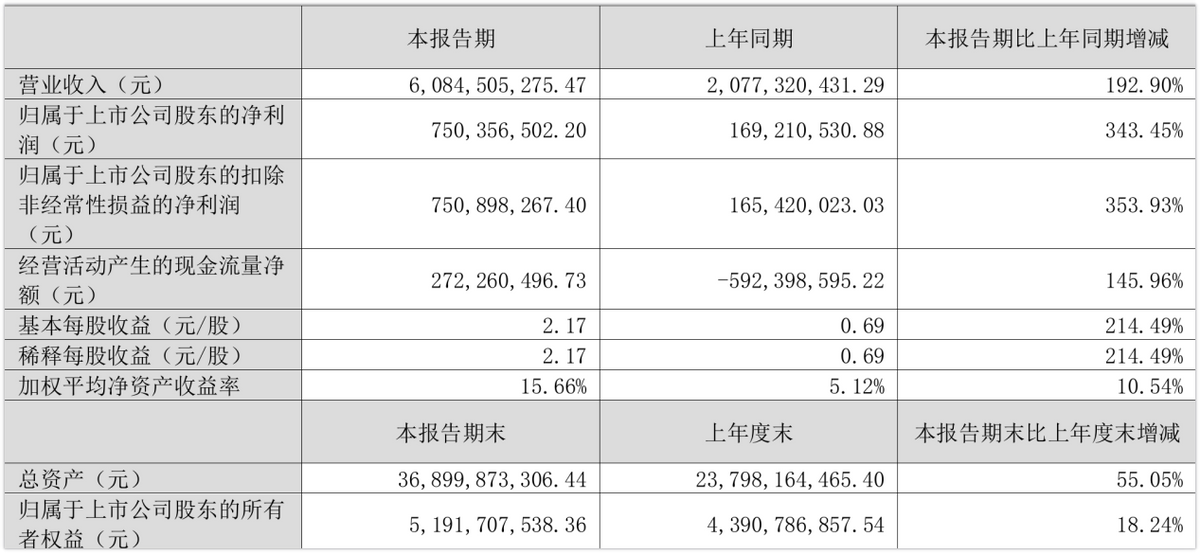

In 2025, its revenue from intelligent computing power products and services reached 2.761 billion yuan, up over 1,700% year-over-year. In the first quarter of 2026, revenue hit 6.085 billion yuan, up 193% year-over-year, with net profit attributable to shareholders reaching 750 million yuan, up 343% year-over-year.

However, given the capital-intensive nature of the computing power industry, Xiechuang Data has disclosed six large-scale procurement plans since 2025, with cumulative AI server purchases exceeding 32 billion yuan. By the end of the first quarter of 2026, its total liabilities reached 31.69 billion yuan, up 382% year-over-year, with the asset-liability ratio rising to 85.89%.

This strategy can be summarized as leveraging scale to drive market share. During periods of rising prosperity, newly added (newly added) computing power can quickly convert into revenue. In the first quarter, Xiechuang Data generated 272 million yuan in operating cash flow, up 146% year-over-year, indicating that invested capacity is indeed yielding returns.

However, its hidden weakness lies in the GPU refresh cycle, which is determined by upstream vendors. While older GPU generations still hold computing value after updates, companies must make additional investments. If new product commercialization pressures rental prices for previous-generation devices before their book depreciation is complete, actual profits shrink, creating a timing mismatch in the income statement and further amplifying asset investment pressure.

After NVIDIA's Blackwell, the Vera Rubin platform is slated to ship in the second half of this year, with updates planned for the next two years, meaning computing power leasing must also 'chase trends.'

Compared to Xiechuang Data, another industry leader, Litong Electronics, is the only domestic company with NVIDIA's Preferred-level AI Cloud Partner certification, giving it advantages in priority direct supply, long-term price locks, and stable quotas for high-end GPUs. It serves as a crucial channel for leasing, with some exclusivity.

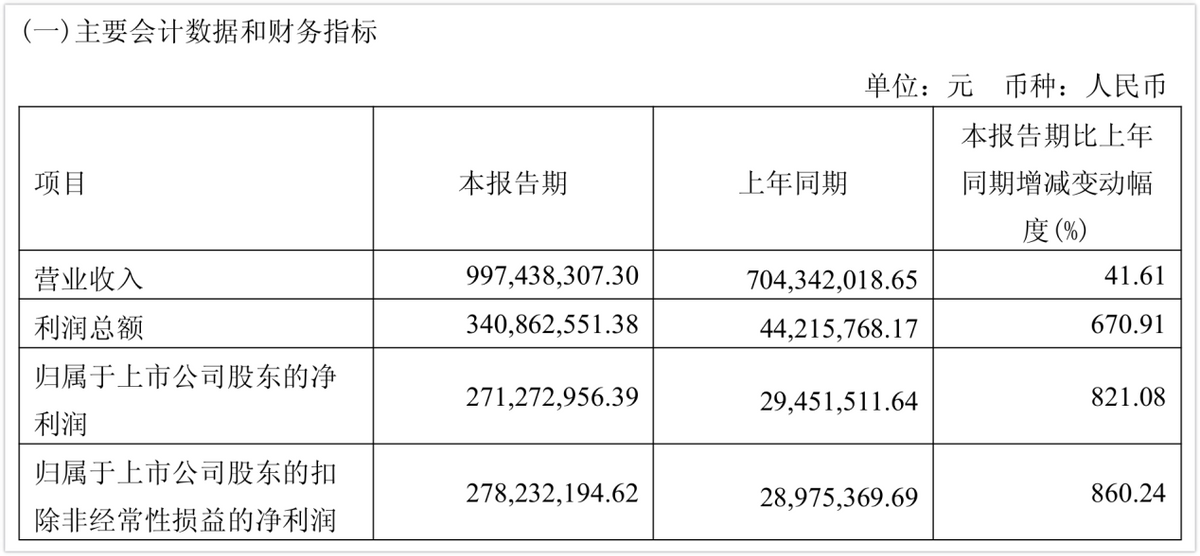

In the first quarter of 2026, Litong Electronics reported revenue of 997 million yuan, up 41.61% year-over-year, with net profit attributable to shareholders reaching 271 million yuan, up 821% year-over-year. Its gross margin stood at 46.23%, leading the computing power leasing sector. Contract liabilities reached 2.172 billion yuan, up 72-fold year-over-year, representing the value of signed but unexecuted leases.

Public information reveals that a 5 billion yuan, three-year contract with Tencent accounts for 80% of its computing power capacity, with 100% utilization and orders extending beyond 2027.

Compared to Xiechuang Data, Litong Electronics is smaller but has stronger barriers. Its moat lies not in capital investment scale but in a certification and the core client relationships it binds. It enjoys higher profit margins, more predictable cash flow, and lower sensitivity to technological iteration shocks, though its expansion speed is limited by NVIDIA's quota allocation rhythm.

Additionally, as 'selling Tokens' becomes the dominant business model in the AI sector, the concept of 'computing power factories' has emerged, with Runze Technology as a representative company.

Originally a traditional IDC hosting provider, Runze Technology is now upgrading to AIDC (Artificial Intelligence Data Center) operations. In 2025, its AIDC business revenue reached 2.51 billion yuan, up 73% year-over-year, with a gross margin of 48.5%. Its clients include leading domestic internet companies and mainstream AI customers. Leveraging its original business foundation, Runze Technology occupies land and power resources around first-tier cities, offering full-stack services from infrastructure to computing power scheduling.

Besides these players, companies like Hongxin Electronics and Topwise Information in the industry have formed their own models, binding different computing power sources to jointly participate in 'baking the cake' and 'dividing the cake.' The market generally tends to price these companies by equating high prosperity with high certainty and revenue growth with operational quality.

While 'tech stocks don't care about PE' is a universally applicable principle, different business models face entirely different risk types within the same prosperity cycle. Leveraged expansion bears financial risks and asset depreciation risks, qualification barriers face policy and technological route risks, and hardware sales confront gross margin pressures and payment cycle risks. Ultimately, what determines who can navigate the cycle are the size and manageability of their respective risk exposures.

3. The Sword of Damocles: What Is the Moat of 'Leasing'?

High industry prosperity easily creates the illusion that growth will persist indefinitely and rental prices will remain firm, but the fundamental nature of manufacturing dictates that supply will eventually catch up. Thus, two viewpoints exist in the market regarding computing power: one argues that short-term computing power supply cannot meet demand, while the other contends that the market has already priced in potential gains, leading to a bubble.

How can we determine whether computing power leasing—or the entire industry—is on the right track? Two key directions warrant attention.

First is GPU cluster utilization. Why have industries like CPO and fiber optics also gained traction since last year? Because they directly relate to signal transmission efficiency and loss, which limit computing power ceilings, making internal and inter-cluster communication crucial.

Unoptimized GPU clusters average only 20-30% utilization, which can be boosted to over 70% through computing power pooling and intelligent scheduling. Even with identical hardware configurations, effective output can differ by two to three times based on usage efficiency. The core competitiveness of computing power leasing is shifting from the quantity of cards to their utilization efficiency.

When supply is tight, having cards guarantees profitability, and low efficiency can be offset by high rental prices. However, as global GPU supply gradually catches up with demand, once rents decline from peak levels, efficiency differences will directly translate into profit disparities. Clusters with 70% utilization remain profitable, while those with 20% utilization incur losses.

Second is the differentiation effect of business models, including the rise of concepts like 'Token factories' and 'computing power factories,' which are tied to these changes.

When clients pay by Tokens rather than hours, the actual revenue of computing power lessors depends on the number of Tokens generated per unit of time. The same GPU running a deeply optimized inference framework can output several times more Tokens than one running an unoptimized bare model. Under Token-based pricing, while computing cards have theoretical output limits, varying production ratios lead to different profit margins for computing power leasing companies.

In summary, computing power leasing is a typical (typical) prosperity-driven industry. Current rental levels, rapid growth in contract liabilities, and capital expenditure guidance from major clients all point to short-term high certainty. However, high certainty does not imply low risk. Earnings reports reveal past performance, while balance sheets and competitive landscapes help anticipate future outcomes.

Before AI becomes a 'universally owned' application, this state of coexisting certainty and uncertainty will persist, advancing in a spiral motion.

Source: Songguo Finance

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle