Why Is a 'Non-Sexy' Robot Dog Company Worth 13.9 Billion Based on Its IPO from DeepCloud Robotics?

05/26 2026

05/26 2026

570

570

Selling Robot Dogs to the Top of the Global Market—What Comes Next?

Just a few days ago, the Shanghai Stock Exchange officially accepted the STAR IPO application from Hangzhou DeepCloud Robotics Co., Ltd.

This most low-profile company among the 'Hangzhou Six Little Dragons' plans to raise 2.503 billion yuan, with CITIC Construction Investment Securities as the sponsor. Based on an issuance ratio of no less than 18%, its pre-IPO valuation has reached approximately 13.9 billion yuan. Combined with DeepCloud's operating revenue in 2025, its PS ratio is approximately 41 times.

How exaggerated is this figure? Take Unitree Robotics, a leading robotics company, as an example. In 2025, Unitree achieved 1.708 billion yuan in operating revenue and 288 million yuan in net profit attributable to shareholders, up 204.29% year-on-year, with non-recurring profit and loss attributable to shareholders reaching 600 million yuan. However, DeepCloud, with less than one-fifth of Unitree's operating revenue and less than one-tenth of its net profit, has secured a PS ratio nearly twice that of Unitree.

So, the question arises: Why is the market willing to pay such a high premium for the 'second-place' company?

01 The 'Scale Paradox' of Quadruped Robots

To understand DeepCloud's 41-times PS valuation, one must first recognize an industry reality: For a long time, 'making money by selling robot dogs' has been a difficult 'puzzle' to solve globally.

For instance, Boston Dynamics' Spot, the world's most famous robot dog, sells for $75,000 but sold only a few hundred units in 2020, its debut year. ANYbotics from Switzerland, which secured over $150 million in financing in September last year and plans to launch its next-generation ANYmal X this year, is still 'burning cash.'

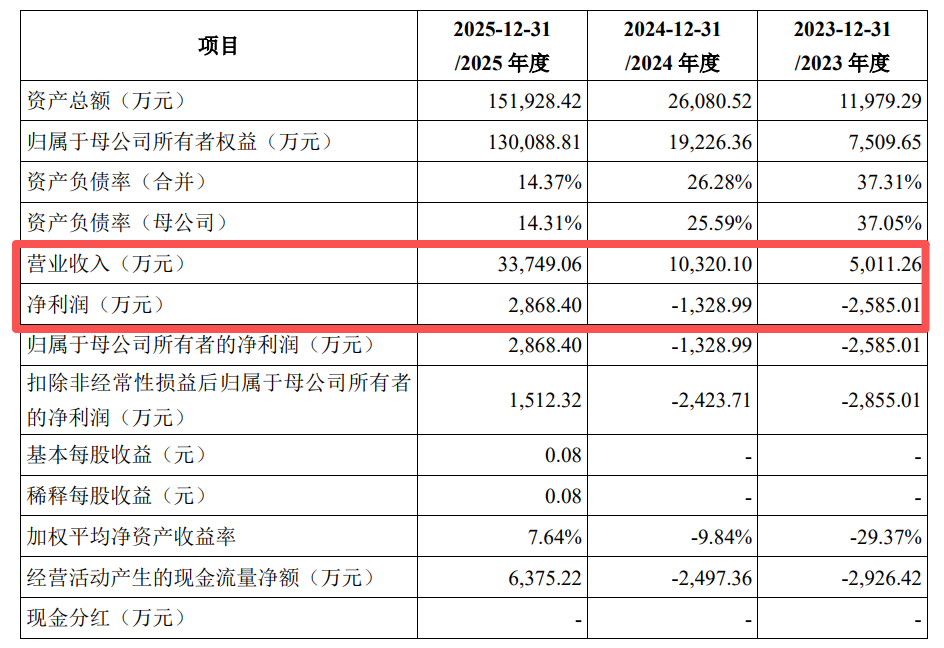

In contrast, DeepCloud reported net profits attributable to shareholders of -25.85 million yuan, -13.29 million yuan, and 28.68 million yuan from 2023 to 2025, achieving its first annual profit in 2025.

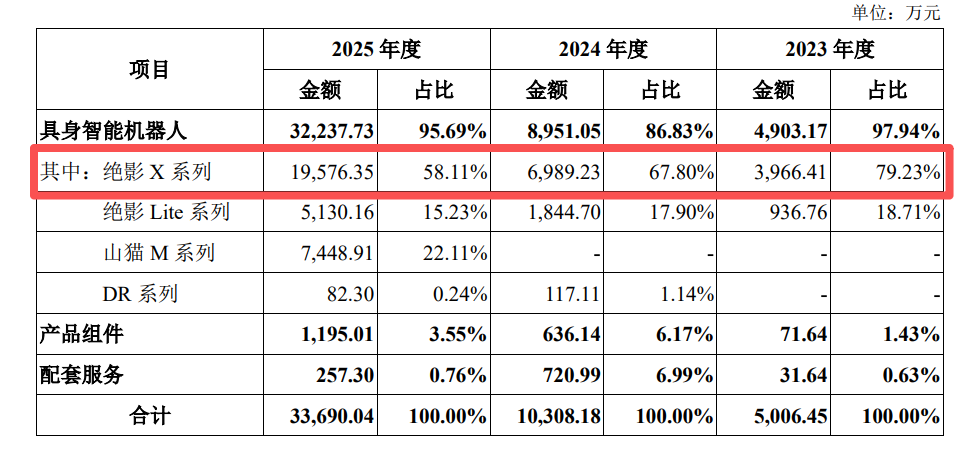

Quadruped and wheeled-legged robots contributed 95.45% of its revenue. In other words, DeepCloud is one of the few companies globally that profits by selling robot dogs.

Moreover, according to Frost & Sullivan data, in 2025, DeepCloud ranked first globally in industry application revenue for quadruped robots and second in overall revenue for quadruped robots. How did it achieve such 'excellent results' with just quadruped robots? The answer may lie in DeepCloud's prospectus.

According to prospectus data, in 2025, DeepCloud's revenue from quadruped and wheeled-legged robots was 322 million yuan, with 258 million yuan from industry applications, 47.15 million yuan from research and education, and 16.3 million yuan from commercial services.

DeepCloud's best-selling product is the industrial-grade quadruped robot X Series, used in power inspection, emergency firefighting, industrial inspection, police security, public infrastructure inspection, patrols, and research and education. In 2025, 681 units were shipped at a unit price of 287,500 yuan, generating 196 million yuan in revenue and contributing more than half of the company's revenue.

To understand the uniqueness of this revenue structure, let's compare it with Unitree Robotics. In 2025, Unitree's quadruped robot revenue totaled 690 million yuan, with 240 million yuan from commercial consumption, 220 million yuan from research and education, and 230 million yuan from industry applications.

In terms of revenue structure, Unitree Robotics follows a 'broad' approach, using consumer-grade products to gain market visibility and then feeding back into other areas. In contrast, DeepCloud chooses to 'go deep,' exchanging high-value, highly customized B-end solutions for deep customer relationships.

With this B-end-focused strategy, DeepCloud has deployed its robots in over 100 substations for State Grid and China Southern Power Grid in the core sector of power inspection, accumulating over 1 million kilometers of inspection mileage, achieving an overall recognition accuracy of 96.5%, and an average fault-free operation time exceeding 1,000 hours, successfully building its moat.

However, the flip side of the coin is evident. With over 10,000 substations nationwide, DeepCloud has penetrated less than 2% of the market. The issue is not insufficient market space but the natural constraints on B-end scenario expansion due to customer procurement cycles and budget processes, which prevent explosive growth like consumer electronics.

Additionally, another structural constraint in the quadruped robot industry lies in the overall market size. Frost & Sullivan data shows that in 2025, the Chinese embodied AI market for quadruped robots reached 1.5 billion yuan, while humanoid robots reached 1.4 billion yuan. However, by 2030, the former is expected to grow to 20.6 billion yuan, and the latter to 47.9 billion yuan, more than double the former.

Thus, the question remains: Is the market's current 41-times PS valuation for DeepCloud based on the scarcity of its 'global first' status in quadruped robots, or is it a bet on its ability to successfully enter the larger humanoid robot market?

The answer likely leans toward the latter.

02 'Lagging Behind' in Humanoid Robots

In stark contrast to the quadruped robots that drive its performance, DeepCloud's layout (layout) in humanoid robots lags significantly.

Currently, it has launched only two humanoid robot models, DR01 and DR02, both still in the technical verification stage. According to prospectus data, DeepCloud sold only four DR series humanoid robots over two years, generating 823,000 yuan in revenue, accounting for just 0.24% of total revenue. In contrast, Unitree shipped over 5,500 humanoid robots during the same period, becoming its largest revenue source.

Zhu Qiuguo, founder of DeepCloud, explained candidly: 'We can't keep up. With limited resources, we hope to solve the quadruped robot issues first.'

This is a pragmatic judgment but also exposes a structural weakness: DeepCloud has little presence in the humanoid robot sector, the most closely watched by capital markets.

However, this does not mean DeepCloud is indifferent to the attractive 'cake' of humanoid robots. In fact, the company launched DR01 as early as August 2024 and released DR02 in October 2025.

The latter is positioned as the 'world's first industry-grade all-weather humanoid robot,' featuring an IP66 protection rating and a wide operating temperature range of -20°C to 55°C, suitable for power operations, emergency firefighting, police security, industrial production, and other outdoor scenarios, continuing DeepCloud's 'scenario-defined product' approach.

The issue lies in the completely different commercialization paths of humanoid and quadruped robots.

Quadruped robots can first succeed in a single scenario like power inspection and then gradually expand. However, humanoid robots face the requirement for generalization, needing to prove themselves in more diverse scenarios.

Zhu Qiuguo stated in an interview: 'Currently, only some partners have received prototypes of our humanoid robot products, which have not yet been mass-marketed. We expect formal sales to begin in the second quarter of 2026.'

From prototypes to scalable delivery and then to significant revenue contribution, DeepCloud will need at least 1–2 more years. This means that from 2026 to 2027, DeepCloud's revenue growth will still heavily rely on quadruped robots.

However, the global quadruped mobile robot market, with sales of $2.3 billion in 2025 and expected to exceed $7.1 billion by 2032 at a compound annual growth rate of 17%, lags far behind humanoid robots. If DeepCloud cannot transition before the next growth curve arrives, it will face a 'track-switching' gap risk.

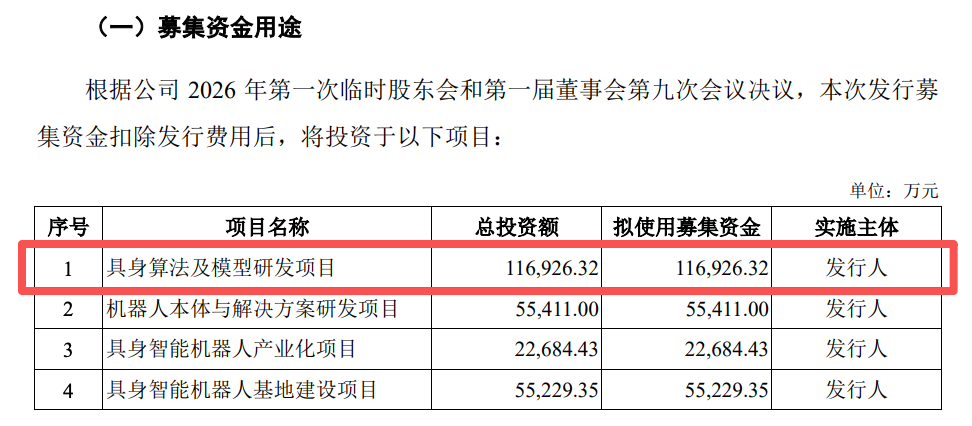

Perhaps aware of this crisis, DeepCloud plans to raise 2.503 billion yuan through its IPO. Among the four fundraising projects, the largest expenditure is 1.169 billion yuan for embodied algorithm and model R&D, accounting for 47% of total funds raised. This is followed by 554 million yuan for robot ontology (body) and solution R&D, 227 million yuan for industrialization projects, and 552 million yuan for base construction.

From the fundraising directions, it is clear that DeepCloud is attempting to address its shortcomings in the 'brain' layer.

However, the current core competitiveness of embodied AI is shifting from 'motion control' to 'environmental understanding and autonomous decision-making.' In the field of embodied AI large models—the true 'brain'—DeepCloud lacks both deep technical accumulation and landmark application cases, with much ground to cover.

03 DeepCloud Is Not Yet Ready to Celebrate

Going public will accelerate DeepCloud's investments in algorithms, models, bodies, solutions, and production capacity. However, before entering the capital market, the company had already received intense capital support in the primary market.

Tianyancha information shows that DeepCloud has completed eight rounds of financing. Its most recent financing was a Pre-IPO round on December 25, 2025, where the National Artificial Intelligence Industry Investment Fund and JD.com jointly invested hundreds of millions of yuan just two days after DeepCloud submitted its listing tutoring (tutoring) application.

Securing continuous heavy investments from 'national team' and industrial capital is inseparable from the continuous improvement of a key metric: gross profit margin.

From 33.48% to 38.76% and then to 52.83% in 2025, the gap between DeepCloud's and Unitree's gross profit margins has narrowed to less than 10 percentage points. However, while these figures look impressive, a closer look raises questions about the quality of DeepCloud's profitability.

First, of DeepCloud's 28.68 million yuan in net profit, approximately 13.56 million yuan came from government subsidies. After deducting non-recurring items, net profit attributable to shareholders was only 15.12 million yuan.

This means that without subsidies, DeepCloud is still some distance from true profitability. The company itself admits in its prospectus: 'The government subsidies we receive are relatively large and play a positive role in our profitability.'

Second, the continuous improvement in DeepCloud's gross profit margins in recent years is partly due to cost reductions from scaled procurement driven by increased sales of the X Series and Lite Series, as well as a higher proportion of high-value-added products like X30 and X30 Pro. However, both factors are difficult to replicate indefinitely. Supply chain cost reductions have limits, and as sales increase, customer bargaining power will strengthen.

Moreover, R&D investment deserves greater attention. According to the prospectus, DeepCloud's R&D expenses were 32.18 million yuan, 38.21 million yuan, and 84.3 million yuan during the period, but its R&D expense ratio dropped from 64.22% in 2023 to 24.98% in 2025.

After a significant decline, the R&D expense ratio now aligns with the industry average. Currently listed robot ontology (body) companies UBTECH and Dobot had R&D expense ratios of 25.36% and 23.23%, respectively, in 2025. This suggests that DeepCloud has moved from an early technology investment phase to a relatively stable R&D stage. However, considering the company still has significant shortcomings in humanoid robots and embodied large models, whether this level of R&D intensity is sufficient remains questionable.

However, improving gross profit margins and declining R&D expense ratios do not fully explain the valuation logic. What truly determines whether DeepCloud can sustain its 41-times PS valuation is a more fundamental question: Can DeepCloud's client structure evolve from 'highly concentrated' to 'diversified'?

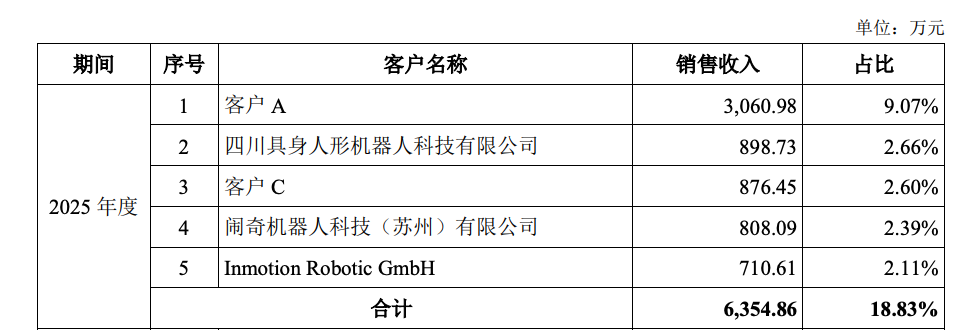

Although DeepCloud's top five customer sales ratio dropped from 47.12% in 2024 to 18.83% in 2025, significantly reducing customer concentration risk, a closer look at the customer list reveals lingering issues.

According to prospectus data, three of the top five customers in 2025 were other robotics companies: Sichuan Embodied Humanoid Robotics Technology Co., Ltd., Naoqi Robotics Technology (Suzhou) Co., Ltd., and Inmotion Robotic GmbH. This means a significant portion of DeepCloud's revenue comes from same kind (peer) robotics companies for R&D, testing, and demonstration purposes rather than from true end-users.

In contrast, Unitree's customer structure is relatively balanced across research and education, commercial consumption, and industry applications, with commercial consumption being the fastest-growing segment. This diversified customer base gives Unitree stronger resilience against single-industry fluctuations.

DeepCloud is clearly aware of this issue. The prospectus shows that the company is expanding into new scenarios like industrial operation and maintenance and logistics transportation, but so far, revenue from these areas remains insignificant. Evidently, transitioning from single-scenario dependence to multi-industry coverage is not a quick fix, and this is precisely the most critical factor for capital markets in assessing its long-term value.

In summary, in today's embodied AI sector, which is shifting from 'showcasing technology' to 'getting the job done,' DeepCloud is one of the few companies that has truly deployed robots in substations and firefighting sites. It has experience in 1,200 different industry scenarios, a 52.83% gross profit margin, and a proven set of engineering capabilities.

However, the fragility of this valuation is equally clear. Lagging in humanoid robots, high customer concentration, and limited market ceiling for quadruped robots—each variable could trigger a valuation correction. Faced with these uncertainties, DeepCloud's IPO is not just a fundraising event but a 'pop quiz' on whether its 'B-end deep cultivation' model can gain recognition from secondary markets.

The bell is about to ring, and the market will give its answer.

* The picture is from the Internet. Please contact us for deletion if there is any infringement.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle