From Selling Computers to Selling AI: How Far Has Lenovo Come?

05/26 2026

05/26 2026

632

632

"Revenue to exceed $100 billion in two years," "net profit margin to double," and "full transformation into an AI-native company"—these are the strategic goals set at Lenovo Group's 2026/27 fiscal year pledge conference held in Beijing on April 1.

The just-concluded 2025/26 fiscal year (April 1, 2025–March 31, 2026) has also been defined as Lenovo's "first year of the new AI decade."

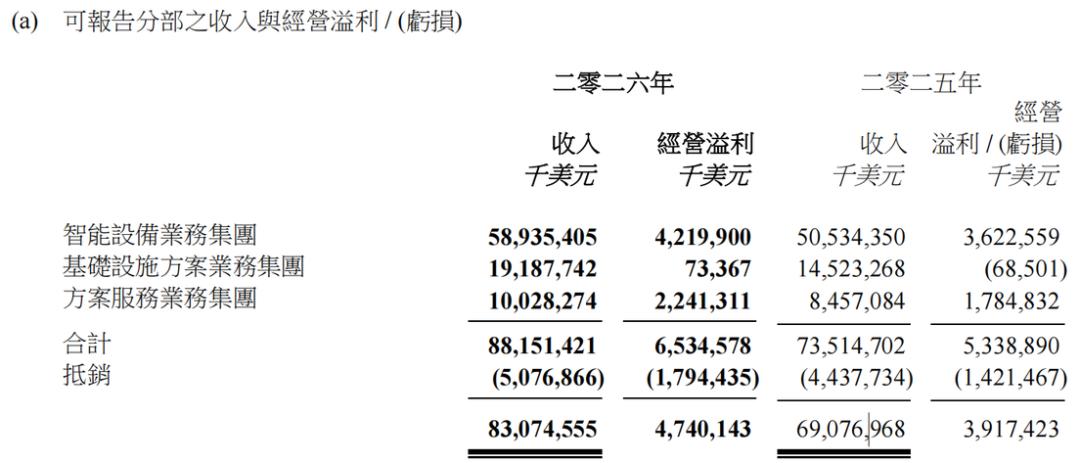

In this year, Lenovo Group achieved a revenue of RMB 589.9 billion (approximately $83.1 billion), a 20% year-on-year increase, with adjusted net profit rising by 42% year-on-year. For the first time in history, all three business groups—IDG (Intelligent Devices), ISG (Infrastructure Solutions), and SSG (Services & Solutions)—achieved full-year profitability simultaneously.

More critically, the structural shift is evident. The proportion of revenue from non-PC businesses has been rising year by year. Annual AI-related revenue surged by 105% year-on-year, accounting for 33% of total revenue, with this proportion further increasing to 38% in the fourth fiscal quarter.

On the day the financial results were released, Lenovo Group's stock price closed up 19.77%.

While this financial report represents significant progress in Lenovo's transformation, it also reveals vulnerabilities, such as ISG's shaky profit foundation, soaring storage costs, industrial migration, and industry competition, all of which pose real constraints.

I. Structural Transformation: No Longer Just Selling Computers

The "computer-selling" Lenovo is becoming a thing of the past.

This trend has become increasingly clear with the release of Lenovo Group's 2025/26 fiscal year results.

IDG, the business segment most familiar to the outside world—selling PCs, smartphones, and tablets—generated $58.9 billion in revenue for the full fiscal year, contributing about two-thirds of total revenue. However, this segment's growth rate was 17%, the lowest among the three businesses, and its share of total revenue also declined.

Correspondingly, the proportion of non-PC businesses has approached half of total revenue.

ISG's revenue reached $19.2 billion, with a growth rate exceeding 32%, leading the three segments. SSG's revenue surpassed $10 billion, growing by 19% and maintaining double-digit growth for 20 consecutive quarters.

In other words, the faster-growing segments are no longer Lenovo's most "traditional" businesses.

This structural change has profoundly impacted profits.

In previous fiscal years, Lenovo's profit landscape was typically characterized by "two segments making money and one burning cash"—IDG and SSG contributed profits, while ISG incurred losses. In FY25/26, this pattern was broken for the first time.

IDG's full-year operating profit was approximately $4.22 billion, with an operating profit margin of 7.2%, still the largest contributor to profits, accounting for about 64.6% of total operating profit.

SSG's full-year operating profit was approximately $2.24 billion, with an operating profit margin of 22.4%. This segment, accounting for less than 12% of group revenue, contributed one-third of operating profit, making it the most stable high-margin source in Lenovo's profit statement.

ISG's full-year operating profit was $73 million, turning from a loss of $68.5 million in the same period last year to profitability, with an operating profit margin of about 0.38%. Looking at the trend, the operating profit margin reached 3.58% in the last quarter, showing a clear improvement trend.

SSG anchoring profits, IDG providing scale, and ISG shifting from a "drag" to a "positive contributor" are the core changes in the profit structure of this annual report.

Coupled with the increased proportion of AI revenue, AI has transformed from an abstract strategic narrative into a separately measurable revenue line in the financial report, collectively forming the logic behind Lenovo's revaluation.

However, the transformation is not entirely secure. The goal of achieving $100 billion in revenue in two years implies an average annual revenue growth rate of 10%. While not overly aggressive, uncertainties remain.

First is the historic surge in memory prices.

TrendForce data shows that global generic DRAM contract prices rose by 90% to 95% quarter-on-quarter in the first quarter of 2026, with PC DRAM prices surging by 110% to 115% in a single quarter and DDR5 spot prices rising by over 300%. Some DDR4 particles soared from $3.2 at their 2025 low to $15, a cumulative increase of 369%.

Cost pressures are directly reflected at the device level. According to TrendForce estimates, based on a mainstream notebook with a suggested retail price of $900 in Q1 2025, by Q1 2026, the proportion of memory and solid-state drives in material costs had risen from 15% to 30%. Combined with rising CPU prices, the three components' combined proportion jumped from 45% to 58%. To maintain profit margins across the supply chain, this product would need a price increase of nearly 40%.

Lenovo's COO openly acknowledged before the financial results announcement: "The cost pressure from memory and solid-state drives is greater than ever."

Lenovo's response was to stockpile inventory. CFO Wong Wai Ming previously revealed that storage inventory at the end of the third fiscal quarter was equivalent to 7-8 months of usage, far exceeding the industry average of 2-3 months.

However, stockpiling only delays pressure; it does not eliminate it.

As inventory is gradually depleted, cost pressures will fully hit the cost side in Q1 FY27. Whether the fourth fiscal quarter's gross margin of 16.4% can be maintained will be a true test for Lenovo.

Tariff uncertainty is another variable. The Americas region accounts for about 34% of Lenovo's total annual revenue, making it the largest regional market. A significant portion of Lenovo's production bases are in China, and the direction of tariff policies will affect its sales performance in the North American market.

As Yang Yuanqing said, in the first half of the year, Lenovo must address dynamic tariff pressures, while in the second half, it must tackle challenges posed by component shortages.

II. IDG: Can the 17% Growth Rate Be Sustained?

IDG grew by 17% year-on-year, with PC and smart device business revenue increasing by 26% year-on-year, marking the highest growth rate in five years. In the fourth fiscal quarter, Lenovo's global PC market share reached 24.4%, up 1.3 percentage points year-on-year, the highest in 15 years; high-end PC shipments accounted for 50%, a 29% year-on-year increase.

Discussing IDG inevitably involves the PC business.

Against the industry backdrop, the global PC market recovered in 2025, with total shipments reaching approximately 279 million units, a year-on-year increase of about 9%. Lenovo's growth rate during the same period significantly outpaced the industry average. IDC data shows that Lenovo shipped 70.85 million PCs in 2025, a 14.6% year-on-year increase.

This indicates that Lenovo is not only benefiting from the industry recovery but also capturing market share from competitors in the existing market.

However, the PC industry is mature, with global annual shipments fluctuating between 250 million and 280 million units over the long term. Can Lenovo sustain such growth?

First, let's examine the reasons behind the PC market recovery.

The most rigid driver came from Microsoft. On October 14, 2025, Microsoft officially ended support for Windows 10. Currently, about 40% of PCs worldwide still run Windows 10, and these devices face a cutoff in security updates. For commercial clients, replacing devices is mandatory. Multiple industry analysts believe that "market growth is primarily driven by operating system replacements."

The second factor is the natural replacement cycle of devices purchased during the pandemic. A large number of PCs bought during the 2020-2021 pandemic, with a typical commercial device replacement cycle of 3-5 years, are now entering a concentrated replacement phase. This demand has a clear time window, but it will not remain open indefinitely.

The third factor is AI PCs. At CES 2025, Jensen Huang noted that AI PC sales in 2024 were underwhelming because terminal-side AI ecosystem investments lagged far behind those in the cloud, leaving demand unmet.

In other words, enterprises are currently purchasing AI PCs more as a "forward-looking configuration" to avoid falling behind in the next 1-2 years, rather than due to immediate, essential AI PC use cases.

The first two factors are cyclical; the third is the endogenous variable driving PC sales growth.

Whether AI PCs can independently take over and how quickly their penetration rate will rise depend on multiple factors, such as the price-performance match and the availability of non-local applications.

Gartner predicted in late 2025 that AI PCs would achieve a 55% penetration rate in 2026, optimistic about an AI PC-driven replacement cycle. However, due to rising BOM (bill of materials) costs, Gartner later revised its forecast, stating that a 50% market penetration rate would not be achieved until 2028.

The profitability situation also requires closer examination.

AI PCs do command higher terminal prices, but their costs are also higher.

Industry data shows that AI PCs with similar configurations are 20% to 40% more expensive than traditional PCs, with commercial models generally priced above $1,000. However, AI PCs require additional AI-specific hardware like NPUs, raising material costs.

Given this, with continuous product structure upgrades and high-end PC shipments accounting for 50% of the total, IDG's operating profit margin of 7.2% remained almost unchanged from the previous fiscal year.

Considering the soaring storage costs, maintaining a 7.2% profit margin in such an environment is indeed commendable. However, this also underscores that AI PCs' current contribution is more about holding the line rather than opening up new growth frontiers or re-establishing themselves as a growth engine.

III. ISG: Turning Profitable, But Still Thin

ISG's return to profitability is a significant turning point in Lenovo's AI narrative.

Where did this turning point come from?

First, global AI capital expenditures have entered a blowout phase. In 2025, the combined AI capital expenditures of North America's four major cloud service providers exceeded $340 billion, a 68% year-on-year increase, with further growth expected in 2026. Domestic cloud providers, including ByteDance, Tencent, and Alibaba, have also accelerated their AI infrastructure deployments.

This explosive growth in demand directly boosted Lenovo's ISG business, with full-year AI server revenue surging by over 50% year-on-year and AI server backlog orders reaching $21 billion by the fiscal year-end.

More importantly, this round of procurement is no longer a simple volume increase for standardized servers. Public information shows that NVIDIA's GB300 NVL72 rack solution began shipping in the fourth fiscal quarter, with the next-generation platform based on the Rubin architecture set to launch in the second half of the year. This means Lenovo has upgraded from selling standardized servers to delivering rack-level systems, officially entering NVIDIA's latest supply chain.

Second, enterprise clients are starting to pay for AI. Traditional enterprises in banking, manufacturing, and other sectors are also deploying AI servers, with E/SMB business margins for these clients far exceeding those of CSPs (cloud infrastructure providers). For example, in the third fiscal quarter, Lenovo's E/SMB business in China grew by 52% year-on-year, significantly outpacing CSP growth.

However, profits remain thin.

The full-year operating profit margin was only 0.38%, still very low in the server industry. For comparison, Dell's ISG division achieved an operating profit margin of 14.8% in its most recent fiscal quarter. Lenovo's ISG still has a long way to go to reach industry maturity.

Thin profits are related to Lenovo's customer mix.

ISG's revenue is primarily driven by CSP orders, which are large in volume but extremely low in gross margin. In other words, for ISG to truly stabilize profitability, the proportion of E/SMB revenue is more critical than the size of CSP orders.

AI demand is shifting from "training" to "inference," a trend affecting both of ISG's business lines.

This is not a unique opportunity or risk for Lenovo's ISG but a structural shift facing the entire AI infrastructure industry. In 2026, the total AI inference computing power of North America's five major CSPs is expected to increase nearly 1.22 times, far outpacing the 56% growth in training computing power.

For Lenovo, this trend has both positive and negative implications.

On the positive side, expanding inference demand means more traditional enterprises will deploy AI servers, precisely E/SMB's target market. If this trend continues, E/SMB's proportion in ISG revenue is expected to rise naturally, improving the overall profit structure.

Additionally, inference has greater memory demands, and Lenovo's acquisition of Israeli high-end storage company Infinidat in April provides a card for future profit structure optimization.

On the negative side, inference servers typically do not require top-tier GPUs, leaving less room for brand premium pricing. Moreover, cloud providers are more inclined to use in-house chips (such as Google's TPU and Amazon's Trainium) or switch to lower-cost ODM white-label servers during the inference phase. These factors may squeeze revenue for integrators like Lenovo.

Meanwhile, Huawei has formed a closed loop in the trusted IT market with its full-stack self-developed Ascend AI chip ecosystem, while Inspur Group has deep accumulations in the internet and government sectors. Lenovo still relies heavily on external chips like NVIDIA, putting it at a disadvantage in terms of cost and supply chain security.

ISG's return to profitability proves that Lenovo has secured a seat at the table in the AI infrastructure wave, but new challenges lie ahead. Only by navigating these challenges can Lenovo solidify its position.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle