Alipay Completes the Final Piece of the Agent Economy Puzzle

05/28 2026

05/28 2026

556

556

By Jide

Edited by Ziye

In 2026, Agents have finally come into their own.

Since OpenClaw swept across the globe, sparking a vibrant ecosystem of AI innovation among developers (often referred to as AI 'shrimps'), AI has transitioned from simple 'chatting' to actually 'getting things done.' Amid a nationwide trend of cultivating AI capabilities, AI Agents have emerged as indispensable 'work buddies' for professionals. McKinsey predicts that by 2030, global revenue from the commercial orchestration of agents will soar to a staggering $3 trillion to $5 trillion.

However, Agents find themselves on one side of a chasm, with commercial closure on the other, separated by the critical barrier of 'payment.' Users are hesitant to let AI handle their finances, developers struggle to receive payments from AI, and that final 'confirm payment' step still requires human intervention.

The history of commerce has consistently demonstrated a fundamental principle: technology must first mature, pathways must be established, and only then can the market truly flourish. The bottleneck lies not in technological limitations but in the absence of trust and transactional pathways. Trust doesn't emerge spontaneously; it requires a bridge—one end anchored in user authorization of Agents and the other in the Agent's ability to execute tasks in the real world.

On May 26, at the AI Payment Industry Ecosystem Conference, Alipay unveiled its solution: 300 million transactions, 95% coverage of general-purpose agents, and the world's first large-scale, commercially available AI-native payment infrastructure. This achievement is supported by a comprehensive bridge that spans from the underlying layers to the terminal.

Simultaneously, the newly released AI Wallet and Token Pay cater to users' need for control over AI spending and large model companies' demand for Token-based payment services, respectively.

More than just a product launch, this marks the 'bridge-opening ceremony' for the Agent economy.

1. The Agent Economy: All Components in Place, Except the Bridge

Payment is not merely the endpoint of a transaction; it is the bedrock of commerce.

Reflecting on the past two decades, every major surge in China's internet sector has been underpinned by a shift in payment systems:

In 2003, escrow transactions resolved trust issues between strangers, propelling the e-commerce industry to new heights. In 2011, QR code payments digitized offline transactions, fueling the rise of O2O, the sharing economy, and mobile e-commerce.

The pattern is clear: new scenarios drive the demand for new infrastructure, which in turn spawns new industries.

The situation with Agents is even more complex. The entity executing transactions shifts from humans to AI, the transaction unit changes from 'orders' to 'intentions,' and transaction frequency transitions from discrete to continuous. Will users trust Agents to spend money on their behalf? Will merchants accept transaction instructions initiated by AI?

Traditional payment systems are ill-equipped to address these questions. Only a new infrastructure for the payment industry can bridge this gap.

Players worldwide are exploring solutions. Some are still in the planning phase, while others have begun implementation, each following its own logic:

The overseas approach leans toward 'protocols + open access.' Visa and Mastercard, guarding their clearing networks, issue 'temporary passes' to AI, launching pilots in Asia-Pacific, Europe, and the Middle East. Stripe and OpenAI jointly built the ACP protocol, leveraging a strong developer-side presence—processing $1.9 trillion in annual transactions and covering 86% of the AI 50 companies.

However, few have achieved scale in real-world scenario validation and data closure at the end-consumer level.

Alipay has taken a different path: laying the groundwork from underlying protocols to upper-layer applications, from users to merchants, and from online to offline—all simultaneously.

The intensive iterations over the past dozen months illustrate this path: in April 2025, it launched China's first payment MCP Server; in June, it introduced AI tipping; in September, it rolled out AI subscription payments and premiered AI Pay; in January 2026, ACT 1.0 was released; in March, it introduced payment integration Skills; in April, ACT upgraded to 2.0, and AI Collection officially went live; in May, the AI Wallet and TokenPay made their debut.

The result: 300 million real transactions, covering 95% of general-purpose agents. The disclosure of these figures itself proves the depth of the ecosystem's closure—currently, only Alipay worldwide can present AI payment data at the hundred-million level.

AI entrepreneurship is inherently borderless, and Agent payments are naturally cross-border. It is understood that Ant International has already collaborated with multiple large model vendors in global markets to advance end-to-end AI shopping and agent payment solutions, integrating various payment methods such as e-wallets and bank cards to enable automatic cross-terminal and cross-scenario deductions.

This also means that Alipay's AI payment infrastructure has laid the groundwork at the core level to handle global agent commercial settlements.

2. Alipay's Four-Layer Infrastructure: The Bridge Is Now Open to Traffic

Integrating agents into the existing payment system is more challenging than anticipated.

Identity vacuums, misinterpreted intentions, unaccountable responsibilities, and ecological silos—ultimately, these stem from systemic pathway barriers.

The full-link infrastructure unveiled by Alipay is designed to level these obstacles.

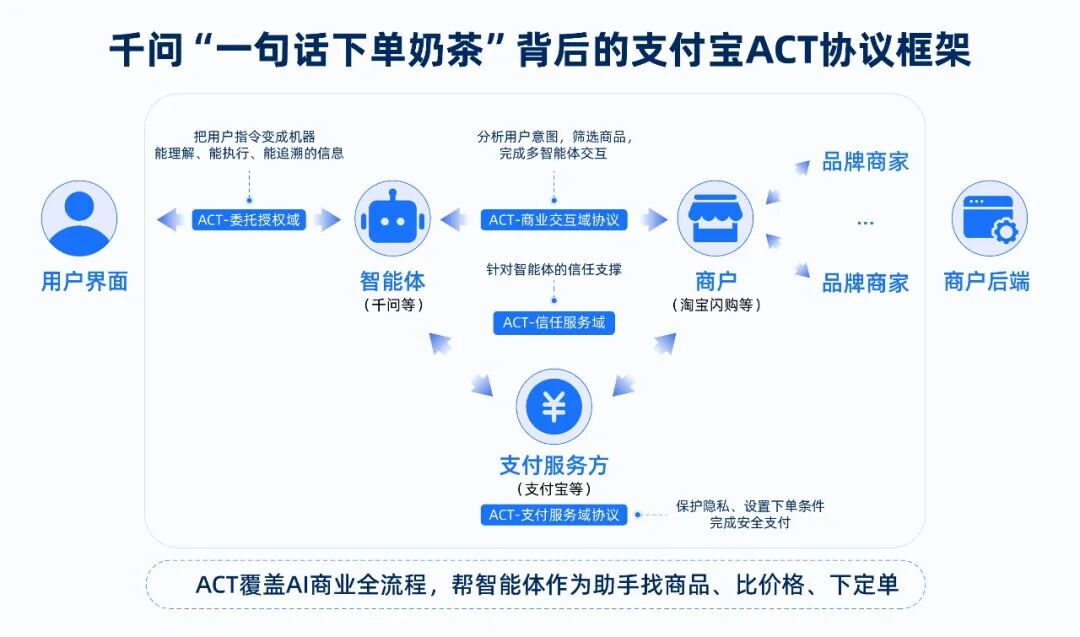

In the bridge's structure, the protocol layer forms the foundation—the bridge piers. The ACT protocol (Agentic Commerce Trust Protocol) is China's first open framework for Agent commerce, jointly launched by Alipay and ecosystem partners.

The 1.0 version, in collaboration with QianWen, Taobao SnapUp, Rokid, and others, achieved closed-loop verification of 'buying milk tea with one sentence,' advancing the entire shopping process through conversational, automated, and non-jump interactions. In April, it upgraded to 2.0, co-built by Alipay and the IIFAA Alliance with over 20 partners, including Xiaomi, Zhipu, and BYD, defining the interaction grammars for A2A (Agent-to-Agent) and A2M (Agent-to-Machine) communications.

Without this 'universal language,' every AI application would have to reinvent the wheel, shattering commercial closures into isolated islands. Alipay's role here is to write universal communication rules for the industry—whoever defines the rules holds the key to the future ecosystem.

Moving upward is the security layer—the bridge's guardrails. Alipay's AgentPayGuard has passed the China Academy of Information and Communications Technology's (CAICT) Tail Lab's highest Level 5 certification, erecting four layers of defense: identity security, runtime security, supply chain security, and intention security. This means that in the AI payment realm, security certification is not just a compliance move but a necessity for market education.

Without proper guardrails, no one would dare to cross the bridge, no matter how wide it is. Alipay uses a trust foundation to reduce market fears—this is the quantifiable aspect of trust.

Above that is the transaction layer—the bidirectional lanes on the bridge. A bridge cannot serve only one side; the Agent economy must simultaneously solve 'who pays' and 'who receives.'

On the consumer side (To C), Alipay has laid lanes across various terminals: within the QianWen App, 'glance-to-pay' in AI glasses like Rokid, smart cockpits in over 10 million vehicles from brands like Li Auto, Chery, Geely, and Dongfeng, and even direct support for general-purpose agents like OpenClaw.

On the business side (To B), Alipay's 'AI Collection' transforms Agents from 'cost resources' into 'revenue-generating products.' Capabilities such as AI tipping, AI subscription payments, and instant collections based on API calls are fully equipped. Alipay has paved both lanes, enabling developers to integrate with zero code and users to transact with a single sentence.

At the top is the terminal layer—the bridge is built, and Agents can now cross. But who decides 'when to let them through' and 'how to control them'? The answer lies in the users' hands.

Think of it as users holding a master switch: authorizing who can cross, setting spending limits, choosing consumption rules, and reviewing every transaction. While the bridge enables Agents to run, the 'AI Wallet' lets users confidently authorize Agents.

Beyond this, Alipay has introduced two new pieces to the puzzle: Token Pay helps large model companies solve global user subscription and Token recharge needs in one stop, with MiniMax and StepFun already onboard. Meanwhile, building on the 'Tap' smart terminals in millions of stores, Alipay launched 'Xiaoyu,' the first merchant operation agent, integrating payment, membership, product, and traffic distribution capabilities into terminals, evolving the 'Tap' device into a store-level AI partner.

From protocols to security, from transactions to terminals, and from online to offline, the full-stack AI payment system is now fully connected. Backed by a billion-user base and the Alibaba ecosystem, Alipay has completed a positive cycle of value validation.

Arguably, the new AI payment infrastructure is Alipay's preemptive move before the Agent economy explodes, and it is strongly propelling the entire Agent industry into an accelerated growth phase.

3. The Other Side of the Bridge: Ecosystem and Flywheel

The bridge is built, but why was Alipay the one to build it?

From escrow transactions and express payments to 'Tap,' and now to AI Pay, Alipay has driven a generational leap in payments roughly every decade. While the industry debates 'ceilings,' Alipay has already found incremental growth in new payment battlegrounds.

Behind this lies the compounding effect of two decades of payment capabilities and the efficient alignment of resources and organization after anchoring its AI strategy. Ant Group CEO Han Xinyi previously stated that payments, finance, and health are the 'three legs' supporting Ant's growth, pushing the business and organization to fully embrace AI. This top-down focus has allowed resources to converge efficiently, accelerated product launches, and created an increasingly complete system.

Combined with the scenario ecosystem built by a billion users and millions of merchants, the network effect will continue to amplify in the future. Leveraging Alibaba's capabilities, including QianWen, Taobao SnapUp, and Alibaba Cloud, Alipay serves as the transaction hub for commercializing Alibaba's AI capabilities across computing power, applications, and consumption scenarios—far from acting alone.

More critically, this AI payment system continues the open philosophy, drastically lowering the barrier to entry for AI entrepreneurship.

In recent years, the threshold for AI entrepreneurship has dropped from 'tens of millions in funding' to 'just an idea.' Previously, building AI products was a game for big tech companies. Not anymore. 'Sunshine Xiaowen,' a normal university graduate who only started exploring AI a year ago, used the Kouzi platform to integrate Alipay's payment collection in 24 hours, turning her prompt engineering methodology into a paid product.

Manually weaving enthusiast Xiao Man wanted to open an independent boutique. She simply typed one sentence into the Qoder dialog box: 'Create an independent e-commerce site for handmade woven bags.' The site was built, and payments were connected. That night, her first order arrived.

The rise of individual creators and micro-entrepreneurs is a precursor to the industry's full-scale explosion.

The open ecosystem is also reshaping the B-side service landscape. Bocha, a leading domestic AI search provider supporting mainstream models like DeepSeek with 30 million daily calls, encapsulated its search capabilities into a paid Skill following the A2M protocol after integrating with Alipay's 'AI Collection.' Now, any Agent needing information verification can call upon it instantly, with micro-payments settled automatically.

As more participants join, Agents become more capable; as the ecosystem thrives, service providers gain greater monetization opportunities. A mutually empowering, cyclical growth flywheel for the industry has now taken shape.

Next comes the moment when the floodgates open.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle