Surging 10 Times in a Year! Memory Chips Become the 'Money Printer' in the AI Era: Three Giants Feast While Domestic Players Get Crumbs

05/28 2026

05/28 2026

685

685

AI Takes Off, Memory Feasts.

When we used to talk about memory products, our first thoughts were RAM sticks, SSDs, and mechanical hard drives—those 'computer accessories.' While important, they were often just another parameter on a build list. For most people, memory and hard drives paled in comparison to CPUs and GPUs in importance.

But in the AI era, everything has changed.

At first, AI companies were just competing for GPUs, with NVIDIA's flagship compute cards being 'hard to come by.' Today, the competition has shifted: memory, hard drives, and even CPUs—all PC-related hardware—are in short supply, with memory chips leading the pack.

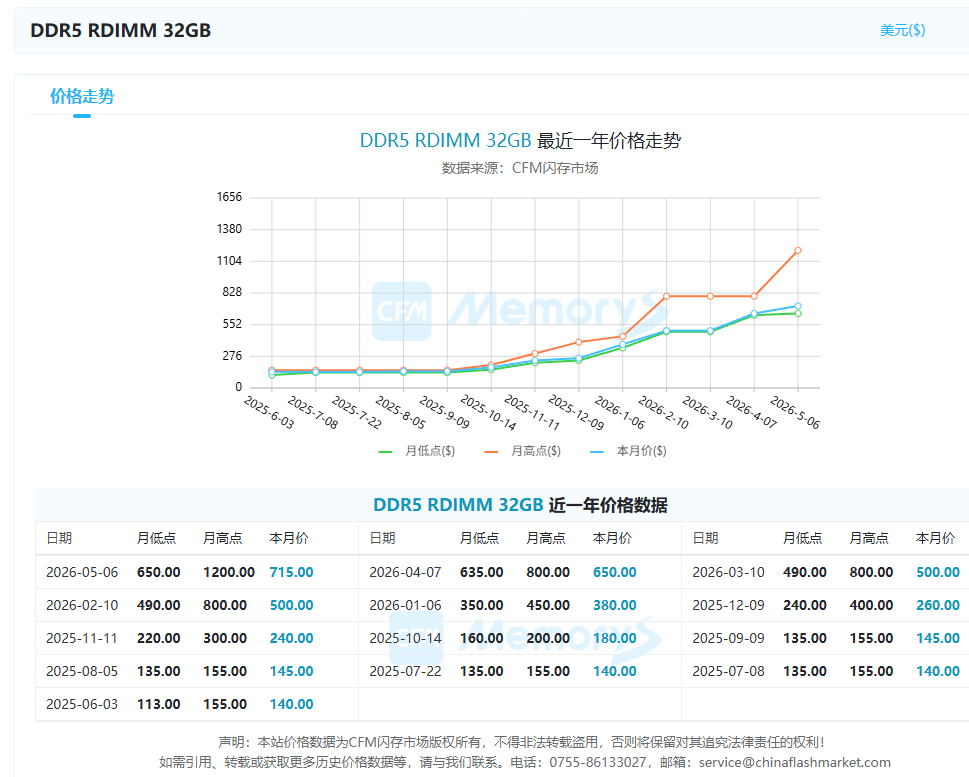

Data from CFM shows that server memory stick prices have surged over 10-fold in the past year. In June last year, a 32GB DDR5 RDIMM hit a low of just $113, but by May this year, prices peaked at $1,200. Even average transaction prices have risen more than fivefold.

Image Source: CFM

The price hikes in memory chips didn't happen in a vacuum. They stem from the growing scale of large models and the increasing number of users, both of which require AI companies to use more storage for model and user data. Meanwhile, GPU demand remains strong, with a single flagship compute card consuming tens to hundreds of GB of high-bandwidth memory. Strong demand from giants like NVIDIA has left the entire market in shortage.

This is why, over the past year, profits and stock prices for memory giants like Micron, Samsung, and SK Hynix have suddenly skyrocketed. These companies were once classic cyclical players: they made money during shortages and saw profits slide during oversupply. But this time, AI isn't driving a typical consumer electronics upgrade cycle—it's creating systemic demand from data centers for HBM, DDR5, enterprise-grade SSDs, and high-capacity HDDs, demands that won't disappear anytime soon.

Moreover, Leitech believes the focus shouldn't just be on 'memory price hikes' but on how AI has redefined the storage industry. Previously, consumer and enterprise demands ran on parallel tracks; now, manufacturers are prioritizing enterprise needs like never before, as they've become an indispensable part of AI infrastructure. The era of severe overcapacity may never return.

Why Are the 'Big Three' in Flash Memory Making So Much?

In this storage boom, the most attention is on Micron, Samsung, and SK Hynix—the so-called 'Big Three' in memory.

They differ fundamentally from many everyday storage brands: while ordinary brands assemble DRAM and NAND particles into end products like memory sticks, SSDs, and portable hard drives, the Big Three control core particle manufacturing (while also producing end products themselves).

Simply put, while others are 'cooking meals,' the Big Three have the rice, meat, and vegetables—plus control over farmland and supply chains. They even run the biggest restaurants themselves. This is their core value in the AI era. Yet most people know their names without understanding their respective strengths in AI.

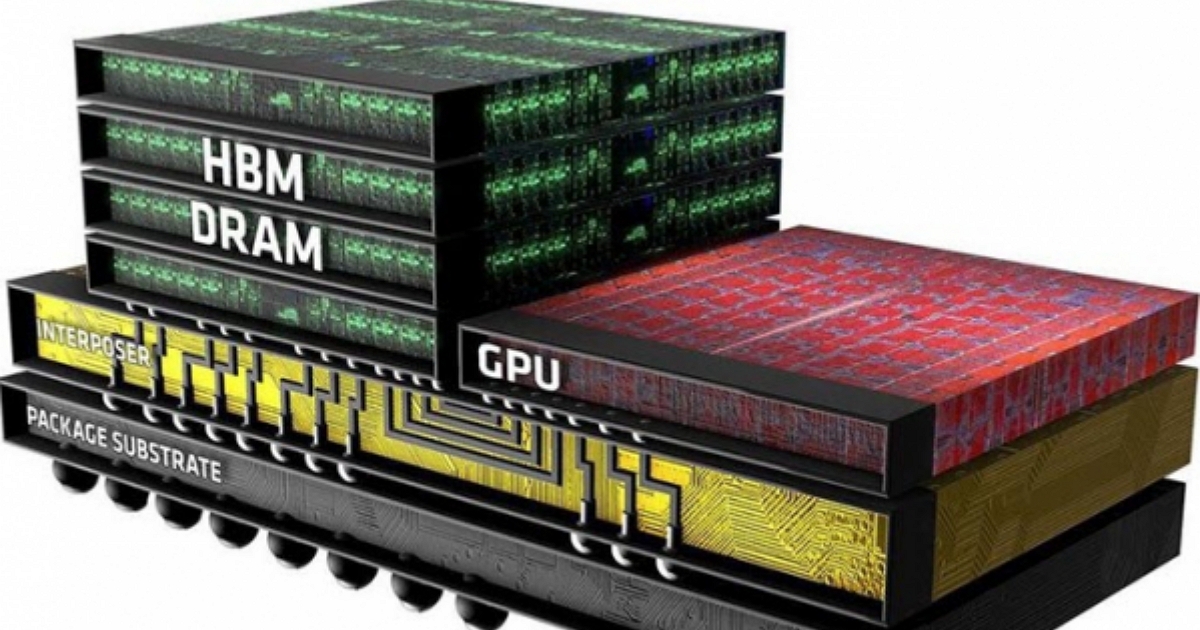

Take SK Hynix first. For years, its defining label has been HBM, once holding nearly 70% of the market; even after Samsung and Micron ramped up, it still holds over 50%. HBM can be thought of as a super-wide highway next to AI GPUs: by vertically stacking multiple DRAM chips and using advanced packaging close to the GPU, it enables ultra-high-bandwidth data flow between the GPU and memory.

Image Source: techbang

This is crucial in AI applications, where large models deal with trillions of data points. Even with techniques like mixture-of-experts architectures to reduce active parameters, bandwidth, speed, and latency requirements remain extremely high. This makes HBM memory essential for top-tier AI models, keeping demand consistently strong.

The issue is that HBM isn't just about stacking a few memory chips. Its production requires nearly full-line improvements and optimizations, followed by rigorous certification from top clients like NVIDIA and AMD. In other words: high technical barriers, slow capacity releases, and deep client binding have given SK Hynix a huge market premium in the AI cycle.

Samsung's strength lies in its 'all-rounder' approach: it makes both DRAM and NAND while covering phones, consumer electronics, wafer fabrication, and more. For Samsung, strong AI server demand means shifting resources to HBM, high-capacity DDR5, and enterprise NAND; when phone and PC markets recover, it can redirect capacity to consumer markets—nothing goes to waste.

Image Source: Samsung

While Samsung doesn't lead technically, its broad industrial coverage gives it stronger risk resistance. From an investment standpoint, Samsung is a safer bet than SK Hynix.

Finally, Micron has a unique edge: it's the largest local (domestic) memory manufacturer in the U.S. Against a backdrop of accelerated AI data center construction and heightened supply chain security concerns, Micron's strategic value has grown significantly.

Historically, Micron was mainly viewed through the consumer market lens. Technologically, it lagged Samsung and SK Hynix, with low enterprise market share. Any consumer demand fluctuations hit Micron hard (it lost billions in 2023). But now, Micron must be viewed within North America's AI infrastructure supply chain.

Over the past two years, Micron has sharply pivoted R&D and capacity toward HBM. With rising U.S. domestic supply chain demand, its HBM market share now closely rivals Samsung's. Meanwhile, Micron became the first among the Big Three to 'cut off' consumer end-product businesses (not halting consumer flash chip production, but stopping finished product sales), dedicating all capacity to enterprise needs.

Image Source: Micron

This is why memory stock prices have soared collectively. Previously seen as 'replaceable commodities,' memory is now recognized for AI's need for high bandwidth, stability, energy efficiency, and sustainable supply—not just capacity. Producing is one thing; reliably supplying top AI clients at scale is another.

However, with all three giants rushing toward enterprise demand, the existence of domestic player ChangXin Memory Technologies becomes intriguing.

Admittedly, ChangXin still lags behind Samsung, SK Hynix, and Micron, especially in HBM, advanced processes, and top-tier server client certifications. But ChangXin's opportunity lies in the vacuum left as the Big Three focus more on AI servers, HBM, and high-end DDR5, leaving the mid-to-low-end and mainstream consumer DRAM markets wide open.

Previously, this market was dominated by low-cost overseas memory particles. ChangXin's particles had neither performance nor cost advantages, making market penetration difficult. Not anymore—terminal manufacturers are practically begging ChangXin for chips.

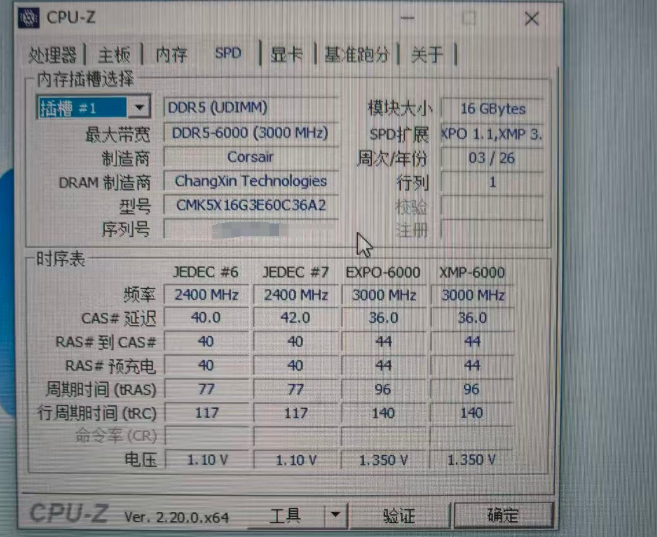

For example, overseas consumers recently found that some DDR5 memory products from renowned PC hardware brand Corsair used ChangXin particles. While this doesn't mean ChangXin has fully broken into the global high-end market, it shows domestic DRAM has entered top-tier consumer brand supply chains, no longer confined to China.

Image Source: wxnod

For ChangXin, this may be more realistic than directly challenging HBM: first capture ordinary DDR5, domestic PCs, consumer memory, and some server memory markets, then gradually advance to higher-end products—stepping up from low to high, as countless Chinese companies have done before.

The latest news is that ChangXin Technology's IPO has been approved. If successful, its market cap is estimated to exceed 2 trillion yuan, ranking it fifth among Chinese companies by market cap—behind only Alibaba, ICBC, and Tencent. Indeed, with dual support from the AI and storage industries, ChangXin could truly 'soar.' Hopefully, it will join the memory Big Three to make them a Big Four.

Don't Just Watch the Big Three—These Players Are Also Feasting

If Micron, Samsung, and SK Hynix are eating the fattest piece of the AI storage pie, then companies like SanDisk, Seagate, Western Digital, Longsys, and SMI are enjoying the spillover industrial dividends.

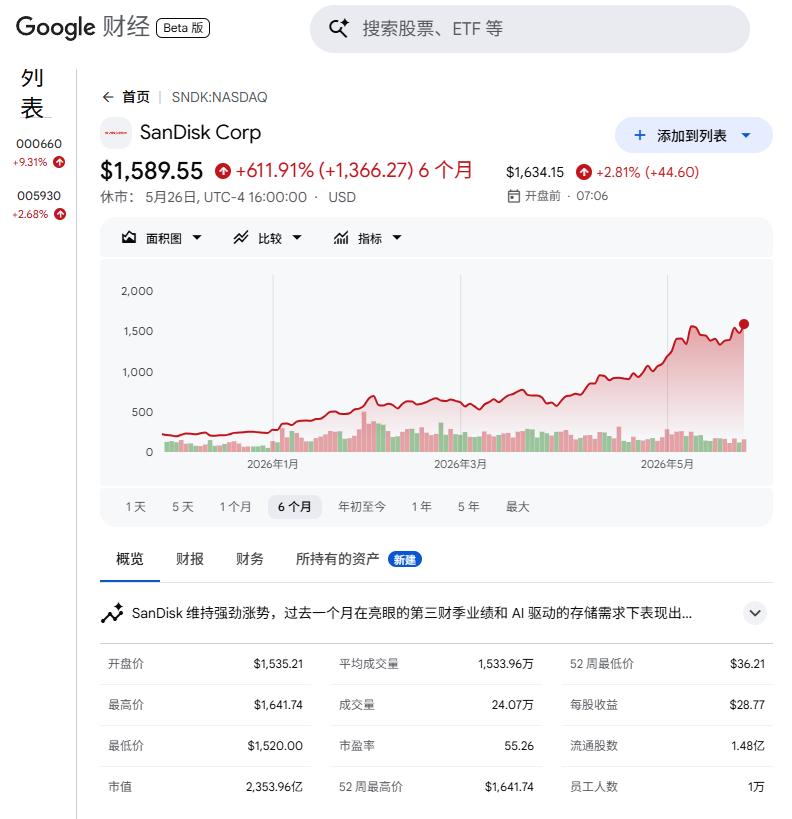

SanDisk's stock price is among the few that have risen as much as the top three. This surprised Leitech—while SanDisk is a top-tier brand, it's not irreplaceable. How did its stock soar?

After digging, Leitech found the answer: core demand for NAND surged, blowing past investor expectations. More importantly, after spinning off from Western Digital, SanDisk shifted its strategic focus entirely to data centers, securing a multi-year $11 billion supply contract with top cloud providers like Amazon.

Image Source: Google Finance

Speaking of SanDisk brings us to another core of this storage boom: SSDs. Everyone knows AI training requires storing massive datasets, and AI inference needs reading model parameters. When enterprises deploy agents and vector databases, they generate huge volumes of cache, logs, and multimodal files.

To ordinary users, SSDs once just meant 'faster boot times.' But in data centers, SSD ratios directly impact read/write throughput, latency, power consumption, and stability. Simply put, they directly affect AI large models' efficiency and inference costs, forcing many data centers to replace HDDs with SSDs—driving SSD demand skyward.

This doesn't mean HDDs are obsolete; their demand is also rising because AI doesn't just 'consume data (training)'—it generates even more. Model training data, video footage, historical logs, backup data, archival data—all can't reside solely on expensive SSDs. The cost-effective, high-capacity HDDs become the best choice.

Growing HDD demand has fueled revenue surges for storage giants Seagate and Western Digital. While both have SSD businesses, as the dual HDD giants (Toshiba holds <20% market share), they've captured nearly all the surging demand.

Moreover, as AI becomes more widespread and data volumes explode, HDDs' value will only rise. Historical data shows the internet generated 2ZB of data in 2010 (1ZB = 1 billion TB); by 2020, this grew to 64ZB; just five years later, it neared 200ZB.

Image Source: Wikipedia

In science, there's a consensus that roughly 90% of human history's data was generated in the past two years. AI empowers everyone to produce vast data volumes, making data this era's core resource.

Thus, as the AI industry grows, HDDs, SSDs, and other hardware are unlikely to return to low prices.

Beyond chipmakers and terminal manufacturers, integrators like Longsys are also affected. Unlike Samsung or SK Hynix, Longsys isn't an upstream fab but sits closer to terminal (end) markets, assembling upstream particles into UFS, eMMC, SSDs, memory modules, and enterprise storage for terminal manufacturers.

Moreover, firms like Longsys with full-chain firmware algorithms and independent controller development capabilities are more sought after, as they can customize storage solutions to client needs, aligning product performance with user requirements.

Recently, Longsys developed multiple embedded storage products for AI PCs and AI Mobile, optimizing power, capacity, and bandwidth compared to previous offerings—better suited for AI applications and model runtime demands.

In this storage wave, nearly all storage firms have found their 'sweet spots' and are competing with 200% effort. Surging demand and tight supply have made storage one of today's most 'money-absorbing' industries.

Final Thoughts

In Leitech's view, this storage boom isn't just another price cycle.

The storage industry has always had cycles: shortages drive price hikes, manufacturers expand production, then oversupply triggers price drops and industry reshuffles (the 2023 storage price crash stemmed from the 2020 crypto boom-driven expansion).

But this time, AI is changing storage's industrial status. Previously, memory and hard drives were just terminal (end) product components: strong phone sales boosted memory; weak PC sales hurt SSDs.

Now, AI places storage in data centers, model training, inference services, and enterprise AI systems. Storage no longer just affects 'capacity'—it directly impacts compute efficiency, system costs, and AI adoption speed. Given current trends, AI demand will remain strong for years. Even if large model development hits bottlenecks, AI's spread is unstoppable.

Of course, this doesn't mean storage is now cycle-proof. If giants keep expanding capacity, prices could still fall—especially as AI investment slows and firms reassess compute center construction more cautiously.

So in the past month, we have actually witnessed a gradual decline in memory storage prices. Had it not been for the sudden large-scale strike at Samsung, which will affect supply for the coming months, chip prices would certainly have continued to fall. This also indicates that the patterns observed in the memory storage industry over the past few decades will not completely disappear.

But what is certain is that AI has made the market re-recognize the value of memory storage.

Samsung, SK Hynix, Micron, Changxin

Source: Leikeji

The images in this article are from the 123RF royalty-free image library. Source: Leikeji

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle