Xiaopeng’s Q1 Performance: Revenue Dives Over 41%, Nearly 1.8 Billion Yuan Loss, Will Mass Production of Physical AI Spark a Revaluation?

05/29 2026

05/29 2026

492

492

On May 28, Beijing time, Xiaopeng Group unveiled its financial results for the first quarter of 2026.

The financial report disclosed that Xiaopeng Group's automotive sales business experienced a downturn in Q1 2026, with 62,682 vehicles delivered during the period. This marks a 33.3% year-on-year decrease and a 42.5% quarter-on-quarter decline. Consequently, automotive sales revenue amounted to 11 billion yuan, reflecting a 23.5% year-on-year drop and a 42.3% quarter-on-quarter decrease.

If there's a silver lining, it's that the quarter-on-quarter decrease in automotive sales revenue was less pronounced than the decline in delivery volume, with a 9.8 percentage point difference. This can be attributed to a slight uptick in the average selling price (ASP) per vehicle, which remained relatively stable quarter-on-quarter, with only a 0.2 percentage point variation.

However, when considering total revenue, Xiaopeng Group reported 13.03 billion yuan for Q1, a 17.6% year-on-year decrease and a 41.4% quarter-on-quarter drop. This decline is primarily due to significant fluctuations in service and other revenues. In Q1 2026, service and other revenues reached 2.03 billion yuan, showing a substantial 41.2% year-on-year increase but a 36.1% quarter-on-quarter decrease.

This variation is tied to the timing of revenue recognition for this business segment. Since most service and other revenues stem from collaboration with Volkswagen, Xiaopeng recognized a substantial one-time revenue of 3.18 billion yuan from this segment in Q4 2025. Nevertheless, a year-on-year increase of over 40% was observed in Q1 2026, indicating potential for continued growth in 2026 as production of Volkswagen-related collaborative models ramps up.

More significantly, the gross margin for service and other revenues is notably high. In Q1 2026, this segment's gross margin stood at 66.5% (compared to 66.4% in Q1 2025 and 70.8% in Q4 2025), elevating Xiaopeng Group's overall gross margin to 20.6% (a 5 percentage point year-on-year increase and a 0.7 percentage point quarter-on-quarter decrease). In contrast, the gross margin for Xiaopeng's auto sales was merely 12.1% (a 1.6 percentage point year-on-year increase but a 0.9 percentage point quarter-on-quarter decrease).

In Q1 2026, Xiaopeng Group reported an operating loss of 1.87 billion yuan and a net loss of 1.78 billion yuan, contrasting sharply with a net loss of only 660 million yuan in Q1 2025 and a profit of 380 million yuan in Q4 2025. It seems that profitability currently hinges heavily on service and other revenues, particularly through collaboration with Volkswagen.

For Xiaopeng Motors, the recurring challenge has been the volatility of auto sales, lacking models that consistently enjoy popularity and stable sales volumes. Typically, new models perform well initially but experience erratic sales throughout their lifecycle, often starting strong and then tapering off.

In Q1 2026, Xiaopeng Group's R&D investment surged to 2.91 billion yuan, a 46.8% year-on-year increase and a 1.1% quarter-on-quarter rise.

Based on Xiaopeng's business operations, R&D efforts have been concentrated on Robotaxi, humanoid robots, the VLA large model, and the Turing chip.

Notably, Xiaopeng unveiled a new full-size SUV model, the GX, on May 20. It is reported that Xiaopeng intends to use this mass-produced vehicle to initiate Robotaxi testing in Guangzhou in the latter half of the year.

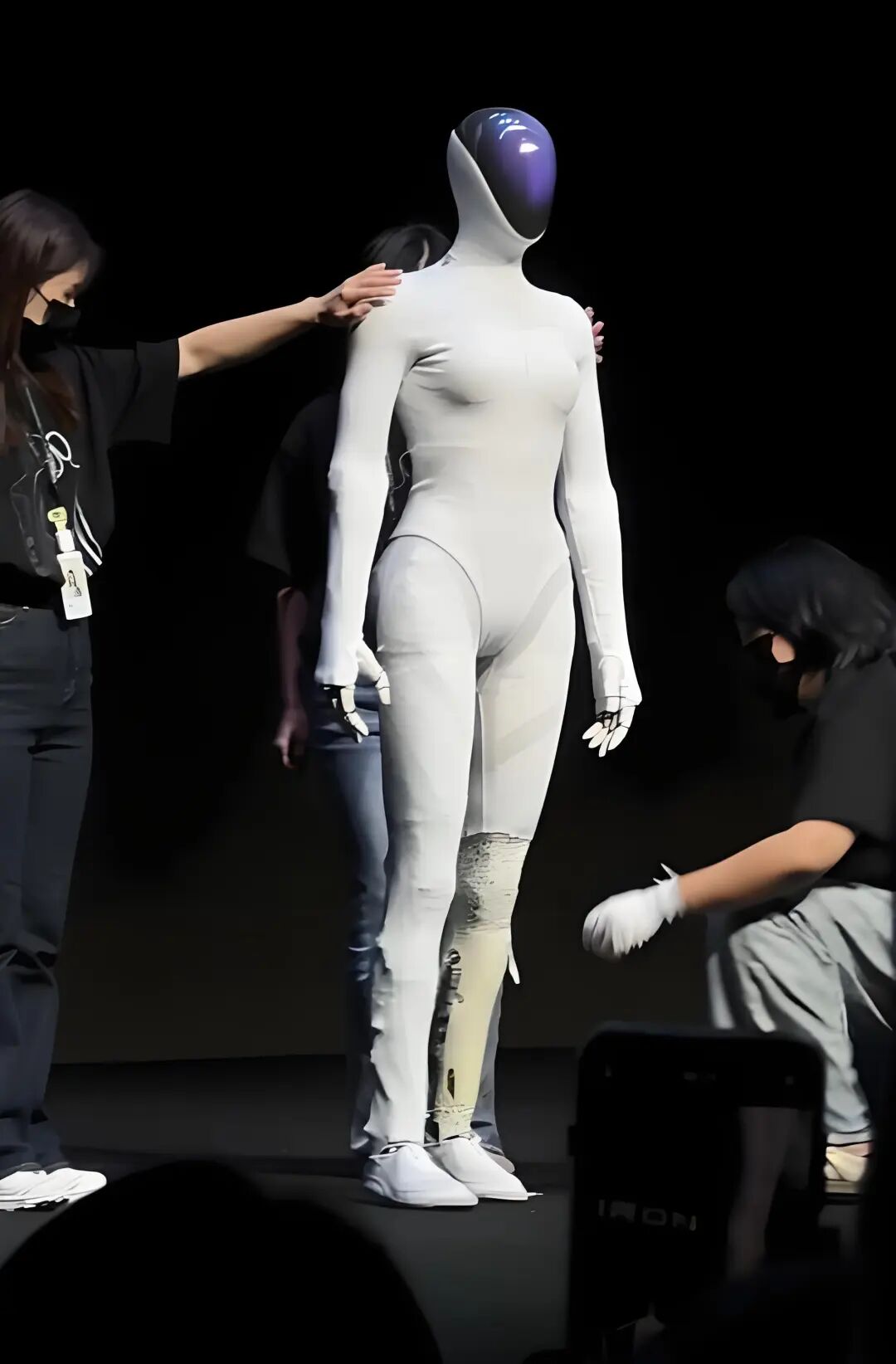

Regarding the mass production of humanoid robots, Xiaopeng's production facility in Guangzhou commenced operations in February, with mass production slated to commence within the year. The walking gait of Xiaopeng's humanoid robot, unveiled last year, was initially met with skepticism, with some suggesting it was portrayed by a model. Xiaopeng responded by disassembling it on stage to demonstrate its authenticity as a robot, thereby captivating the public.

Robotaxi and humanoid robots are the two flagship products that He Xiaopeng asserts will transform leading physical AI technology into new catalysts for revenue and profit growth.

As for Xiaopeng's auto business, 31,011 units were delivered in April. Xiaopeng's delivery forecast for Q2 ranges between 100,000 and 106,000 units, representing a 59.54% to 69.11% increase compared to Q1.

Due to the anticipated rise in auto sales, Xiaopeng Group's revenue projection for Q2 is between 19.6 billion and 20.8 billion yuan, marking a 50.38% to 59.59% quarter-on-quarter increase compared to Q1.

However, the financial report did not provide a profitability forecast for Q2, and achieving profitability seems highly improbable.

Finally, let's examine Xiaopeng Group's cash reserves. As of March 31, 2026, Xiaopeng's cash reserves stood at 42.09 billion yuan, down from 45.28 billion yuan in the same period last year and 47.66 billion yuan as of December 31, 2025.

For the capital market, whether it will assign a valuation to Xiaopeng Group based on its physical AI technology remains uncertain. Judging by the recent trend in Xiaopeng's stock price, some investors appear optimistic.

After all, Xiaopeng has consistently followed in Tesla's footsteps, including He Xiaopeng's venture into car manufacturing, the shift to pure vision-based autonomous driving by abandoning LiDAR, the promotion of Robotaxi, and the development of humanoid robots. Each move has mirrored Tesla's strategy, with the only exception being the plan to launch flying cars, an area where Tesla is unlikely to venture in the near future.

However, Tesla's market capitalization speaks volumes, as does Xiaopeng's. Will the capital market draw comparisons between the two?

It's worth mentioning that Cambrian Technologies, listed on the A-share market, is often seen as a counterpart to NVIDIA, with a market capitalization nearing 1 trillion yuan. Similarly, Zhipu AI, a prominent AI model listed in Hong Kong, boasts a market capitalization exceeding 700 billion yuan.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle