AI Financial Report Makes Initial Appearance: Kuaishou Initiates Dual Narratives

05/29 2026

05/29 2026

520

520

Kuaishou aspires to be more than just a short-video platform monetizing through traffic; its ultimate goal is to become an AI-driven ecosystem company.

Edited by | Meng Wen

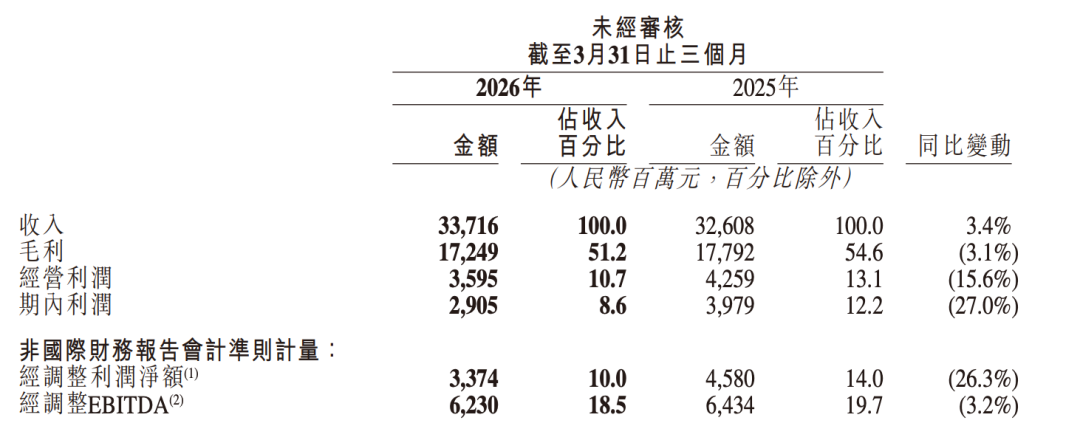

Kuaishou's Q1 2026 financial report shows two distinct trajectories for its main platform and Kling AI:

Total revenue reached RMB 33.72 billion, a historic high, but adjusted net profit fell from RMB 4.58 billion to RMB 3.37 billion, a year-on-year decline of 26.3%.

On the other hand, Kling AI's quarterly revenue exceeded RMB 650 million, a year-on-year increase of over 300%. As of March 2026, its ARR approached $500 million, up from just $100 million a year earlier.

Market rumors also suggest that Kling is seeking independent financing at a $20 billion valuation, nearly equivalent to 70% of Kuaishou's parent company's market capitalization. Tencent appears on the list of potential investors, with plans for an IPO as early as next year.

Kling's spin-off is not just a valuation story but also a stress test: Kuaishou aims to gamble on a new AI-driven future by 'letting go.'

Kling and Kuaishou: 'Not on the Same Path'

Kling and Kuaishou's core user bases hardly overlap.

Kuaishou boasts 412.7 million daily active users and 771.7 million monthly active users, a historic high. These users engage in short-video viewing, live streaming, and shopping on the platform, representing typical content consumers in sink markets (lower-tier markets).

Kling's user demographics are entirely different. During the Q1 earnings call, Cheng Yixiao clearly outlined Kling's primary application scenarios: professional creative fields such as advertising, film and television, short dramas, and gaming. Its revenue comes from 'a dual-wheel drive of API call revenue from B-end enterprise clients and subscription revenue from P-end paying users.'

More intriguing is the geographical distribution. In Q1 2026, 70% of Kling's revenue came from North America and other overseas markets. The product topped the art and design download charts in over 40 countries globally and ranked first in iPhone graphic design revenue in South Korea and Russia.

Source: Kling AI

Source: Kling AI

An AI tool headquartered in Beijing and born out of a short-video platform has first succeeded in commercializing its business model among overseas professional creators. This implies that Kuaishou's hundreds of millions of domestic users hold little direct conversion value for Kling's growth.

Comparison with peers is more revealing. During the same period, Zhipu AI's MaaS API platform had an ARR of approximately $230-240 million, while MiniMax's ARR was around $150 million. Kling clearly led with nearly $500 million in ARR, but this revenue did not come from traffic diversion from Kuaishou's main platform; instead, it was built through word-of-mouth expansion within professional creative circles.

In the past, internet companies prioritized traffic synergy for new businesses. Kling's uniqueness lies in being the first AI business to emerge from Kuaishou that operates 'independent of the main platform's ecosystem.'

Since the two businesses do not share the same ecosystem, independent operations will not sever any critical synergies but instead provide clearer valuation and independent financing capabilities.

These factors form the 'foundation' for Kling's $20 billion valuation narrative.

Two 'Key Figures'

Kling's journey to success is inseparable from two individuals: Ge Kun and Zhang Di.

Ge Kun's career is legendary in China's AI circle. With a Ph.D. from Tsinghua University specializing in recognition and intelligent systems, he joined Alibaba in 2011 as part of the inaugural 'Ali Star' cohort, leading ad algorithm and AI technology development at Alimama and reaching the P10 level.

He proposed a deep user network interest distribution model to optimize user click preference predictions. When he joined Kuaishou in 2020, Alibaba sued him for violating a non-compete agreement, resulting in a multimillion-yuan settlement and causing a stir in the industry.

At Kuaishou, Ge Kun oversaw technological layout (layout) for content understanding, recommendation large models, and video generation large models, leading the team to launch Kling in June 2024. In April 2025, Kuaishou established the Kling AI Business Unit, with Ge Kun as its general manager, reporting directly to CEO Cheng Yixiao.

Ge Kun, Senior Vice President of Kuaishou and Head of Community Science Line

This marked Kling's elevation from a technical project to a strategic business for the company.

However, the technical groundwork for Kling's growth from 0 to 1 was laid by Zhang Di.

Zhang Di completed his undergraduate and master's degrees in computer science at Shanghai Jiao Tong University. He joined Alibaba in 2010, deeply involved in the technical transformation of search, recommendation, and advertising businesses into the deep learning era at Alimama, leaving as a senior technical expert. In 2020, he followed his mentor Ge Kun to Kuaishou, taking full charge of the large model and multimedia technology team in early 2023.

His most critical decision at Kuaishou came after Sora's release in 2024. While many companies in the industry remained wait and see (on the sidelines), Zhang Di, as the 'top technical figure,' resolute (decisively) approved internal reviews, pushing the team to quickly adapt and optimize through self-research, fully committing to the video generation route.

This decision allowed Kling to launch one to two months ahead of most peers.

After Kling 1.0's debut, it underwent over 30 iterations in just over a year. Those close to him describe him as 'technically savvy, decisive, and unbureaucratic,' a leader whom technical personnel can directly approach for solutions without navigating cumbersome processes.

However, in August 2025, amid Kling's rapid growth and just after its ARR surpassed $100 million, Zhang Di suddenly resigned.

After leaving Kuaishou, Zhang Di briefly joined Bilibili as head of technology but departed after just over a month. In November 2025, he returned to Alibaba, leading the 'Future Life Lab' at Taotian Group, reporting directly to the CTO of Alimama. His departure from Kuaishou to landing at Alibaba took just three months.

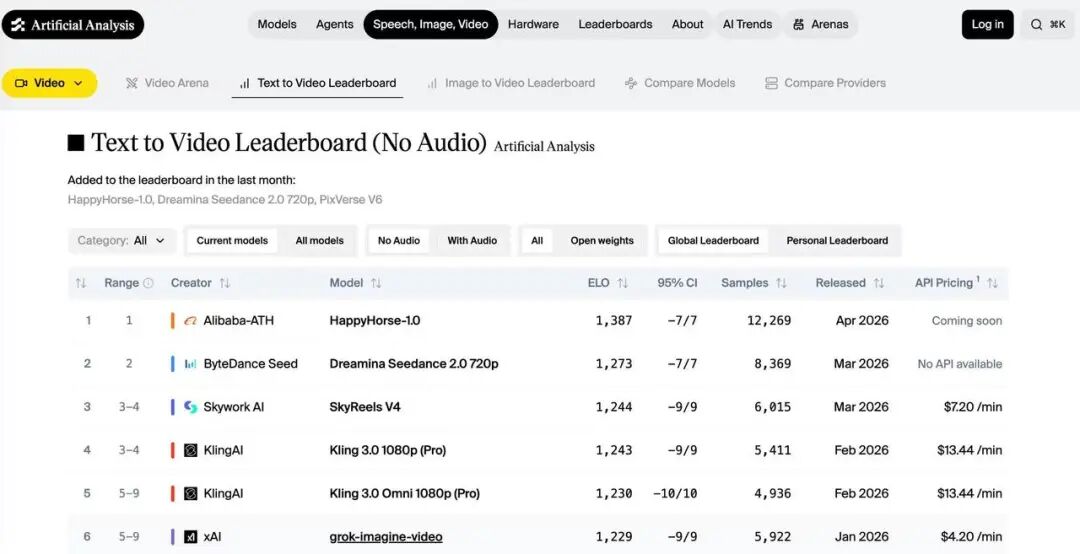

Then, in April 2026, HappyHorse-1.0 topped the Artificial Analysis rankings, surpassing ByteDance's Seedance and Kling in both text-to-video and image-to-video categories. Only five months had passed since Zhang Di left Kuaishou to create 'HappyHorse' at Alibaba.

This does not negation (negate) Kling's previous achievements but raises a practical question: What is Kling's core competitiveness?

The outside world often discusses its model capabilities and iteration speed, but a detail emerged last year when Kuaishou's management revealed that Kling 2.5 Turbo's cost per video generation had dropped nearly 30% from the previous generation, with gross profit margin (gross margin) for inference-generated videos nearly breaking even.

These are tangible engineering achievements. AI video generation is extremely costly, with high GPU inference costs per generation and rapidly escalating expenses in high-concurrency scenarios. Sustaining revenue growth while continuously reducing inference costs demonstrates Kling's mature engineering capabilities.

However, engineering, productization, and organizational execution all heavily rely on people. Zhang Di's departure underscores that these capabilities are not unbreakable.

And he is not an isolated case.

In December 2025, Kuaishou's Vice President and head of foundational large models and recommendation models, Zhou Guorui, also resigned. Since Cheng Yixiao became chairman in 2023, over ten vice presidents have left or stepped down from Kuaishou. Continuous executive turnover and stability issues among AI's core personnel form the hidden narrative behind this financial report.

Notably, while Kling became an independent unit in April 2025, it only established a separate option pool and incentive mechanisms distinct from the parent company around the time news of its spin-off financing emerged.

For a business competing with ByteDance and Alibaba for top AI engineers, independent equity stories are inherently more attractive than parent company options.

Thus, spinning off Kling AI is both a capital maneuver and Kuaishou's battle to retain AI talent.

A 'Strategic Retreat' Gambit

The AI video sector entered a 'knockout phase' this year, with Sora's failure marking a turning point.

Sora, which shocked the global market in 2024 with its astonishing results, ultimately exited in early 2026 due to prohibitive inference costs and commercialization challenges.

Sora's fate instead validated Kling's value in 'controllable inference costs.' Among today's video generation players, only Kling AI and ByteDance's Seedance can simultaneously achieve 'large-scale commercialization' and 'cost control.'

According to industry sources, Seedance now holds over 80% of the market share by daily consumption, with Kling accounting for about 14% and Alibaba's Wanxiang 2.7 and HappyHorse combined at less than 5%.

As video generation costs continue to decline, AI-powered comic dramas have surged in popularity. After Seedance 2.0's launch in February, comic drama and short drama companies flocked to the platform. By late March, ByteDance's comic drama daily consumption exceeded RMB 70 million, surpassing live-action short dramas for the first time.

Kuaishou also capitalized on this trend. During the Q1 earnings call, Cheng Yixiao highlighted this business, noting that Kuaishou's AI comic drama marketing consumption grew over 100x year-on-year and over 150% quarter-on-quarter. By late March 2026, daily AI comic drama marketing consumption on Kuaishou peaked at over RMB 20 million.

Behind the sector's prosperity lies an all-out arms race in computing power, capital, talent, and engineering. If Kling remained within Kuaishou Group, it would inevitably be constrained by the parent company's capital efficiency and investment pace, struggling to keep up with the industry's rapid iterations.

Kuaishou's management has calculated this clearly. Kuaishou's total capital expenditures for 2026 are approximately RMB 26 billion, substantial among AI companies but dwarfed by giants like ByteDance.

According to Bloomberg, ByteDance plans to raise its AI infrastructure investment to $70 billion this year, nearly 20 times Kuaishou's figure. Even at the previously rumored $30 billion, it would still be over eight times Kuaishou's. When competition reaches this level of computing power and capital investment, Kling's 'leadership' carries an uneasy undertone.

CFO Jin Bing mentioned during the earnings call, 'Despite capital expenditures of RMB 26 billion, Kuaishou maintains its goal of positive free cash flow at the group level for the full year. Our total usable funds stand at RMB 117.7 billion.' While this seems substantial, Kuaishou set Kling's revenue target for the year at around RMB 2 billion. With a 13:1 input-output ratio, concerns about sustained erosion of group profits are inevitable among capital markets.

Raising $2 billion at a $20 billion valuation for Kling, allowing it to fight its battles with independent resources, is more practical and pragmatic than keeping it locked within Kuaishou's system.

The capital logic behind Kling's spin-off is sound, but the valuation figure itself warrants scrutiny. Kuaishou's overall market capitalization is about $29 billion, while Kling targets $20 billion in independent financing. By comparison, Kuaishou's core business (annual revenue of approximately RMB 140 billion, net profit of RMB 20.6 billion, and over 400 million DAUs) receives an implicit valuation of only about $9 billion.

Whether Kuaishou's main business is undervalued or Kling's valuation is inflated by hype remains undetermined. Management only mentioned that B-end and P-end user retention trends remain favorable without disclosing specific figures, leaving the valuation's rationality (reasonableness) in question.

Beyond valuation speculation, spinning off Kling is part of Kuaishou's broader AI strategy.

In addition to Kling AI, Kuaishou has launched end-to-end agents covering user interest inference, creative production, product screening, and marketing bidding decisions. Meanwhile, Kuaishou's online marketing services revenue reached RMB 19.643 billion, up 9.3% year-on-year, accounting for 58.3% of total revenue.

Kling AI serves as Kuaishou's AI strategy's 'flagship,' not only achieving rapid growth itself but also driving iterative upgrades across the platform's AI infrastructure, including recommendation large models, intelligent bidding, and AIGC material generation, with capabilities permeating layer by layer.

Externally a 'financing target' and internally a 'transformation engine,' Kuaishou's push for Kling's independence resembles extracting high-growth AI assets from the parent company's valuation system, granting them independent financing channels, incentive spaces, and pricing power while retaining their ability to technically empower Kuaishou's core businesses in short videos, marketing, and e-commerce—rewriting the platform's commercialization logic with AI.

This move is never about 'letting go' but about 'strategic retreat.' Kuaishou aspires to be more than just a short-video platform monetizing through traffic; its ultimate goal is to become an AI-driven ecosystem company.

Editor: Muren Proofreader: Zhang Wenxin Producer: Rui Zong

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle