Dell: AI Surges, Traditional Servers Heat Up, the Old Guard is 'Full of Energy'!

05/29 2026

05/29 2026

487

487

Dell (DELL.N) released its Q1 FY2027 financial results (as of April 2026) after the market closed on the early morning of May 29, Beijing time:

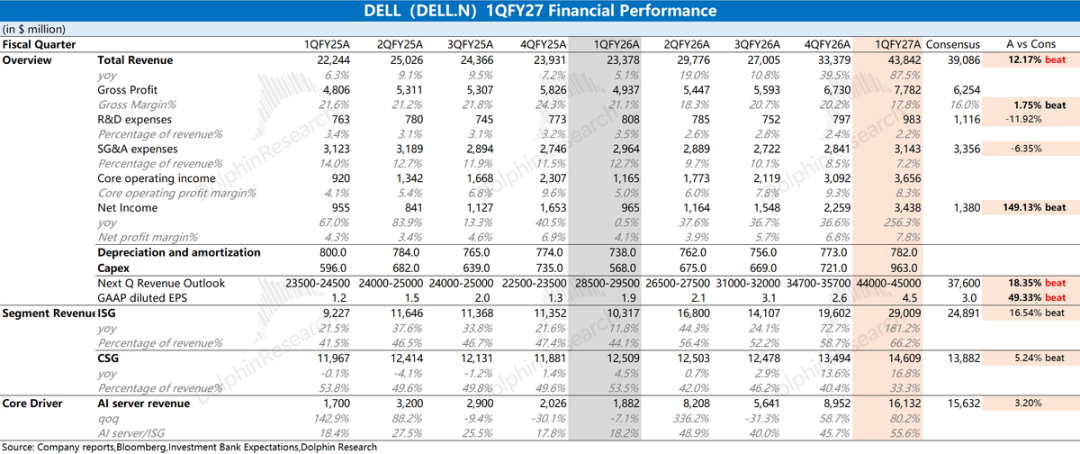

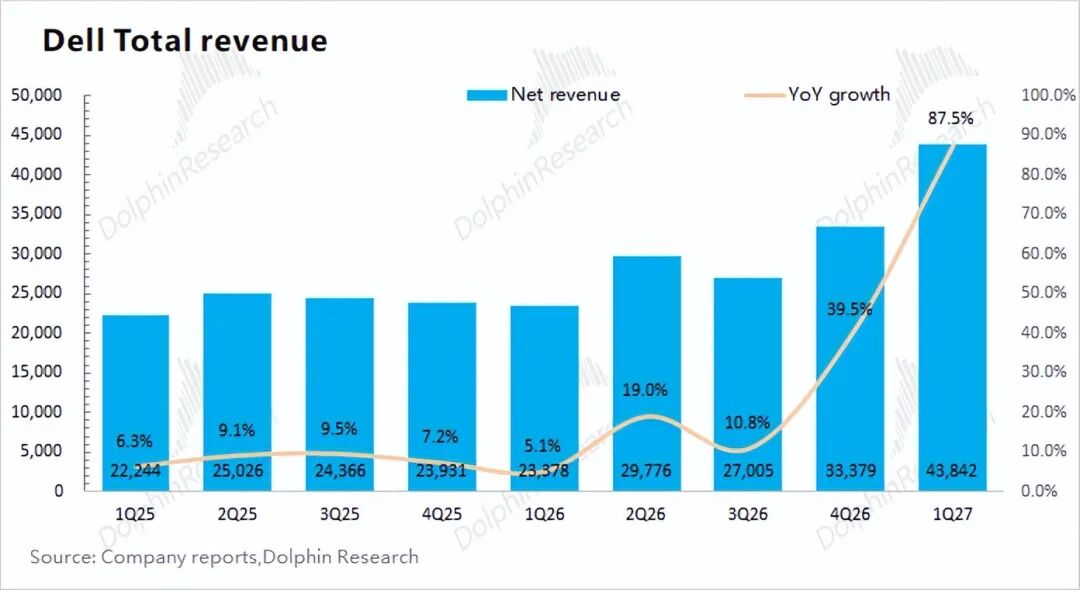

1. Core Performance: This quarter, revenue reached $43.8 billion, up 87% year-over-year, significantly exceeding market expectations ($39 billion). The company achieved a quarter-over-quarter revenue increase of $10.5 billion this quarter, primarily driven by growth in AI server shipments.

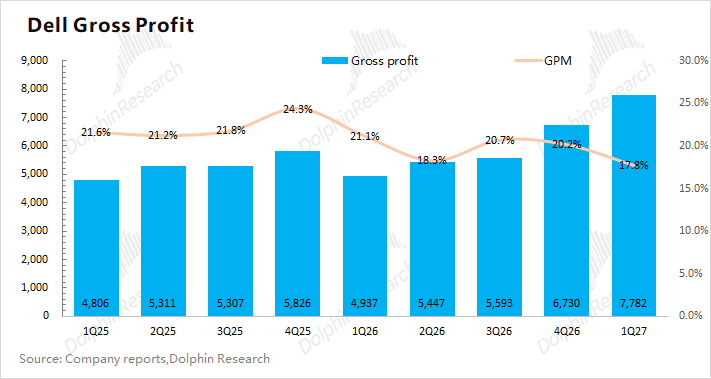

The company's gross margin for the quarter was 17.8%, down 2.4 percentage points quarter-over-quarter but better than market expectations (16%). The decline in gross margin was mainly due to the combined impact of rising storage prices and significant growth in lower-margin hardware products.

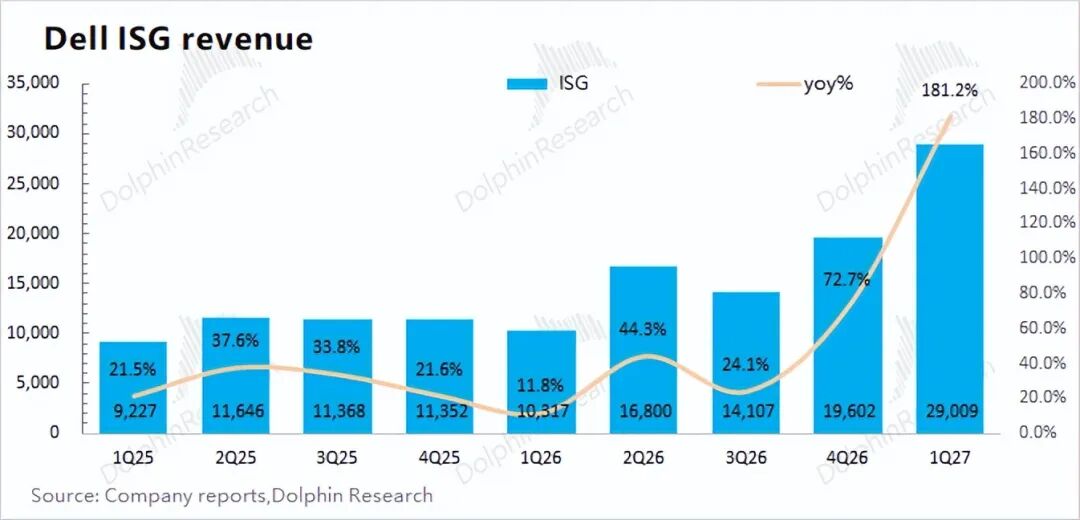

2. ISG Business (Infrastructure Solutions Group): Revenue for the quarter was $29 billion, up $9.4 billion quarter-over-quarter, significantly exceeding market expectations ($24.9 billion). The quarter-over-quarter increase was driven by growth in AI servers and a rebound in traditional servers.

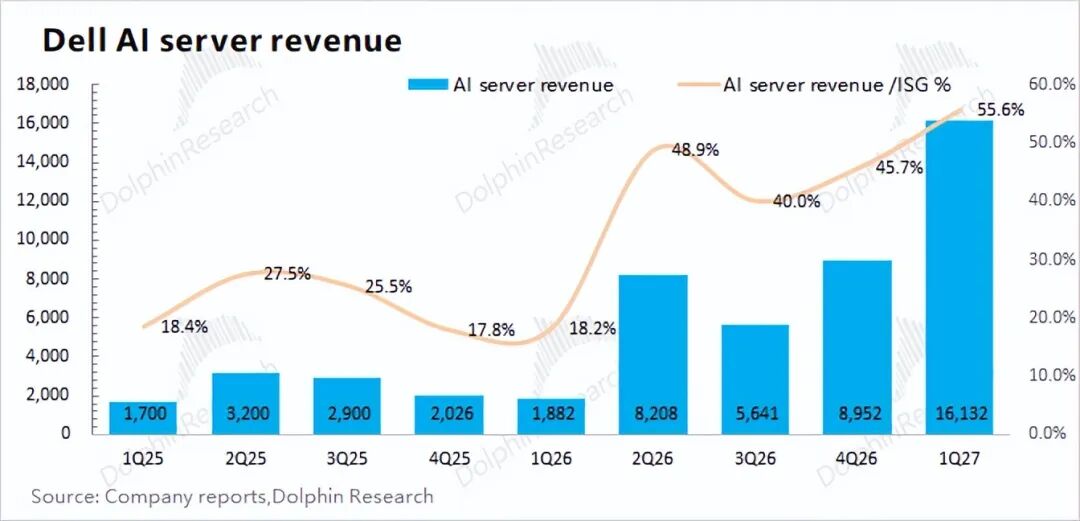

① AI Server Segment: The company's AI server revenue for the quarter was approximately $16.1 billion, better than the raised buyer expectations ($15.6 billion).

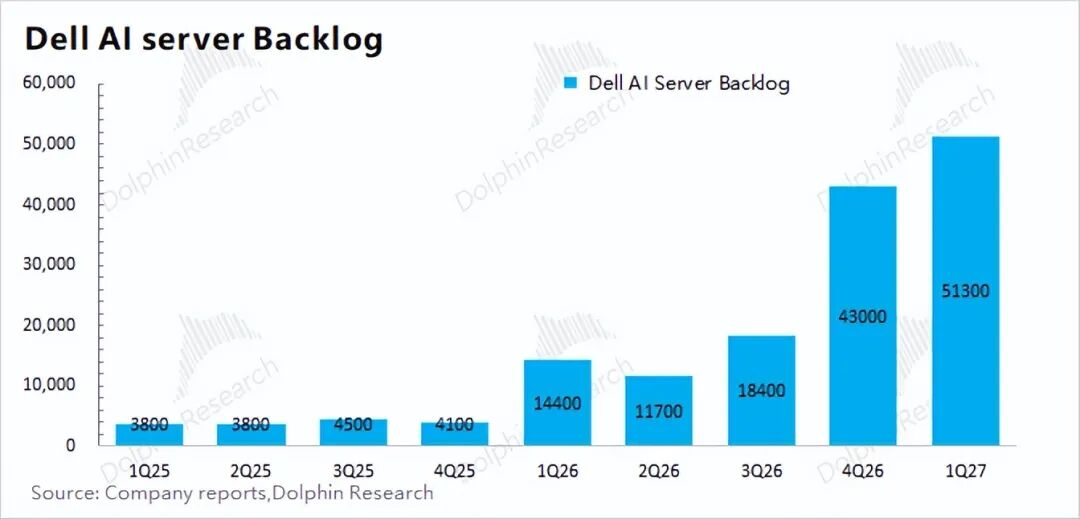

The company's new AI orders for the quarter reached $24.4 billion, with AI backlog orders reaching $51.3 billion by the end of the quarter. Dolphin Research estimates that the company's AI server revenue will exceed $15.5 billion next quarter, indicating a clear situation of 'supply falling short of demand.'

② Other Segments: In addition to AI servers, traditional businesses also saw a significant rebound this quarter. Traditional server-related businesses contributed approximately $8.5 billion in revenue, up 92% year-over-year, significantly exceeding market expectations ($5 billion) and serving as the main source of the quarter's earnings surprise. Storage business contributed around $4.3 billion in revenue, up 8% year-over-year.

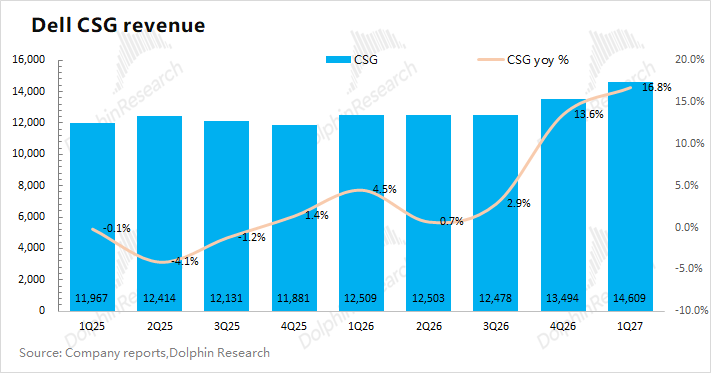

3. CSG Business (Client Solutions Group): Revenue for the quarter was $14.6 billion, up 17% year-over-year, better than market expectations ($13.9 billion). Specifically, Dell's client business remains primarily focused on commercial customers. Revenue from commercial customers for the quarter was $13 billion, up 18% year-over-year, while revenue from individual consumers was only $1.6 billion, up 9% year-over-year.

4. Dell's Guidance for Next Quarter: The company expects revenue of $44-45 billion in the second quarter of FY2027, better than market expectations ($37.6 billion). The company's EPS (GAAP) for the next quarter is projected at $4.5, better than market expectations ($3).

Dolphin Research's Overall View: Fully Exceeds Expectations, with Both AI and Traditional Servers 'Taking Off'

Dell's performance this time fully exceeded expectations, with quarter-over-quarter revenue growth of $10.5 billion, continuing to accelerate. The company's growth this quarter was primarily driven by shipments from the ISG business (servers).

The company achieved $16.1 billion in revenue from its AI business this quarter, up $7.2 billion quarter-over-quarter, better than the raised market expectations ($15.6 billion). The company's new AI orders for the quarter reached $24.4 billion, better than market expectations ($10-15 billion), with backlog orders reaching $51.3 billion by the end of the quarter, laying the foundation for the company's future high growth.

Regarding expectations for AI servers, the market had already raised them before the earnings report. The biggest surprise in this earnings report was the traditional server segment. The company's traditional server revenue reached $8.5 billion this quarter, up 92% year-over-year, significantly exceeding market expectations ($5 billion) and serving as the main source of the earnings surprise.

Originally, the market expected 'steady but moderate growth' for traditional servers, but this time, demand for traditional servers also began to rise significantly.

The recent sustained growth in the company's stock price has been primarily driven by increased market expectations for Dell's AI servers. Currently, the company's AI servers are transitioning from GB200 to GB300, which will directly drive an increase in ASP. The company is benefiting from both volume and price growth, along with the rebound in traditional servers. In particular, the high growth in the AI business has driven the company's valuation upward, breaking through the upper limit of traditional valuation ranges.

The company's management raised its full-year guidance this time, projecting revenue of $165-169 billion for the fiscal year, an increase of $27 billion (previous guidance: $138-142 billion). In fact, this quarter alone exceeded the original quarterly guidance by around $10 billion. Dolphin Research believes that the company's full-year guidance remains relatively conservative and may be raised again in the future.

Beyond the earnings report, the market is primarily focused on the following aspects of the company:

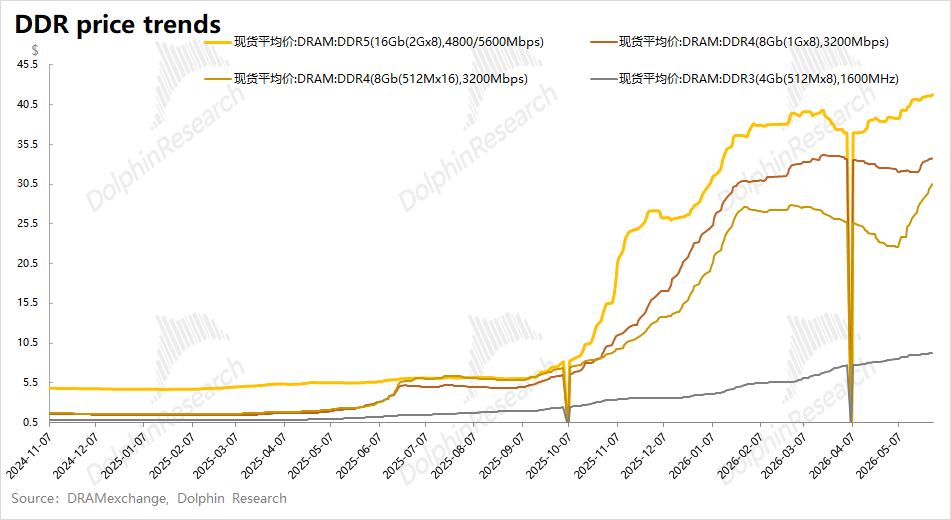

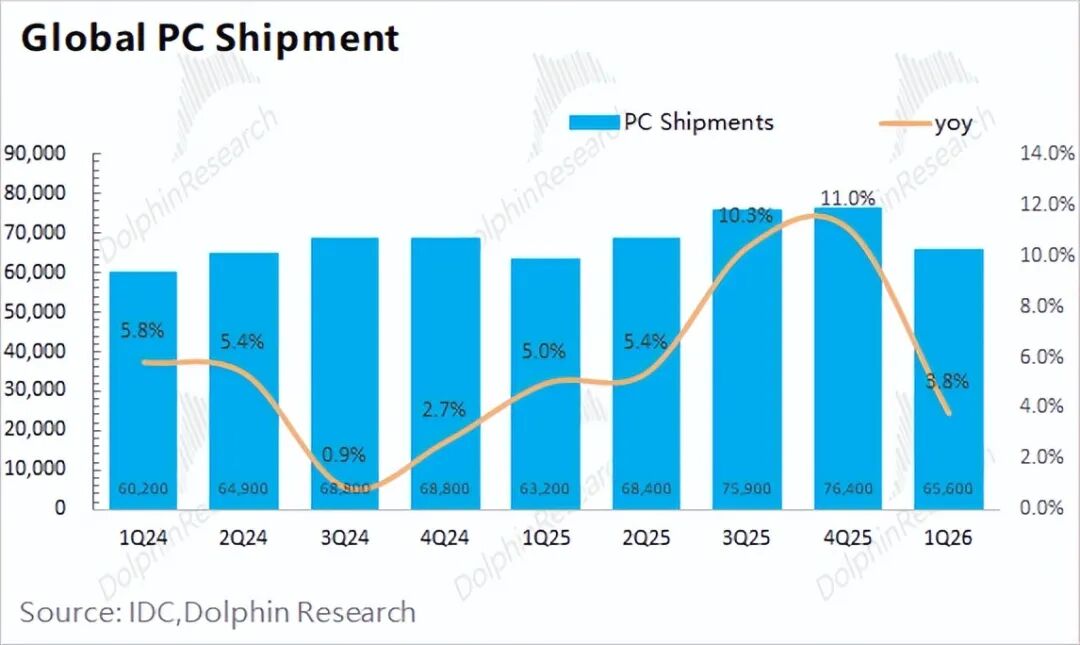

a) The 'tight' storage market: The biggest impact is on the PC sector, where rising storage costs have affected end-market demand through the 'cost -> price -> demand' chain, with overall PC market growth slowing to 4% this quarter.

On the other hand, the sustained rise in storage prices has impacted the gross margins of the company's overall hardware products, including both PCs and servers. The company's gross margin fell sharply to 17.8% this quarter, also affected by the cost increase from rising storage prices. Although the gross margin still declined, it was better than market expectations (16%), demonstrating the company's relatively strong cost management capabilities.

b) AI Servers: With traditional businesses under pressure, AI progress is the company's biggest highlight.

Recently, major cloud service providers have raised their capital expenditure outlooks. Dolphin Research estimates that the four core cloud vendors (Google, Meta, Microsoft, and Amazon) are expected to have capital expenditures exceeding $700 billion in 2026, with year-over-year growth of around 80%.

With continued acceleration in investments by major players, the company's AI server business, which had previously struggled to break through $10 billion, now has market expectations for significant AI growth. The company's AI server revenue reached $16.1 billion this quarter, up $7.2 billion quarter-over-quarter, showing substantial high growth. This reflects both the strong current market demand for AI servers and the increase in ASP due to the upgrade from GB200 to GB300.

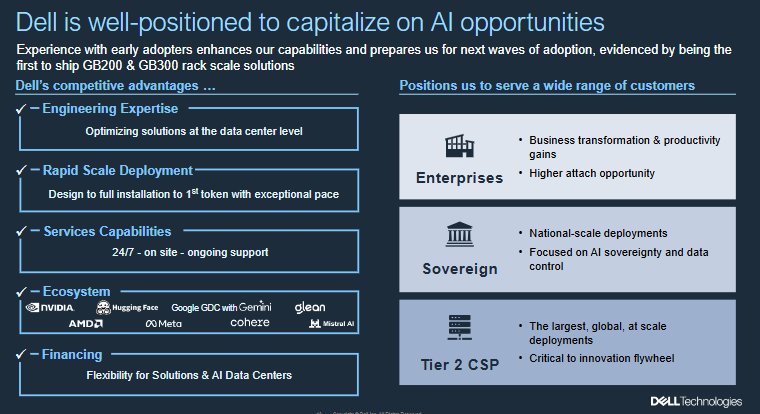

Dell has established deep cooperation with NVIDIA, offering customers choices between different solutions such as Blackwell and Vera Rubin, and participating in the development of the next-generation Feynman platform. Especially in the secondary cloud (Neocloud/Tier-2 CSP) and government-enterprise markets, these customers do not directly purchase from ODMs, as this requires a strong internal team for integration. Instead, they prefer OEMs that can provide complete solutions.

Dell offers full-stack service capabilities, covering everything from desktop AI workstations (GB10/GB300 DGX) -> rack-level servers -> storage -> network switches -> software orchestration (OpenManage) -> services (installation, debugging, 7x24 support). Dell's 'end-to-end' services enable the company to secure more orders in the secondary cloud and government-enterprise markets.

With the recent significant rise in the company's stock price, the market has already factored in expectations for accelerated growth in the company's AI business. Mainstream institutions have raised their AI revenue expectations to $65 billion, up 163% year-over-year. This means the market also expects the company to raise its full-year outlook after this earnings report.

The company's management raised its full-year AI guidance to $60 billion after this earnings report (previously $50 billion), but Dolphin Research believes this is clearly conservative: (1) The company's AI revenue will reach $31.6 billion in the first half of the year, and with the iterative upgrade of Rubin servers in the second half, revenue will not be lower than in the first half; (2) The company's current AI backlog orders exceed $50 billion, and while AI revenue is growing significantly, backlog orders are still increasing, indicating a clear situation of 'supply falling short of demand.'

Overall, Dell's AI business is accelerating, traditional servers are clearly rebounding, and PC business and gross margin performance are also better than expected. The company's operating performance is improving across the board, with opportunities to raise its full-year outlook again in the future. Supported by AI and high earnings growth, the company can no longer be viewed from a traditional perspective, and its valuation is expected to continue breaking through historical upper limits.

Detailed Analysis Below

1. Dell's Overall Performance

1.1 Revenue

Dell achieved revenue of $43.8 billion in the first quarter of FY2027 (26Q1), up 87% year-over-year, meeting market expectations ($39 billion). The company's quarter-over-quarter revenue growth of $10.5 billion was driven by growth in the ISG business (Infrastructure Solutions Group), with AI revenue up $7.2 billion quarter-over-quarter and traditional servers up $2.7 billion quarter-over-quarter.

1.2 Gross Profit

Dell achieved a gross profit of $7.8 billion in the first quarter of FY2027 (26Q1), up 35.6% year-over-year.

The company's gross margin for the quarter was 17.8%, down 2.4 percentage points quarter-over-quarter but better than market expectations (16%).

This was mainly affected by two factors: (1) the impact of rising storage prices on gross margins; (2) the impact of a higher proportion of relatively low-margin ISG business, which structurally diluted the overall gross margin.

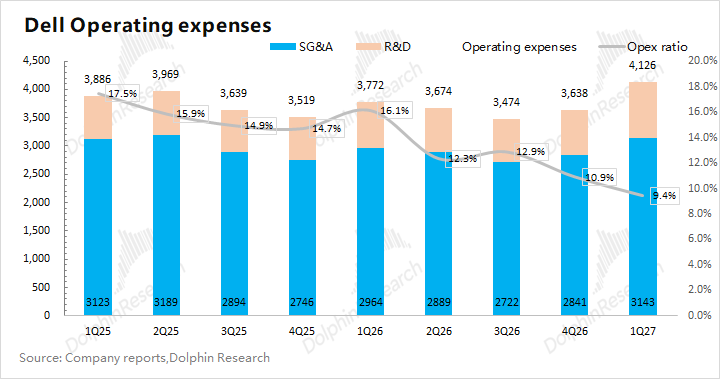

1.3 Operating Expenses

Dell's operating expenses for the first quarter of FY2027 (26Q1) were $4.1 billion, up 9% year-over-year. Due to scale effects, the operating expense ratio fell to 9.4% this quarter.

(1) R&D Expenses: The company's R&D expenses for the quarter were $980 million, up 22% year-over-year, with accelerated growth in R&D spending; (2) Sales and Administrative Expenses: The company's sales and administrative expenses for the quarter were $3.1 billion, up 6% year-over-year.

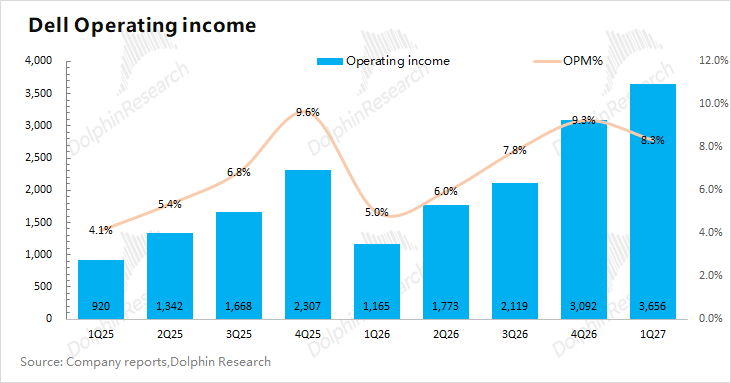

1.4 Net Profit

Dell achieved a core operating profit of $3.66 billion in the first quarter of FY2027 (26Q1), up 214% year-over-year, with a core profit margin of 8.3% this quarter. The growth in profit this quarter was primarily driven by significant revenue growth.

2. Core Business: AI Growth Accelerates, Traditional Business Rebounds

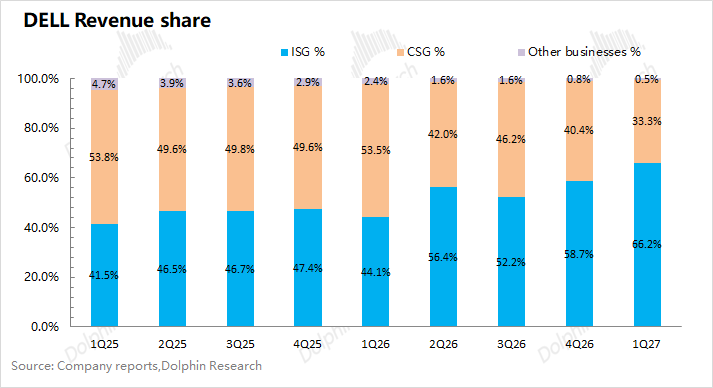

From Dell's business segment performance, driven by growth in AI servers, the company's ISG business (Infrastructure Solutions Group) showed an upward trend, accounting for 66% this quarter.

Based on the company's previous growth guidance, the ISG business is expected to achieve a compound annual growth rate (CAGR) of 11-14% between FY2026 and FY2030, significantly higher than the CSG business (2-3%), with the ISG business's share continuing to rise.

The ISG business is the most critical segment for the company, with specific breakdowns as follows:

2.1 ISG Business (Infrastructure Solutions Group)

Dell's ISG business achieved revenue of $29 billion in the first quarter of FY2027 (26Q1), up 181% year-over-year, significantly exceeding market expectations ($24.9 billion).

Specifically: (1) AI server business revenue was around $16.1 billion this quarter, up $7.2 billion quarter-over-quarter, contributing the majority of the incremental revenue in the company's ISG business; (2) Traditional server and related business revenue was $8.5 billion this quarter, up 92% year-over-year; (3) Storage business revenue was $4.3 billion this quarter, up 8% year-over-year.

The growth in the ISG business this quarter was driven by both AI servers and traditional servers, with traditional servers showing a significant rebound this quarter. High-growth AI business now accounts for over 50% of the ISG business.

Beyond AI revenue for the current quarter, the company's management also provided details on new AI orders and backlog, which are forward-looking indicators. The company secured $24.4 billion in new AI orders this quarter, surpassing market expectations ($10-15 billion). The AI order backlog reached $51.3 billion at the end of the quarter, laying the foundation for sustained high growth in the company's AI business through FY2027.

From a supply-side perspective, Dell has established deep collaboration with NVIDIA, offering customers choices between different solutions such as Blackwell and Vera Rubin, and participating in the development of the next-generation Feynman platform. With upgrades from GB200 to GB300 to Rubin, the average selling price of the company's AI servers will continue to rise.

From a client-side perspective, secondary cloud providers (Neocloud/Tier-2 CSPs) and government-enterprise markets are unlikely to purchase directly from ODMs, as this requires a strong internal team for integration. Instead, they prefer OEMs that can provide complete solutions. Dell's "end-to-end" services make it the preferred choice for secondary cloud and government-enterprise clients, offering opportunities for the company to secure more orders in this market.

Although the company raised its full-year AI business guidance to $60 billion (up from $50 billion), Dolphin Research believes this is relatively conservative. The company achieved $31.6 billion in the first half of the year, and with expected growth driven by Rubin server upgrades in the second half, combined with its current backlog exceeding $50 billion, the company is likely to raise its full-year guidance again.

2.2 CSG Business (Client Solutions Group)

Dell's CSG business generated $14.6 billion in revenue in the first quarter of FY2027 (Q1 2026), up 17% year-over-year, outperforming market expectations ($13.9 billion).

Specifically, Dell's client business remains primarily focused on commercial clients. Revenue from commercial clients reached $13 billion this quarter, up 18% year-over-year, while revenue from individual consumers was $1.6 billion, up 9% year-over-year.

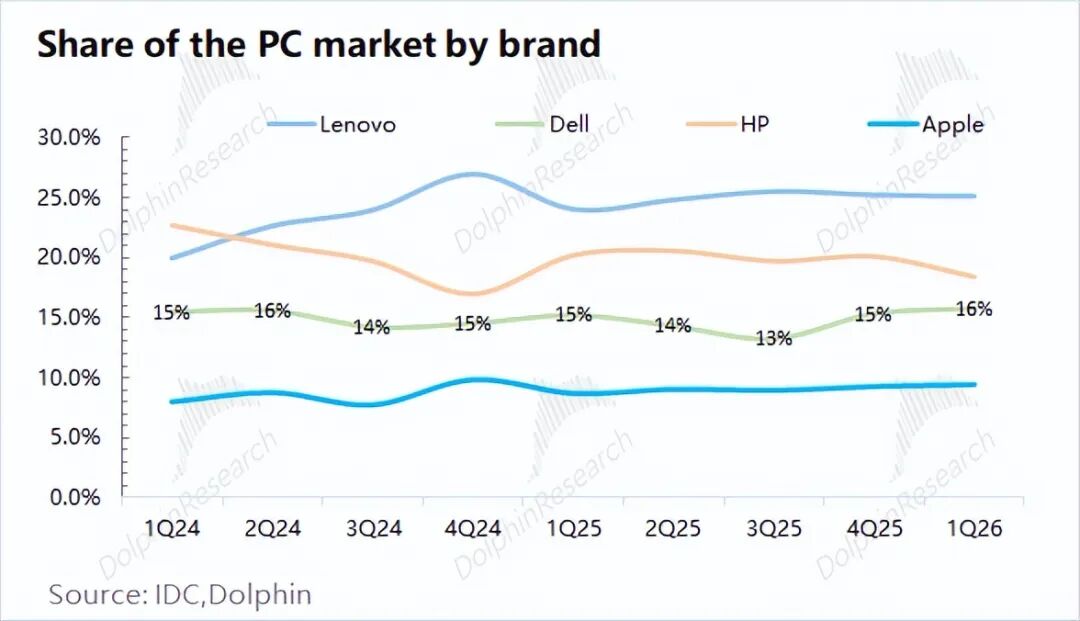

According to global PC market data, global PC shipments reached 65.6 million units in the first quarter of 2026, up 4% year-over-year, with growth significantly slowing. Dell shipped 10.3 million units, up 7% year-over-year, outperforming the industry average and increasing its market share to 15.7%.

Although overall demand in the PC market remains weak, Dell's client base is predominantly commercial, making it less affected by consumer market fluctuations. Notably, the company's commercial PC revenue grew by 18% this quarter.

Additionally, amid rising storage costs, Dell uniformly raised PC product prices earlier in the year. Despite passing on some cost pressures to downstream markets, the company still achieved year-over-year shipment growth, demonstrating its brand strength and management capabilities.

Overall, while "storage shortages" may continue to impact overall PC market demand, Dell's client mix and operational capabilities position its CSG business for steady growth.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprints require authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliates. It does not consider the specific investment objectives, product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses arising from the use of data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, or completeness of the information and data.

The information or opinions expressed in this report shall not, under any jurisdiction, be construed as or deemed to be an offer to sell or a solicitation to buy securities, nor shall they constitute advice, inquiries, or recommendations regarding securities or related financial instruments. The information, tools, and materials in this report are not intended for distribution to, or use by, persons in jurisdictions where such distribution, publication, provision, or use would contravene applicable laws or regulations or result in Dolphin Research and/or its affiliates or subsidiaries being subject to registration or licensing requirements in such jurisdictions.

This report reflects only the personal views, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliates.

This report is produced by Dolphin Research, and its copyright is solely owned by Dolphin Research. Without prior written consent from Dolphin Research, no institution or individual may (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle