Token Price Surges 370-Fold in Five Years: Who's Fueling AI Companies' 'Money Printing'?

05/29 2026

05/29 2026

659

659

Global Capital Is Converging Toward Industry Leaders.

The Fear of Missing Out Trumps Fear of Losses. Throughout May, valuations of AI companies skyrocketed.

Valuations doubled, single-round financing reached new heights, and companies like Yuezhi Anmian secured 2-3 rounds of funding before the year's halfway mark:

DeepSeek, which had previously resisted financing, launched a massive RMB 50 billion funding round, potentially valuing it at over RMB 350 billion. Yuezhi Anmian completed three funding rounds in under six months, raising over USD 3.9 billion cumulatively, with its latest valuation exceeding USD 20 billion. A day later, Jieyue Xingchen reportedly secured nearly USD 2.5 billion in financing, with a post-money valuation approaching USD 10 billion. This year, Mianbi Intelligent and Shengshu Technology have also completed two consecutive funding rounds, with Shengshu Technology valued at over USD 2 billion. While Mianbi Intelligent has not disclosed its valuation, it has crossed the unicorn threshold (over USD 1 billion).

Globally, capital enthusiasm knows no bounds.

In Q1 2026, global AI startups raised USD 255.5 billion, surpassing the total AI venture capital investment for all of 2025. However, two-thirds of this amount came from just three mega-deals—totaling USD 172 billion.

In March 2026, OpenAI announced the completion of a USD 122 billion funding round, co-led by Amazon, NVIDIA, and SoftBank. Just weeks earlier, in February, Anthropic unveiled a USD 30 billion Series F round, attracting top-tier investors such as Singapore's sovereign wealth fund GIC, UAE-based MGX, BlackRock, Blackstone, and Morgan Stanley.

Global capital is converging toward industry leaders.

The financing frenzy intensifies as AI companies demonstrate profitability and the potential to turn losses into gains.

Take Anthropic as an example: CEO Dario Amodei stated at an overseas event that the company's revenue surged 80-fold year-over-year in Q1 2026. Beyond revenue growth, Anthropic expects to achieve its first-ever quarterly profit in Q2 2026, with revenue soaring to USD 10.9 billion and an estimated operating profit of USD 559 million.

As AI company valuations soar beyond expectations, debates over an AI bubble resurface, raising a critical question: Are these valuations justified, or are they a bubble waiting to burst?

AI Companies' Sky-High Valuations: A 100x PS Phenomenon

To assess whether current AI company valuations represent a bubble or reasonable pricing, let's examine how the market evaluates company valuations.

How have valuation logics for AI companies evolved over the past three years? Guangzhui Intelligence analyzed financing data from four AI companies over three years, uncovering some patterns.

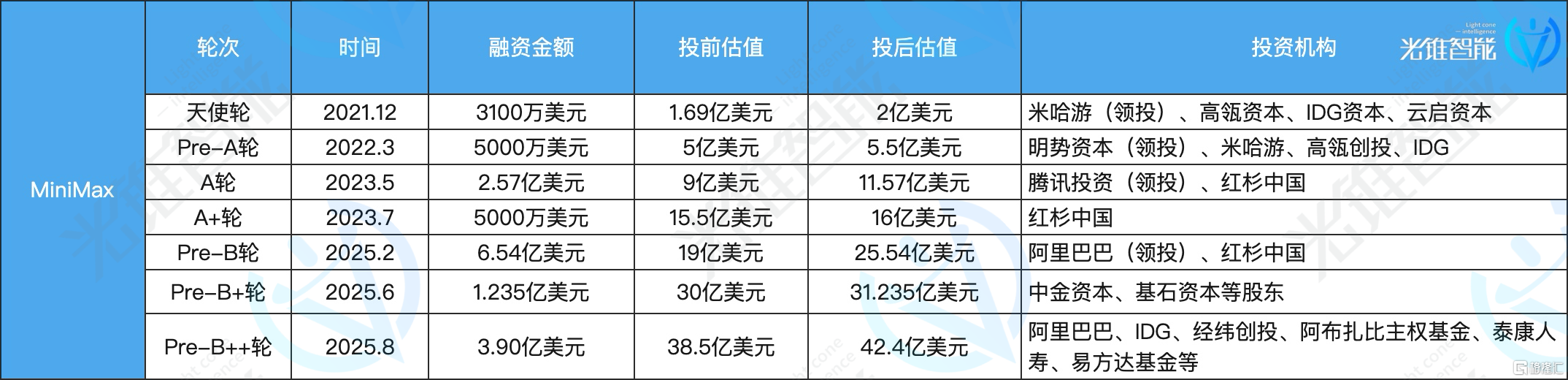

As early entrants, MiniMax and Zhipu were founded before ChatGPT's rise, with their IPOs separated by just one day. Comparing their pre-IPO financing rounds and post-money valuations reveals similarities.

Before going public, both MiniMax and Zhipu commanded price-to-sales (PS) ratios of around 60x, indicating that capital markets held similar expectations for their future market potential:

Using the PS ratio, Zhipu's 2024 annual revenue was RMB 312 million, with a pre-Series B6 valuation of RMB 20 billion in May 2025, implying a PS ratio of approximately 66x. MiniMax's 2024 annual revenue was about USD 30.52 million, with a pre-money valuation of USD 1.9 billion in February 2025, translating to a PS ratio of roughly 63x.

A valuation of around 60x PS suggests that the market holds high expectations for AI companies.

Investor confidence is partly driven by the consistent revenue growth of industry leaders, with acceleration trends becoming increasingly pronounced.

Take OpenAI as an example: In 2024, its annual revenue reached USD 3.7 billion, more than doubling year-over-year. In 2025, revenue is projected to hit USD 12.7 billion, a 243% increase. Anthropic's annual recurring revenue (ARR) also surged ninefold from USD 1 billion in 2024 to an estimated USD 9 billion in 2025.

During the same period, Chinese AI startups maintained similar growth trajectories. MiniMax, for instance, reported USD 30.5 million in annual revenue for 2024, up 782% year-over-year. In the first three quarters of 2025, revenue reached USD 53.437 million, a 174.7% increase.

Given the industry's high growth potential, AI has proven to be a lucrative business. From both business adoption and revenue growth perspectives, high valuation expectations are somewhat justified.

Take API revenue as an example: According to MiniMax's prospectus, its API revenue gross margin reached 69.4% in the first nine months of 2025. As model inference costs decline, gross margins could improve further. The AI industry's growth rate far exceeds that of traditional software, offering investors greater imagination space. Zhipu, for instance, reported 2025 revenue of RMB 724 million, a 131.9% increase, maintaining three consecutive years of revenue doubling.

In terms of investor composition, these companies have secured funding from different sources based on their business focus.

Zhipu has attracted funding from various regional funds and state-backed capital, aligning with its mission to deploy models across regions. MiniMax, which targeted overseas markets from its inception, secured significant funding from Middle Eastern funds, including those from Abu Dhabi. This international background added a premium to its valuation.

While Zhipu and MiniMax follow industry-logic-based valuations, with pricing tied to business adoption, Yuezhi Anmian, which commercialized later, exhibits a different valuation approach, with a significantly higher PS ratio than its predecessors.

Yuezhi Anmian's pre-2026 investors primarily included traditional VC firms and internet giants—Meituan, Tencent, and Alibaba took turns investing, with support from veteran capital firms like Sequoia China and IDG.

However, through heavy investment from internet companies and the viral success of its long-text AI assistant Kimi, Yuezhi Anmian managed to boost its valuation. According to LatePost, Yuezhi Anmian, which sought investment from Xiaohongshu and others at a USD 900 million valuation in late 2023, raised its pre-money valuation to USD 1.5 billion after Alibaba's USD 800 million investment.

Following the February 2024 launch of its long-text feature and the viral success of Kimi, driven by marketing and user advocacy, Yuezhi Anmian's valuation skyrocketed, reaching a post-money valuation of USD 2.5 billion.

Despite being the last among these companies to commercialize, Yuezhi Anmian's valuation surpassed its peers. In January 2024, Zhipu's post-money valuation was RMB 7.2 billion, half of Yuezhi Anmian's.

Although Yuezhi Anmian did not disclose specific revenue figures initially, based on its K2.5 model generating over USD 100 million in ARR within a month of its 2026 launch and surpassing 2025's full-year revenue within 20 days, we roughly estimate its 2025 revenue at around USD 8.33 million. Even at its August 2024 Series B post-money valuation of USD 3.3 billion, Yuezhi Anmian's PS ratio approached 400x—significantly higher than Zhipu and MiniMax at the time.

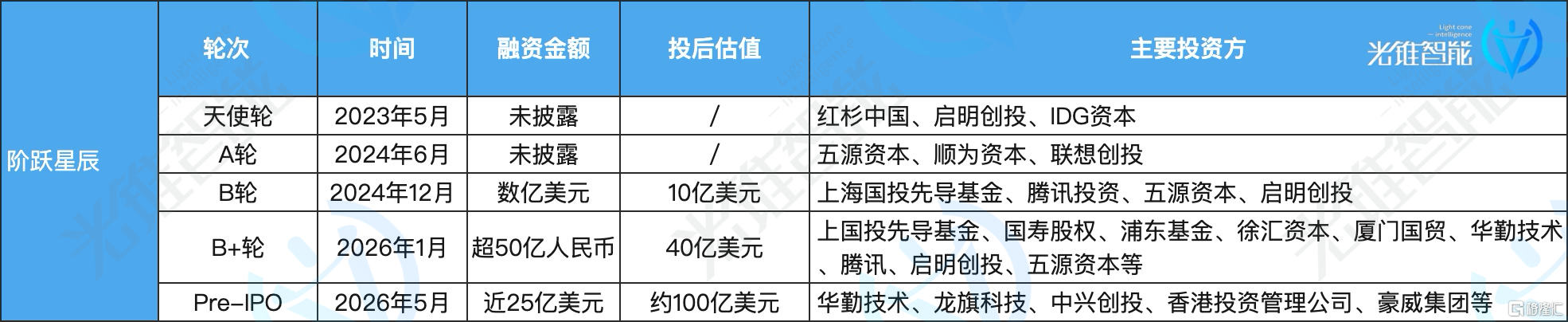

In contrast, Jieyue Xingchen, which pivoted its strategy, saw its PS ratio fluctuate like a rollercoaster. After approaching Yuezhi Anmian's 200x level, it fell back to a range similar to Zhipu and MiniMax's early PS ratios after shifting to a B2B focus.

Initially focused on "super models + super apps," Jieyue Xingchen secured hundreds of millions of dollars in funding from Shanghai State-owned Investment and Tencent Investments, valuing it at USD 1 billion. Based on media reports of RMB 30 million in 2024 annual revenue, its PS ratio reached 233x, closer to Yuezhi Anmian's.

However, since pivoting to B2B in early 2025 and focusing on agent deployment in intelligent terminals, Jieyue Xingchen's PS ratio declined to around 56x, aligning with Zhipu and MiniMax's pre-IPO levels, based on a USD 4 billion post-money valuation in early 2026 and RMB 500 million in 2025 revenue.

Reviewing the valuation trajectories of these four companies, the early market demonstrated some consensus on investing in AI companies. While "rocket-like" valuation surges existed, the upper limit based on business logic hovered around 60x PS.

However, after 2026, the valuation models for AI model companies underwent significant changes.

The Valuation Leap of DeepSeek and Longxia AI Companies

From the similar valuation logics of AI companies in 2024 to their current "soaring" valuations, two key stages have reshaped AI financing:

The first stage began in 2025 with DeepSeek's disruption. Its R1 model, comparable to overseas counterparts, caused a stir. Its impact was dual-edged, bringing both opportunities and pressure.

On one hand, DeepSeek shifted AI startups' focus back to technology-first approaches amid the 2024 commercialization (commercialization) scramble. It proved the existence of technological dividends, with its AI assistant achieving viral success without paid marketing and indirectly driving user adoption of other AI products, educating the market.

Building on this, faster-commercializing companies like MiniMax and Zhipu accelerated financing and IPO plans based on initial revenue growth. Slower commercializers, such as Yuezhi Anmian, focused more on model development (e.g., K2).

On the other hand, DeepSeek's cost-effectiveness highlighted the imminent arrival of closed-loop AI applications, but capital flowed more toward agent-led AI product companies than AI large model firms.

As deep thinking models matured, they required engineering-driven product interventions to ensure stable multi-round task execution, shifting from providing answers to truly assisting users. Thus, agents permeated various industries.

"DeepSeek's emergence has bottlenecked financing for large models," said Hu Shuo, partner at Gaorong Capital, in a public statement.

In 2025, Yuezhi Anmian and Jieyue Xingchen faced financing gaps of over a year. Yuezhi Anmian announced a new funding round in December 2025, 16 months after its previous round. Jieyue Xingchen also experienced a 12-month funding hiatus, a stark contrast to their previous 3-6 month financing cycles.

Fortunately, a second turning point arrived a year later. In 2026, the popularity of Longxia (Clawdbot) ignited the token consumption logic.

From Longxia's January 19, 2026, launch to its viral success by month-end, and throughout the Lunar New Year, various domestic platforms rolled out Longxia-like products.

Unlike traditional dialogue, where users ask one question and AI responds, consuming hundreds to thousands of tokens per interaction, Longxia tasks could run for half an hour or longer, burning tokens through each reasoning step, tool call, and self-correction. A simple "weekly report" task might involve opening emails, reading documents, drafting content, and sending previews—consuming dozens to hundreds of times more tokens than standard dialogue.

This validation arrived faster than expected. As Longxia went viral, Zhipu and MiniMax, whose models powered Longxia, saw their market caps surge.

Take MiniMax: After its flagship model, MiniMax 2.5, became Longxia's base model and topped OpenRouter's consumption rankings, its market cap growth steepened from late January, breaking through previous ceilings. Zhipu and MiniMax followed nearly identical trajectories, with acceleration starting in late January.

For model base companies, agent-driven token consumption has raised the commercialization ceiling to astonishing heights.

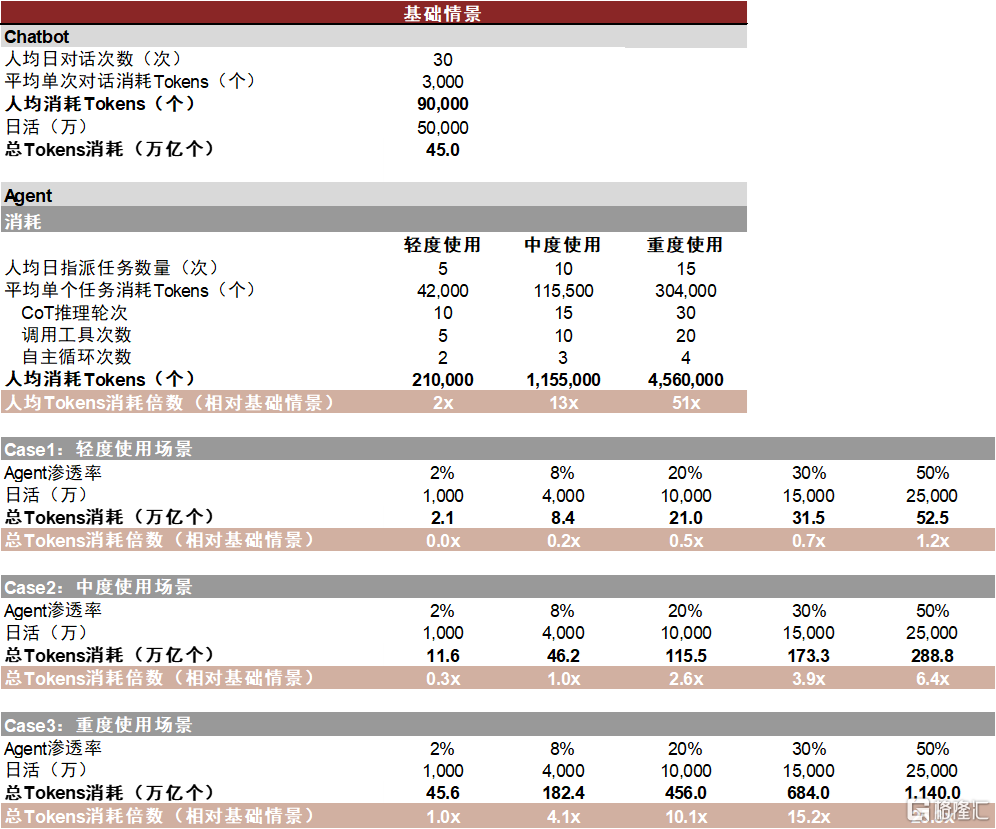

CICC noted in a research report that when agent penetration reaches 8%, total token consumption from agents equals that of chatbots. If agent usage surges to 16% penetration, token consumption doubles.

When an uncertain path suddenly transforms into a clear highway, the soaring valuations of large model companies are no surprise.

But AI company valuations must have a ceiling.

Valuations Soar as Capital Chases the Next Era

To understand whether the current valuations of domestic AI companies are reasonable, besides looking at industry development, Anthropic serves as a good reference.

As the biggest competitor of OpenAI, Anthropic has achieved a valuation surpass, and is about to end losses and welcome its first profitable quarter.

According to foreign media reports, Anthropic is about to complete a new round of financing, with total financing expected to exceed $30 billion, and the company's valuation is expected to surpass $900 billion. As valuations soar, Anthropic's revenue has more than doubled, with Q2 revenue this year expected to reach $10.9 billion and an operating profit of $559 million.

Most of Anthropic's revenue comes from the B-side. At the end of last year, Anthropic CEO Dario Amodei predicted that over 80% of the company's revenue in the coming year would come from selling AI models to enterprises.

The surge in revenue also stems from the successful implementation of AI application scenarios, with a significant increase in model token consumption by enterprises and developers. Its CEO also stated this year that in two months, the number of enterprise clients spending $1 million on the Claude platform rose from 500 to 1,000.

Anthropic's revenue has sustained growth (continuously increased) for three years. Source: X@Anthropic

Over the past two years, with the establishment of the token-selling business, Anthropic's estimated PS (Price-to-Sales) ratio has been declining, gradually returning to a normal range.

Based on an annualized revenue of $40 billion, Anthropic's current PS ratio is around 22 times. However, going back to the end of 2025, with an annualized revenue of $87 million in early 2024 and a valuation of $18.5 billion in February of the same year, the company's PS ratio was as high as 212 times.

The decline in PS indicates that Anthropic is maturing. The previously expected "hypothetical" revenue is starting to appear on the company's books, and the company's future growth potential is no longer "elusive." For example, in the Coding sector, Anthropic has almost become the de facto "king." When it becomes a consensus for programmers to use Claude Code, it means that in the Coding sector, Anthropic has lost its explosive growth potential.

On the domestic front, the growth of AI companies currently shows no sign of hitting a "ceiling." Although domestic progress still lags behind that of top overseas companies, the exponential growth in token consumption provides the confidence for capital markets to offer high premiums.

According to official company disclosures, MiniMax's daily token consumption in February 2026 had grown to more than six times that of December 2025, with consumption in the Coding plan increasing more than tenfold; after Zhipu released its Coding plan in September 2025, token consumption in the coding plan grew 15-fold within six months.

As for how much room there is for future growth, JPMorgan predicted in a report this year that China's AI inference token consumption will grow from about 10 quadrillion in 2025 to about 390 quadrillion in 2030, a 370-fold increase over five years. This translates to a staggering compound annual growth rate of 227% over five years.

The soaring valuations of Chinese AI companies are not an isolated case. Overseas, to lay the foundation for AI and build AI data centers and infrastructure, a host of tech giants are Crazy bond issuance ( Crazy issuance of bonds , madly issuing bonds) to secure a ticket to the future.

In March this year, Amazon issued a total of $37 billion in bonds in the U.S. bond market and €14.5 billion in bonds in Europe the next day; in April, Meta issued a total of $25 billion in bonds on April 30, and Google's parent company Alphabet also issued €9 billion and CAD 8.5 billion in bonds that month. According to statistics, so far in 2026 alone, these hyperscale tech companies have issued approximately $110 billion in bonds, accounting for more than 15% of the total issuance of U.S. investment-grade bonds.

If previous AI investments were reinvestments based on these giants' income statements, with annual "spending" from earned profits, then borrowing to invest in AI is already a "bet on the future."

As capital floods into the AI sector with such momentum, we are witnessing the growth of an industry—in this race that will determine the tech landscape for the next few decades, no capital is willing to miss such an opportunity.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle