Who Captures the Lion’s Share of Wealth in the AI Era?

05/29 2026

05/29 2026

422

422

It’s widely acknowledged that the AI boom is generating substantial wealth. From SK Hynix to NVIDIA and now Changxin, companies are reporting soaring profits. Yet, the reality that wealth is heavily concentrated at the upstream end of the supply chain is rarely discussed. Cloud service providers and large-model companies in the midstream and downstream sectors are still struggling to turn a profit. The question remains: How sustainable is this wealth narrative?

The AI wave is surging, propelling the entire industrial chain forward. From NVIDIA to SK Hynix and on to Changxin Memory, financial results are reshaping perceptions. The wealth myths of the AI era are unfolding one after another. However, amid this wave of wealth creation, a critical but often overlooked detail is that wealth is being concentrated in the hands of a select few to an unprecedented degree. Rather than viewing it as a simple dividend of AI development, this phenomenon represents a new reconfiguration of the wealth landscape. Some have ascended to the pinnacle of the pyramid, while others remain on the fringes, struggling to keep pace.

Upward Signals from Two Financial Reports: NVIDIA and Changxin

Recently, the release of two financial reports nearly simultaneously ignited the capital market. Changxin Technology’s IPO prospectus on the STAR Market prompted the investment community to exclaim, “China’s SK Hynix has arrived.” Data shows that in the first quarter of 2026, Changxin Technology reported revenue of 50.8 billion yuan and net profit attributable to shareholders of 24.762 billion yuan, representing year-on-year increases of over sevenfold and sixteenfold, respectively.

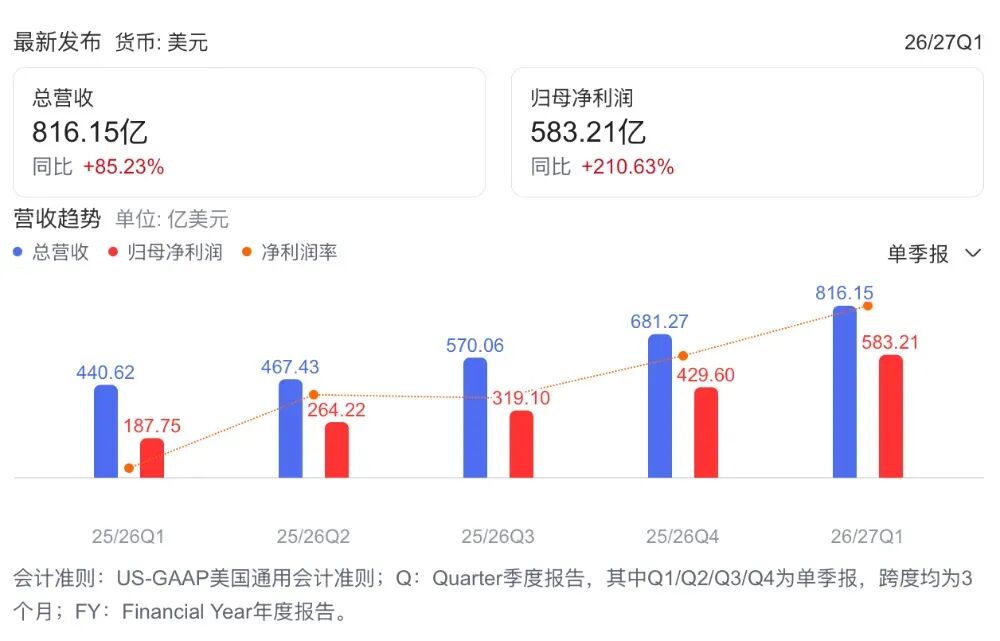

Capital market estimates of its post-IPO market value are extremely optimistic, predicting it will soar to over 2 trillion yuan. This figure even exceeds the total market value of 124 A-share listed companies in Nanjing. Almost simultaneously, NVIDIA released its financial report for the first quarter of fiscal year 2027. The report showed quarterly revenue of 81.6 billion USD and net profit of 58.3 billion USD, both far exceeding market expectations. Among these, the data center business contributed 75.2 billion USD, accounting for 92% of total revenue.

On one side is the global leader in AI computing chips, and on the other is China’s leading storage chip manufacturer. They operate in different segments of the industrial chain but have delivered equally astonishing results. The underlying logic is straightforward: as core players upstream in the AI development industrial chain, they possess extremely high technical barriers, long capacity-building cycles, and large, loyal customer bases. These advantages have allowed “NVIDIA and its peers” to secure the largest slice of the pie in the AI wave.

Middle and Downstream Players: Participants on the Fringes of the Trend

While upstream players in the industrial chain are thriving, those in the midstream and downstream sectors appear to be struggling. Consider the following data: According to TrendForce estimates, in 2026, capital expenditures by the world’s four largest hyperscale cloud service providers (Google, Microsoft, Amazon, and Meta) will surge to 725-755 billion USD. In 2025, this figure was only 359 billion USD. Estimates for the combined capital expenditures of the world’s nine largest cloud service providers are projected to soar to approximately 830 billion USD.

This means that the annual hardware expenditures of the four major cloud providers already exceed the combined revenue of all AI chip and storage manufacturers. Cloud providers are effectively fueling the upstream sector with massive capital investments. What is most frustrating for these providers is that they have not yet achieved scalable profitability in their AI businesses but must continue to increase their bets. If they stop investing, they risk falling behind in the race for AI infrastructure. This explains why, despite NVIDIA’s better-than-expected performance, its stock price still fell after hours. The market’s concern has never been about this quarter’s profits but rather how much longer downstream cloud providers can sustain their capital expenditure pressures.

If one day, cloud providers begin to cut back on procurement, can NVIDIA’s growth story continue? Shifting our focus back to China, the situation is equally complex. Currently, domestic large model startups generally face dual pressures: massive R&D investments on one hand and unproven business models on the other.

Early on, many companies adopted a free model to capture market share. Now, when they try to shift to a paid model, most users are unwilling to pay. For the average user, the value of large models is limited to “retrieving information” and “assisting with text output,” with far lower willingness to pay than expected. This stands in stark contrast to the hundreds of billions in profits enjoyed by upstream chip manufacturers. Ultimately, the profit distribution in this industrial chain follows a simple yet brutal logic: whoever possesses something that others cannot produce holds pricing power; whoever engages in replaceable processes can only earn meager profits. However, this logic has an important premise: it assumes that the global AI industrial chain is a unipolar landscape dominated by international giants like NVIDIA and SK Hynix. But the reality is that another track is growing in parallel.

China’s ‘Local Story’: A Computing Closed Loop is Taking Shape

Many people are unaware that the global AI computing industrial chain is currently evolving along a “dual-track” trajectory. One track is the international supply chain centered around NVIDIA and SK Hynix; the other is China’s local supply chain centered around Huawei Ascend and Changxin Memory. In the Chinese market, a local supply chain for AI computing is forming its own closed loop. Huawei Ascend is NVIDIA’s most formidable local competitor. In 2025, Ascend tied with NVIDIA for first place in China’s AI chip market with a 40% share. Some large models, including DeepSeek, are gradually reducing their reliance on NVIDIA’s computing chips and instead adapting to Huawei Ascend. Multiple agencies predict that by 2026, Huawei will capture 50% of China’s AI chip market, while NVIDIA’s share will plummet from 95% three years ago to around 8%.

In the storage sector, domestic substitution is also accelerating. Changxin Technology’s transformation from a decade of losses to a quarterly profit of 24.7 billion yuan, with its global market share rising to 7.67%, is the most compelling evidence. A clear picture is emerging: cloud providers are pairing domestic chips for computing power and domestic storage for storage capacity, forming a complete local supply chain that is already taking shape. If there is one missing piece, it is the localization of HBM (High Bandwidth Memory)—once achieved, China’s AI computing infrastructure will truly achieve autonomous closure.

Underestimated Cyclical Risks: How Long Will the Wealth Feast Last?

Amid this AI frenzy, everything appears prosperous on the surface. However, the history of the storage industry has repeatedly proven that the companies standing at the peak and those in the valley are often the same batch. Changxin’s explosive performance is highly dependent on the DRAM price rally. According to TrendForce data, since the second half of 2025, DRAM prices have continued to rise, with some specifications surging by over 100%. In the first quarter of 2026, DRAM contract prices saw further quarter-on-quarter increases of 93-98%. If DRAM prices fall, how much of Changxin’s profit will remain? Of its quarterly net profit of 24.7 billion yuan, how much is a testament to the company’s own capabilities, and how much is simply “being at the right place at the right time”? Changxin Technology’s prospectus explicitly mentions the history of widespread losses during the industry’s downturn cycle from 2022 to 2023 under “Special Risk Warnings.” NVIDIA is not immune to such cyclical risks either. If cloud providers’ enthusiasm for capital expenditures wanes or the commercialization of AI applications falls short of expectations, the retreat of infrastructure investments could arrive faster than imagined.

Reflections on the Industrial Landscape: Who Will Stand at the Pinnacle in the Next Cycle?

The value chain of the AI industry is forming a clear hierarchical structure: the infrastructure layer captures most of the profits, the service layer bears cost pressures, and the application layer is still struggling to acquire users. Profits are concentrated upstream, while costs are shifted downstream. In China, thanks to the rise of companies like Huawei Ascend and Changxin Memory, a complete closed loop for local AI infrastructure is being drawn. However, cyclical risks cannot be ignored. The history of DRAM prices has repeatedly proven a simple truth: the most profitable moments are often the most dangerous. As investment enthusiasm for AI infrastructure reaches unprecedented heights, sustainability becomes an unavoidable question. This chain of “profits flowing upward and costs shifting downward” may hold logically but remains untested in terms of long-term commercial viability. The answer to this question will determine who can continue standing at the pinnacle in the next cycle.

- END -

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle