Starting at 9.9 Yuan: China’s Telecom Giants Dive into Token Economy. Will AI Be as Easy to Access as Mobile Data?

05/29 2026

05/29 2026

508

508

By | Xiaofeng

Source | Bowang Finance

A Token war has erupted. Previously, Jensen Huang leveraged AI chips like GPUs to sell Tokens, driving a staggering 85% quarterly revenue surge. Now, China is witnessing a surge in Token exports, with companies rushing to sell Tokens globally.

Domestically, the action is heating up. In May 2026, China’s telecom sector reached a historic turning point as China Mobile, China Unicom, and China Telecom jointly launched Token computing power packages.

At China Telecom, a mere 9.9 yuan/month grants access to 10 million Tokens.

The telecom industry is clearly shifting from “traffic management” to “Token management.” Has the traditional monthly subscription model reached its end? Operators are attempting to redefine their commercial value with AI-era “phone bills.”

However, this transformation is fraught with challenges. Will the Token business revive the telecom industry, or is it just another overhyped trend?

01

Is the Traditional Monthly Subscription Model Obsolete?

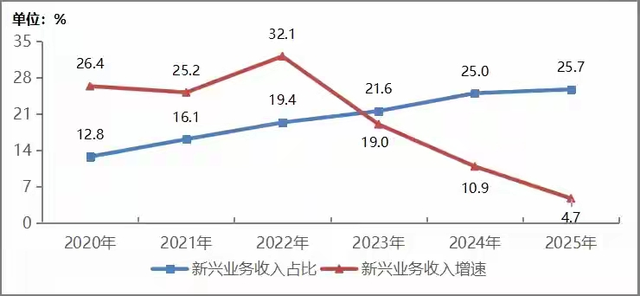

Is the golden age of China’s telecom industry fading? The once-lucrative data traffic business, which fueled operator profits, has now become a low-margin—or even loss-making—grind.

In 2025, China’s telecom industry generated 609.7 billion yuan in revenue from mobile data services, a 3.1% decline year-on-year. Its share of total telecom revenue dropped from 36.2% to 34.8%, marking rare negative growth. Financial reports from the three major operators also revealed operational pressures. In Q1 2026, net profits attributable to shareholders fell across the board: China Unicom by 18%, China Telecom by 17.08%, and China Mobile by 4.2%. Traditional telecom businesses urgently need new growth drivers.

A clear pattern emerges in the telecom industry’s evolution: each era has its core billing unit. In the voice era, operators sold calling minutes; in the SMS era, they sold text messages; in the data era, they sold gigabytes of traffic. Each technological shift spawned new billing methods and growth opportunities. But once a product becomes infrastructure, profits are infinitely diluted.

Today, data traffic is as essential as water, electricity, and gas. User demand for traffic continues to rise, but pricing dynamics have shifted. To compete for users, price wars have intensified, and low-cost packages have proliferated. The result? Users consume more traffic, but competition has become fiercer.

Moreover, instant messaging apps like WeChat and QQ have replaced traditional SMS and voice calls, while short-video platforms like Douyin and Kuaishou consume most of the traffic. However, operators only earn meager pipeline fees, with the real profits going to internet companies. This “pipelining” dilemma has plagued operators for over a decade.

Long-term revenue growth for all three operators fell below 1% in 2025, and net profit growth hit a six-year low. The industry’s slowdown has persisted for over a year. Traditional voice and broadband businesses have peaked, and cloud service growth, which previously drove expansion, has also slowed significantly. The support from old growth drivers continues to weaken.

To escape this predicament, operators have explored numerous transformation paths, from early value-added services to later ventures in cloud computing, big data, IoT, and now AI. However, most attempts have fallen short of expectations. While cloud computing has grown rapidly, it still lags far behind Alibaba Cloud and Tencent Cloud, and profitability remains a challenge. Overall, the industry grew by 4.7% last year, a modest increase.

The iron law of business is that few industries remain perpetually sunrise; only evolving companies do. When traditional growth engines stall, operators must find new drivers. Tokens in the AI era are precisely the next core billing unit they’ve been seeking. The shift from selling minutes to traffic to Tokens represents not just product iteration but a fundamental transformation of the telecom business model.

02

Why Are Operators Targeting Tokens?

Before diving in, we must clarify what Tokens are and how the Token consumption closed loop works. Currently known as “word units” in China, Tokens are widely regarded as the “industrial oil” of the AI era. Without Tokens, large models cannot function, and AI cannot serve humanity.

Strictly speaking, Tokens are the smallest computational units for large models to process text, images, and voice. In Chinese text, one Token roughly corresponds to 1.5 to 2 characters (including punctuation), so 1,000 Tokens equate to about 500-700 characters. When you ask, “How’s the weather in Beijing today?” AI breaks it down into five or six Tokens for processing. Every character in its response is also a Token. In short, every AI interaction consumes Tokens.

How large is the Token market?

Data from the National Data Bureau shows that in early 2024, China’s daily average Token consumption was 100 billion; by the end of 2025, it surged to 100 trillion; in March this year, it exceeded 140 trillion, a thousandfold increase in two years.

This growth far outpaces the internet and mobile internet booms. JPMorgan predicts that by 2030, China’s Token consumption will increase another 370-fold. This is a trillion-yuan blue ocean market that no company can afford to ignore.

Operators are well-positioned to capitalize on the Token economy due to their unique advantages.

First is their massive user base. The three major operators collectively serve over 1.7 billion mobile users, covering nearly all internet users in China. This allows them to push Token packages directly to every mobile user at virtually zero marginal cost—an advantage unmatched by any large model firm or internet company.

Second is their mature payment infrastructure.

Operators boast the most convenient phone bill payment systems, significantly lowering user adoption barriers.

Third is their robust computing infrastructure. After years of investment, the three operators have built China’s leading intelligent computing networks. These resources are the foundation for Token production.

Compared to large model firms, operators’ Token models offer distinct advantages. Currently, large model firms charge Tokens model-specifically—Tokens bought from OpenAI only work with GPT. Industry insiders emphasize that for ordinary users, opting for telecom operators eliminates the hassle of choosing large models. Users seeking multiple AI services no longer need to download multiple apps; operators can provide a single interface for all.

Evidently, operators are actively transitioning from “selling communications services” to “selling computing power and intelligent services.” By selling Tokens, they are repackaging their decades-accumulated networks, users, and payment capabilities into universal AI infrastructure. Their goal isn’t to compete with large model firms but to become the “power companies” of the AI era. Just as grid companies don’t manufacture appliances but power them, operators won’t develop all AI applications but will provide computing power and Tokens for them.

03

Telecom AI Services: Still a Gimmick?

While operators’ Token packages seem promising, we must recognize that this business is still in its infancy and faces multiple challenges. In the short term, the Token business is unlikely to become a core revenue stream for operators.

The most immediate issue is inconsistent product experience. Currently, operators’ Token packages primarily integrate their proprietary large models and some third-party models, but these lag significantly behind top-tier models in performance.

China Telecom’s Xingchen, China Mobile’s Jiutian, and China Unicom’s Yuanjing models, while strong in certain verticals, fall short of DeepSeek, Zhipu GLM, and other leading models in general capabilities.

Functionality also needs improvement. User demand for AI has expanded beyond basic chat and writing to images, videos, audio, and more. Text-only functions struggle to meet diverse needs.

Another critical point is ecosystem development. Competition in the AI era is fundamentally about ecosystems. Internet giants have already built relatively complete AI ecosystems, spanning office, entertainment, education, healthcare, and other fields with a proliferation of AI applications.

Commercially, if operators continue to sell Tokens with a “traffic-selling” mindset, focusing solely on volume rather than user experience, they risk repeating the mistakes of the traffic business.

The popularization of any new technology takes time. The transition from traffic to Tokens won’t happen overnight. Operators must humble themselves, truly center on users, refine product experiences, and build open ecosystems. They need deep collaboration with large model firms, AI app developers, and hardware vendors to jointly advance the Token economy. Only when users genuinely perceive Token value and willingly pay for AI capabilities will operators’ Token business truly succeed.

From selling minutes to traffic to Tokens, each transformation by the three major operators reflects the trajectory of China’s digital economy. The 9.9-yuan Token package is just the beginning. In the future, when AI permeates every aspect of our lives and every smart interaction consumes Tokens, we may indeed pay for AI capabilities monthly, just like phone bills.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle