Wang Xiaochuan and Li Kaifu Navigate the 'Controlled Descent' of China’s AI ‘Six Little Tigers’

06/01 2026

06/01 2026

490

490

It’s Time for AI Entrepreneurs to Land

Had you asked Chinese tech investors two years ago which of the six AI large model startups was poised to become the ‘king,’ the consensus would likely have pointed to two names: Li Kaifu’s 01.AI and Wang Xiaochuan’s Baichuan Intelligence.

One brandishes the prestige of Silicon Valley and top-tier capital appeal; the other carries practical experience and technological conviction from the search engine era. The external narrative often positioned 01.AI as ‘the Chinese company most resembling OpenAI,’ while Wang Xiaochuan’s tenure at Sogou demonstrated his ability to transform technology into resilient products.

During the fierce ‘Hundred-Model War’ in 2023, these two stood as flagbearers in China’s AI landscape. By 2026, however, the direction of their flags had shifted.

On May 26, Wang Xiaochuan displayed a contemplative mood in an interview. Nearing the company’s second anniversary, he expressed uncertainty about his purpose and the value he was creating. This introspection ultimately led Baichuan Intelligence to strategically contract and refocus, with a May announcement revealing that core resources would be fully invested in the vertical battlefield of healthcare.

Two days later, an internal letter marking 01.AI’s third anniversary surfaced. Li Kaifu no longer discussed AGI (Artificial General Intelligence) and Scaling Laws; instead, he emphasized applications, agents, commercialization, and how to achieve profitability with real revenue. He even declared that 2026 would see 01.AI become China’s first profitable AI 2.0 company, with an IPO planned for 2027.

MiniMax, Kimi, and DeepSeek subsequently reported financing news, as the entire Chinese large model sector collectively shifted from cloud-based technological narratives to grounded commercial realities. The idealists who once stood at the forefront now candidly admitted: The first phase of AI entrepreneurship has concluded.

01 The ‘Money Leopard’ and the ‘Family Doctor’ Exit

In January 2025, 01.AI announced it would merge most of its pre-training and AI infrastructure teams into Alibaba Cloud, abandoning the pursuit of ultra-large models.

At the time, this decision was nearly tantamount to ‘surrendering’ in an industry obsessed with burning GPUs, scaling parameters, and believing that ‘bigger is better.’ At one point, a third of 01.AI’s workstations stood idle.

A year later, this move proved visionary. With the launch of DeepSeek-R1’s inference model and collective pressure on the ‘base model tigers,’ 01.AI, having completed its strategic contraction early, gained greater maneuverability.

Throughout 2025, 01.AI secured 500 million yuan in orders and generated 250 million yuan in revenue; by May 2026, total orders had surpassed 1.5 billion yuan, with a sprint toward 2 billion yuan. Critically, nearly half of these orders represented verifiable annual recurring revenue (ARR), while annual operating costs were just over 200 million yuan—since abandoning costly pre-training, personnel expenses became the primary cost, with minimal computational investment.

In essence, the company had transformed from a capital-intensive infrastructure project requiring constant infusions of capital into a commercially viable entity capable of self-sufficiency.

Li Kaifu himself underwent a role transformation accordingly. He began frequently meeting clients in person, negotiating orders, and even studying corporate financial reports to measure which revenue metrics AI could actually enhance.

In 2025, he traveled to Kazakhstan, the Middle East, Africa, and other countries, knocking on the doors of corporate leaders. In his internal letter, he even introduced a new label: ‘Don’t call us the ‘Six Little Tigers’—call us the ‘Money Leopard.’ The meaning became clear: not participating in anyone’s ranking competition, but pursuing true commercial profitability.

If 01.AI’s transformation represents a lateral shift from technology-driven to service-driven, then Baichuan Intelligence’s change resembles a complete reconstruction.

Wang Xiaochuan admitted in interviews that in 2024, as the company approached its second anniversary, he fell into unprecedented confusion: ‘Continuing to compete in general-purpose models and follow the mainstream path is one choice. Even if we go public and look glorious, the anxiety wouldn’t decrease by half.’ It wasn’t that the company lacked money—Baichuan still had 3 billion yuan in cash reserves—but rather that he felt what he was doing wasn’t truly creating value.

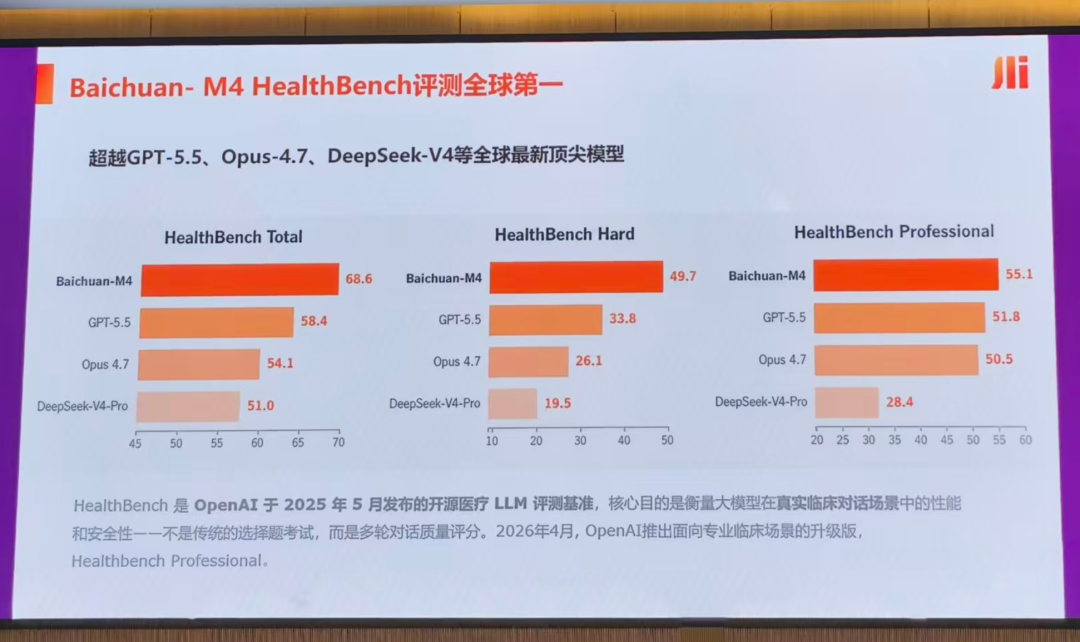

The answer ultimately landed in the medical vertical. On May 26, 2026, Baichuan Intelligence unveiled its new-generation medical large model, Baichuan-M4, and the AI family doctor product ‘Bai Xiaoyi’ at Tsinghua University.

M4 ranked first globally across three major medical benchmarks—HealthBench, HealthBench Hard, and HealthBench Professional—surpassing top general-purpose models like GPT-5.5, Opus 4.7, and DeepSeek-V4-Pro.

More importantly, leveraging its original factual perceptual reinforcement learning algorithm, M4 reduced factual hallucination rates in medical consultation scenarios to 3.3%, a new global low.

The significance of this figure in medical scenarios may be hard for the average person to fully grasp. Wang Xiaochuan presented comparative data at a forum: General-purpose models are assessed as ‘problematic’ in about 50% of medical Q&A sessions, with misdiagnosis rates generally exceeding 80%. When real patients use them independently, accuracy plummets from 94.9% to 34.5%.

Therefore, his judgment on the rigid requirements for large models in medical scenarios is very clear: low hallucination, strong evidence-based reasoning, and the ability to ask questions—none of which general-purpose large models meet.

At the product level, Bai Xiaoyi’s positioning is also quite pragmatic. It is not an aggressive product attempting to replace doctors but rather an ‘AI family doctor’ integrated into users’ WeChat ecosystem. Through corporate WeChat, it establishes independent health records for family members, captures health signals, and provides proactive interventions.

Currently, Baichuan has initiated clinical joint research with three top hospitals—Beijing Children’s Hospital, the Cancer Hospital of the Chinese Academy of Medical Sciences, and Shanghai Ruijin Hospital—with AI pediatrician consultation accuracy reaching 95%.

After gaining clarity, both Li Kaifu and Wang Xiaochuan actively chose a narrower but more certain path.

02 Three Forks in the Road, Six Survival Strategies

In early 2026, Zhipu and MiniMax went public, with both companies exceeding 100 billion yuan in market capitalization.

This marked the first differentiation among the ‘Six Little Tigers’: Zhipu, MiniMax, Yuezhi Dark Side, and Stepfun Stars remained at the general-purpose large model table as ‘holdouts,’ while 01.AI and Baichuan Intelligence chose to pivot. However, finer distinctions exist between ‘holding out’ and ‘pivoting.’

Zhipu follows a university-affiliated + full-ecosystem approach. In April 2025, it became the first among the ‘Six Little Tigers’ to sign an IPO Tutoring Agreement, listing on the Hong Kong Stock Exchange the following year as the ‘first large model stock.’

But going public doesn’t equal profitability. Although revenue grew 132% year-on-year to 724 million yuan in 2025, adjusted net losses reached approximately 3.182 billion yuan, with brokers predicting losses would likely continue for at least two more years.

Zhipu’s strategy relies on Tsinghua’s technological foundation with the GLM architecture, using an MaaS platform for API business and deploying models into localized environments for government and financial clients. Localized deployments account for over 70% of its revenue structure.

This approach is highly dependent on relationship-based sales and government/enterprise orders, offering deep moats but also clear growth ceilings.

MiniMax takes a different path—going global + C-end. Leveraging video generation and AI social products in overseas markets, MiniMax has accumulated a large user base abroad.

Bloomberg reported in July 2025 that MiniMax was planning a Hong Kong IPO with a valuation exceeding $4 billion. By early 2026, MiniMax went public with a market cap surpassing 100 billion yuan.

Its strength lies in products and traffic, but its challenge is sustained model iteration capability. Its inference model, M1, is seen as a response to DeepSeek-R1, but to continue competing with tech giants on foundational models, burning money won’t slow down.

Yuezhi Dark Side and Stepfun Stars remain relatively low-profile. According to LatePost, Yuezhi Dark Side completed a $500 million funding round in late 2025, pushing its valuation to approximately $4.3 billion, with plans to initiate an IPO in the second half of 2026.

Stepfun Stars’ founder, Jiang Daxin, recently stated publicly that he doesn’t want to abandon the mainstream growth trend and insists on foundational model R&D. However, without a clear IPO timeline or commercialization breakthrough, market patience is wearing thin.

The common thread among these four companies is their continued belief in the importance of foundational model capabilities and their search for ecological niches amid competition with tech giants.

02 An ‘Controlled Descent’ Unforeseen by Anyone

Shifting focus from China to the United States in May 2026: Around the same time Li Kaifu and Wang Xiaochuan released their internal letters and gave interviews, Anthropic announced the completion of a $65 billion Series H funding round, reaching a post-money valuation of $965 billion—surpassing OpenAI to become the world’s highest-valued AI startup.

Not long before, the four U.S. tech giants—Microsoft, Google, Amazon, and Meta—disclosed their 2026 capital expenditure plans: totaling over $725 billion, up from $410 billion a year earlier. This nearly matches 90% of Japan’s annual fiscal spending and about 40% of Germany’s fiscal budget.

This is a gap no startup can bridge, nor a structural disparity any individual effort can offset. When Microsoft alone plans to spend $190 billion on AI in 2026, the combined financing scale of all Chinese AI startups might not cover a fraction of that figure.

Against this backdrop, Chinese AI startups’ strategic options have been compressed into an extremely narrow range: continue competing head-on with U.S. giants in the general-purpose model race or retreat to the deep waters of commercial implementation, using real customer dollars to test their value.

The former means sustained massive capital consumption and long-term uncertainty; the latter means abandoning the grand narrative of ‘benchmarking OpenAI’ and accepting a more pragmatic—if less ‘glamorous’—role.

Li Kaifu and Wang Xiaochuan chose the latter. And they made this choice while still having cash on hand, a capable team, and before the market completely cooled.

Does this mean a comprehensive rout for China’s large model entrepreneurship? The answer is clearly no. Zhipu and MiniMax’s IPOs prove capital market recognition of Chinese AI assets, while Yuezhi Dark Side and Stepfun Stars’ funding sprees show that top projects can still secure massive capital support.

But even successful IPOs face the same fundamental issue: When the U.S. doubles down on compute, capital, and talent, how much competitiveness can Chinese AI companies maintain in core general-purpose models?

Stock prices ultimately return to fundamentals, and for any company heavily invested in large models, fundamentals point to commercialization capability.

This isn’t just a turning point for individual companies but the end of an era. The first half of China’s AI 2.0 entrepreneurship was a story of ideals, parameters, and benchmark-chasing.

Three years ago, the ‘Hundred-Model War’ swept the nation, VCs placed crazy bets, the ‘Six Little Tigers’ emerged, and everyone aimed to become China’s OpenAI. It was a phase filled with problem-solving excitement, where technical metrics were the only KPI and Scaling Laws the only faith.

But today’s reality offers a different answer: This isn’t the mobile internet—it’s a heavy industry war, and not every player can afford the burning costs.

In 2026, the second half begins—a story about products, orders, profits, and survival.

As for where this controlled descent will ultimately lead them, only time will tell. But one thing has become clear: A controlled descent is far more dignified than a passive crash.

- END -

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle