Zuckerberg to Compete with Nvidia's 'Protégé' in Cloud Market

06/01 2026

06/01 2026

522

522

Meta Aims to Become the 'Cloud' for Clouds

Will Meta Become the Fourth Cloud in North America?

On May 28, CNBC reported that Meta CEO Mark Zuckerberg stated that if the company overinvests in data centers and ends up with surplus computing power, Meta might enter the cloud computing market.

Zuckerberg reiterated his statement from last year's earnings call, saying, 'Almost every week, different companies approach us, either wanting us to build API services or asking if we have computing power to sell them, even willing to pay more than our procurement costs.'

As the last of North America's top four internet companies to possess hyperscaler-grade infrastructure without yet productizing it into a public cloud, Meta isn't lacking in cloud capabilities—it just hasn't sold them to others before.

So, is Meta truly planning to launch a Cloud to compete head-on with AWS, GCP, and Azure? And who would be the biggest 'victim' of Meta's entry into the cloud computing market?

01 A New Game-Changer in the AI Computing Power Market

Meta isn't a veteran in the public cloud space but has been deeply involved in cloud infrastructure for years.

As early as 2011, Facebook launched the Open Compute Project, openly sharing its server, power supply, rack, backup power system, and architectural designs from its first self-built data center in Prineville, Oregon.

According to Facebook at the time, this self-developed infrastructure improved data center energy efficiency by 38%, reduced construction costs by 24%, and achieved a PUE (Power Usage Effectiveness) close to 1.07.

This wasn't something an ordinary internet company would do, but with services like Facebook, Instagram, WhatsApp, advertising systems, recommendation systems, content moderation, and short-video distribution serving billions of users, all required massive servers, networks, and data centers. Thus, Meta had no choice but to invest heavily in data infrastructure.

In 2012, Facebook's capital expenditures were only $1.24 billion; by 2015, they had grown to $2.52 billion; in 2018, they further jumped to $13.92 billion; and by 2021, before the generative AI boom, Meta's capital expenditures had reached $19.24 billion.

These funds were repeatedly verified in earnings reports and conference calls as being invested in servers, data centers, and network infrastructure.

Thus, Meta has always had strong cloud capabilities—it just hasn't productized them into a revenue-generating public cloud business. But AI has arrived, and times have changed.

Over the past few years, North America's top four internet companies have nearly all been driven by FOMO (Fear Of Missing Out) to do the same thing: pour profits into data centers. Amazon is expanding AWS capacity and developing Trainium chips; Microsoft is providing computing power for Azure and OpenAI; Google is strengthening the foundation for Google Cloud, Gemini, and its search business.

Their CapEx investments make sense because these three companies are inherently cloud vendors, and data centers are their production assets. But Meta's uniqueness lies in the fact that it isn't a public cloud vendor yet has started spending at a cloud vendor's scale.

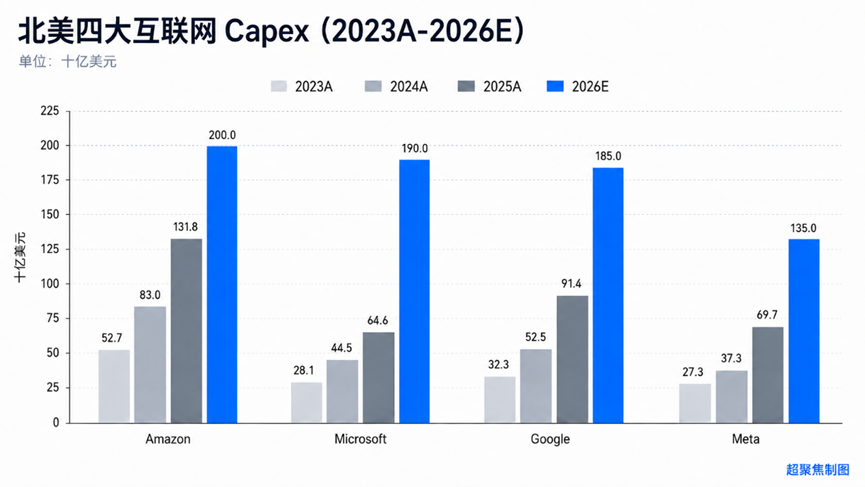

From 2023 to the present, CapEx for North America's top four internet companies has been rapidly rising. Amazon's CapEx surged from $52.7 billion to $200 billion; Google's from $32.3 billion to $185 billion; Microsoft's from $28.1 billion to $190 billion.

Meta hasn't been left out.

In 2023, Meta's CapEx was $27.3 billion; by 2025, it had reached $69.7 billion; and by 2026, it was expected to further rise to $135 billion. While still slightly lower in absolute terms than the other three, this is far from the level of a typical social advertising company merely 'buying servers'—it's a classic hyperscaler-level investment.

From an investment perspective, it's not surprising that Meta wants to enter the cloud market.

It already has data centers, server clusters, a global network, massive business scenarios, an internal scheduling system, and years of engineering experience serving billions of users. And in the latest AI wave, it has accumulated a vast amount of AI chips and computing power.

But the question remains: Will Meta's offering be a traditional AWS, Azure, or GCP-style public cloud?

Our judgment is: not likely. The reason is simple—the traditional public cloud market isn't one where you can just sit at the table by buying servers.

The true barriers for North America's top three CSPs (Cloud Service Providers) aren't just how many data centers they have but how they've absorbed enterprise customers' IT budgets, developer habits, partner ecosystems, and software vendor distribution channels over the past decade.

A new public cloud vendor, even with a lot of GPUs, would struggle to persuade a large enterprise to migrate its core systems, databases, application architectures, and operational frameworks entirely. For customers, switching clouds isn't just switching vendors—it's switching operating systems. That's why, over the past decade, hardly any new true public cloud giants have emerged globally.

Moreover, Meta doesn't need to do this. In the AI era, what's truly scarce isn't databases or Kubernetes hosting platforms—it's NVIDIA's B300s, electricity, data center capacity, and the engineering capabilities to stably schedule these resources.

This happens to be what Meta is most likely to have in surplus now.

So, even if Zuckerberg does enter the cloud market, he won't create a general-purpose public cloud for all developers, enterprises, and workloads. Instead, he'll offer a narrower, heavier, more upstream AI infrastructure cloud tailored to large customers.

This isn't the narrative of a typical public cloud but of large-customer computing power procurement.

Under the narrative of 'Meta entering the cloud market,' the truly disrupted may not be AWS, Azure, and Google Cloud but another category of players: Neoclouds that have grown rapidly by supplying GPUs, AI clusters, and computing power resale, standing between NVIDIA and AI customers.

And the most typical—and subtle—name in this category is Nvidia's 'protégé,' CoreWeave.

02 Meta vs. CoreWeave: Friends or Foes?

CoreWeave's journey is inextricably linked to AI.

It didn't start as a proper cloud vendor but as a company that grew out of cryptocurrency mining. In 2017, three investors from Wall Street founded the company under the name Atlantic Crypto to engage in mining, where GPUs were the core asset.

But good times didn't last. As the cryptocurrency cycle declined and Ethereum completed its mechanism switch in 2022, mining was no longer a profitable business, forcing CoreWeave to pivot. It began repurposing its accumulated GPU infrastructure for broader high-performance computing scenarios.

This transition wasn't easy. Going from a mining company to a cloud company required more than just a website change—it needed customers, products, a scheduling system, data centers, power, networking, and financing capabilities.

But the AI wave arrived, turning CoreWeave into a pig riding the wind.

In 2023, large model companies, AI application firms, and traditional tech giants were all vying for GPUs, while AWS, Azure, and Google Cloud's computing power quotas were far from sufficient. Suddenly, Neoclouds like CoreWeave, specializing in GPU clouds, became scarce suppliers in the market.

Its business model is straightforward: secure long-term computing power contracts with large customers, use those contracts to secure financing for purchasing cards, renting data centers, connecting to power grids, and deploying racks, and then lease out GPU clusters while collecting payments in installments. More aggressively, it uses customer contracts and existing GPU assets to support financing, then uses that financing to buy more GPUs and lease them to more customers.

This self-reinforcing business model, surprisingly, became highly sought after by giants amid the AI wave.

CoreWeave disclosed in its prospectus that Microsoft was its largest customer in 2023 and 2024, contributing 35% and 62% of its revenue, respectively.

OpenAI was also on the list. In March last year, CoreWeave signed a computing power agreement with OpenAI, which committed to paying up to approximately $11.9 billion.

Besides Microsoft and OpenAI, CoreWeave's disclosed client roster includes Meta, IBM, Mistral, Cohere, Nvidia, and others. Especially model companies like Mistral highlight CoreWeave's value—many enterprises lack the capability to build their own computing infrastructure and need rapidly deployable large-scale GPU clusters.

This is CoreWeave's most attractive aspect. It transforms NVIDIA's chips into cloud computing power for AI companies, turns GPU scarcity into contractual revenue, and converts large model companies' anxieties into growth stories that capital markets are willing to buy.

Critically, this approach has received strong support from NVIDIA.

Before its IPO, NVIDIA was already a significant shareholder in CoreWeave; when CoreWeave went public, NVIDIA participated in the IPO investment. Later, the two sides signed a deeper capacity agreement, where NVIDIA would purchase some of CoreWeave's remaining data center capacity when it wasn't fully consumed by other customers.

NVIDIA's willingness to invest real money in supporting CoreWeave is simple: CoreWeave has become the largest 'reservoir' for NVIDIA's externally sold GPUs.

When the market is good, CoreWeave can continue procuring GPUs, expanding data centers, signing large customers, and further amplifying AI computing power demand; when the market slows, it can help NVIDIA absorb some chip supply, converting hardware sales into cloud computing power consumption.

This makes CoreWeave a highly unique entity: it's both a major buyer of NVIDIA GPUs and a distribution channel in NVIDIA's AI computing power ecosystem, as well as a crucial lever for NVIDIA to extend chip demand into the cloud services market.

Reflected in its financials is soaring revenue and CapEx.

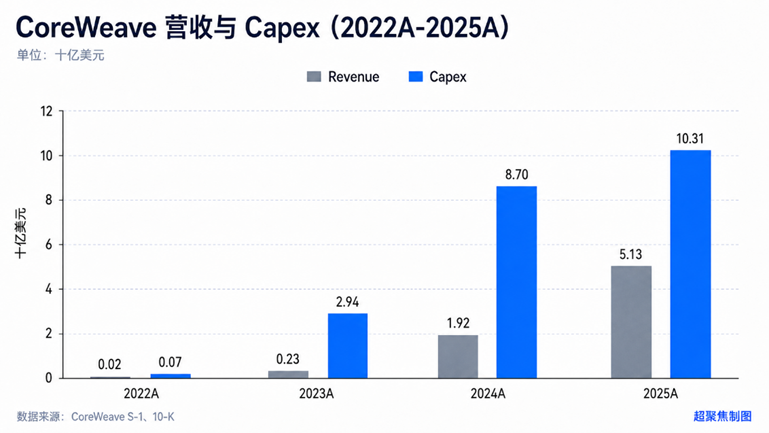

In 2022, CoreWeave's revenue was just $16 million; in 2023, it grew to $229 million; in 2024, it surged to $1.9 billion; and by 2025, revenue had reached $5.131 billion, growing over 320-fold in three years—a textbook example of explosive growth in the AI infrastructure industry.

But controversy arises here. CoreWeave isn't a light-asset software company but a heavy-asset computing power rental business. While revenue surges, capital expenditures are also expanding crazy (wildly/aggressively). In 2022, CoreWeave's spending on property and equipment was just $72.4 million; in 2023, it jumped to $2.943 billion; in 2024, it further rose to $8.702 billion; and in 2025, it reached $10.309 billion.

This means its growth is fueled by massive GPUs, data centers, debt, and long-term contracts.

Supporters see CoreWeave as having seized the window of AI computing power scarcity, using aggressive expansion to secure large customers and scale revenue; skeptics see a company highly dependent on NVIDIA GPUs, a few large customers, financing capabilities, and one premise (prerequisite/assumption): AI computing power must remain scarce.

If GPUs continue to be in short supply, CoreWeave will be a 'cloud prince' holding scarce resources; but if AI demand fades, CoreWeave's story will shift from a new cloud giant of the AI era to a flash in the pan during the computing power shortage.

This is where Meta's potential entry becomes most subtle.

Meta may not create an AWS-style public cloud or immediately compete head-on with CoreWeave for customers. But the moment it starts selling surplus AI computing power to external large customers, the market will rethink the scarcity of Neoclouds like CoreWeave.

Because CoreWeave's most valuable asset isn't just how many GPUs it has today but the market's belief that, during the era of AI computing power scarcity, it's one of the few entities that can prioritize access to cards through its 'parent-child' relationship with NVIDIA, rapidly deliver clusters, and serve large customers.

Ultimately, CoreWeave capitalizes on the dividend (dividends/gains) of AI computing power shortages. Once Meta enters the market, doubts will arise about how long such shortages can last.

This also raises the next question: If Meta truly opens its data centers to lease computing power at scale, how will the AI cloud market be reshaped?

- END -

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle