The Dividends of AI Investment Have Yet to Materialize: Replicating a Century of Electrification, Industrial Transformation Approaches a Turning Point

06/01 2026

06/01 2026

562

562

A thought-provoking phenomenon is spreading globally when reviewing corporate financial reports from the past two years.

Since the rise of generative large models in 2023, virtually no enterprise—from multinational conglomerates to small and medium-sized startups—has sat out this AI arms race. Investments in model services, dedicated technical team formation, and department-wide AI pilots have surged, with tangible financial commitments escalating wave after wave. Employees have a clear sense of this: tools for copywriting, code development, data organization, and daily communication have measurably reduced repetitive workloads, with individual productivity visibly improving.

Yet when it comes to core business metrics, everything seems to have hit pause. Revenue curves have not risen in tandem, cost structures have not seen substantive optimization, and heavily funded AI projects have failed to translate into positive gains on profit statements. Many managers are now confused: with a severe imbalance between input and output, is today’s AI truly a new productive force leading industrial transformation, or merely a conceptual frenzy that fades after the excitement?

A longer view of industrial history reveals that today’s dilemma is not unique to AI. More than a century ago, when electricity entered industrial systems, it similarly went through cycles of 'technology diffusion, efficiency perception, and delayed benefits.' The growth stalemate AI faces today is essentially the necessary growing pain of general-purpose technology implementation. The proliferation of technological tools is merely the first step; truly unlocking value requires overcoming multiple barriers related to organization, processes, and business models.

Efficiency Stuck at the Individual Level: Organizational Value Hits a Growth Deadlock

In the office environments of most companies today, AI applications are actually highly similar. Administrative staff use large models to draft official documents and organize meeting minutes, marketing teams rely on AI to batch-produce promotional materials, and technical personnel use intelligent coding tools to accelerate development. Single-point efficiency gains in functional roles have become the norm. According to joint statistics from multiple research institutions, over 80% of professionals acknowledge AI’s empowerment effect on their individual work, with routine task processing times generally shortened by more than 30%.

However, this individual-level efficiency improvement rarely translates into organizational competitiveness. This is the core contradiction of current AI commercialization: tools have changed single-point work methods but failed to shake up long-established business frameworks and management logics.

After many tech companies implemented AI coding tools internally, engineers’ code output increased significantly, yet when it came to overall product launches and business iterations, changes were minimal. The reason? Traditional processes like requirement submission, multi-level reviews, cross-departmental coordination, and manual retesting remained cumbersome, and the time saved by AI was ultimately consumed by these rigid handoff steps. Some executives from overseas travel companies have also publicly admitted that while AI can optimize the development efficiency of certain functions, it has consistently failed to establish a clear quantitative link between 'technological investment' and 'business revenue growth.'

On one hand, model vendors are seeing their customer bases and average contract values rise year after year, with industry enthusiasm continuing to climb. On the other hand, end-user companies keep increasing their investments without seeing equivalent commercial returns. This 'enthusiasm at both ends, blockage in the middle' reality has left AI in an awkward position of 'visible efficiency but elusive profits.'

At its root, current AI applications remain at a superficial, tool-supplementation stage. They simply 'add on' to existing work modes rather than 'reconstruct' industrial operation logics. It’s like factories installing electric lights in the early days—workers bid farewell to dim gas lamps, and working environments and individual efficiency improved, but factory layouts, mechanical transmission methods, and production lines all remained unchanged, so the core value of electricity could not be unleashed.

Retracing a Century of Electrification: The Three-Stage Evolution of General-Purpose Technology Implementation

In the history of technological development, general-purpose technologies like electricity, computers, and the internet that permeate entire industries have followed strikingly similar implementation paths. Nobel laureate in economics Robert Solow famously posed the 'computer paradox' in the 1980s: computers were everywhere, yet absent from productivity data. This observation applies equally well to today’s AI industry.

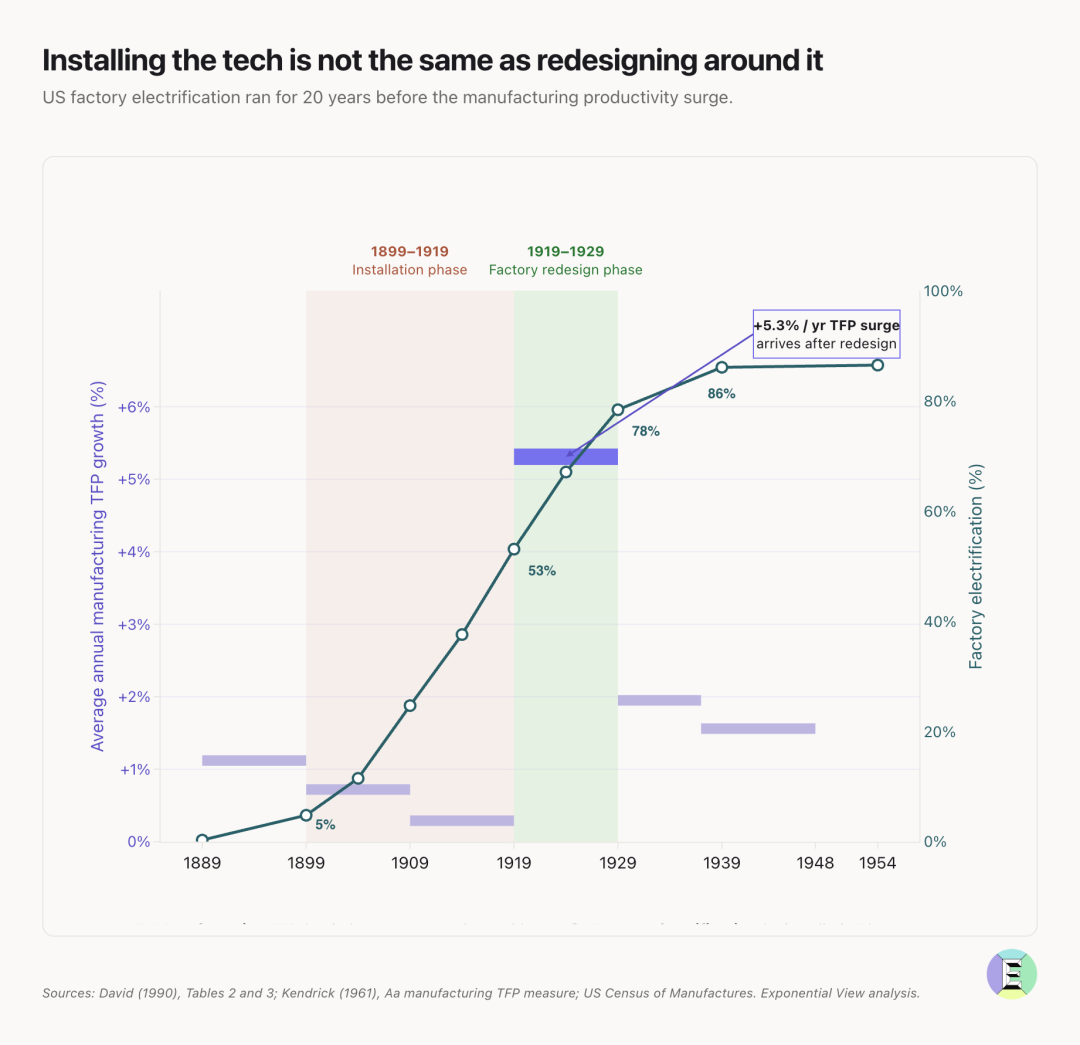

By tracing the century-long journey of electricity’s industrialization, scholars have dissected the complete lifecycle of general-purpose technology implementation—a development trajectory now fully replicating in the AI industry. The process broadly unfolds in three stages, each corresponding to a distinct form of value release.

(1) Single-Point Empowerment Stage: Tool Substitution and Localized Improvement

During electricity’s first two decades in industrial settings, its application logic was straightforward. Factories installed electric lights and small electric devices simply to replace traditional lighting and manual labor. Production equipment still relied on central steam drive shafts, workshops followed steam-era layout standards, and staff scheduling, management systems, and production processes saw no innovation.

During this phase, workers’ experiences improved and individual output rose slightly, but overall factory capacity limits and operating costs remained unchanged. Technology merely optimized 'single-point experiences' without touching the industry’s underlying rules.

This mirrors the generative AI wave around 2023, when the industry was precisely in this stage. Large models, centered on conversation, generation, and auxiliary processing capabilities, took over repetitive mental labor in workplaces. Companies procuring models and deploying tools essentially replicated what factories did when installing electric lights. Everyone enjoyed single-point efficiency gains, but few asked: How can we redesign business processes and organizational structures based on this new technology? This is the core reason behind AI’s high investment and low return.

(2) Process Adaptation Stage: Localized Transformation and Bottlenecks Emerge

As electrical technology matured, electric motors gradually replaced steam drive shafts, freeing industrial production from coal-fired boilers and sharply reducing energy costs. However, most factories retained their old equipment layouts, with all machinery arranged around traditional transmission logics—merely swapping out the 'power source.'

Energy efficiency improved, but entrenched production processes and collaboration models created new bottlenecks, slowing capacity growth. The dividends from technological upgrades were continuously diluted by outdated systems.

From 2024 to 2025, the AI industry entered this stage. Pure conversational large models were no longer mainstream; AI agents capable of task orchestration began to proliferate. AI no longer handled only fragmented work but could take on entire basic business chains: intelligent customer service completed reception, Q&A, and work order routing; AI recruitment systems handled resume screening and initial ratings; automated office robots managed report generation and data aggregation.

While application depth seemed to increase, all AI agents adapted to old processes. After AI completed preliminary work, it still entered traditional chains of manual review, cross-departmental approval, and multi-level escalation. No matter how fast intelligent tools ran, they were stalled by lengthy processes. Efficiency gains were continuously consumed, corporate investments kept rising, yet profit growth stalled—the industry’s 'revenue up but profits flat' characteristic became more pronounced.

(3) Systemic Reconstruction Stage: Rule Reshaping and Value Explosion

Electricity truly ignited industrial productivity when production systems were completely overhauled. Ford Motor Company pioneered abandoning the decades-old central drive model, equipping each production machine with its own motor and redesigning workshop layouts, staffing, and collaboration rules based on product manufacturing flows—giving birth to the modern assembly line.

When technology stopped accommodating old systems and instead became the core defining the system, productivity soared exponentially. Over the next decade, U.S. manufacturing productivity leaped forward, and electricity’s true value as a general-purpose technology was finally fully realized.

This is the direction the AI industry is now eyeing. When tool and process improvements reach their limits, only by reconstructing organizational and business logics can AI transform from a 'cost center' to a 'profit center.' And the rapidly emerging world models in the past two years are precisely the key to unlocking this stage.

From Large Models to World Models: Three Years of Iteration Bring AI to a Transformational Tipping Point

From 2023 to now, in just three years, AI has completed a full iteration from conceptual explosion to scenario deepening, with technological routes evolving from single large language models toward world models. This technological progression line has also shown the industry a path to break through current predicament (difficulties).

2023 marked the breakout year for large language models. Products like ChatGPT went viral, showing the global market the capabilities—and limits—of generative AI. Leveraging strong text understanding and content generation abilities, large models quickly penetrated basic office scenarios across industries. Competition in this phase focused on parameter scale, conversational ability, and multimodal expansion, with corporate application thinking stay at (stuck at) 'using AI to replace manual labor.'

Market sentiment was optimistic then, with many believing AI would rapidly disrupt industries. But after more than a year of implementation, the industry cooled: the ceiling on single-point efficiency gains was visible, and merely using large models for task substitution struggled to create entirely new commercial value.

By 2024, the industry shifted focus to AI agents. The technological direction moved from 'single-round interaction' to 'autonomous task execution,' with models gaining the ability to plan, execute, and orchestrate multi-step work. Application scenarios expanded from individual tools to department- and business-line-level automation systems. Major domestic tech firms and leading overseas model companies all launched agent products for enterprise services.

It was also during this stage that investment pressures on the enterprise side became apparent. Deploying, operating, and customizing agents required ongoing investment, while process bottlenecks led to lower-than-expected returns, prompting collective industry reflection on the true path of AI commercialization. People gradually realized that no matter how advanced the technology, without alignment with industrial systems, it would ultimately struggle to land.

By 2026, world models became the industry’s new core track (track), marking AI’s formal charge into the third stage. Unlike large language models focused on text and semantic understanding, world models’ core capability is perceiving the physical world, understanding real-world logics, and inferring how things develop. No longer confined to content generation in digital spaces, they can interface with real industrial scenarios to make judgments, decisions, and take actions in complex environments.

Currently, multiple top labs and research teams globally are deeply exploring this direction. The greatest breakthrough of such models is moving beyond the traditional mode of 'humans issue instructions, AI executes tasks' to possess potential for autonomous judgment and decision-making. In enterprise settings, this means AI can step outside existing process frameworks to participate in or even lead business operations—precisely meeting the core needs of the third stage of general-purpose technology implementation: 'systemic reconstruction.'

The Evolution Path and Trend Forecast for AI Commercialization Over the Next Three to Five Years

Combining the development cycles of general-purpose technologies, current technological iteration rhythms, and corporate implementation realities, the AI industry will gradually emerge from its high-investment, low-return dormant phase over the next three to five years. Commercialization will exhibit clear phased characteristics, with industry landscapes, profit models, and application forms undergoing profound transformation. Beyond the mature implementation of core world models, the AI industry will see qualitative changes across four dimensions—vertical models, edge-cloud collaboration, embodied intelligence, and engineering cost innovations—reshaping commercial logic industry-wide.

(1) 2026–2027: Process Streamlining Leads, Vertical Fields Achieve Profitability First

Over the next two years, the industry will not see across-the-board explosion but rather core trends of inventory optimization (stock optimization) + local penetration (localized breakthroughs).

More companies will abandon the mindset of 'endlessly stacking AI tools' and instead turn inward to streamline business processes. They will cut redundant approval steps, merge duplicate work nodes, simplify cross-departmental collaboration chains, first completing lightweight organizational process transformations before embedding world models and industry-specific agents. This is the most pragmatic path to unlock AI value at the current stage.

In terms of implementation, not all sectors will uniformly achieve profitability; vertical niches will be the first to close commercial loops. Industrial quality inspection, financial risk control, professional code development, offline scenario operations, and urban traffic autonomous driving—areas demanding extreme process efficiency and decision speed—will be the first beneficiaries. These scenarios have clear business logics, high standardization, and relatively low process transformation difficulty, allowing AI’s cost-reduction and efficiency-enhancement effects to be precisely quantified, with return on investment steadily improving. For example, Mushroom Autonomous Driving has operated soft-hard integrated closed-loop models combining its MogoMind physical large model + MOGOBUS autonomous buses in over 20 cities nationwide, serving over 200,000 passengers and safely traveling over 5 million kilometers. Benchmark routes like Singapore, Qin’ao cross-border medical lines, and Rizhao Wanpingkou have achieved full implementation of technology, scenarios, and services, validating the commercial logic that physical world AI scenarios can be landable, profitable, and scalable.

Meanwhile, the reasoning and deployment costs of foundational models will continue to decline. With lower technical barriers, small and medium-sized enterprises will also be able to afford customized AI services, further broadening industry application coverage. Competition among leading model vendors will shift from parameter size and conversational ability to deep cultivation (deep cultivation of) industry solutions and alignment with process reconstruction needs. Collaborations between general-purpose model vendors and vertical industry service providers will become the dominant form.

(2) 2028–2029: Organizational Structures Reshape, Industry Dividends Fully Released

Once process transformations become widespread consensus across industries, AI will deeply integrate into the underlying logics of corporate operations, triggering large-scale organizational innovation.

The traditional pyramid-style hierarchical management structure will gradually loosen under the impact of AI. A large amount of repetitive, audit-based, and basic decision-making work will be autonomously completed by AI, leading to a transformation in the roles of middle-level functional positions. Instead of forcing AI to fit into outdated structures, companies will rebuild collaboration models around AI capabilities, with networked and flattened organizations becoming the mainstream.

At this stage, AI will completely shed its label as a “cost center” and transform into the core source of productivity for enterprises. Globally, the average return on investment in AI projects will achieve leapfrog growth. Leading companies formed through technological barriers and industry resources will emerge as industry giants in core sectors such as finance, industry, healthcare, government and enterprise services, and intelligent transportation.

There will also be significant differentiation in business models: mass AI services for consumer-end (C-end) will gradually move toward free or low-barrier models, monetizing through traffic and value-added services; enterprise-level services for the business-end (B-end) will form a diversified fee structure combining “basic subscriptions + customized solutions + performance-based revenue sharing,” marking the maturation of commercial monetization models.

(III) 2030 and Beyond: World Models Mature, AI Becomes Social Infrastructure

Five years later, world model technology will gradually become generalized and inclusive, achieving deep integration between the digital and physical worlds. AI will no longer be a mere “tool” or “system” but will become a fundamental support for societal operations, akin to electricity, water, and the Internet.

In the workplace, AI agents will become a normalized collaborative role, with over half of all mental work forming a fixed “human-machine collaboration” model. Physical industries such as manufacturing, logistics, public services, and intelligent transportation will achieve end-to-end intelligent operations relying on world models. Humanoid robots and offline intelligent terminals, combined with world models, will enter more production and living scenarios.

At the industrial ecosystem level, a complete industrial chain will stabilize. From foundational model research and development and computational support at the bottom layer, to industry-specific model customization and agent development in the middle layer, and finally to scenario implementation and operational services at the top layer, each segment will form a stable profit model. The global AI industry will reach a new scale, with technological innovation and commercial operations forming a virtuous cycle.

(IV) Four Emerging Core Trends Reshaping the Long-Term Commercialization Landscape of AI

Beyond the iterative implementation of core world models, commercial breakthroughs in the AI industry over the next three years will concentrate on four key segments, thoroughly breaking the current industry dilemma of “high investment, low returns.”

1. Vertical Specialized Models Replace General-Purpose Large Models as the Core Profit Driver

The parameter race and conversational capability competitions among general-purpose large models will descend into a homogeneous red ocean, with profit margins continuously shrinking, ultimately reducing them to inclusive infrastructure for the industry. In contrast, vertical specialized models deeply integrated with industry-specific physical rules, business logic, and scenario data will become the core profit carriers. These models, requiring no ultra-large parameters and primarily featuring small to medium parameters (7B-70B), are cost-effective, highly adaptable, and deployable, precisely addressing real industry pain points.

2. Edge-Cloud Collaborative Architecture Becomes Ubiquitous, Shifting AI from Centralized Cloud to Distributed Intelligence

Traditional pure cloud-based AI deployment suffers from high latency, high costs, offline failure, and significant data security risks, failing to meet the rigid demands of physical industries. The industry will fully adopt a distributed architecture combining “real-time decision-making at the edge + regional collaboration at the side + global iteration in the cloud.” Edge devices handle millisecond-level local decisions, side systems manage regional data fusion and scheduling, while the cloud undertakes global training, model optimization, and data closed loop (closed-loop) tasks.

3. Embodied AI Lands, Breaking Down the Final Barrier Between Digital AI and Physical Industries

While world models address AI’s ability to “understand the world,” embodied AI achieves the leap to “physically transform the world,” representing the largest incremental track for AI commercialization. AI will fully transcend pure software and text-based virtual forms, deeply integrating with hardware such as autonomous vehicles, industrial robotic arms, service robots, and intelligent terminals to achieve end-to-end autonomous operation in perception, decision-making, and execution. From 2027-2029, large-scale commercialization of L4 autonomous driving, fully unmanned industrial processes, and intelligent urban operations will materialize one by one. Full-stack capabilities combining models, hardware, scenarios, and data will replace parameters and algorithms as the core competitive barriers of the industry.

4. AI Engineering Cost Revolution Ushers in an Era of Inclusive Profitability

One of the current core bottlenecks in AI commercialization is the high costs of training, inference, deployment, and talent. Over the next three years, with the maturation of engineering technologies such as model distillation, sparsification, quantization compression, dedicated ASIC chips, and computational pooling, overall AI inference costs will drop by another 90%, significantly lowering deployment barriers. Small and medium-sized enterprises will no longer need to build in-house AI teams or purchase expensive computational power; instead, they can directly subscribe to industry models and agent services on-demand, paying based on results. This drastic cost reduction will fully activate the lower-tier market, transforming AI from a “premium technology” exclusive to large firms into an “inclusive productivity” common across industries, comprehensively raising the commercialization ceiling.

Enterprise Strategies: Moving Beyond Tool-Centric Thinking to Embrace Systemic Transformation

Faced with the current dilemma of “high AI investment with low returns,” many companies continue down the old path: constantly procuring new models, hiring technical staff, and launching more pilot tools. This approach remains stuck in the mindset of “installing electric lights”—no matter how much is invested, it fails to address the core of industrial transformation.

Drawing on the experience of the century-long electrical revolution and current AI technological trends, to truly capture this wave of technological dividends, companies must shift their mindset and replan their AI strategies across three dimensions.

First, abandon point-based efficiency thinking and anchor on business reconstruction goals. Instead of focusing on “how much time AI can save employees,” think holistically about the business: which links can be entirely reconstructed with new technologies, and which redundant steps can be directly eliminated. The upper limit of AI’s value is determined not by its tool capabilities but by the business framework.

Second, prioritize process transformation over technological implementation. Begin by mapping out the full workflow of core businesses, streamlining unnecessary hierarchies and steps, and building new processes suited for intelligent operations. Having technology serve the new system, rather than forcibly adapting AI to a convoluted old system, is the key to reducing internal friction and unlocking efficiency.

Finally, allocate resources toward world models and industry-specific agents. With homogeneous competition among general-purpose large models reaching fever pitch, merely competing on technical parameters holds little meaning. Combining their own industry attributes, companies should deeply cultivate world models and industry agents capable of understanding scenario logic and making autonomous decisions. Physical industries such as transportation, manufacturing, and energy must adhere to implementation paths centered on “physical world models + edge-side intelligence + large-scale real-world data.”

Throughout industrial development history, every widespread adoption of a general-purpose technology has required a prolonged dormant period. It took decades for electricity to move from factories into assembly lines; similarly, the journey from the birth of computers to the universal adoption of the Internet spanned generations. While technology itself spreads rapidly, the iteration of human society, industrial organizations, and commercial rules always requires time for alignment.

Today, AI is in the latter half of its dormant phase. We have moved beyond the initial stage of relying solely on tools for efficiency gains and experienced the growth bottlenecks brought by process adaptation. Currently, technological innovations in world models, embodied AI, and edge-cloud collaboration, combined with industrial process reforms, are jointly propelling the industry toward a new stage.

In the short term, AI profit realization will not happen overnight, and growing pains will persist for some time. However, one certainty remains: the broad direction of this technological transformation will not change. For companies, the priority now is not to question the value of technology or blindly double down but to focus on completing internal process and organizational reforms to keep pace with technological iteration.

The moment technology and industrial systems achieve deep integration, the accumulated productivity dividends of AI will erupt. Those who complete their strategic layout (layout) early and dare to embrace change will ultimately seize the initiative in the new industrial landscape. The AI wave that began in 2023 has only just lifted its curtain.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle