From Selling Cloud Services to Selling Tokens: Operators Fully Join the AI Battlefield

06/01 2026

06/01 2026

511

511

Elon Musk once predicted that in the future, Tokens would be consumed like data traffic.

Today, this statement is not just an imagination of how AI will be used but an early description of a new industrial measurement logic. When we shift our focus from the operators' 'self-reconstruction' to the broader market, a new industrial landscape driven by Tokens is unfolding.

Author | Dou Dou

Editor | Pi Ye

Produced by | Industry Insight

AI cloud is approaching a milestone turning point.

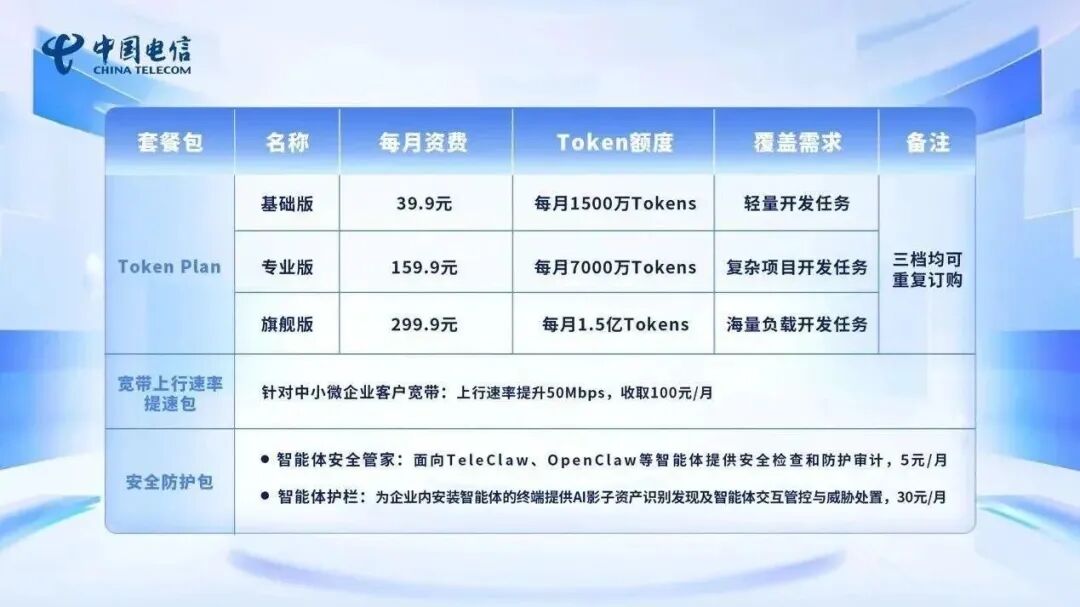

On May 17, China Telecom announced the trial commercial launch of Token packages nationwide. For individuals and families, the lowest package starts at 9.9 yuan/month, including 10 million word tokens; for developers and small, medium, and micro enterprises, three tiers are set at 39.9 yuan, 159.9 yuan, and 299.9 yuan, corresponding to 15 million to 150 million word tokens per month.

This means that Tokens are taking over from voice, text messages, and data traffic as the fourth fundamental communication service measurement unit for the three major operators. From 'selling data traffic' to 'selling Tokens,' operators are striving to reshape themselves into the 'State Grid' of the AI era.

Behind this transformation lies the operators' second identity reconstruction in three decades. The first leap occurred during the cloud computing era, where operators leveraged their 'controllable, secure, and national team' status to enter the top tier of government and enterprise cloud services. The second leap is happening now, as they are reshaping themselves from 'government and enterprise cloud providers' into 'total integrators of AI access services.'

As the curtain rises, a series of ultimate questions about the industry's fate arise: What game are the operators playing? What is the underlying logic driving their self-revolution? What changes are needed to transition from 'selling cloud services' to 'selling Tokens'? How should these changes be implemented? Where will this role reconstruction, rooted in three decades of foundation, ultimately lead the operators?

I. Operators Collectively Renovate the 'AI Gateway'

Over the past three decades, operators' trump card has been integrating communication resources. Facing the AI era, this logic is upgrading to integrating AI resources and selling Tokens. To truly implement complex AI capabilities, traditional communication gateways can no longer suffice; they must be renovated into a new entry point through Token packages.

It is evident that all three operators have entered the fray, reorganizing their AI service entry points around Token packages.

China Telecom bundles Tokens, connectivity, and security together, offering personal and family packages starting at 9.9 yuan/month, while setting independent tiers for developers and small and medium-sized enterprises. User entry points are no longer limited to traditional cloud platforms; they can be accessed through the Tianyi Cloud official website, China Telecom App, or the Tianyi AI Cloud Computer with built-in intelligent agents.

China Mobile is advancing simultaneously at the local company and group levels. Beijing Mobile offers a 5.99 yuan per-use package and a 24.99 yuan/month package for 10 million Tokens; Shanghai Mobile, in collaboration with Tencent, launched the WorkBuddy intelligent agent workstation, where 1 yuan can buy 400,000 Tokens, and payment can be made directly through phone bills. At the group level, China Mobile released MoMA, which accesses over 300 models and reduces the unit Token cost by about 30% through intelligent routing, caching, and Token compression.

China Unicom further upgrades its Token Plan into a combination of 'MaaS + tools + computing power.' Unicom Cloud and Yuanjing provide access to models like DeepSeek and MiniMax for individual users, while the team version adopts Credits flexible billing, covering research and development teams, government and enterprise office solutions, and industry-specific applications.

What is the reason for this massive migration from 'connectivity resources' to 'computing power and model resources'?

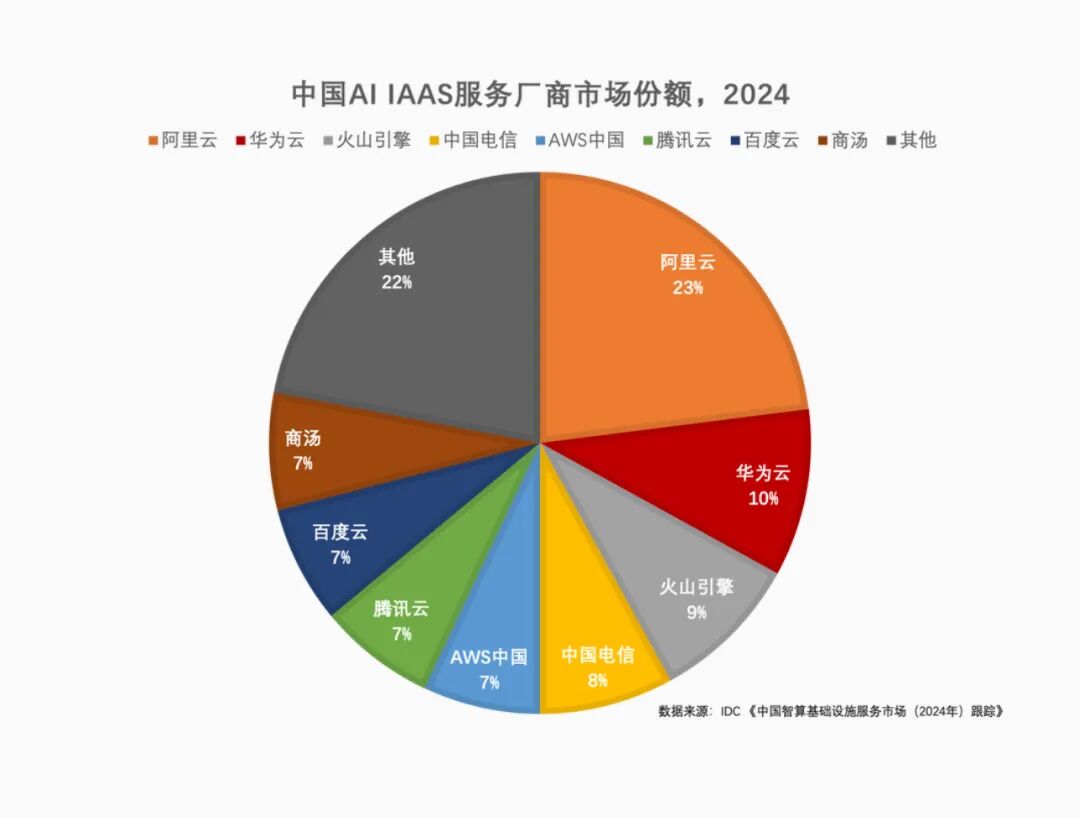

First, consider market positioning. IDC's 2024 China AI IaaS market share shows Alibaba Cloud at 23%, Huawei Cloud at 10%, Volcano Engine at 9%, China Telecom at 8%, and Tencent, Baidu, AWS China, and SenseTime all at 7%. Although operators have entered the Top 5, they still lag significantly behind the leading tier.

According to Omdia's 'China AI Cloud Market, 1H25' data, by the first half of 2025, market share will further concentrate among top cloud providers. Alibaba Cloud will hold 35.8%, Volcano Engine 14.8%, Huawei Cloud 13.1%, Tencent Cloud 7%, and Baidu Intelligent Cloud 6.1%. Operators will have dropped out of the Top 5. This means that if operators fail to develop capabilities exclusive to them, their share in the AI cloud market will continue to be diluted.

More critically, internet giants have already taken the lead in packaging model services into user-friendly and easily purchasable packages. For example, Alibaba Cloud's BaiLian offers a Token Plan, using Credits to uniformly offset consumption across multiple models; Tencent Cloud's Large Model Token Plan provides four tiers—Lite, Standard, Pro, and Max—with 39 yuan/month buying 35 million Tokens; Baidu Qianfan's Coding Plan offers two subscription tiers at 40 yuan and 200 yuan.

This indicates that Token packaging is not just a billing method in the developer market but is becoming a universal packaging for AI services entering the mass market.

Beyond external pressures, operators themselves have reached a point where they must shift gears.

Data shows that in 2025, China Mobile's revenue was 1.0502 trillion yuan, up 0.9% year-on-year; China Telecom's operating revenue was 529.6 billion yuan, roughly flat; China Unicom's revenue was 392.2 billion yuan, up 0.7% year-on-year. The three operators' fundamental position remains vast, but growth elasticity is diminishing.

Meanwhile, computing power and intelligent services are emerging as new growth drivers. China Mobile's intelligent computing service revenue grew by 279%, China Unicom's AI business revenue increased by over 140%, and all three operators raised their computing power investment to over 30% by 2026. Growth is shifting from traditional communication services to computing power, models, and intelligent applications.

The problem is that AI cloud competition is no longer just about data centers, dedicated lines, and GPUs. It hinges on model capabilities, computing power scheduling, inference costs, developer ecosystems, industry applications, and service response speed. If operators remain stuck at the 'resource-selling' stage, they will face simultaneous pressure from internet cloud providers, model companies, and industry software vendors.

Therefore, operators must build a new gateway that supports large models at the top, mobilizes computing power resources at the bottom, and connects users, developers, and enterprises in the middle through Token packages.

II. From Cloud to AI: What Are Operators Changing?

So, what does the blueprint for this 'new gateway' look like? For operators, what complex industrial elements must be integrated to transition from 'selling data traffic' to 'selling Tokens'?

The answer depends on changes in customer demand.

In the past, when enterprises adopted cloud services, they bought servers, storage, and networks from operators. Today, when enterprises implement AI, they seek not just an isolated model interface but a complete system covering model invocation, computing power scheduling, application access, and unified billing. This compels operators to upgrade from 'selling cloud shelves' to 'becoming total integrators of AI entry points.'

First, models must be integrated. Multiple general-purpose, industry-specific, self-developed, and third-party models must be connected to a unified entry point, allowing enterprises to invoke, switch, and manage models through a single API or platform.

Second, computing power must be integrated. AI computing power is more complex than cloud computing resources, involving intelligent computing centers, domestic chips, GPU resources, heterogeneous scheduling, cross-regional networks, and inference cost control. Operators must transform computing power scattered across regions, chips, and platforms into a schedulable, billable, and guaranteed computing power network.

Third, applications and intelligent agents must be integrated. Enterprises adopt AI not just to invoke models but to transform business processes. Customer service, marketing, research and development, production, operations, approvals, risk control, and knowledge management are the true endpoints. Models are merely underlying capabilities; only when encapsulated into industry-specific intelligent agents, toolchains, and Skills packages can they enter enterprises' daily systems. Therefore, operators must not only provide model interfaces but also create application foundations for government, state-owned enterprises, energy, transportation, finance, healthcare, and education sectors, helping enterprises solve the problem of 'how AI truly integrates into business.'

Fourth, billing and operations must be integrated, which is where Token packages truly add value.

Different models, computing power levels, and intelligent agent tasks are difficult to place within a single pricing system. A question-and-answer session, code generation, document processing, and intelligent agent execution all consume different models and computing power. For enterprises, if each item is purchased, settled, and managed separately, usage thresholds become high. Operators must simplify complex resources into straightforward packages. Users do not need to understand the intricate chains behind each invocation; they only need to know how much quota they have purchased, which scenarios it can be used in, and how billing works beyond the quota, thereby helping enterprises solve the problem of 'whether AI can be scaled operationally.'

In summary, this 'renovation' is essentially a way for operators to reconstruct AI services: using models to open capability entry points, computing power to support underlying supply, intelligent agents to undertake (chengjie, meaning 'take on') business scenarios, packages to complete commercial loops, and security compliance to uphold trust from government and enterprise clients.

III. Operators Positioned as the 'Scaffolding' of the AI Era

Deconstructing the top-level logic is just the first step. When ideals meet reality, more industry-specific implementation challenges arise: How exactly should operators handle the vast ecosystem of computing power, models, and applications?

Operators are building an end-to-end 'five-layer scaffolding' encompassing the model layer, computing power layer, application layer, billing layer, and security compliance layer.

Specifically, the core of the model layer is controlling entry points.

Operators understand that relying solely on self-developed models makes it difficult to fully catch up with leading internet giants, nor is it necessary. Therefore, they adopt a strategy of 'self-developed foundation + external model aggregation.' China Telecom's Xingchen, China Mobile's Jiutian, and China Unicom's Yuanjing stabilize the basic disk of industry adaptation and autonomy; meanwhile, mainstream models like DeepSeek, Tencent Hunyuan, Alibaba Tongyi Qianwen, ByteDance Doubao, Zhipu GLM, and Kimi are integrated into a unified platform.

Take China Mobile's MoMA as an example: 'model federation + intelligent routing' allows users to remain unaware of which model is invoked behind the scenes, as the system automatically distributes tasks based on cost and effectiveness. Essentially, all models are distributed through the operator's entry point.

For models to circulate, underlying computing power support is essential. The computing power layer is also where operators have the greatest opportunity to build moats.

Operators control East-to-West computing nodes, backbone networks, dedicated lines, government and enterprise networks, and long-term capabilities in building computing power networks—capabilities that cannot be replicated shortly. This gives them a significant advantage in unified scheduling across hubs and chip models. Operators are connecting heterogeneous resources from domestic chips, existing NVIDIA equipment, and multiple computing power enterprises into a network, forming a formidable barrier. Examples include Tianyi Cloud's 'One Cloud' and China Mobile's 'Xingluo' computing network brain.

Above computing power lie applications and intelligent agents.

To enable customer service, office, marketing, research and development, operations, approvals, and risk control processes to run smoothly, operators are standardizing intelligent agent frameworks like MobileClaw, TeleClaw, and Uniclaw, paired with industry-specific Skills packages. This creates an 'AI app store' for state-owned enterprises and government clients, allowing AI capabilities to be rapidly assembled into existing office and production systems, helping enterprises solve the problem of 'how AI enters business.'

For applications to circulate and for high-frequency, complex invocations to be accounted for clearly, operators are leveraging key innovations from their three decades of billing (Billing) and CRM systems. They have introduced mechanisms like 'Tianyi Token Coins,' abstracting consumption across different models and computing power into unified billing units, seamlessly transitioning the past 'data package' logic to a 'Token package' logic. This is the underlying reason why Token packages can rapidly roll out nationwide overnight.

The final step in the commercial loop is trust.

As 'national teams,' operators naturally dominate the computing power pools of state-owned enterprises. Through layered reinforcement of classified protection, indigenous innovation, and trusted data spaces, they have built a 'government and enterprise reserved track' that internet vendors find difficult to penetrate.

Today, based on this 'scaffolding,' operators have broadly laid out their capabilities.

For example, by the end of 2025, China Telecom had 43 EFLOPS of self-owned intelligent computing power, precipitate (chenjian, meaning 'accumulated') over 110 industry large models and 350 intelligent agents, serving 37,000 clients with an AI penetration rate of 85% among central enterprises; China Mobile's intelligent computing scale reached 61.3 EFLOPS, its MoMA platform aggregated over 300 models, and reduced unit Token costs by about 30%; China Unicom is also advancing toward a 45 EFLOPS intelligent computing goal, with its AI revenue year-on-year growth (tongbi zengzhang, meaning 'year-on-year growth') as high as 147%.

IV. Operators Fully Commit to AI in the Token Economy

Elon Musk once predicted that in the future, Tokens would be consumed like data traffic.

Today, this statement is not just an imagination of how AI will be used but an early description of a new industrial measurement logic. When we shift our focus from the operators' 'self-reconstruction' to the broader market, a new industrial landscape driven by Tokens is unfolding.

Over the past two years, the main theme of the AI industry has been model competition. Whoever has larger parameters, stronger inference, and more complete multimodal capabilities is more likely to gain market attention. However, as AI enters the industrial implementation stage, the focus of competition is shifting. What enterprises truly care about is no longer just how intelligent a model is but whether it can integrate into existing systems, process business stably, account for costs clearly, and be audited and managed.

The challenge lies in transforming models into daily-usable, continuously purchasable, and risk-controllable production capabilities for enterprises. Low-threshold, purchasable, and quantifiable intelligent capabilities will become a rigid demand (gangxing xuqiu, meaning 'rigid demand').

The door renovated by the operators happens to integrate models, computing power, networks, security, and billing into a single entry point, enabling enterprises to procure intelligent capabilities just like purchasing communication services or cloud resources, without the need to reunderstand a complex AI technology stack. This is the true industrial value of the Token package. On the surface, it appears to be a credit limit, but behind the scenes, it could become the unit of measurement, settlement, and operation for AI services.

It is foreseeable that today's Token resembles a general-purpose package, but in the future, it is likely to further differentiate into an office package for employee efficiency, a developer package for R&D teams, an exclusive model package for central state-owned enterprises and government scenarios, and industry-specific intelligent agent packages for finance, energy, transportation, healthcare, and education.

However, although the prospect of 'buying Tokens as easily as topping up phone credit' is appealing, there is still a long way to go before it truly becomes a reality. Operators still face several tough challenges, such as whether the model's performance is good enough, whether intelligent agents can stably complete tasks, whether inference costs can continue to decline, whether customers are willing to pay for long-term use, and whether these investments can ultimately translate into substantial revenue.

Therefore, the key to success for operators does not lie in who is the first to launch a Token package or how low the package price is, but rather in whether they can turn 'AI access' into a carrier-grade service that is measurable, billable, operable, and guaranteed. If this step is achieved, operators will no longer be merely sellers of cloud resources, dedicated lines, or computing power pools in the AI industry but will become trusted infrastructure providers in the process of industrial AI implementation.

By then, for enterprises, AI may no longer be a new technology that requires repeated deliberation but will become a factor of production that can be accessed, billed, and continuously used, just like water, electricity, and networks.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle