10 Trillion! China is Becoming an AI Infrastructure Powerhouse

06/02 2026

06/02 2026

486

486

Please note, China is about to make its move.

By Hua Shang Tao Lue, Da Nan

In 2026, the global AI competition will reach a fever pitch, with massive amounts of capital pouring in on an unprecedented scale.

The four U.S. tech giants—Microsoft, Google, Amazon, and Meta—are expected to invest approximately $650 billion.

China's cumulative investment is projected to reach RMB 10 trillion by 2030.

Europe and Japan have announced investment plans of €200 billion and ¥1 trillion, respectively.

Where is all this money going?

Building power grids, competing for chips, snapping up optical modules, and stocking up on transformers are just the basics.

A deeper and more decisive area in the AI competition is becoming the top priority in the strategic layout (Chinese for "layout") of countries worldwide.

That area is AI infrastructure.

【01 The Battleground】

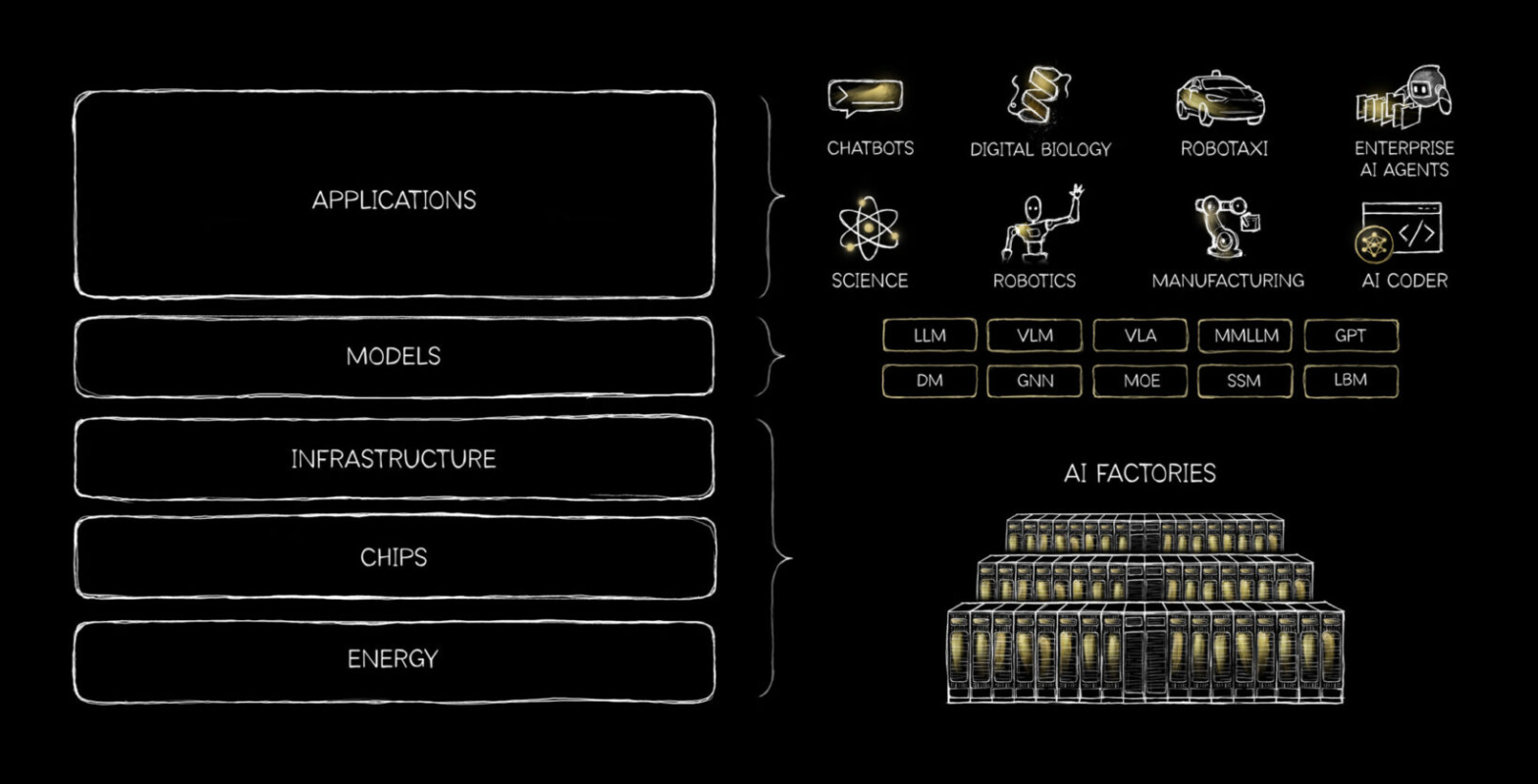

On March 10, NVIDIA CEO Jensen Huang published a lengthy blog post titled "AI is a Five-Layer Cake" in his personal capacity. It was his first in-depth article in five years.

In his view, AI is far more than just ChatGPT or a search product—it is a complete system.

He divides this system into five layers: energy, chips, infrastructure, models, and applications. Like layers of a cake, each layer supports the one above it.

This framework is equally suitable for analyzing the global AI competition landscape.

▲ Jensen Huang's "Five-Layer Cake" framework for AI. Source: NVIDIA's official website

The energy layer is the foundation, with electricity at its core. In the current energy landscape, China not only has the largest total capacity—more than double that of the United States—but also leads the world in major power generation sectors, including thermal, wind, hydro, solar, and nuclear power.

In contrast, the United States generates less than half of China's electricity and faces structural challenges such as aging grid infrastructure and fragmented eastern and western grid systems.

As netizens sum it up: "At the end of AI is computing power, at the end of computing power is electricity, and at the end of electricity is China." In the energy layer, China is undoubtedly the clear winner.

Above the energy layer is the chip layer. The United States leads in advanced chip manufacturing, but China is accelerating its catch-up.

There was a widespread belief that training top-tier large models must rely on the most advanced chips, as if being constrained in chips meant an inability to develop top-tier models.

However, DeepSeek broke through this limitation. Through algorithmic innovations in architectures like Mixture of Experts (MoE) and Multi-Head Latent Attention (MLA), it achieved breakthrough progress in large model performance under limited computing power conditions.

As large models overcome chip limitations, domestic chips continue to make strides. Huawei's Tao (τ) Law has charted a unique path for China's semiconductor industry, projecting that by 2031, its high-end chip transistor density will reach parity with the 1.4nm process. Domestic chip players like Hygon, Cambrian, and Kunlunxin are also achieving breakthroughs in their respective fields.

Correspondingly, NVIDIA's chips have gone from the U.S. refusing to sell them to China not buying them. U.S. Secretary of Commerce Lutnick, responding to inquiries during a congressional hearing on April 22 about NVIDIA's H200 chip sales to China, said: "So far, China hasn't bought a single chip because they want to focus their investments on developing their domestic industry."

Even Jensen Huang could only say with frustration: "We've become a company restricted by both sides." He emphasized: "Remember, semiconductors are ultimately manufacturing. Anyone who thinks China can't do it is seriously mistaken."

At the AI large model layer, data from July 2025 shows that of the approximately 3,755 AI large models operating globally, 1,509 are from China, ranking first in the world. China also ranks first in downloads of open-source large models, a key metric.

On April 13, Stanford University's HAI Laboratory released its 2026 AI Index Report, showing that the performance gap between Chinese and U.S. large models has narrowed to 39 points, down from over 300 points two years ago.

Less than two weeks after the report's release, DeepSeek-V4 Preview was announced as open-source. The V4-Pro version matched world-class closed-source large models in mathematics, STEM, and competitive coding, surpassing all publicly available open-source models. Notably, V4 prioritized compatibility with domestic chips like Huawei's, completing a bottom-up migration from NVIDIA's CUDA ecosystem to Huawei's CANN architecture, achieving an independent closed loop between domestic large models and domestic chips.

In chips and large models, the U.S. leads, but China is catching up rapidly. At the top application layer, China's advantages are significant.

By the end of last year, China's domestic generative AI user base surpassed 600 million, with a penetration rate of 42.8%. Among young people aged 18-24, penetration exceeded 91%. In contrast, the U.S. AI penetration rate is 28.3%, and the EU's is 32.7%, both lower than China's.

Having experienced technological backwardness, the Chinese are more afraid of falling behind and thus more open and proactive in embracing new technologies.

China is a massive single market of 1.4 billion people, with extremely high AI acceptance and exceptionally diverse application scenarios.

In March of this year, Sora, the U.S. AI video generation platform that once "made Hollywood tremble," shut down due to an unsustainable business model. Meanwhile, Chinese video creators successfully monetized AI short dramas produced with Seedance. A Hangzhou-based company, Ruiqi Software, earned RMB 1 billion annually from an AI app that helps foreigners identify flowers.

An MIT report directly pointed out that despite U.S. companies investing over $30-40 billion in generative AI, a staggering 95% of pilot projects fail to transition to actual production.

While the technological sophistication of AI is crucial, the ability to be the first to apply new technologies at scale is equally important.

Overall, China has clear leading advantages in the energy and application layers. In the chip layer, China lags behind the U.S. but is striving to catch up. In the model layer, China and the U.S. each have their strengths.

The focus of the next phase of competition is clear: the third layer, AI infrastructure, will be the key to victory.

【02 Global Scramble】

Whoever becomes the "AI infrastructure powerhouse" will gain the upper hand.

However, building computing centers is no easy feat. It requires integrating key equipment like chips, optical modules, and servers while also involving civil engineering, power supply, cooling, and other engineering aspects.

It is a complex systems engineering project where a single shortcoming can lead to overall failure.

Currently, countries are pulling out all the stops to tackle this challenge.

The United States is the biggest spender on AI infrastructure.

In 2026 alone, Meta plans to invest $135 billion, Microsoft $105 billion, Google $185 billion, and Amazon $200 billion, with the four giants' total investment increasing by 70% compared to last year.

The giants also know that spending money alone is not enough. Thus, U.S. companies are forming alliances to combine their strengths and compensate for each other's weaknesses.

OpenAI and Oracle launched the "Stargate" initiative, investing $500 billion to expand AI infrastructure. Microsoft formed an alliance with BlackRock and xAI. NVIDIA invested $1 billion in Nokia to transform millions of global base stations into computing nodes...

However, sometimes it is the small, overlooked components that hold up the entire progress.

In 2026, nearly half of the planned new data center projects in the United States were delayed or canceled due to shortages of key components, especially power equipment like transformers.

Andrew Licence, head of Crusoe Energy and Infrastructure, compared it to "a crazy (Chinese for 'crazy') jigsaw puzzle where any delay in the supply chain means the entire project cannot be delivered."

To address this dilemma, the White House proposed over 90 policies and even established a cross-departmental AI infrastructure working group. Some joked that this was an attempt to emulate China's National Development and Reform Commission's industrial policies. To keep up, the U.S. was willing to try anything.

Although Europe ambitiously aims to leverage up to €200 billion in investments by 2030, the reality is stark.

In AI hardware, Europe heavily relies on external supplies, holding only a 10% global share in semiconductors. Even Italy's top supercomputer, Colosseum, relies on NVIDIA for its core architecture.

French President Macron admitted that Europe's AI infrastructure is highly dependent on the U.S. and China and urgently needs to build autonomous industrial capabilities.

What slows Europe down further are the significant differences in regulations and interests among countries. The EU's AI Act took three years to barely reach a consensus—a delay that, in the fast-paced AI industry, means missing the boat.

In Asia, Japan plans to invest ¥387.3 billion (about $2.4 billion) in AI infrastructure this year, while South Korea has set an AI-specific budget of ₩10.1 trillion (about $7 billion).

Compared to the hundreds of billions in investments by China and the U.S., this seems inadequate. Moreover, AI training requires massive amounts of data as fuel, and Japan and South Korea are naturally limited in data scale.

Japan and South Korea are well aware of this and choose to avoid direct competition with China and the U.S., instead taking alternative paths.

Japan plans to abandon the race for general-purpose large models and focus on "physical AI." Domestic giants like SoftBank, NEC, and Honda are joining forces to deeply integrate AI with physical industries like automotive and robotics.

South Korea has also selected five consortia, including NAVER Cloud, Upstage, and SK Telecom, to launch its "Sovereign AI" strategy, aiming to establish an AI system exclusive to South Korea.

Globally, the core arena of AI competition remains between China and the United States.

【03 China as the AI Infrastructure Powerhouse】

By re-examining the challenges of AI infrastructure, China's advantages become clear.

One of them is the ability to coordinate power and computing resources at the national level.

Four years ago, China launched a highly strategic national project: "East Data, West Computing."

This initiative, comparable to the "South-to-North Water Diversion" and "West-to-East Electricity Transmission" projects, aims to seamlessly connect the booming computing demand in the east with the abundant green power in the west. Today, world-class computing hubs are hidden in the mountains of Guizhou, the deserts of Ningxia, and the sands of Gansu.

More ingeniously, computing power and electricity can work in tandem.

During peak electricity usage in the daytime, the system suspends non-urgent AI training tasks to reduce grid pressure. At night, when wind power is abundant, computing power runs at full speed to consume excess green electricity. Meanwhile, AI models can help the grid with intelligent scheduling.

Electricity supports computing power, and computing power optimizes electricity, forming a closed loop that achieves a golden balance between cost and efficiency.

Currently, China's total computing power ranks second globally, while its number of supercomputers tops the world. Moreover, its total computing power is growing at an annual rate of 30%, meaning it can double in less than three years.

Supporting this growth is the ability to coordinate resources "nationwide as one."

Focusing on data centers themselves, China possesses full-chain independent manufacturing capabilities, from the smallest screws to the largest server rooms—another significant advantage.

In the AI chip sector, domestic players like Huawei's Ascend, Hygon Information, and Cambrian are rising rapidly. Last year, domestic chips increased their market share in China to 41%, with over 1.65 million units shipped.

In the AI inference server sector, five Chinese companies rank among the global top ten: Inspur, Huawei, New H3C, Sugon, and Lenovo.

In the fiber optic sector, four Chinese companies—YOFC, Hengtong Optic-Electric, Zhongtian Technology, and FiberHome—are among the global top ten.

In the optical module sector, seven of the top ten global manufacturers are Chinese. The "Yi-Zhong-Tian" trio (Eoptolink, Zhongji Innolight, and TFC Communication) account for 60% of the 800G/1.6T high-speed optical module market.

China produces 60% of the world's transformers, which are in short supply globally.

Additionally, China holds another potential advantage in AI infrastructure: its engineering and infrastructure speed.

Building an AI supercomputing center in the United States takes about three years. In China, constructing a large data center takes 18 to 24 months, or as little as six months or even less with prefabricated and modular approaches.

▲ The data center in Zhongwei, Ningxia. Source: Ningxia Daily

What is the foundation behind China's speed?

It is "people."

China produces over 5 million graduates in science, technology, engineering, and mathematics (STEM) fields annually, with top AI researchers accounting for 50% of the global total. This talent ecosystem allows ideas to take root and grow at an astonishing pace.

China also has a vast army of industrial workers: electricians, construction workers, plumbers, steelworkers, and installation technicians. Without their efficient collaboration and rapid response, even the most advanced blueprints would remain on paper.

Ultimately, the competition in AI infrastructure is a "final exam" for a country's accumulated infrastructure and comprehensive national strength.

Once, we lacked high-speed rail. Today, we have built the world's largest high-speed rail network, spanning over 50,000 kilometers.

Once, we were a power-poor nation. Today, we are the only country in the world with universal electricity access.

Once, our land was divided by towering mountains and natural barriers. Today, among the top 500 highest bridges in the world, we dominate with 439.

History has proven that China is a true infrastructure powerhouse. The future will prove that in the AI era, we can equally become the world-leading AI infrastructure powerhouse.

【References】

[1] "AI Is a Five-Layer Cake" by Jensen Huang

[2] "U.S. Media Realizes: Building AI Data Centers Requires China's Power Equipment" by Guancha.cn

——END——

Welcome to follow [Hua Shang Tao Lue] to learn about influential figures and read legendary strategies.

All rights reserved. No unauthorized reproduction allowed.

Some of the images are sourced from the internet.

If any infringement is involved, please contact us for deletion.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle