Jensen Huang’s One-Liner Sends Marvell Stock Soaring 25%: The Rise of the AI Sector’s Most Influential Figure

06/03 2026

06/03 2026

619

619

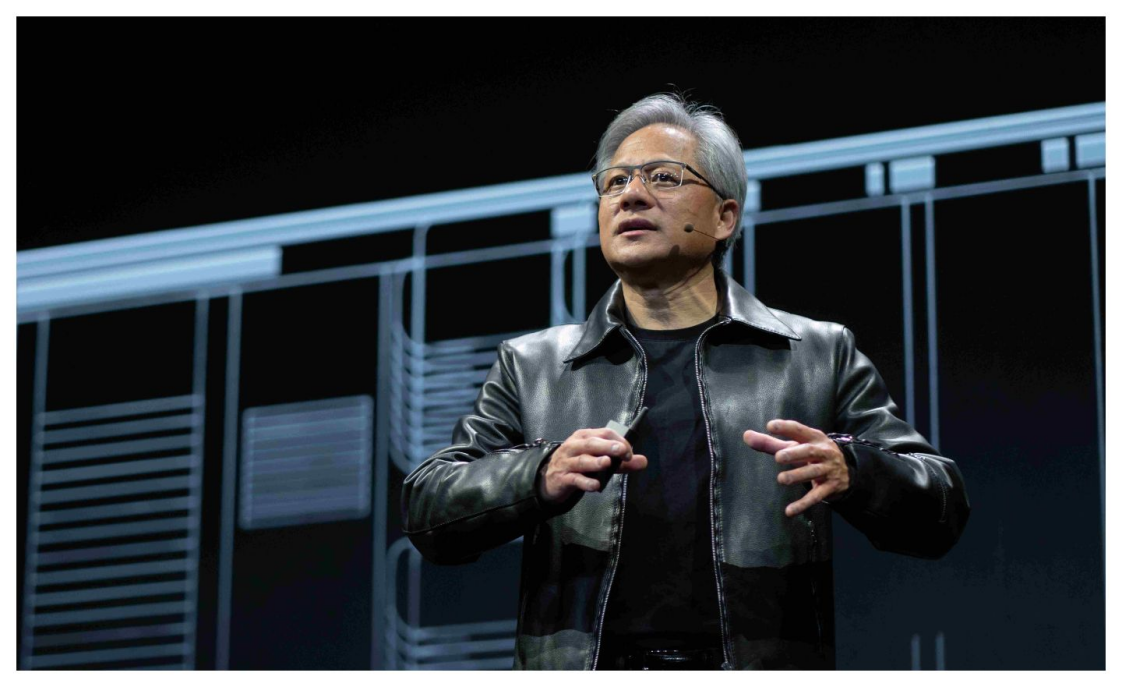

At COMPUTEX 2026, Jensen Huang shared the stage with Marvell’s Matt Murphy and made a bold declaration: “Ladies and gentlemen, Marvell is poised to become the next trillion-dollar company.” This statement was met with thunderous applause and triggered a 25% surge in Marvell’s stock price, rivaling the market impact of HPE’s exceptional earnings report.

Whether you’ve been paying close attention or not, this year’s market has developed a Pavlovian response: follow NVIDIA, and the gains will follow. Jensen Huang has effectively become the AI sector’s most authentic and influential figure, wielding the power to significantly influence market trends.

COMPUTEX 2026 brought together luminaries from the computing world, focusing not just on computation but also on the future of AI. The signals released by industry leaders during this event extend far beyond Marvell’s stock surge. The entire AI landscape is undergoing significant transformation, with Jensen Huang’s five-layer framework (energy, chips, infrastructure, models, applications) driving wealth redistribution at every level.

The chip layer has already produced NVIDIA, the first $5 trillion company in history, along with $2 trillion Broadcom and other trillion-dollar players like TSMC, AMD, ARM, and Intel. The infrastructure layer has seen Micron, SK Hynix, and Samsung Electronics achieve remarkable growth, with storage companies like Sandisk, Seagate, Western Digital, and Jiangbo Long following suit.

What’s next on the horizon? Optical modules or liquid cooling? This time, Huang emphasizes connectivity as the incremental driver, advocating for a combined approach of “fiber and copper.” Chips and storage form the backbone of servers, which in turn form clusters requiring robust data center and AI factory connectivity—key to the expansion of distributed data centers. Murphy elaborated on the value of connectivity in his speech, noting that AI infrastructure bottlenecks are being addressed sequentially: computing power (led by NVIDIA) → memory (with new trillion-dollar memory companies emerging) → connectivity (currently in focus).

How to address connectivity challenges? Huang advises: “Use copper where possible, and optics only where necessary.” Copper has physical limitations in bandwidth and distance, making it a simple, low-cost, and practical solution before those boundaries are breached. Once critical points are passed, fiber optics will handle inter-rack, inter-data center, and cross-data center expansion. “For the next 5-10 years, we’ll rely heavily on copper while also deploying vast quantities of optical components. These data centers are now an integral part of our infrastructure,” Huang stated.

Copper can overheat, introduce delays, and limit bandwidth at high densities, necessitating optical or hybrid architectures—exactly Marvell’s area of expertise. As AI data centers’ physical limits shift from computation to transmission, Huang’s endorsement of Marvell is no coincidence. The company specializes in building “critical networking and connectivity infrastructure for next-gen AI data centers.” On the same day, NVIDIA announced full mass production of its Spectrum-X Ethernet silicon photonics technology, supporting the deployment of the NVIDIA Vera Rubin platform for horizontal and cross-regional AI factory expansion in data centers.

Which companies are active in the connectivity layer? I asked AI to compile this list:

AI Ethernet switch chips: Broadcom, Marvell, Arista

High-speed interconnects and Retimers: Astera Labs, Credo

Copper cables and AEC: Credo, Amphenol, TE Connectivity

Optical modules and CPO: Coherent, Lumentum, Ciena

AI server network architecture: Nvidia, Broadcom, Marvell, HPE, Arista

But Huang’s infrastructure vision extends beyond connectivity. Storage forms one part, connectivity another, with liquid cooling also playing a crucial role. All infrastructure supporting data center expansion is being revalued, with AI server adoption already surging.

Dell’s Q1 FY2027 revenue hit $43.8 billion (+88% YoY), with AI server revenue surging to $16.1 billion (compared to $1.9 billion YoY, a 7x increase). New AI orders reached $24.4 billion, with a backlog totaling $51.3 billion—locking in two years of future performance. HPE’s Q2 results triggered a 28% after-hours surge, with AI server order growth far exceeding expectations. Lenovo’s ISG business reported $5.6 billion in revenue (+37% YoY) and $202 million in profit, both record highs, with AI server order backlog expanding to $21 billion.

These three traditional hardware giants have seen miraculous stock rallies this year: Lenovo +160% (doubling last week alone), Dell +150%, HPE +80%. The logic is simple: AI computing power ultimately requires complete server systems. Server vendors now sell racks, networking, switching, routing, storage, power, and cooling as a package—not just standalone machines. Even Softstone (parent company of Mechanical Revolution) has ridden this wave—this IT services and solutions provider has repeatedly appeared in Huawei Ascend and domestic AI server supply chains over the past year.

This layered logic also applies to Huang’s application layer vision.

The clearest hardware explosion point has been AIPC—not just a concept, but backed by sales data. Gartner projects global AI PC shipments will reach 143 million units by 2026 (55% penetration), meaning one in two new computers will run AI with NPU. MacBook series remain hot sellers, with even “headless MacBooks” (screenless products like Mac Studio and Mac mini) in short supply as developers find them most cost-effective for local model running.

At COMPUTEX, NVIDIA unveiled RTX Spark, a superchip designed for AI PCs. Huang stated that NVIDIA would partner with Windows to redefine PCs, creating a Windows platform specifically designed for AI Agents—completely reconstructing PC computing paradigms. Microsoft, ARM, and NVIDIA now aim to make Arm on Windows equal to x86 in performance and capability.

Qualcomm has supplied Arm CPUs for Windows laptops for two years, yet Arm holds less than 6% of the PC market share—not due to inferior architecture, but Qualcomm’s weak ecosystem. Now NVIDIA enters with RTX Spark for PCs, completely changing the game.

The software layer is evolving more slowly. Tencent’s stock soared over 10% today—its biggest single-day gain in over five years, adding HK$408 billion in market cap—simply due to rumors of a WeChat AI assistant launch. The market is voting with its wallet: WeChat’s massive user base combined with AI Agent capabilities may represent the surest signal for AI application adoption. The day WeChat AI assistant formally launches to consumers will truly ignite the AI application layer.

The question remains: How to commercialize consumer AI? Doubao plans to launch paid subscriptions starting late June (from RMB 68) while exploring e-commerce integration. Subscription models, advertising, e-commerce—all paths are being explored, but definitive answers remain elusive.

Huang’s speech proposed distributed Agent operation, believing future AI models will reside permanently on notebooks, workstations, and various endpoint devices rather than as single cloud brains. Qualcomm’s Cristiano Amon systematized this vision at COMPUTEX—2026 will be the “Year of the Agent,” with computing resources spanning milliwatt-class earbuds, glasses, and watches up to kilowatt-class vehicles, robots, industrial systems, and data centers, forming an “end-to-edge-to-cloud computing continuum.” Globally, over 40 smart glasses models are in production or have been launched, with Qualcomm predicting smart glasses will become the largest personal AI device category. AI phones, cars, and earbuds will all host Agents eventually, but widespread adoption takes time.

Thus, Marvell’s 27% surge essentially shares the same phenomenon as Dell, Lenovo, and HPE’s rallies: capital seeks AI targets with reasonable valuations, but stable cash flow remains more important than empty promises. The first explosions always happen in infrastructure.

Every technological revolution in history shares this trait: infrastructure always precedes applications.

Railways came before commercial prosperity; power grids preceded household appliance adoption; internet coverage and 3G networks enabled the iPhone and Xiaomi phone explosions, followed by mobile app booms. AI follows the same pattern—the biggest profits now come not from applications, but from infrastructure “shovel sellers.”

From GPUs to HBM, storage to connectivity, liquid cooling to servers, data centers to AI PCs—every time Jensen Huang takes the stage, he draws a new treasure map for the market. He points the direction, but the market creates the wealth itself.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle