Top Robotics Firm Goes Public, Yet Unitree Faces a Steep Climb Ahead

06/04 2026

06/04 2026

537

537

At the 2025 Spring Festival Gala, a troupe of robots clad in floral-patterned jackets stole the show with their lively Yangko dance, etching an unforgettable moment into the audience’s memory. This whimsical yet captivating performance thrust Unitree into the public eye, branding it as a "top-tier" name in robotics.

When the topic of robots arises, Unitree is often the first name that comes to mind.

A year and four months later, the company transitioned from the stage to the STAR Market. On June 1, Unitree Technology officially cleared its listing hearing and is poised to become the "first A-share humanoid robot company." From prospectus submission to hearing approval, the process took just 73 days.

But amid the excitement, a lingering question remains for most: beyond performances, what practical applications do these dancing, tumbling robots have? What commercial value can they unlock, and for whom? Behind the glare of the spotlight, will Unitree, now a recognized leader, sustain its winning streak?

I. Who is buying Unitree's robots?

Unitree Technology’s operating revenue soared to RMB 1.699 billion in 2025, up 332.64% from RMB 393 million in 2024—a remarkable growth rate.

By Q1 2026, however, the revenue growth rate had slowed to 68.49%, with an expected H1 growth rate of 35.62%–45.61%. The company acknowledged that with a significantly higher revenue base, easing industry hype, and intensifying market competition, sustaining such high growth rates may prove challenging.

Breaking it down, quadrupedal robots were once the undisputed mainstay.

In 2023, quadrupedal robots contributed 75.78% of the main business revenue. By 2025, humanoid robots accounted for 51.78%, surpassing quadrupedal robots for the first time.

In 2025, Unitree sold 5,215 humanoid robots at an average price of RMB 166,400 and 23,037 quadrupedal robots at an average price of RMB 30,300. While humanoid robots command a much higher unit price, their prices are declining rapidly—from an average of RMB 260,400 in 2024, a 36% drop in just one year.

Looking ahead, "who is buying?" and "what are they buying for?" matter more than just sales volume.

The buyer structure for quadrupedal robots is relatively balanced. In the first three quarters of 2025, research and education accounted for 31.58%, commercial consumption for 42.30%, and industrial applications for 26.12%. For the first time, commercial consumption surpassed research and education as the largest revenue source, driven mainly by surging online sales.

Unitree believes that in the short term, industry scenarios such as power grid inspections and firefighting rescue will be the first to adopt its robots, while in the medium to long term, it sees strong potential in the consumer market.

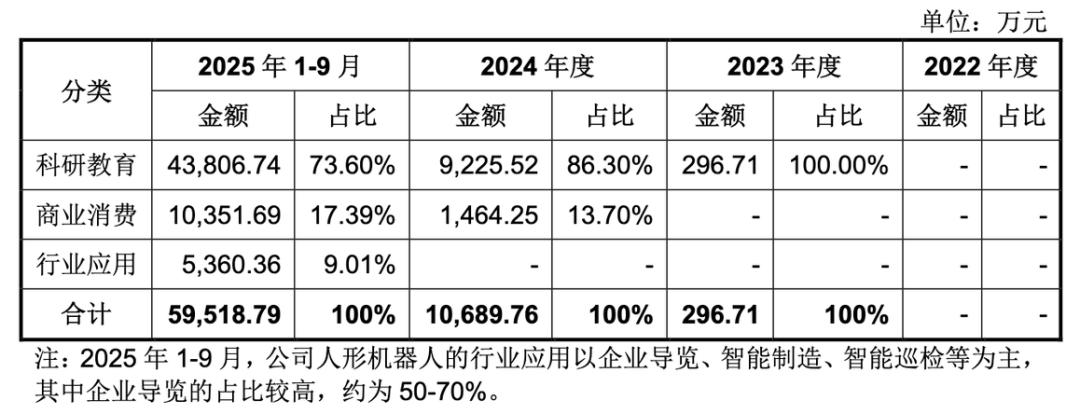

Humanoid robots, however, show a clear "bias." During the same period, research and education accounted for 73.60% of humanoid robot revenue, commercial consumption for 17.39%, and industrial applications for just 9.01%. Within industrial applications, corporate guided tours accounted for roughly 50%–70%.

In other words, the main buyers of humanoid robots are still universities, research institutions, and tech companies, which use them primarily for algorithm validation, secondary development, and research projects. The proportion of robots actually entering factories for handling, quality inspection, assembly, and inspections remains small.

Research and education clients are typically less price-sensitive, and with limited options for humanoid robot products currently available, Unitree often sees sustained repeat purchases from existing customers whenever it launches a new model.

As mentioned in its response letter, the offline repurchase rate in the research and education sector rose from 49.71% in 2023 to 59.38% in 2024 and remained at 56.58% in the first three quarters of 2025. The average purchase amount from repeat customers increased from RMB 349,500 in 2022 to RMB 1,390,700 in the first three quarters of 2025.

While a high repurchase rate is certainly positive, it may also indicate slower growth in new customer acquisition. For example, the repurchase rate in the commercial consumption sector declined, which the company attributed to a surge in new customers and rapid revenue growth following increased brand recognition.

On one hand, the research and education market has a relatively narrow customer base. On the other hand, research in this field still focuses on validating "whether the technology works" rather than "whether it is commercially viable" or "how broad the market is."

Unitree's prospectus states that in the short to medium term, humanoid robots will primarily be used in scientific research, application development, education, cultural performances, and intelligent services. The long-term goal is to enter factories and households, providing services for industrial, domestic, and social scenarios.

Whether for quadrupedal or humanoid robots, both face the same challenge: bridging the gap between "someone is buying" and "being applied to a wider range of scenarios" involves not just time but also a series of yet-to-be-broken bottlenecks.

II. What does Unitree lack for large-scale commercialization?

Let's first clarify three key concepts in embodied intelligence: "body," "cerebellum," and "brain."

The "body" refers to physical hardware such as mechanical structures, joints, and dexterous hands. The "cerebellum" handles motion control—walking, balancing, and somersaulting—to ensure the robot "stands steady and moves smoothly." The "brain" corresponds to the embodied large model, responsible for understanding tasks, planning actions, and adapting to new environments.

A weakness in any of these three layers can drag down overall performance.

Currently, some robot players excel at the "brain," while others lean more toward the "body" school.

For body-focused players, an awkward situation is emerging: robots perform impressively in single-task abilities like running, jumping, or backflips. However, when placed in real production lines or home environments with changeable (dynamic) scenarios and tasks, they struggle to cope.

For brain-focused players, the issue lies elsewhere. Models perform brilliantly in simulated environments but may encounter engineering problems like sluggish responses, structural errors, or communication delays when deployed on real robots. Ultimately, model capabilities are constrained by the physical hardware itself.

Unitree's early R&D investments focused more on the body and cerebellum, only starting to strengthen R&D for the embodied large model (the brain) in 2024.

Unitree's competitive advantages also lie in the body and cerebellum. Its quadrupedal robots rank first globally in shipments, and its humanoid robots can perform standing backflips and side flips, thanks to solid motion control algorithms and in-house hardware R&D capabilities. There is no dispute about this in the industry.

In Wang Xingxing's view, developing the brain carries higher risks because no one can guarantee who will do it best or fastest—the AI field changes extremely rapidly. In contrast, hardware companies may face less volatility.

This strategy has not only given Unitree an edge in shipments and market share but also created its current bottlenecks.

In its response letter, Unitree admitted that two core bottlenecks currently restrict its general-purpose robots from entering factories and households: insufficient generalization capabilities of the embodied large model and inadequate precision and durability of dexterous hands.

Among these, the generalization capability of the embodied large model is more critical. Enhancing robot versatility and reducing reliance on scenario-specific programming is key to making robots truly productive tools.

For example, industrial settings involve numerous non-standard variables across industries (e.g., oily floors, dynamic material stacking). Existing training data mostly comes from laboratories or single, customized scenarios, making it difficult to cover cross-scenario differences. In home settings, highly unstructured living environments and personalized user needs far exceed the boundaries of current training data.

Currently, the paths for embodied large models have not converged, with multiple technical routes—such as VLA models, WMA models, and dual-system approaches—developing in parallel. This is another manifestation of how rapidly the AI field evolves and why developing the brain carries high risks.

Industry players commonly adopt VLA architectures (vision-language-action large models) to enable robots to see scenes, understand instructions, and directly generate actions. Models like Galaxy Universal's GraspVLA and TrackVLA, Qianxun Intelligence's Spirit-V1.5, and Physical Intelligence's π-0 follow this route. Some have already been integrated into product pipelines, collecting data and iterating through real-world tasks.

Unitree focuses on WMA (World Model) as its primary direction while betting on both VLA and WMA routes. It has open-sourced two versions—UnifoLM-WMA-0 and UnifoLM-VLA-0. Its prospectus states that its self-developed general-purpose embodied large model has undergone R&D testing and deployment verification in pilot scenarios such as its own factories.

The latest development is that in May 2026, Unitree released its next-generation brain, WVLA2.0, and deployed a conference room autonomous organization function on the G1. Meanwhile, the G1 entered Tokyo's Haneda Airport for luggage handling trials, a project set to run until 2028.

Compared to Qianxun Intelligence's G1, which has already started scaled operations in CATL's factories, Unitree Technology's G1 at Haneda Airport is still in a "pilot verification phase."

Nearly half of Unitree's IPO proceeds—around RMB 2 billion—will go toward brain-related R&D, covering technical breakthroughs in large and cerebellum models, training infrastructure setup, and real-world data collection. The plan is to release a "general-purpose humanoid robot embodied foundation model" within three years, capable of scenario generalization, instruction generalization, action generalization, and task generalization.

III. What cards does Unitree hold?

Strengthening its brain R&D is precisely about maximizing the value of the cards Unitree already holds. But first, let's examine the strengths and limitations of these cards.

The first card is manufacturing efficiency and cost control.

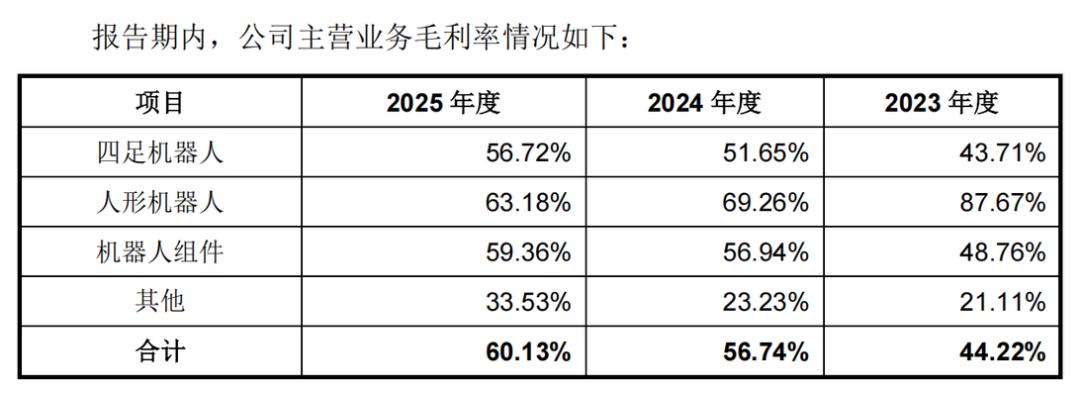

From 2023 to 2025, Unitree's gross margin rose from 44.22% to 60.13%, despite continuous price reductions for its products. This reflects cost advantages from in-house R&D of key components and scaled-up shipments. By manufacturing motors, reducers, and joint modules in-house and negotiating lower prices through bulk procurement, Unitree also leverages a shared supply chain for quadrupedal and humanoid robots to spread costs.

Of course, the relatively price-insensitive nature of research-oriented and demonstration-oriented demand also plays a role.

However, when the downstream market shifts to households or factories, factory owners will calculate how quickly a robot can recoup its cost compared to hiring workers. At that point, manufacturing efficiency advantages may persist, but gross margins are unlikely to remain as attractive.

Honor's strong performance in a half-marathon offers some insights. Prior to the event, Honor's humanoid robot team had been established for just over a year, and the half-marathon project began even later.

This does not mean Unitree's engineering barriers do not exist, but it points to a trend: as supply chains for core components and motion control algorithm infrastructure mature, the time it takes for latecomers to catch up in motion capabilities is shortening.

The second card is cross-platform reuse.

Some components of humanoid robots share commonalities with quadrupedal robots, allowing technical sharing and reuse in core modules such as joints, structures, batteries, and algorithms. This reduces R&D and mold costs while accelerating the transition from prototype to mass production. Reuse enables Unitree to move faster and cheaper in bipedal motion control.

However, reuse addresses how to build cheaper, not what to build to sell.

The current robotics industry resembles the early automotive industry, with diverse forms. Large-scale production later forced an optimal solution—Ford's Model T plus assembly lines—leading to industry convergence.

Today's coexistence of humanoid, wheeled, and quadrupedal robots may eventually converge into a single dominant form or result in optimal forms tailored to each mature scenario.

From this perspective, Unitree's simultaneous development of quadrupedal, humanoid, and wheeled versions is not just risk hedging but also preparation for different endgames. Before the hardware endgame is determined, reuse helps Unitree win local battles but does not decide whether it has chosen the ultimate battlefield correctly.

The third card is data from shipments.

Physical interaction data generated by devices is a scarce resource. Just as Tesla uses driving data from millions of vehicles to train FSD, Unitree follows a similar logic: the more robots it ships, the more data it collects, and the smarter its models become.

However, a key difference exists between embodied intelligence data and autonomous driving data. Tesla drivers naturally generate labeled signals with every brake or lane change. In contrast, a robot's physical interaction data only becomes valuable with clear task objectives and success/failure feedback.

Currently, Unitree's devices mainly flow into research and demonstration scenarios, with limited task diversity. While somersaults, dances, and parkour moves are impressive, they offer little value for training a "brain" capable of factory work.

As supply chains reach a higher level of maturity, manufacturing efficiency may eventually catch up. However, the benefits of reuse hinge on whether the long-term objectives align with the strategic path chosen by Unitree. Additionally, the data feedback loop is currently lacking effective training mechanisms. These issues are not exclusive to Unitree; rather, they are indicative of the developmental stages the entire industry is still working through. The quicker a company progresses, the sooner it will face these challenges—and its ability to surmount them will shape its trajectory in the years ahead.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle