Why Is CATL Included on DeepSeek's Major Investor List?

06/04 2026

06/04 2026

618

618

Today, foreign media released a report detailing the latest financing developments at DeepSeek.

The financing scale remains unchanged at 5 billion yuan, with an estimated valuation ranging from 350 to 400 billion yuan.

This time, however, the investor lineup was further unveiled. Tencent is set to invest 10 billion yuan, while CATL, the world's foremost power battery manufacturer, plans to contribute 5 billion yuan, joining Tencent as the largest external investors.

DeepSeek anticipates securing no more than 10 financing entities in this round, including other participants such as the National Integrated Circuit Industry Investment Fund and internet giants like NetEase and JD.com.

The involvement of internet companies in DeepSeek's investment comes as no surprise—no further explanation is needed—given their inherently digital nature. These companies must either proactively transform using large models or risk being overtaken by new business models driven by such innovations.

CATL's participation, however, is particularly noteworthy. A battery manufacturer and a large model developer don't intuitively seem like natural partners. Yet this seemingly unusual pairing holds the key to understanding the latter stages of the AI competition.

The Energy Bottleneck in the AI Race's Latter Stages

DeepSeek is not in need of funds. It originated from the renowned quantitative fund High-Flyer and faces no financial constraints. Liang Wenfeng, its founder, was not initially eager to bring in external shareholders. Beyond raising capital, the primary goal of this financing round is to establish an anchor for employee stock options and to serve as a strategic "alliance-building" move.

Merely possessing capital is insufficient to secure a spot on the final investor list; what truly matters is the resources one can contribute to DeepSeek's future growth.

Tencent can offer substantial resources, particularly if DeepSeek becomes more focused on serving consumer clients. Tencent's distribution channels would be immensely beneficial. Moreover, Tencent is quite proactive—its 10 billion yuan investment is likely the largest among external shareholders.

Tencent's own large model, "Hunyuan," has underperformed, lagging behind ByteDance's Doubao and DeepSeek. With WeChat and QQ, Tencent boasts a massive user base in the hundreds of millions but lacks a sufficiently powerful model.

As early as the beginning of 2026, WeChat Search and Tencent Yuanbao had already integrated DeepSeek. For Tencent, rather than waiting for its own model to catch up, it makes more strategic sense to incorporate the best model directly into its ecosystem.

What can CATL offer? Over the past two years, the industry has been preoccupied with questions about computing power and chip availability. However, entering 2026, the most perceptive industry players have begun to realize that the competitive focus is shifting deeper—from "who has computing power" to "who has electricity."

The most prominent advocate of this perspective is NVIDIA's Jensen Huang.

At the COMPUTEX conference, he repeatedly emphasized the looming electricity shortage. He bluntly stated that Taiwan's manufacturing sector is expanding too rapidly, outpacing its electricity supply. "To unify human labor, robotic labor, and AI labor, we need a lot more energy," he remarked.

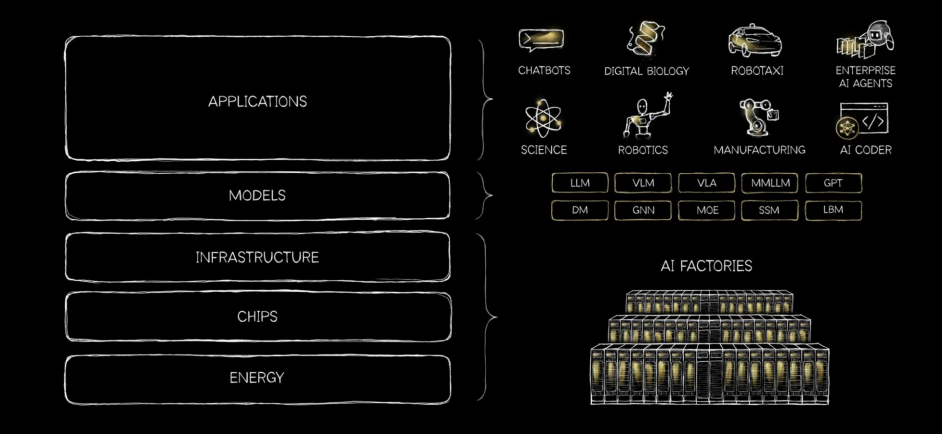

Huang employs a "five-layer cake" framework to describe the AI industry: from bottom to top, it consists of energy, chips, infrastructure, models, and applications. Notice what lies at the foundation: not chips, but energy. In his view, electricity is not merely a supporting element for AI but the cornerstone of the entire edifice.

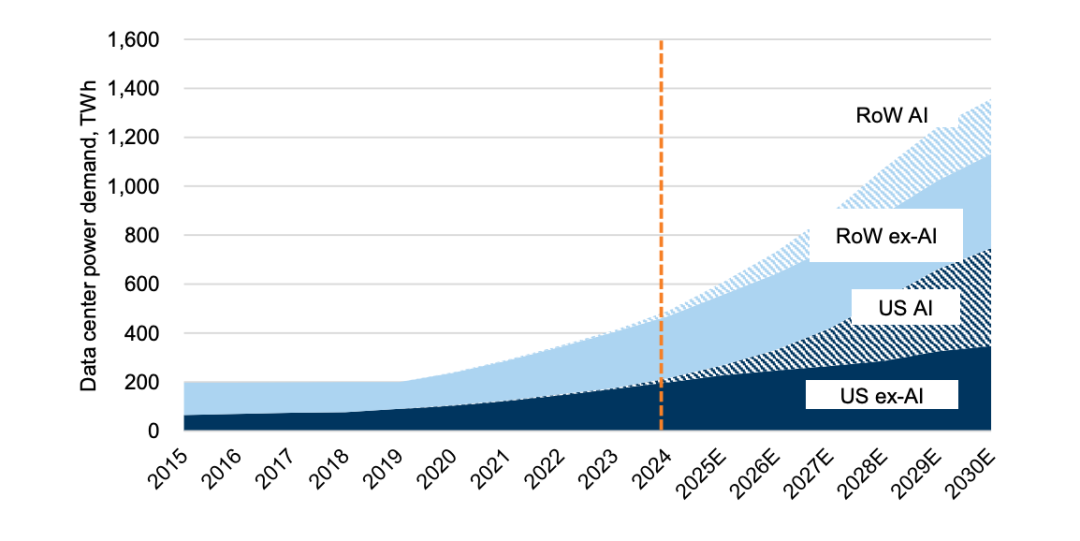

Why is AI so energy-intensive? Consider this: An AI data center is essentially a facility packed with tens of thousands of chips operating continuously, converting electricity into computational power. The larger the model and the greater the user base, the more electricity this facility consumes. And just how substantial is this consumption? Recent calculations by several top investment banks yield staggering figures.

In a report from early 2026, Goldman Sachs significantly revised upward its forecast for global data center electricity demand: by 2030, global data center electricity consumption is projected to increase by 220% compared to 2023, representing a net increase of approximately 905 terawatt-hours. In the United States, data center installed capacity is expected to surge from 32 gigawatts in 2025 to 95 gigawatts in 2030—roughly tripling in five years.

Morgan Stanley, in a report from late May, estimated that electricity demand for data centers in Asia will grow at an average annual rate of about 24% between 2023 and 2030, outpacing growth in the United States and Europe, primarily due to stronger expansion in AI inference (i.e., the widespread use of models after deployment).

To meet this colossal demand, annual energy investment across Asia will need to double—from about $660 billion per year over the past decade to an average of $1.1 trillion per year over the next five years. The International Energy Agency shares a similar outlook: global data center electricity consumption will rise from 415 terawatt-hours in 2024 to about 945 terawatt-hours in 2030, roughly equivalent to Japan's current national electricity consumption.

These figures converge on a single conclusion: In the latter stages of the AI race, the truly scarce—and truly lucrative—resource is shifting from chips to electricity. Consequently, something previously unthinkable is now occurring: energy companies are, for the first time, taking center stage in the AI narrative.

CATL: Beyond a Battery Maker; DeepSeek: No Ordinary Model Provider

Yet, a crucial link remains to be established. CATL manufactures batteries, but what does that have to do with data centers?

First, it's essential to recognize that CATL is no longer merely a battery manufacturer. Over the past year, CATL has made significant investments in what the industry terms "computing-power-electricity synergy." In essence, this involves linking the "power generation, storage, and supply" chain with "computing power consumption."

CATL invested approximately 4.1 billion yuan to acquire a stake in the controlling shareholder of electrical equipment company Hithium and spent about 6.4 billion yuan to become the largest shareholder of data center operator 21Vianet, with total investments exceeding 10 billion yuan. Morgan Stanley even bestowed upon it a new identity: "A power infrastructure giant for the AI era."

This transformation is not occurring in isolation. The industry is evolving: Supplying power to AI data centers was once the domain of traditional electrical companies, but starting in 2025, a wave of companies originally focused on battery energy storage, backup power (those "super-sized power banks" that activate when the grid fails to keep machines running), and even electric vehicle charging stations began entering the data center power supply business en masse.

For CATL, investing in DeepSeek means directly aligning itself with China's premier demander of computing power, securing its energy storage and power supply solutions in the procurement lists for AI infrastructure.

But here's the query: AI does require electricity, but couldn't DeepSeek, like its competitors, simply rent computing power from cloud providers, purchase cloud services, and outsource the complexities of electricity, data centers, and daily operations? Indeed, competitors like Zhipu and MiniMax have largely adopted this "asset-light" approach, minimizing expenditures and maintaining agility.

So why does DeepSeek need an energy partner?

The answer lies in its core strategy. From the outset, DeepSeek has embraced an "asset-heavy" approach. High-Flyer self-funded the construction of its initial computing cluster for 200 million yuan in 2019 and a second for 1 billion yuan in 2021, equipped with roughly 10,000 NVIDIA A100 chips. It also developed its own low-level scheduling software.

For DeepSeek, "controlling physical-layer computing power" is not a novel option but an ingrained capability. Its greatest strength lies in maximizing computing efficiency through hardware-software synergy. This is why its R1 training and inference costs were low enough to astonish Silicon Valley.

Once you opt to build your own data centers, you internalize the "electricity problem." Asset-light competitors offload electricity concerns to cloud providers, eliminating the need for energy partners. However, DeepSeek, which constructs its own data centers, must address the issues of electricity sourcing, storage, and stability. This explains why an energy company like CATL is on its investor list.

Supporting this asset-heavy strategy is an enticing business proposition. Selling models on a pay-per-use basis (known in the industry as MaaS, or Model-as-a-Service) is emerging as a lucrative market: Citigroup predicts that this business for Alibaba Cloud will grow at an average annual rate of 235% over the next five years, accounting for more than half of Alibaba Cloud's total revenue by fiscal year 2031.

In other words, within a few years, more than half of cloud providers' revenue will derive from "selling models" rather than "selling computing power."

Of course, it remains unclear whether DeepSeek aims to expand its MaaS revenue, as its commercial considerations are somewhat opaque, but it's certainly a viable option.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle