Broadcom AVGO: A Clash of Titans—Is the ASIC Camp Fragmenting?

06/04 2026

06/04 2026

608

608

On the early morning of June 4, 2026, Beijing time, following the market's close, Broadcom (AVGO.O) unveiled its financial results for the second quarter of FY2026 (ending April 2026):

1. The crux of this financial report: Broadcom's pivotal guidance projects AI business growth at $16 billion for the next quarter, a sequential increase of $5.2 billion, yet falling short of market expectations, which stood at $17 billion.

Company management provided AI guidance exceeding $56 billion for the current fiscal year and $100 billion for the next fiscal year, figures deemed 'unremarkable.' In fact, mainstream market institutions generally anticipate the company's AI revenue for the next fiscal year to surpass $130 billion.

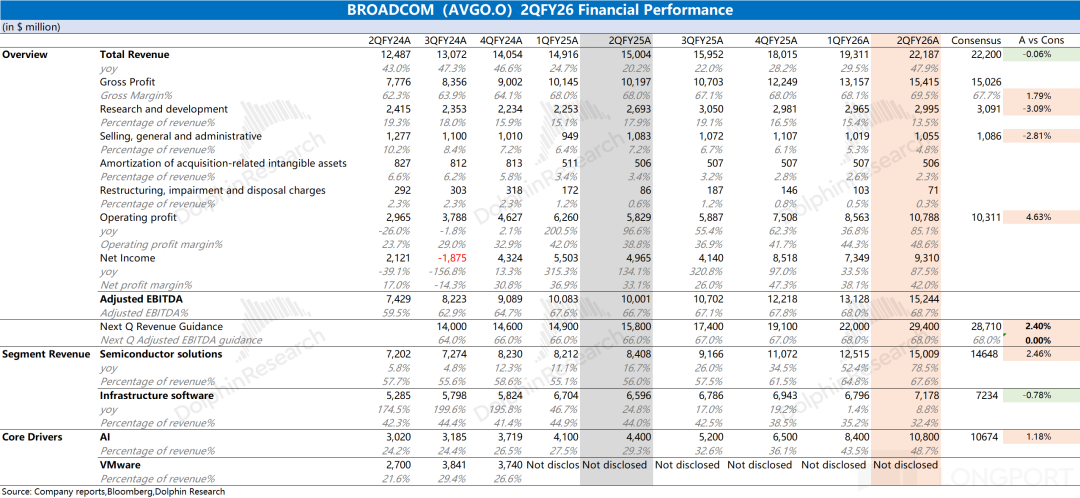

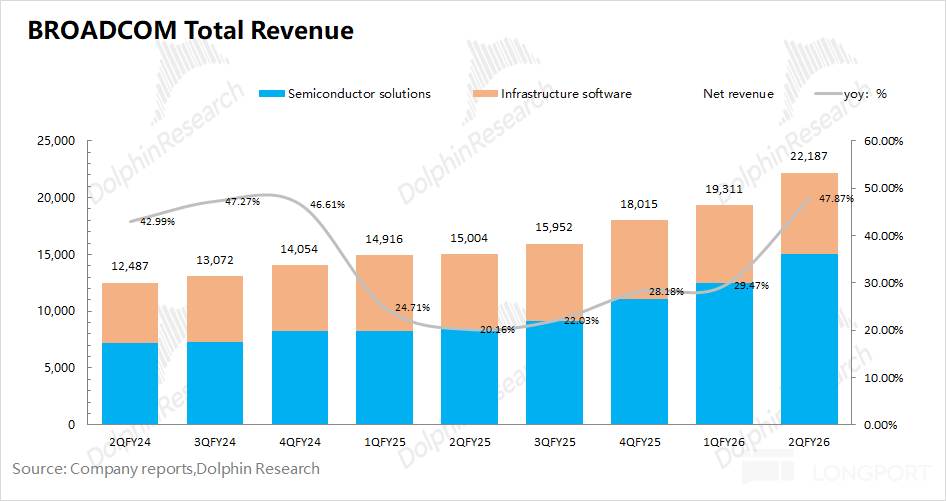

2. Overall performance: Broadcom (AVGO.O) reported revenue of $22.2 billion this quarter, marking a 47.9% year-over-year increase, aligning with market expectations of $22.2 billion. The sequential revenue rise of $2.9 billion was primarily propelled by growth in the AI business.

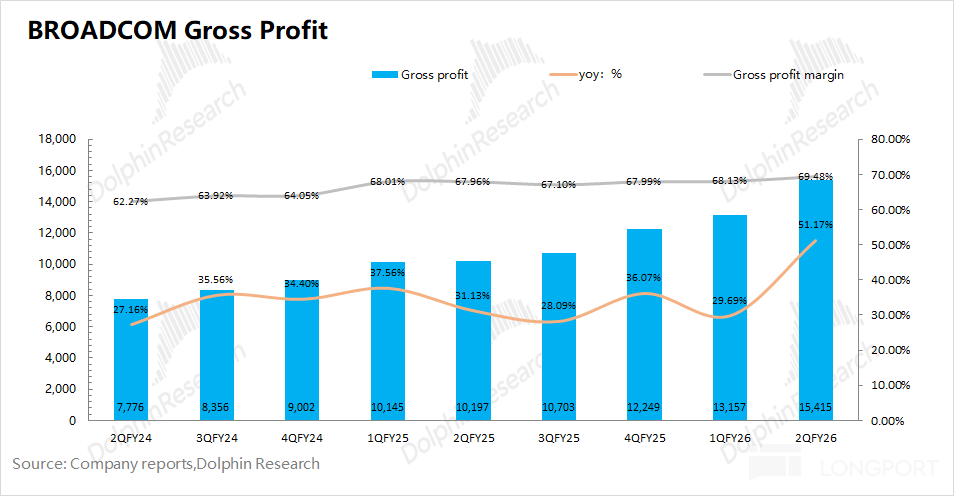

The company's gross margin for the quarter stood at 69.5%. After excluding the impact of acquisition amortization and restructuring expenses, the actual operating gross margin reached 76.1%, remaining relatively stable sequentially. Despite the semiconductor segment's comparatively lower gross margin, the high gross margin of network switching chips within semiconductors served as a hedge.

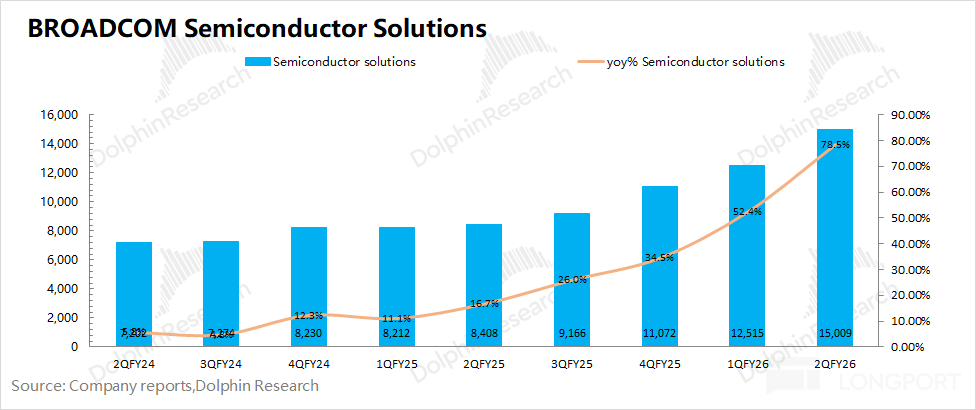

3. Semiconductor business: This quarter, revenue hit $15 billion, a sequential increase of $2.5 billion, with the AI business being the primary contributor to this growth. Details are as follows:

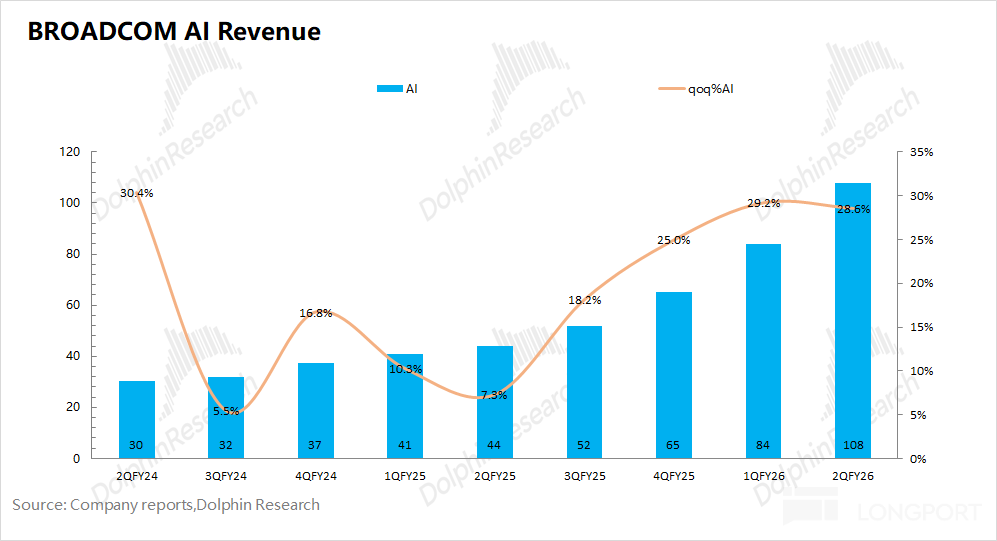

① AI business: Revenue reached $10.8 billion, a sequential increase of $2.4 billion, in line with market expectations of $10.7 billion. Broadcom's AI revenue currently stems from three major customers: Google, Meta, and ByteDance. Quarterly growth was primarily driven by increased shipments of Google's TPU from these major customers.

Meta and other major companies recently raised their capital expenditure outlook for 2026, and Anthropic is also set to start contributing revenue in the second half of the year, suggesting that Broadcom's AI business growth is expected to continue accelerating. The company anticipates AI business revenue of $16 billion next quarter, a sequential increase of $5.2 billion.

② Non-AI business: Revenue amounted to $4.2 billion, a 6% year-over-year increase, with overall stable performance in non-AI businesses.

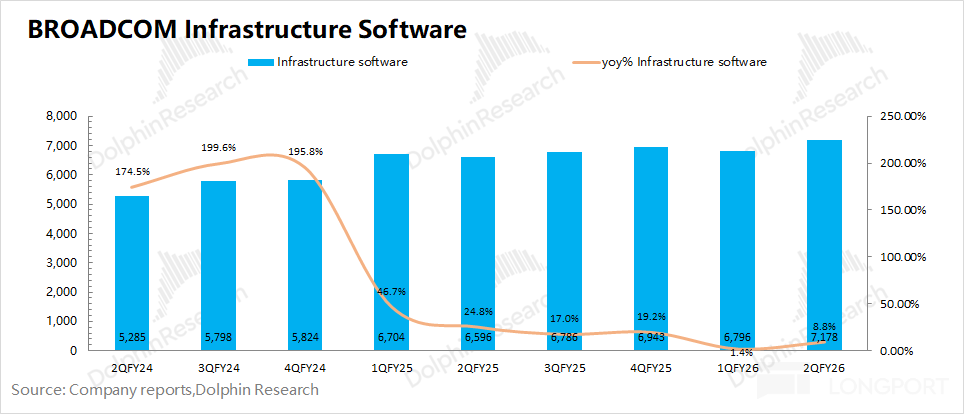

4. Infrastructure software: This quarter, revenue reached $7.2 billion, a 9% year-over-year increase. Previous growth was primarily driven by the integration of the VMware acquisition and adjustments to pricing models (a comprehensive shift from permanent license models to subscription models). The high growth from the acquisition has ended, and future growth in the software business will primarily focus on organic growth from VMware's subscription model.

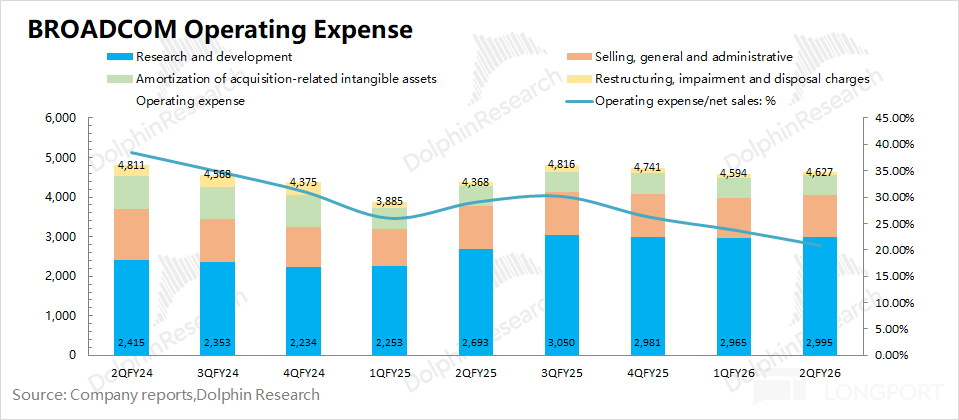

5. Operating expenses: This quarter, core operating expenses (R&D expenses + sales and administrative expenses) were $4.05 billion, slightly increasing sequentially. Affected by scale effects, the core operating expense ratio decreased to around 18.3%.

Over the past two years, the company has significantly increased expenses related to equity incentives (currently accounting for nearly half). Excluding the impact of equity incentives, the company's core operating expenses this quarter were $2.2 billion, a sequential increase of $140 million.

6. Inventory: The company's inventory this quarter was $4.3 billion, a 46% sequential increase. Compared to past single-digit sequential increases, this significant rise is not a concern, as the company is primarily pre-stocking for semiconductor demand such as XPUs.

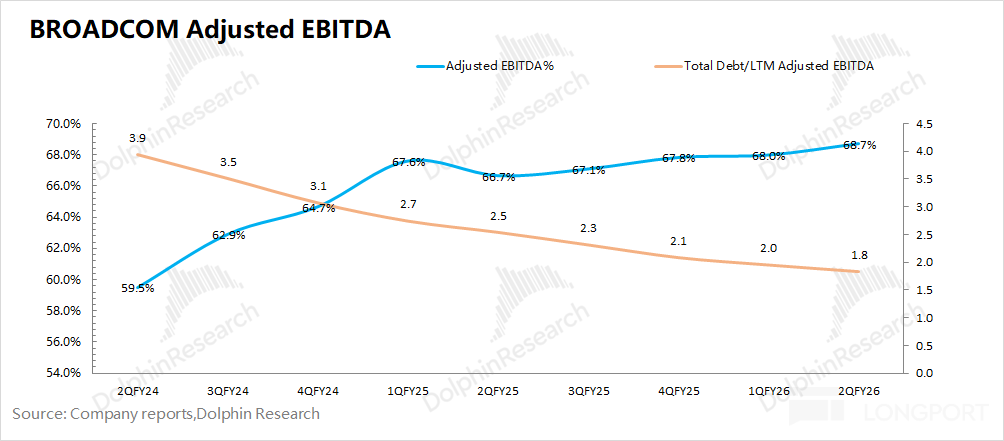

7. VMware integration progress: Dolphin Research introduced the debt repayment metric (Total Debt/LTM Adjusted EBITDA), calculating that this metric further decreased to 1.8 this quarter. This metric has returned to pre-acquisition levels, indicating that the impact of the VMware acquisition on the company's debt has been absorbed within two years.

8. Broadcom's performance guidance: Expected revenue for the third quarter of FY2026 is around $29.4 billion, slightly exceeding market expectations of $28.7 billion. The company anticipates an adjusted EBITDA margin of 68% for the third quarter of FY2026, in line with market expectations of 68%.

Dolphin Research's overall view: Behind the chips lies the ambition to dismantle NVIDIA's 'network fortress.'

Due to the cooperation between Anthropic and Broadcom, which will shift from purchasing entire server racks to chip sales, the market has already adjusted downward its expectations for Anthropic's revenue contribution to Broadcom AVGO.

From the company's guidance, although AI revenue continues to accelerate, it still falls short of the adjusted expectations of mainstream institutions.

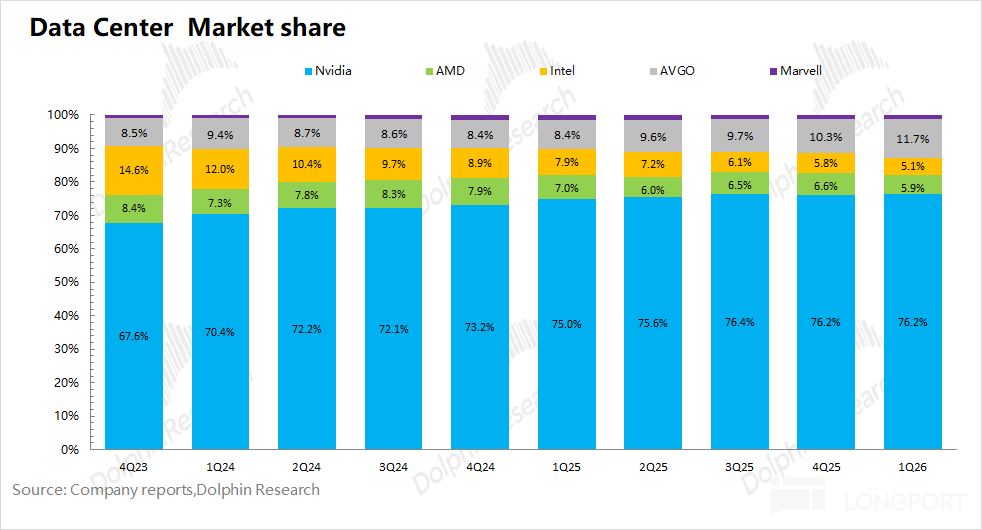

As a core focus, the AI revenue guidance, in a context where peers are operating at full capacity (NVIDIA's latest quarter saw a $13 billion sequential increase, with next quarter's guidance indicating an $8-9 billion sequential increase), appears underwhelming for Broadcom, a more growth-oriented player in the ASIC segment of the computing power market.

a) Customers and capital expenditures: Broadcom AVGO currently has six custom XPU customers (no new additions), including Google TPU, Meta MTIA, Anthropic, Open AI, and two undisclosed customers. Google and Meta are currently the primary 'buyers' of the company's custom ASIC chips and the main sources of AI revenue.

Among new customers, Anthropic will start contributing new increments in the second half of the year. Regarding Anthropic's cooperation with the company, the shift from purchasing entire server racks to chip sales will somewhat impact Anthropic's revenue contribution to Broadcom AVGO, especially in the early ramp-up phase. Chip sales account for only about 20-30% of the revenue from entire server racks, though gross margins are relatively higher.

b) AI chip progress: In the AI chip sector, Broadcom, as the key player behind several cloud vendors' self-developed ASICs, originally aimed to challenge NVIDIA and capture computing power market share.

The market expected it to demonstrate higher growth potential than NVIDIA, thereby increasing the overall market share of ASIC computing power from the current 10%+ to over 20%. However, this quarter's guidance does not align with the market's long-term expectations.

Among the XPU products currently shipped by the company, the most critical product is Google TPU. Currently, TPUv7 is in mass production and ramping up, with greater anticipation for the next-generation TPUv8. TPU8 will come in two versions: TPU8i (inference) and TPU8t (training), both supporting FP4 and roughly catching up to NVIDIA's Blackwell series in terms of computing power performance.

With Google's TPU upgrades and potential future opportunities for external supply, Broadcom's market share in AI chips is expected to continue increasing.

However, a potential concern now is that Google, to further strengthen its self-developed ratio, may gradually reclaim some front-end business processes. The progress of this development remains unclear, but it is indeed a latent concern for Broadcom.

Moreover, in subsequent calls, Broadcom did confirm that suppliers, including Google, are diversifying. Additionally, the usually excellent CEO, Hock Tan, was not at his best this time, initially reading from the script for Q2 2025.

c) The hidden 'network moat': In fact, Broadcom, similar to Marvell, is primarily engaged in network connectivity beyond ASICs, with a stronger product lineup than Marvell.

Behind the ASIC business lies a hidden 'network capability moat,' which is actually the main reason for the company's ability to 'stand out' in the ASIC market.

NVIDIA has nearly monopolized high-end GPU clusters with its proprietary InfiniBand technology (low-latency, lossless networking). However, as cluster scales expand, major cloud vendors, to avoid 'single-vendor lock-in,' are enthusiastically embracing the UEC (Ultra Ethernet Consortium) led by Broadcom.

Broadcom's core strategy is to demonstrate, through ultimate chip performance, that open-source, standardized Ethernet is not only more cost-effective but also more resilient and scalable than InfiniBand in hyperscale clusters.

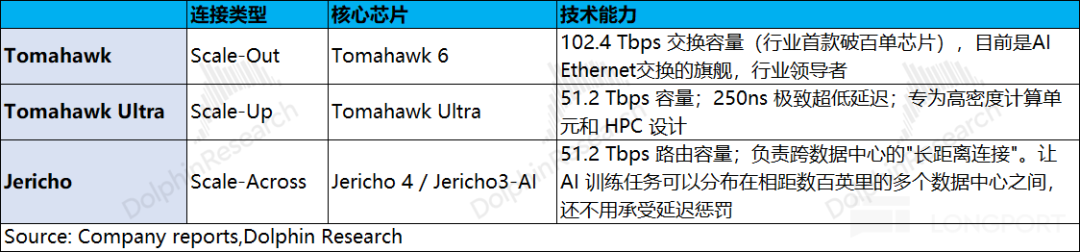

Broadcom's current network business product lineup primarily consists of three segments: 'switching + routing + optical interconnects,' covering Scale-Out, Scale-up, and Scale-Across.

① Tomahawk 6: Broadcom's flagship product. It is the world's first Ethernet switch chip to exceed 100Tbps (reaching 102.4 Tbps) on a single chip, doubling the bandwidth of its predecessor.

Ultra-high bandwidth means that when data centers build clusters with hundreds of thousands of cards, the network hierarchy can be 'flattened' from a three-tier topology to two tiers. Fewer tiers mean fewer 'hops' for data forwarding, resulting in a sharp decline in overall latency and equipment failure rates.

② Jericho 4/Jericho3-AI: Through intelligent 'end-to-end traffic scheduling,' it achieves lossless transmission comparable to or even surpassing InfiniBand under standard Ethernet architectures, enabling hundreds of thousands of chips to function as if within a single system.

Marvell's stock price has recently surged, primarily due to market recognition of its interconnect capabilities. However, Broadcom's 'network capabilities' are hidden behind TPUs/ASICs. As we enter the AI inference phase, the importance of computing power diminishes somewhat, while the significance of 'CPU + storage + connectivity' becomes more prominent. The market is also willing to assign a certain valuation premium to 'connectivity.'

Overall, the company's guidance for the next quarter and the full year is 'relatively weak,' which will temporarily affect market confidence. However, with the AI business still accelerating and new increments from TPU mass production and other customers like Anthropic, the company's growth prospects in AI semiconductors and connectivity remain promising.

As the market gradually recognizes the company's stronger competitiveness in the 'ASIC + connectivity' space, its value will become more apparent.

Below is a detailed analysis.

I. Broadcom's Main Business Overview

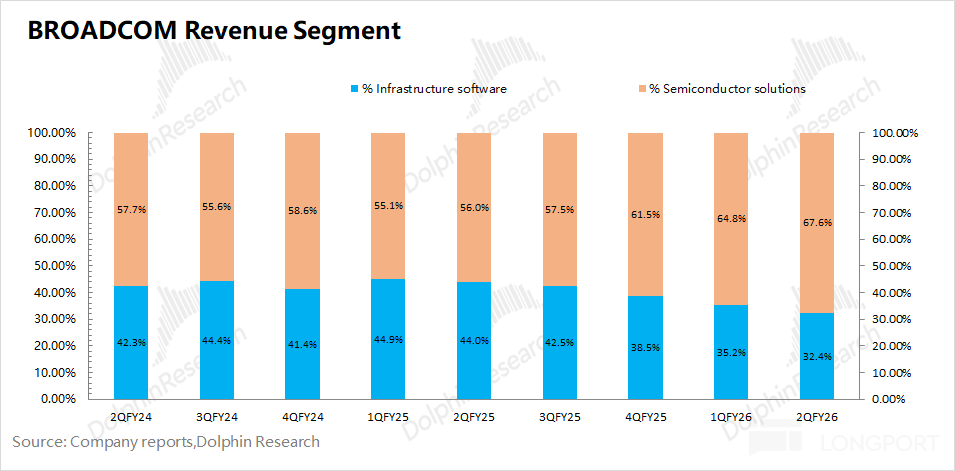

Broadcom's previous performance growth primarily came from its AI business and the acquisition and consolidation of VMware. Thus, the custom ASIC chips in the AI business and VMware's pricing adjustment strategies are the market's main focus. Specifically:

1) Semiconductor Solutions: Primarily benefits from growth in AI revenue, driven by demand for custom ASICs from customers such as Google, Meta, and ByteDance. Other non-AI businesses remain largely flat.

AI Business: Currently, the primary increment comes from shipments of Google's TPU. The company already has six major AI customers (including Google, Anthropic, Meta, and OpenAI), with current revenue primarily coming from Google and Meta. Anthropic will start contributing revenue in the second half of the year.

For the 2027 outlook, the combined computing power demand of the six major customers is expected to reach 10GW (maintained), generating over $100 billion in AI revenue (maintained). Among them, Anthropic's computing power demand exceeds 5GW, and OpenAI will mass-produce its first XPU (computing power exceeding 1.3GW).

2) Infrastructure Software: With the consolidation of VMware, software revenue now accounts for around 30%. The company adjusted pricing strategies for VMware's customers, with price increases driving revenue growth, though this impact has significantly weakened.

II. Overall Performance: AI-Driven Growth Acceleration

2.1 Revenue

Broadcom (AVGO.O) achieved $22.2 billion in revenue in the second quarter of FY2026, a 48% year-over-year increase, in line with market expectations ($22.2 billion). The year-over-year growth was primarily driven by the AI business.

Sequentially, the company's revenue increased by $2.9 billion this quarter, with the AI business contributing a $2.4 billion sequential increment and the software business also seeing sequential growth.

2.2 Gross Profit

Broadcom (AVGO.O) achieved $15.4 billion in gross profit in the second quarter of FY2026, a 51% year-over-year increase. The company's gross margin this quarter was 69.5%, slightly improving sequentially.

After excluding the impact of acquisition amortization and restructuring expenses, the actual operating gross margin was 76%, roughly flat sequentially. Although the semiconductor segment's gross margin is relatively low, the high gross margin of network switching chips within semiconductors provides a hedge.

From a medium- to long-term perspective, the overall gross margin still faces downward pressure due to the increasing proportion of lower-margin ASIC business.

2.3 Operating Expenses

Broadcom (AVGO.O) incurred $4.63 billion in operating expenses in the second quarter of FY2026, roughly flat sequentially.

Excluding equity incentives, the company's core operating expenses (R&D expenses + sales and administrative expenses) were $2.18 billion this quarter, a $140 million sequential increase. Despite the company's current high-growth performance, its operating expenses remain stable.

2.4 Profit Perspective

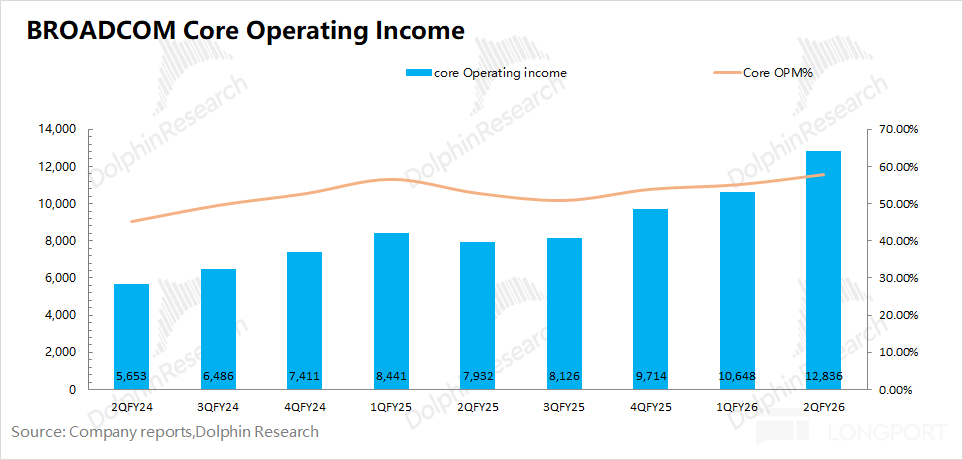

Broadcom (AVGO.O) achieved a net profit of $9.3 billion in the second quarter of FY2026.

When compared to net profit, Dolphin Research holds the view that core operating profit (calculated as gross profit minus R&D expenses and selling and administrative expenses) offers a more accurate reflection of a company's true operational performance. This quarter, Broadcom (AVGO) reported a core operating profit of $12.8 billion, marking a sequential increase of $2.2 billion. This growth was primarily fueled by the expansion of its AI business.

2.5 Broadcom's EBITDA

Given Broadcom's proficiency in external mergers and acquisitions, the company often employs adjusted EBITDA percentage as a key operational metric. Dolphin Research projects that the company's adjusted EBITDA percentage rebounded to 68.7% in the second quarter of FY2026, slightly surpassing the company's guidance of 68%.

Delving deeper into the company's debt repayment capacity, the ratio of total debt to LTM (Last Twelve Months) Adjusted EBITDA continued its downward trend, reaching 1.8 this quarter. Spurred by growth in AI performance, this ratio has now reverted to pre-acquisition levels. Over the past two years, the impact of the company's acquisition of VMware has been fully absorbed, paving the way for the company to potentially embark on new merger and acquisition opportunities.

III. Specific Business Performance: Maintaining 6 Major AI Clients, with Moderate Guidance

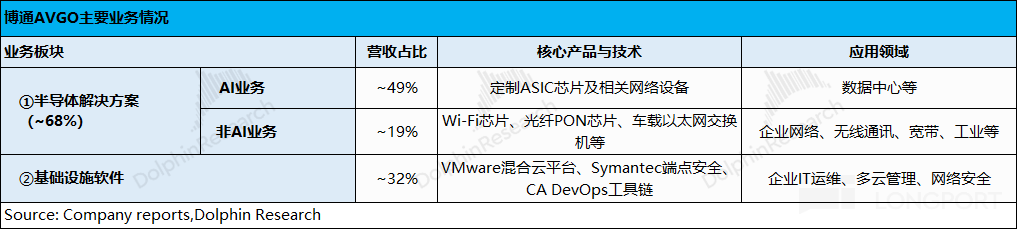

Broadcom (AVGO.O) primarily operates in two main sectors: semiconductor solutions and infrastructure software.

These two broad categories can be further broken down as follows: 1) Semiconductor solutions encompass networking (AI business), wireless, storage connectivity, broadband, industrial, and other segments; 2) Infrastructure software includes VMware, CA, Symantec, Brocade, and more.

3.1 Semiconductor Solutions

In the second quarter of FY2026, Broadcom (AVGO.O) generated $15 billion in revenue from semiconductor solutions, representing a year-over-year increase of 78%. The growth in the company's semiconductor business this quarter was predominantly driven by the AI segment, while non-AI businesses maintained stability.

1) AI Business

The AI business has emerged as the most critical contributor to the company's performance. This quarter, the company's AI revenue reached $10.8 billion, marking a sequential increase of $2.4 billion and accelerating once again. This growth was primarily driven by shipments of Google's TPU.

Currently, the company's AI revenue is derived from three major clients: Google, Meta, and ByteDance. With major companies like Meta increasing their capital expenditures and Anthropic expected to start contributing revenue in the second half of the year, the company anticipates AI revenue of $16 billion next quarter, representing a sequential increase of $5.2 billion. However, this figure falls short of market expectations of $17 billion.

Broadcom's ASIC business had previously announced six clients: Google, Meta, Anthropic, OpenAI, and two others. This quarter, the company's management did not disclose any new clients, maintaining the count at six.

For the full-year outlook of FY2026, the company expects AI business revenue to exceed $56 billion. Regarding AI revenue for FY2027, which is of greater concern to the market, although the company has increased Anthropic's computing power demand to 5GW (up from 3GW), it still maintains expectations of over $100 billion.

While the company subsequently clarified that the $100 billion figure would be easily surpassed, mainstream institutions have generally raised their AI revenue expectations for FY2027 to over $130 billion. The "$100 billion" figure is clearly relatively conservative, and the market is eager for an outlook that exceeds expectations.

On the other hand, in addition to ASICs, the company's AI business also encompasses networking capabilities, which serve as a hidden competitive advantage or "moat." Broadcom's current networking business product line mainly consists of three segments: "switching + routing + optical interconnects," covering Scale-Out, Scale-up, and Scale-Across.

Broadcom's core strategy is to demonstrate, through superior chip performance, that open-source, standardized Ethernet is not only more cost-effective but also more resilient and scalable than InfiniBand in hyperscale clusters.

As we transition into the AI inference phase, it becomes increasingly evident that "AI infrastructure = XPU + storage + connectivity," with connectivity playing an increasingly vital role. While the market currently focuses on the company's TPU/ASIC shipment performance, competitiveness in the connectivity space also has the potential to enhance the company's valuation.

2) Non-AI Business

This quarter, the company's non-AI semiconductor business revenue reached $4.2 billion, representing a year-over-year increase of 6%.

The company's non-AI businesses primarily include enterprise storage, broadband, wireless, and industrial segments, among others. Specifically, revenue from broadband, server storage, and enterprise networking increased year-over-year this quarter, offsetting the seasonal decline in the wireless business. The company expects AI semiconductor revenue of approximately $4.5 billion next quarter, representing a year-over-year increase of 12%.

3.2 Infrastructure Software

In the second quarter of FY2026, Broadcom (AVGO.O) generated $7.2 billion in revenue from infrastructure software, representing a year-over-year increase of 9%. The impact of the previous VMware merger and integration has now been fully absorbed, with future focus primarily on organic business growth.

Broadcom's software business is primarily divided into two parts: VMware and the original software businesses such as CA, Symantec, and Brocade. Since the original software businesses like CA, Symantec, and Brocade maintain quarterly revenues of around $2 billion, the main focus of the company's software business is on the acquired VMware.

According to Dolphin Research, the impact of VMware on the company's performance is mainly twofold: "progress in financial absorption of the merger" and "the full transition from perpetual licenses to a subscription model." Based on the software business performance this quarter, Dolphin Research estimates that VMware generated approximately $5 billion in revenue this quarter.

Considering the company's guidance of $8.9 billion, the company expects VMware and software business growth to accelerate next quarter, continuing to benefit from the increased penetration of the subscription model. With the debt repayment metric now down to 1.8, the acquisition of VMware has been fully absorbed by the company, which will no longer disclose detailed VMware segment data separately. The AI business is now the company's primary focus.

- END -

// Reproduction Authorization

This article is an original piece by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is intended solely for general comprehensive data purposes, catering to the general viewing and data reference needs of users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any individual making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be held liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and data contained in this report are not intended for or proposed for distribution to jurisdictions where distribution, publication, provision, or use of such information, tools, and data would contravene applicable laws or regulations or result in Dolphin Research and/or its subsidiaries or affiliated companies being subject to any registration or licensing requirements in the relevant jurisdiction, nor to citizens or residents of such jurisdictions.

This report solely reflects the personal views, opinions, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) make, copy, reproduce, duplicate, forward, or distribute in any form any copies or replicas, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle