Re-evaluating Unitree: Beyond the Numbers in Financial Reports

06/05 2026

06/05 2026

412

412

Among the pantheon of standout companies, Unitree Technology shines brightly as a beacon of innovation.

On June 1, Unitree made its grand entrance into the capital market.

From filing to listing, the process spanned a mere 66 days, a testament to the company's remarkable prowess.

The enthusiasm surrounding Unitree is palpable.

Firstly, let's consider the investors.

Early adopters included heavyweights such as Dexun, Sequoia, Shunwei, and Matrix Partners.

Later, industry titans like Alibaba, Ant Group, Tencent, Geely, and Meituan, along with state-backed platforms such as Jingguorui, Shanghai Science and Technology Innovation Fund, and Zhongguancun Science City, joined the fray, creating a stellar investor lineup.

Investors are eager to get a piece of the action. In recent years, few companies have garnered such widespread acclaim.

In the capital market, related concept stocks have already seen a surge, with companies like Leader Harmonic Drive, Changsheng Bearing, and Wolong Electric experiencing multiple waves of growth.

Image Source: AI

However, controversies have also emerged as Unitree's products frequently take center stage in performances.

For instance, in March of this year, TSMC's CEO C.C. Wei poured cold water on the hype: 'They just jump around; it looks nice, but that's about it.'

We won't delve into that debate here.

Heiban Jun has observed that assessing the value of AI or robotics companies based solely on traditional financial report data is challenging.

For example, AI company Zhipu's annual revenue pales in comparison to its soaring market value, and the same can be said for Insta360.

In 2025, a wave of embodied robot companies emerged in the domestic market, but Unitree's popularity remains unparalleled.

So, why Unitree? What sets this company apart? How should we evaluate Unitree?

01 Evaluating Financial Reports Within the Sector

For tech-driven companies like Unitree, the valuation approach should shift from a primary focus on financial reports to a broader consideration of the sector.

First, examine the sector's potential, growth stage, and competitive landscape, then use financial data to verify the company's positioning.

Robots are not a new concept; humanity has been exploring their future for nearly a century.

According to economist Joseph Schumpeter's innovation theory:

An entrepreneur's role is to introduce new inventions into the production system; innovation is the first commercial application of an invention.

Humanoid robots, in the public eye, have just transitioned from labs to large-scale commercial applications.

Numerous companies are vying for a piece of the humanoid robot pie. According to incomplete statistics, Unitree faces 107 direct competitors globally from 22 countries.

For example, overseas giants like Tesla and Honda, and domestic players like Zhiyuan, Ubtech, Honor, and XPENG.

Unitree is like the frontrunner after the starting gun, excelling in commercialization.

Firstly, it's the only company that has achieved a closed commercial loop and even profitability.

Image Source: Prospectus

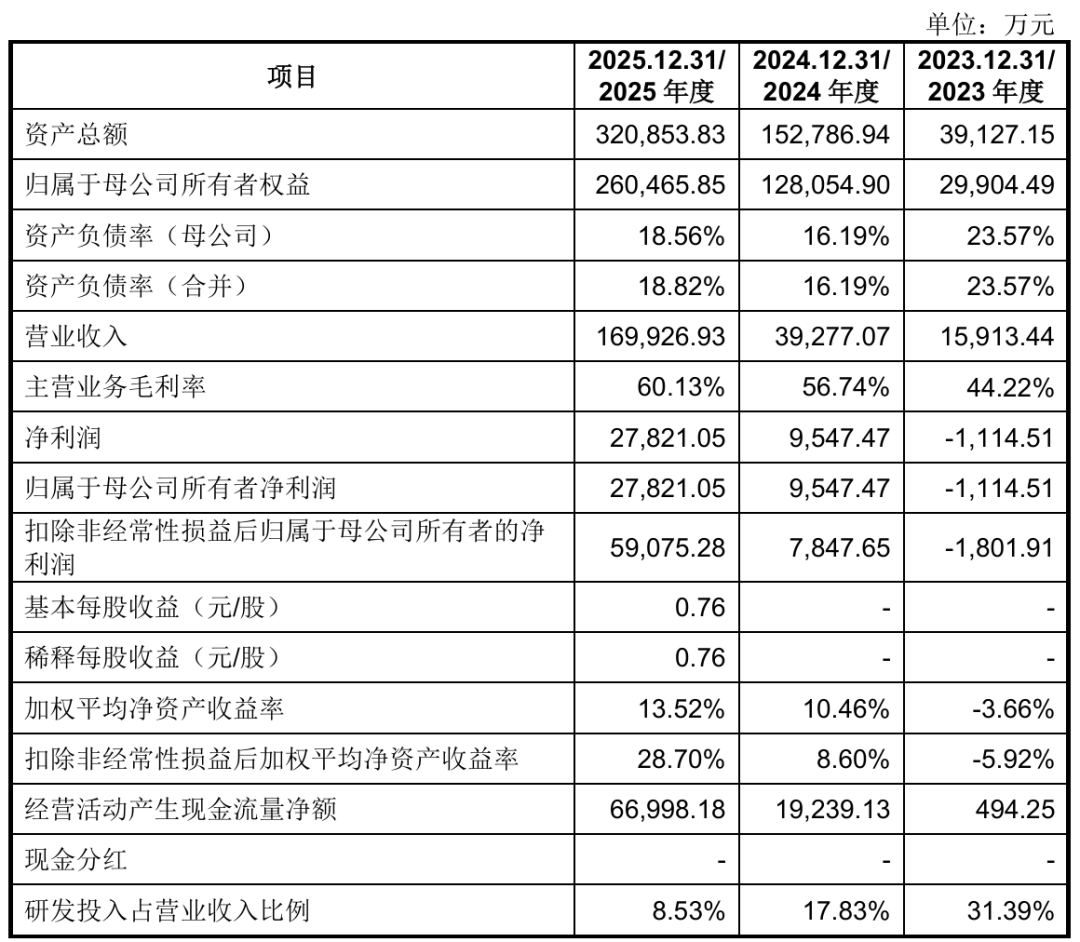

According to the prospectus, Unitree Technology's revenue reached 1.708 billion yuan in 2025, with non-recurring net profit at 591 million yuan and a gross margin of 60.13%.

In comparison, Ubtech, after over two years of listing, reported 2.001 billion yuan in revenue in 2025 but a net loss of 703 million yuan. Tesla, XPENG, and others have yet to begin commercial sales of their humanoid robots.

While most in the sector are burning cash to fuel future growth, Unitree Technology has quietly achieved positive cash flow.

A closer look at the data reveals that from January to July 2025, total revenue from humanoid robots reached 595 million yuan, with 73.6% coming from scientific research and education.

In 2026, its appearance in the Spring Festival Gala catapulted it to fame, sparking global participation in commercial performances by rental companies and opening up new commercialization paths.

Secondly, Unitree Technology's rapid iteration of self-developed technologies has swiftly brought products to market.

From a robot dog that could keep walking after a gentle kick in 2016 to humanoid robots that undergo qualitative changes every Spring Festival Gala.

As product technologies evolve, Unitree Technology's self-sufficiency rate in core components exceeds 90%.

In particular, the cost of its self-developed motors is only about one-third to one-fifth of similar imported products.

Through self-development and co-creation with the domestic supply chain, Unitree Technology continues to highlight China's manufacturing cost advantages while possessing large-scale production capabilities.

In 2025, Unitree Technology shipped over 5,500 humanoid robots, accounting for over 30% of the global market.

The average price of humanoid robots also dropped from 593,400 yuan in 2023 to 166,400 yuan in 2025, with the latest R1 dual-arm humanoid robot starting at just 26,900 yuan.

Image Source: Screenshot from Taobao APP

With rapid technological iteration, self-developed supply chains, mass production capabilities, and low controllable costs enabling price reductions and scale effects, Unitree Technology's commercial flywheel is spinning faster and faster.

Founder Wang Xingxing doesn't just want to build robots; he aims to create the Android or Windows of the robot era.

Unitree Technology holds 262 global patents.

It has begun building a general-purpose robot platform featuring 'standardized hardware + open software + developer ecosystem' and launched UniStore, the world's first humanoid robot app store, witnessing an explosion in global registered developers and the emergence of an ecosystem.

With technology, commercialization, and an ecosystem, Unitree's business model, as seen in its financial reports, has proven viable and laid a solid foundation for future growth.

Indeed, Unitree's rapid revenue and profit growth over the past few years reflect a broader transition from research to commercialization, with potentially vast future market opportunities.

02 Viewing the Sector Through Financial Reports

For companies in traditional, mature industries, we can assess quality through core indicators like revenue, net profit, cash flow, PE, and PB. However, this framework fails to fully capture a company's value in the current cycle of this emerging sector.

Short-term financial losses don't necessarily indicate a lack of technological barriers; stage-specific profitability shouldn't be measured solely by current profits for long-term value.

Static PE ratios ignore the sector's explosive growth potential over the next 5-10 years, akin to measuring an emerging sector with rules designed for mature industries.

Looking deeper at Unitree, financial reports struggle to quantify intangible core assets, such as the future core value of humanoid robots lying in full-stack self-developed algorithms, core technologies for motor reducers, massive real-world training data, landing scenario resources, and global mass production capabilities.

Unitree's self-developed servo motors, reducers, and embodied control algorithms eliminate reliance on externally purchased core components to reduce overall costs. These technological barriers cannot be directly translated into current earnings on the income statement but support future product price reductions and market share gains—values that traditional financial reports cannot price.

Image Source: Screenshot from Taobao APP

However, financial reports do offer some clues, depending on interpretation.

Unitree's gross margin exceeding 60% far surpasses the conventional 25%-35% range for the complete machine manufacturing industry.

This reflects tangible manifestations of technological barriers, with some core critical links stemming from Unitree's full-chain self-development.

Within the logic of the humanoid robot sector, high gross margins indicate the company's ability to sustain price reductions and capture market share:

When future whole-machine price reductions drive volume, competitors will see rapid margin contraction and losses due to externally purchased components, while Unitree can maintain profitability through self-development. The financial report's gross margin data validates the authenticity of technological barriers.

Furthermore, Unitree's future sales potential is evident.

The customer composition in financial reports shows that, besides universities and research institutes, State Grid, local emergency management agencies, and industrial manufacturing enterprises are gradually becoming key clients, with orders shifting from one-time prototype purchases to sustained bulk procurements.

This indicates that dancing performances are merely the prelude. The changing customer structure reflects the sector's transition from experimental trials to industrial necessity, with versatility creating new market spaces.

03 Industrial Pivot

Unitree's value extends beyond just selling robots.

As the most promising industry in the next decade, humanoid robots represent not just a star product but the supply chain supporting it.

Just as Apple nurtured the 'Apple supply chain' and Tesla the 'new energy supply chain,' pivotal companies like Unitree will drive the growth of the domestic robot supply chain while keeping core technologies in-house.

According to the prospectus, over 85% of Unitree Technology's robot components are localized.

Among the hundred-plus global humanoid robot manufacturers, few can achieve bulk shipments and full-stack self-development of core components.

This underlies Unitree's additional value.

Image Source: CCTV Screenshot

Of course, this only explains Unitree's current value, but such optimism doesn't rule out valuation bubbles.

First, continuously monitor Unitree's customer structure.

If scientific research procurements from universities and colleges outweigh industrial and commercial orders, it suggests declining product market competitiveness.

Second, watch for gross margin fluctuations.

A decline in gross margins could indicate either industry price wars or weakening advantages in self-developed technologies.

Finally, assess R&D conversion.

If significant R&D investment post-IPO fails to boost revenue and growth, it suggests issues with technological commercialization.

We must acknowledge that while Unitree Technology shines with various strengths today, it doesn't guarantee ultimate success.

Consider the pioneers of modern computing—MITS, the progenitor of browsers Netscape, 3D graphics card pioneer 3dfx, and home gaming console pioneer Atari—all washed away by time.

Yet, no one doubts their immense contributions to shaping their eras.

Unitree Technology's commercial robot applications remain in scientific research, education, and performance patrols, far from replacing humans in repetitive tasks in factories, cities, and households as depicted in sci-fi films.

Looking ahead, a wave of high-tech companies will enter the capital markets, requiring different valuation approaches.

Financial reports represent a company's current footprints; the sector is its future frontier. However, empty sector narratives without financial substance will ultimately collapse into speculative bubbles.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle