Unitree’s IPO Gets the Green Light: Can It Be the Pioneer of A-Share Humanoid Robot Stocks and Rival Tesla?

06/05 2026

06/05 2026

414

414

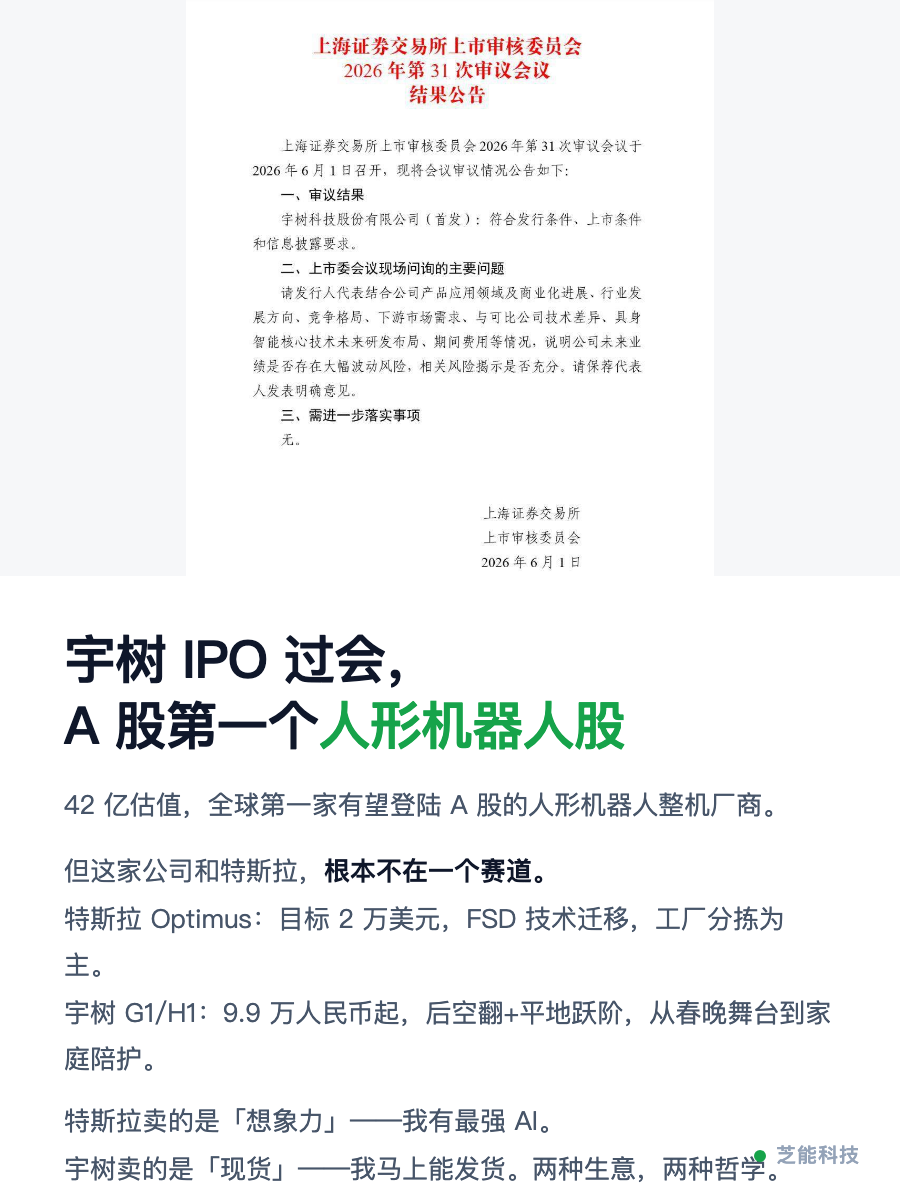

On June 1st, Unitree Technology's Initial Public Offering (IPO) underwent review at the 4th session of the Shanghai Stock Exchange (SSE) Merger and Acquisition Restructuring Committee.

From the acceptance of its application on March 21st to the review on June 1st, the entire process spanned a mere 73 days—a remarkably swift timeline.

With a substantial funding of 4.2 billion yuan, annual revenue of 1.699 billion yuan, and a net profit (excluding non-recurring items) of 591 million yuan, Unitree Technology has successfully introduced pure robotics to the STAR Market.

However, the public's response has been rather intriguing. On social media platforms, the label 'large toy' has resurfaced, often used in a mocking tone.

On Zhihu's trending list, a question inquiring, 'Is Unitree Technology merely exploiting investors?' garnered over 2,000 responses. The most scathing remark in the discussion was: 'A tech company with 1.6 billion yuan in revenue? Isn't that just a toy seller?'

Is this criticism warranted? Partially. But it uncovers a more profound issue: we might fundamentally misunderstand what truly defines a 'real robotics company.'

Tesla, under the visionary leadership of Elon Musk, aspires to construct a 'general-purpose humanoid robot' from scratch. While theoretically flawless, the engineering challenges are immense, with bipedal locomotion, fine manipulation, and full-body coordination still in the developmental stages. Tesla is not lacking in financial resources or talent. In contrast, Unitree Technology adopts a divergent approach.

If Tesla is 'attacking the big cities' (with its focus on general-purpose robots), then Unitree is 'encircling them from the countryside.' From its initial Laikago (a quadrupedal robot dog) to the subsequent Go1 (a consumer-grade robot dog) and finally the Unitree H1 (a humanoid robot), Unitree's strategy has remained consistent: first, introduce a product tailored for a specific niche market.

Unitree's annual revenue of 1.699 billion yuan predominantly stems from industrial inspection orders—replacing manual patrols in substations, factories, and other settings. Its product gross margin remains above 40%, a robust and sustainable figure within any manufacturing sub-sector.

Unitree has also unveiled its proprietary embodied large model, UnifoLM, a vertical model capable of comprehending the physical world and devising action plans.

Without real-world scenarios, there is no data. Without data, there is no large model. China's robotics industry does not need to develop foundational capabilities from the ground up; instead, it can first validate application scenarios and subsequently utilize the resulting data to refine underlying models.

Returning to the harshest criticism: 'Unitree is just a big toy.'

◎ Misconception 1: Dismissing technological depth based on the form of the end-product.

The term 'toy' implies triviality, as if consumer products are inherently low-end. Yet, the consumer electronics industry serves as a crucible for technological intensity. DJI began with 'flying cameras' and now commands the global drone market.

The form of the end-product is never a technological barrier; the true challenge lies in commercializing technology on a large scale. Unitree's robot dog can perform backflips—a feat that demands mechanical design, motion control, and perception algorithms.

◎ Misconception 2: Dismissing imagination based on revenue composition. The value of humanoid robots in industrial settings lies in replacing high-risk jobs—such as high-voltage maintenance, hazardous chemical handling, and mining operations. Unitree now holds the key to a multi-billion-dollar market.

The two companies operate in different industrial phases.

◎ Tesla pursues 'artificial general intelligence,' aiming for disruptive innovation. With the support of the capital market, Unitree can also achieve significant growth. Neither approach is inherently right or wrong—it's merely a matter of priority. Musk chooses to 'reach for the stars,' while Wang Xingxing (Unitree's founder) opts to 'keep feet on the ground.'

Tesla embodies the 'American model': starting from fundamental science, validating technical feasibility, and then seeking applications. This approach offers boundless imagination but entails extremely long commercialization cycles. Optimus has been hyped for three years but remains far from mass production.

◎ Unitree represents the 'Chinese model': starting from application scenarios, achieving commercialization first, and then using profits to fund R&D. This approach ensures healthy cash flow but may limit foundational innovation. Yet, Unitree's UnifoLM proves that China's market is vast enough to support both applications and underlying technologies.

Where will these two models converge?

In addressing the question: 'What specific jobs can humanoid robots replace?' The answer is not 'serving tea' but automating high-risk tasks.

Substation inspections are merely the beginning. Nuclear plant maintenance, deep-sea operations—these are the ultimate battlegrounds for humanoid robots, where humans are reluctant to work.

Ultimately, Unitree and Tesla are pursuing the same objective: liberating humans from dangerous work.

Summary

The 73-day lightning-fast IPO approval and the 4.2 billion yuan in funding reflect recognition of China's robotics industry path: prioritizing engineering, followed by monetization, and then iteration. Sometimes, the 'big toy' is the most formidable player—one that can not only innovate but also sell at scale.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle