Google Borrows Another $80 Billion: Is It a Market 'Refill' or a Bubble 'Touchstone'?

06/05 2026

06/05 2026

523

523

Google (GOOGL.US), a full-stack AI star stock, has seen some weakness in its stock price recently. Amid this, the company announced an additional $80 billion in external funding to be invested in AI infrastructure. Over the past year, Google has raised over $85 billion through bond issuances across six different markets, but this round represents the largest single funding amount.

As for how the funds will be used, the company has provided a general outline: The $80 billion in new capital will primarily be used to expand AI infrastructure capacity, purchase call options to partially hedge against future equity dilution from convertible preferred shares, and cover tax payments related to employee option vesting.

Ultimately, the essence of the fundraising is still directed toward AI investment to maintain smooth cash flow for daily operations. Regarding this financing round, Dolphin Research believes several points are worth discussing:

1. 'Significant Growth' in 2027 Capex: What's the Maximum Budget?

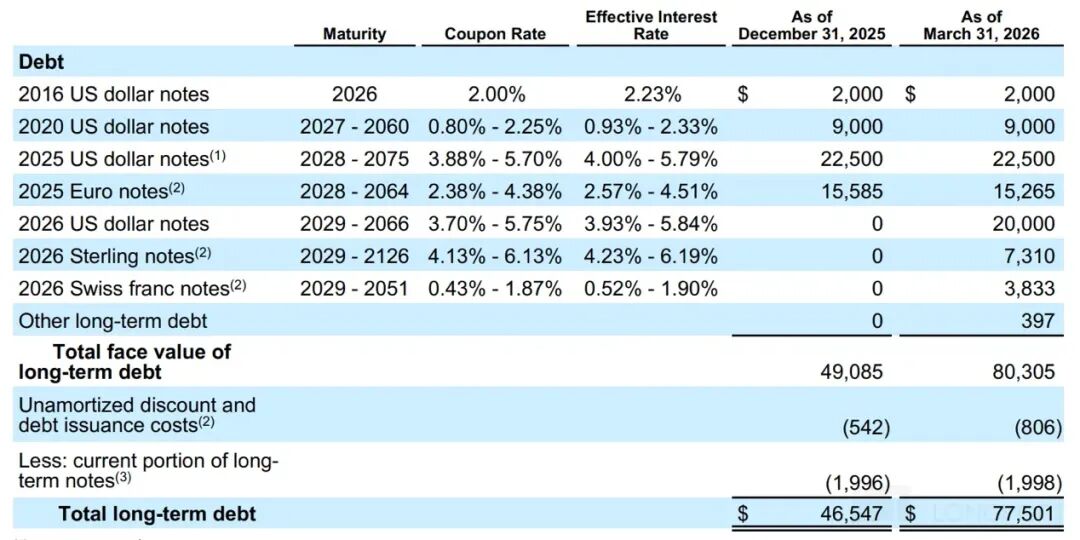

As a giant with quarterly operating cash flow (OCF) of $40-50 billion, $126.8 billion in cash + short-term investments, $25 billion in short-term commercial paper, and $77.5 billion in long-term interest-bearing debt—resulting in $25 billion in net cash under strict standards—the company can theoretically still manage annual CapEx of up to $250 billion.

Unless Google's budget for next year exceeds $250 billion, its reserves will be depleted, making financing urgent. In the Q1 earnings report, management guided a 2026 CapEx target of $180-190 billion and expects 'significant growth' in 2027.

After this $80 billion fundraising, assuming no further financing, the maximum theoretical space available for next year's CapEx is:

2027 OCF of $240 billion (projected 20% growth) + $80 billion fundraising = $320 billion, plus an additional $25 billion in net cash if pushed to the limit, totaling nearly $350 billion in funding. This nearly doubles the 2026 budget.

2. Why Continue to Expand Investment?

It is necessary for Google to increase investment in AI foundational computing power. In the AI giant competition, Google's full-stack AI strategy has paid off, but it has also made enemies on all sides—cloud services (Amazon, Microsoft, and Neocloud); AI chips (NVIDIA, Amazon); large models (Anthropic, OpenAI), as well as AI application scenarios—autonomous driving, where Waymo competes with Tesla.

However, based on current data center investments, Google's planned production capacity still falls short of its ambitious goals. According to SemiAnalysis's end-May statistics (as shown below), measuring data center computing power growth in 2027 based on current progress, Google's new capacity (3GW in 2026, 6GW in 2027) lags behind Amazon's (6GW in 2026, 10GW in 2027), despite accelerating compared to previous years.

Yet Amazon is not as fixated on a full-stack AI strategy. For example, it has not delved deeply into self-developed large models or autonomous driving. Currently, Trainium still lags behind first-tier chip performance, and its signed orders are limited.

Conversely, Google's overall cloud + chip orders in hand are worth $460 billion. Therefore, strategically, compared to Amazon's computing power capacity as a reference, Google still needs to increase its foundational computing power investment.

3. Dilution of Equity Value from $80 Billion Fundraising?

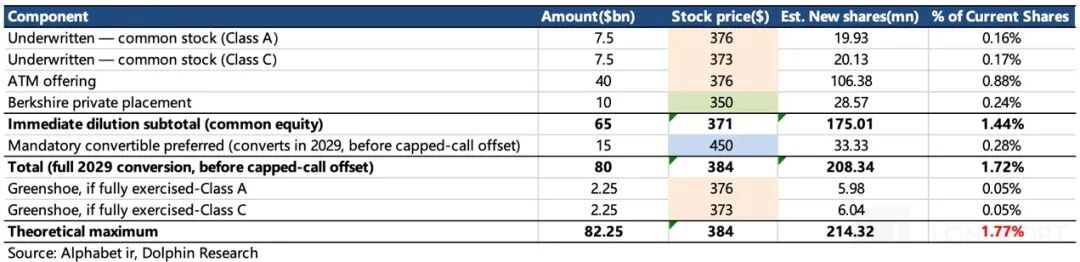

Finally, let's revisit the specifics of the $80 billion financing plan. This funding is divided into three parts:

(1) Ongoing $30 billion follow-on offering + ($4.5 billion over-allotment option): Includes $15 billion in convertible preferred shares (issued in two batches, convertible after three years) and $15 billion in Class A/C common stock follow-on offering. This money is primarily used for AI investment and purchasing call options.

The company granted underwriters participating in the Class A/C common stock offering a 30-day over-allotment option to purchase an additional $2.25 billion in shares. Similarly, underwriters participating in the convertible preferred share offering were granted an equal $2.25 billion over-allotment option, exercisable within 13 days of issuance.

(2) Future gradual implementation of a $40 billion follow-on offering: An agreement has been signed with Goldman Sachs, JPMorgan, and Morgan Stanley to irregularly issue Class A/C common stock at market prices in the secondary market through these brokers starting in Q3 2026.

This money is primarily used for tax withholdings related to employee option vesting. When Google grants equity incentives to employees, it withholds a portion of shares for tax purposes and uses its own cash to pay taxes on behalf of employees. The gradually raised $40 billion can cover this cash gap.

(3) Private placement of $10 billion: Berkshire Hathaway subscribed to $10 billion at a 6.5% discount to yesterday's closing price, comprising $5 billion in Class A shares and $5 billion in Class C shares (Class A has voting rights; Class C does not).

When calculating dilution, for the $15 billion in Class A/C common stock issuance in part (1), we calculate the issuance price based on yesterday's closing price (Class A: $376/share; Class C: $373/share). For the convertible preferred shares, we calculate the conversion price at $450/share (a typical market premium of 20%).

For the $40 billion in part (2), we calculate based on the current price (yesterday's closing price). For part (3), since the issuance price is fixed at $351.8 for Class A and $348.2 for Class C (average $350/share), we use this figure.

As shown below, as of April 22, when Q1 results were disclosed, Google had 5.824 billion Class A + 836 million Class B + 5.456 billion Class C shares, totaling 12.1 billion shares. Under the above financing plan, the immediate dilution ratio is 1.44%. Including potential future conversions, the dilution ratio reaches 1.72%. Adding the two $2.25 billion over-allotments, if fully exercised by brokers, the total dilution ratio reaches 1.77%. Considering the company's simultaneous purchase of call options to hedge, the theoretical total dilution ratio should be less than 1.77%.

4. When Everyone Is on Board...

Last year, several software giants among the 'Magnificent Seven' embarked on multi-billion-dollar fundraising paths. Of course, for these trillion-dollar market cap giants, hundreds of billions in financing individually represent a theoretically low dilution ratio, with minimal impact. In contrast, there may be fewer than a handful of stocks with market caps exceeding $50 billion among Chinese concepts.

The key issue lies in the scale of incremental market capital absorbed. When other giants also start issuing bonds, gradually escalating from $10 billion to $20 billion, then to 'lion's maw' demands of $50 billion to $100 billion, the only entities being siphoned are mid- and small-cap stocks on the AI periphery.

Opinions differ on whether AI investment is a bubble. Both bulls and bears have their reasons. Without delving into whether the industry itself is a bubble, sentiment remains high even as more enterprise clients struggle to justify AI spending.

Admittedly, AI hardware performance and orders are tangible today and for the next 1-2 years, justifying stock price doublings while valuations seem less exaggerated. The critical question is: When even the most cautious investors jump on board, where will incremental capital come from?

As everyone knows, even greater siphoning lies ahead: SpaceX leads next week (latest valuation: $1.8 trillion), Anthropic follows next month (latest valuation: $965 billion), and OpenAI by year-end (latest valuation: $852 billion).

When giant concentration exceeds 1/3 of the $70 trillion U.S. stock market (up 10% from last year, but interest rate expectations do not favor sustained incremental attraction), accommodating three additional multi-trillion-dollar giants will bring deeper reshuffling and contraction:

On one hand, more assets outside the final circle will become abandoned 'blood bags.' On the other hand, after extreme sentiment reverses, some capital will seek high-to-low rebalancing.

- END -

// Republication Permission

This article is an original work by Dolphin Research. Republication requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general viewing and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, product preferences, risk tolerance, financial status, or special needs of any recipient. Investors must consult independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referencing the content or information in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses arising from the use of data in this report. The information and data in this report are based on publicly available sources and are for reference only. Dolphin Research strives for but does not guarantee the reliability, accuracy, or completeness of this information and data.

The information or viewpoints mentioned in this report shall not, under any jurisdiction, be construed as or deemed an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, solicitations, or endorsements of relevant securities or related financial instruments. The information, tools, and data in this report are not intended for or designed for distribution to jurisdictions where distribution, publication, provision, or use of such information, tools, or data contradicts applicable laws or regulations or subjects Dolphin Research and/or its subsidiaries or affiliates to registration or licensing requirements in those jurisdictions, nor to citizens or residents of such jurisdictions.

This report reflects only the personal viewpoints, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, with copyright solely owned by Dolphin Research. Without prior written consent from Dolphin Research, no institution or individual may (i) reproduce, copy, duplicate, reprint, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all related rights.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle