Alarming! Net Profit Plummets to Zero. What’s Going On with the Tech Giant, AI狂龙战士 (AI Crazy Dragon Warrior)?

06/05 2026

06/05 2026

514

514

This marks the 1,331st original article from 'New Energy Frontier'. Click 'New Energy Frontier' above to follow and 'star' our account. This article solely reflects the opinions of 'New Energy Frontier' and does not constitute investment advice. The author does not manage investment groups, charge for stock tips, or handle client funds.

--------

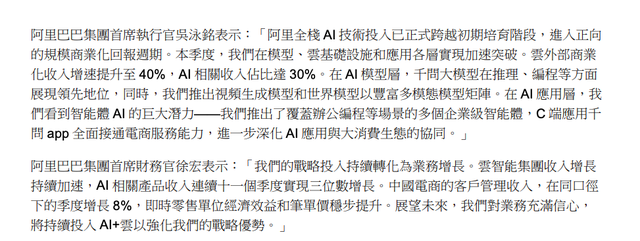

Revenue reached RMB 243.38 billion, up 3% year-on-year. Non-GAAP net profit was a mere RMB 86 million, marking a staggering 100% year-on-year decline, nearly hitting zero. Adjusted EBITA dropped 84% year-on-year to RMB 5.102 billion, with a quarterly operating loss of RMB 848 million, compared to an operating profit of RMB 28.465 billion in the same period last year.

These are Alibaba's latest quarterly results, which have left many stunned. However, the actual operating situation isn't as grim as the numbers suggest and warrants a detailed discussion.

That said, Alibaba is a company that seems straightforward to analyze but is, in reality, quite complex.

Contradictory, isn't it? It indeed is, but hold your judgments for now. Let Leo elaborate.

01 Forging Ahead on the AI Frontier

Previously, when tracking Alibaba, 'New Energy Frontier' discussed its challenges and opportunities. The issue lies in the escalating competitive pressure on its core e-commerce business, with no signs of the competitive landscape improving in the long run. All the company can do is focus on its 88VIP membership program to retain loyal users. Additionally, the company's AI investments have been overly aggressive. If it ultimately fails to achieve a commercial closed loop, the company may end up with little to show for its efforts. However, on the flip side, the AI technological wave is indeed distinct from the internet era. Once Alibaba leads in AI and achieves a commercial closed loop, the outcome could be vastly different.

Based on the facts, it's clear that Alibaba has chosen to forge ahead in the AI race, a decision reaffirmed by its Q1 report.

The above is the opening summary of the Q1 financial report. To be honest, after reading it, one might feel puzzled. What kind of company is Alibaba? An e-commerce company? Or an AI-centric company? The entire summary is brimming with AI references, with e-commerce mentioned only once, and even then, it was as a hidden reference related to Qianwen.

Since Alibaba positions itself as an AI company, let's assess how its AI business is faring.

Regardless, the data alone looks impressive. At least given the current market's focus on AI, these figures are sufficient to justify the company's previous aggressive investments in AI. This is precisely why, after the financial report was released, the secondary market surged by nearly 8 points at one point.

02 No Issues with the MaaS Strategy

The dire financial report and the secondary market's leniency suggest that Alibaba will continue to forge ahead in AI. The commercial closed loop is primarily achieved through the Token economy, namely MaaS (Model as a Service).

First, let's address whether this strategy is flawed: It is not!

When we previously tracked Google's Q1 2026 financial report, we already mentioned that Google's performance proved that the model-as-a-service path is viable. The correct approach to leveraging cloud computing services is to utilize large models, integrate various service capabilities, and package them for sale to customers. Only then can high prices be justified. This is particularly crucial for Chinese cloud service companies, as evidenced by Alibaba's disclosed AI-related business growth.

Alibaba Cloud's EBITA margin has hovered around 9% for the past four quarters. The management's long-term goal is 20%, or even over 30%. Regarding the Token economy, Alibaba has already revamped its organizational structure and established the Alibaba Token Hub business group, directly overseen by Wu Yongming, to advance related work.

However, the MaaS business model faces a fundamental issue: Unless computing power prices drop significantly, this business model, unlike the internet, does not have zero marginal costs, making it difficult to achieve strong economies of scale. Moreover, it lacks obvious differentiation, as customers choose large models based on their capabilities, resulting in minimal network effects.

Additionally, since large models are still evolving, Alibaba will need to continue making high-intensity investments in this area. This aligns with Alibaba's official plans. Since proposing the 'RMB 380 billion' investment plan in February 2025, Alibaba has already invested a cumulative RMB 126.063 billion over the past year. Management recently stated that the investment cycle will be extended to around five years, and the investment amount will far exceed previous expectations.

Is aggressive investment a mistake? It's too early to tell. The key question is when will the investment break even? This can only be verified later.

03 When Will the Relentless Expansion Cease?

For Alibaba, the awkward situation is that its core e-commerce business is under continuous pressure, and its instant retail operations are still in the investment phase. In other words, the company is currently expanding in multiple directions, facing tremendous pressure.

Its core e-commerce business faces fierce competition from Pinduoduo, Douyin E-commerce, and Video Account E-commerce. Over the long term, Alibaba does not possess stronger competitive advantages compared to these rivals. It lacks price advantages over Pinduoduo and traffic advantages over Douyin and Video Account E-commerce. Therefore, Alibaba's current strategy is to leverage its 88VIP membership program to firmly bind and serve these loyal users.

However, from Leo's personal experience, the long-term competitive dimension of retail still hinges on price. Although the number of 88VIP members continues to grow, it does not necessarily mean that Alibaba's e-commerce foundation is secure, as many people may join for the 88VIP benefits but still shop based on price.

Taobao and Tmall are currently Alibaba's bedrock. If this foundation crumbles, services like Alipay, Cainiao, Xianyu, 1688, and Hema will become rudderless.

Alibaba still needs to continuously prove its ability to defend Taobao and Tmall's market position and demonstrate its competitiveness in the e-commerce sector.

The same goes for flash sales. Objectively speaking, although Alibaba's foray into flash sales has been controversial, from 'New Energy Frontier's' perspective, we firmly endorse this strategy. Despite ongoing losses, Alibaba's market share has indeed risen, and user stickiness appears promising based on grassroots research and market share trends.

Although the synergy between flash sales and the overall e-commerce market is not immediately apparent, this is not a flaw in flash sales but rather an issue with Alibaba's e-commerce foundation. As long as Taobao and Tmall can stabilize, especially by matching Pinduoduo's pricing, the synergy will gradually materialize.

Furthermore, flash sales are trending toward positive unit economics (UE) through scale and algorithmic optimization. According to Jiang Fan, there is confidence in achieving positive UE before the end of the new fiscal year. If true, this would be one of the biggest boons for Alibaba. However, whether Meituan will allow this remains to be seen. From a personal standpoint, I do not believe the instant retail war will end quickly.

Alibaba's logic is quite simple: several key questions remain. When will Taobao and Tmall's core business truly stabilize? When will the AI investments break even, or at least show a trend toward doing so? When will flash sales become self-sustaining?

This is what was meant at the beginning by saying that analyzing Alibaba is both straightforward and challenging. It is straightforward because the key factors determining its performance in the secondary market are the questions listed above. It is challenging because none of these questions currently have definitive answers.

Based on the Q1 report, one can only say that things have not worsened and may even show a slight positive trend. However, whether this improvement can continue remains unclear and can only be determined through continued observation.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle