Marvell: In the AI Inference Era, Is Connectivity More in Demand Than Computing Power?

06/05 2026

06/05 2026

558

558

On May 28 (Beijing Time), after the market closed, Marvell Technology (MRVL.O) released its financial results for the first quarter of fiscal year 2027 (as of April 2026):

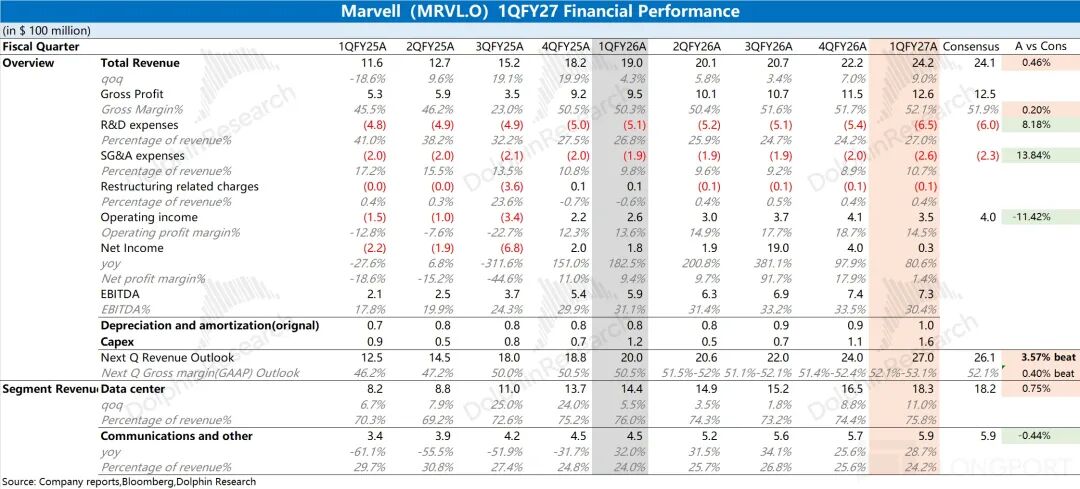

1. Revenue: In this quarter, revenue reached $2.42 billion, up 9% from the previous quarter, meeting market expectations of $2.41 billion. The $200 million quarter-over-quarter increase was mainly driven by growth in the data center business.

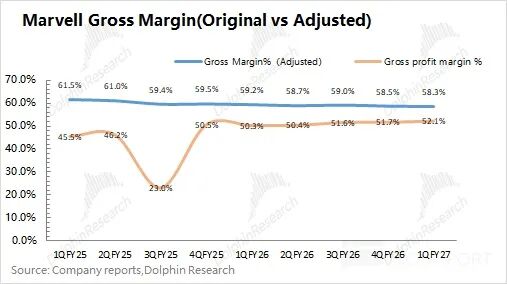

2. Gross Margin: The gross margin for this quarter was 52.1%, up 0.4% from the previous quarter. However, due to the impact of amortization from acquired assets on the company's gross margin, the figure reported in the financial report does not directly reflect operational performance. After excluding this impact, the adjusted gross margin, as referenced by Dolphin Research, was 58.3%, down 0.2% from the previous quarter. Affected by lower-margin businesses such as custom ASICs, the gross margin still showed a declining trend.

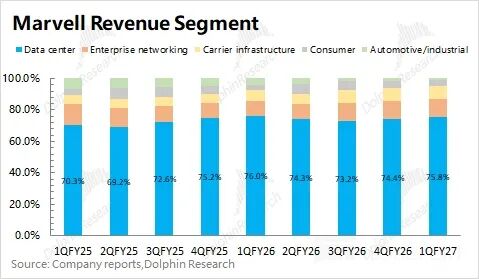

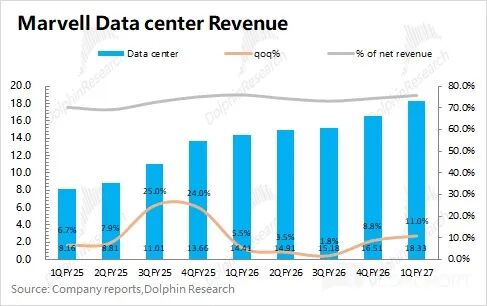

3. Data Center Business: This is a key focus for the market. Revenue in this quarter was $1.83 billion, up 11% from the previous quarter, mainly driven by growth in optical interconnect products. The data center business accounted for 75.8% of total revenue this quarter.

Previously, the market's focus on the company's AI business was primarily on custom ASICs. However, Marvell's performance in Amazon's Trainium products was relatively weak. Although the company still provides Trainium 2.5 chips for Amazon, its newly released Trainium 3 chips are mainly supplied by Alchip, which also suppressed the company's stock performance at that time.

As we enter the AI inference phase, the importance of computing power significantly decreases, while major players place greater emphasis on capabilities in storage, CPUs, and interconnects. Marvell already has relatively leading products in the interconnect market. Even with the recent sluggish performance of ASICs, strong demand for interconnect products will ensure high growth in the company's performance.

4. Next Quarter Guidance: Revenue is expected to be $2.7 billion, better than market expectations of $2.61 billion, with quarter-over-quarter growth primarily driven by increased demand for interconnect products. The gross margin (GAAP) is expected to be 52.1%-53.1%, remaining relatively stable.

5. Full-Year Outlook: The revenue outlook for fiscal year 2027 has been raised to $11.5 billion (previous guidance: $11 billion), representing a 40% year-over-year increase. This is mainly due to an upward revision in the growth rate of interconnect products to over 70% (previous guidance: 50%+), with ASIC growth exceeding 20% (maintained). The revenue outlook for fiscal year 2028 has been raised to $16.5 billion (previously $15 billion), representing a 43% year-over-year increase.

Dolphin Research's Overall View: Betting on the AI Super Cycle, Interconnects Drive Growth

The company's financial results this time largely met market expectations, with revenue growth primarily driven by the data center business (interconnect products). After excluding the impact of amortization, the company's adjusted gross margin was 58.3%, down 0.2% from the previous quarter.

The company adjusted its business disclosure metrics last quarter, consolidating its business into two segments (data center, and communications and others) from the original five. The data center business was the primary growth driver this quarter, with an 11% quarter-over-quarter increase. ASIC performance was relatively weak this quarter, with growth mainly driven by demand for interconnect products.

Marvell expects revenue to reach $2.7 billion next quarter, up 11% from the previous quarter, better than market expectations of $2.61 billion. Given that management provided full-year guidance, the importance of next quarter's guidance is reduced.

The company's stock price has surged recently, primarily due to significant changes in its "narrative logic." Previously, the market was mainly concerned about the loss of Trainium market share, progress in 1.6T DSP mass production, and competition from Broadcom (AVGO). However, under the current optical super cycle, even with relatively weak performance in custom ASICs, the company's interconnect products (such as DSP chips) can still drive certain high growth in performance.

After entering the AI inference phase, it becomes clearer that "AI infrastructure = storage + XPU + connectivity." Marvell already has relatively leading optoelectronic connectivity products and has enhanced its AI networking capabilities through a series of acquisitions. Mainstream market institutions have already raised their performance expectations for the company, and management's upward revision of revenue guidance for fiscal years 2027/2028 to $11.5 billion/$16.5 billion, respectively, largely meets market expectations.

Beyond the financial data, Marvell's "growth" highlights include:

1) Rack-Level Networking Capabilities: The company's recent acquisitions of XConn (PCIe/CXL switching), Celestial AI (photonic interconnects), and Polariton (silicon photonics) have given it complete capabilities across the three major AI networking layers: Scale-Out, Scale-Up, and Scale-Across. This allows the company to offer customers a full suite of high-speed interconnect hardware from within racks to across data centers.

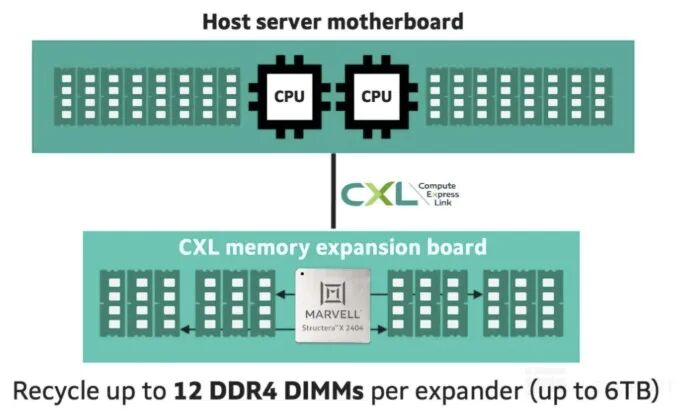

2) CXL Memory Expansion/Pooling (Structera): This is not actually used for "storing data" but rather adds a layer to the memory hierarchy where data runs. Currently, in the AI inference phase, massive KV Cache is required. HBM is too expensive, and DRAM is not large enough, necessitating the use of NAND/storage-class memory expansion.

Marvell's layout in CXL memory expansion and pooling mainly includes three categories: Structera A, Structera X, and Structera S, which serve as near-storage accelerators, memory expansion controllers, and memory pooling and switching functions, respectively.

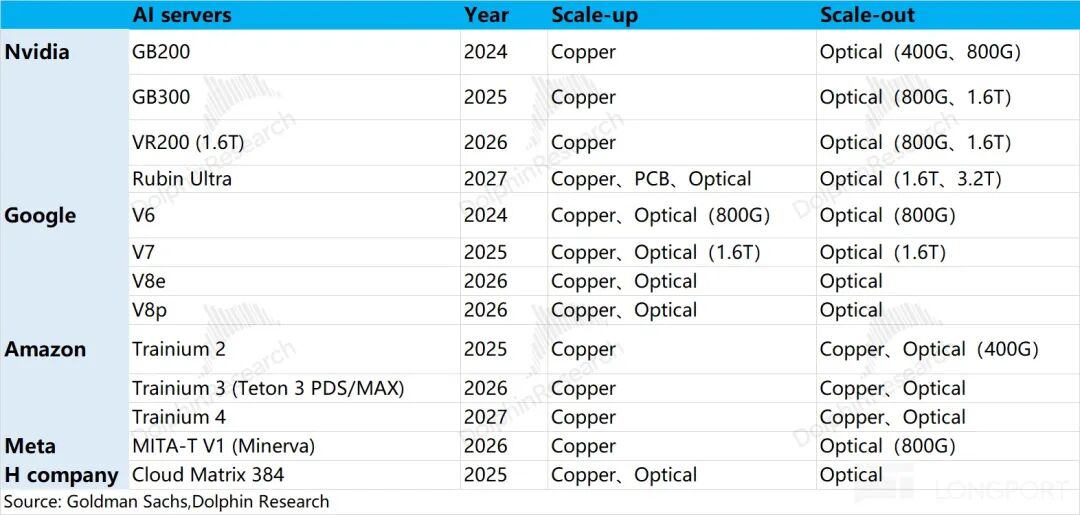

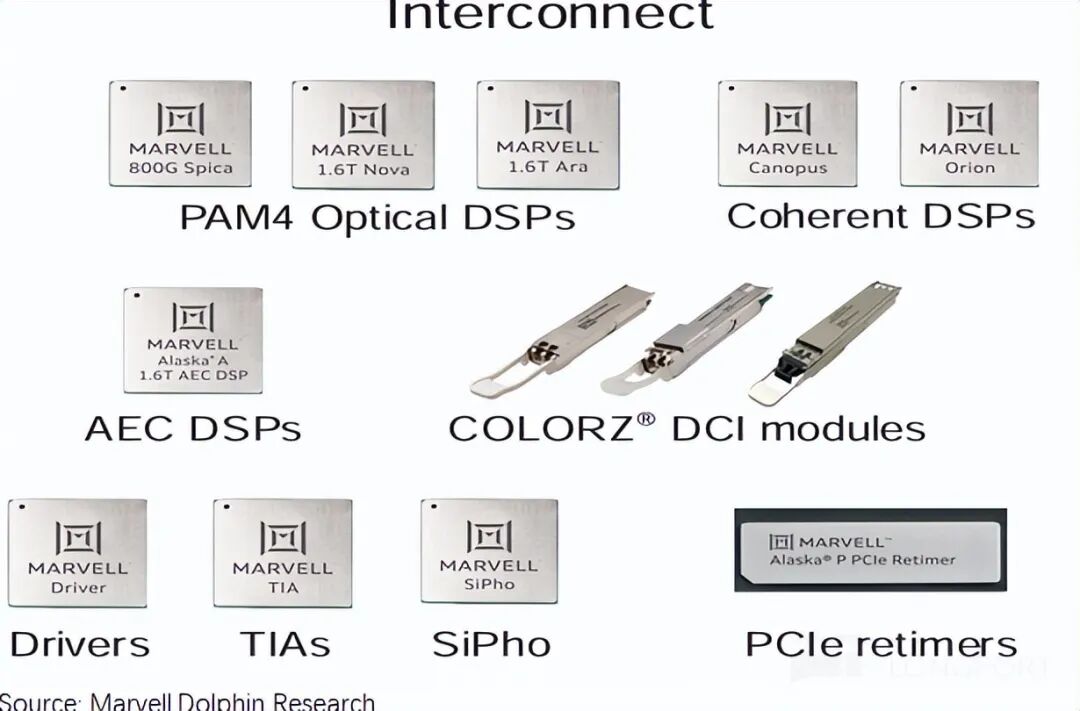

3) Full-Stack Optical Interconnect Capabilities: Regarding morphological changes in the connectivity field, from "copper cables → pluggable optical modules (relatively leading in PAM4 DSP) → LPO/OBO (on-board optics) → CPO (co-packaged optics) → all-optical interconnects," Marvell has technological layouts at each stage.

In the current Scale-Out optical interconnect scenario, traditional pluggable optical modules remain the absolute mainstay. Major players like NVIDIA and Google primarily use pluggable optical module solutions, with CPO solutions expected to see small-scale adoption in the second half of 2026.

Marvell's PAM4 DSP is relatively leading in the pluggable optical module market. Company management previously mentioned that "1.6T solutions have begun mass production and will rapidly ramp up in fiscal year 2027," which will be a major growth driver for the company's interconnect products in the near term. Beyond DSPs, Marvell has also made technological layouts in LPO/OBO, CPO, and all-optical interconnects.

In terms of the company's financial results this time, performance was relatively "average." Since the company provided full-year guidance, the importance of quarterly performance is diminished. Regarding the full-year guidance, the revenue outlooks for 2027/2028 largely meet the raised expectations of mainstream analysts.

The company's relatively high PE reflects excessive market expectations. The annual guidance provided by the company did not bring more "surprises," which may leave the market slightly "disappointed" in the short term.

Under the new guidance, the company's growth rate is expected to remain above 40% over the next two years, still reflecting sustained high growth. Beyond interconnect products, the company's ASIC business, CXL memory expansion/pooling (Structera), and rack-level solutions provide mid-to-long-term imagination space. Even if the annual guidance is "relatively plain," the company's "high-growth" narrative logic remains intact.

Here is a detailed analysis:

I. Marvell Technology's Business

Marvell Technology started with storage technology and subsequently expanded its business through a series of "external M&A" efforts. The data center business has become the company's largest revenue source.

Specific business details:

1) Data Center Business (~75%): A high-growth business driven by demand for data centers and ASICs, it is currently the market's primary focus. The business includes optoelectronic interconnect products, SSD controllers, custom ASICs (such as customized chips for Amazon AWS and Google Axion CPU), primarily used in cloud servers, edge computing, and other scenarios.

2) Other Businesses (~25%): The company has consolidated "enterprise networking, carrier infrastructure, consumer, automotive + industrial" into a "communications and others" segment.

II. Core Data: Connectivity Heats Up, Revenue Growth Accelerates

2.1 Revenue

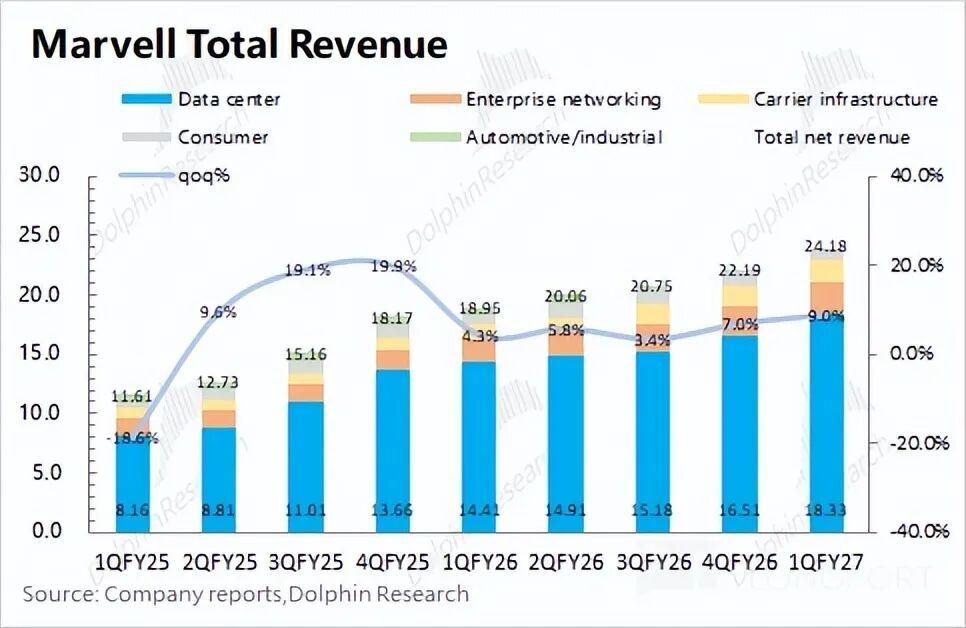

Marvell Technology achieved revenue of $2.42 billion in the first quarter of fiscal year 2027, up 9% from the previous quarter, meeting market expectations of $2.41 billion. The company's revenue growth this quarter was primarily driven by growth in optoelectronic interconnect products.

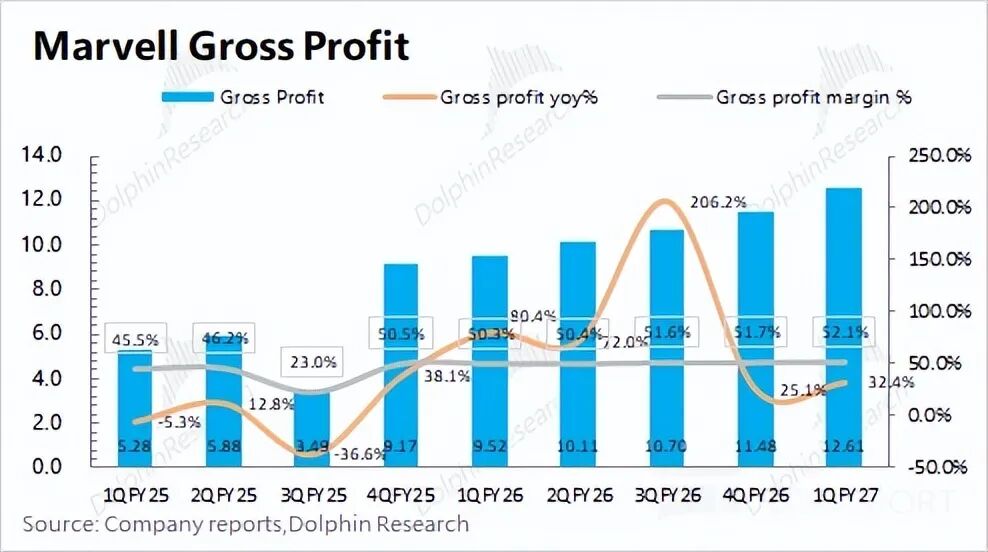

2.2 Gross Profit

Marvell Technology achieved a gross profit of $1.26 billion in the first quarter of fiscal year 2027, up $110 million from the previous quarter. The gross margin for the quarter was 52.1%.

Due to the impact of amortization from acquired assets on the company's gross margin, the figure in the financial report does not directly reflect operational performance. After excluding this impact, the adjusted gross margin, as referenced by Dolphin Research, is considered.

The company's adjusted gross margin for the quarter was 58.3%, down 0.2 percentage points from the previous quarter. Affected by lower-margin businesses such as custom ASICs, the gross margin still showed a declining trend.

2.3 Operating Expenses and Profit

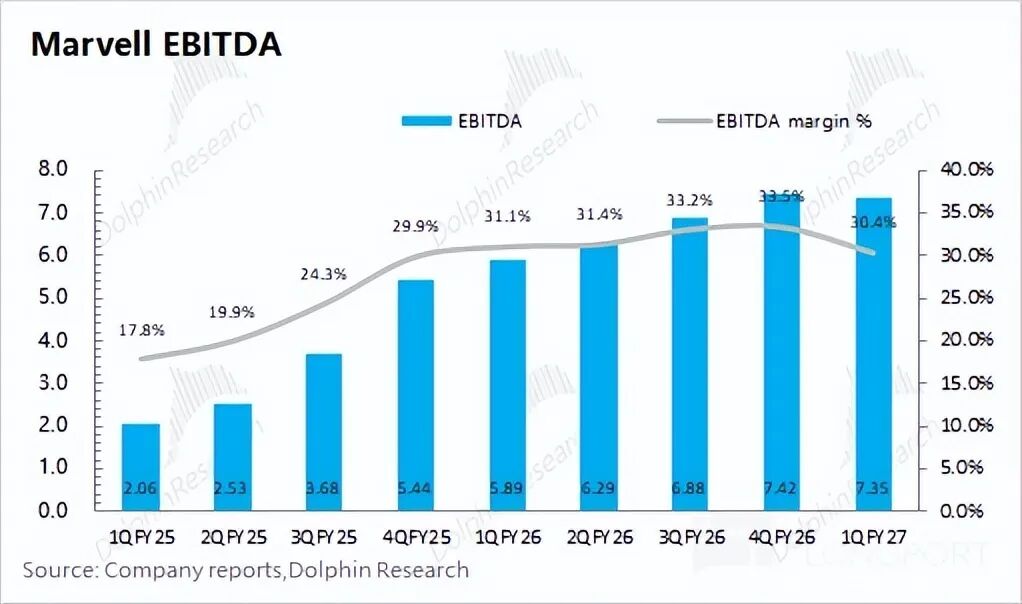

Marvell Technology achieved a net profit of $35 million in the first quarter of fiscal year 2027.

Excluding non-recurring factors, from an EBITDA perspective, the company's EBITDA for the quarter was $735 million, with the EBITDA margin falling to 30.4%, mainly due to the decline in the adjusted gross margin and a significant increase in operating expenses.

III. Business Performance: High Growth in Interconnect Products, "Growth" Highlights Abound

Since 2018, Marvell Technology has successively acquired companies such as Cavium and Innovium, enhancing its capabilities in connectivity and ASICs. Driven by demand for interconnect products and custom ASICs, the company's data center business has shown an upward trend and is the biggest influence on its performance.

The company began to categorize its traditional businesses uniformly as Communications and Others starting last quarter, with revenue contributions from enterprise networks, operator infrastructure, consumer electronics, and automotive and industrial sectors all declining to around or below 10%.

3.1 Data Center Business

Marvell achieved revenue of $1.83 billion in its data center business for the first quarter of fiscal year 2027, representing an 11% sequential increase and aligning with market expectations of $1.82 billion. This growth was primarily driven by demand for optoelectronic interconnect products.

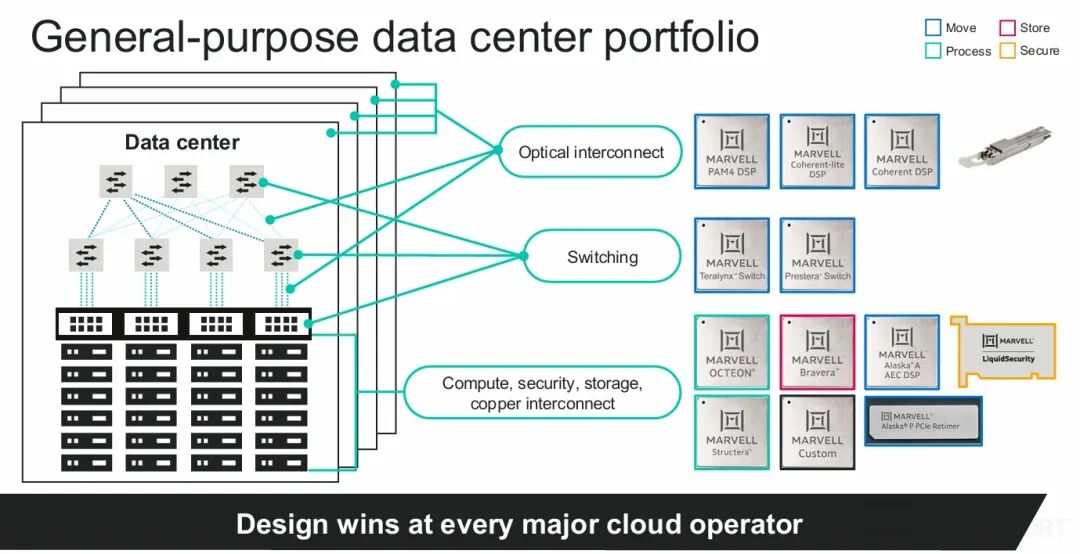

Within Marvell's data center operations, the current business focus lies primarily on interconnect products and custom ASIC solutions.

1) Custom ASICs: Amazon's Trainium is currently the largest product

Marvell continues to supply Amazon with Trainium 2.5 products, but Amazon's latest Trainium 3 offerings will primarily be provided by Alchip. This shift is the main reason for the recent weaker performance in the company's ASIC business.

Regarding the outlook for custom ASICs, the company maintains modest expectations for fiscal year 2027, projecting an annual growth rate of only 20% (significantly lower than the capital expenditure growth rate of CSPs). This projection reflects the company's loss of market share with a major client (Amazon).

However, the company has provided

As artificial intelligence (AI) advances into the inference phase, the significance of the "AI infrastructure equation—storage + XPU + connectivity" has become more pronounced, complementing the role of computing power. Currently, pluggable optical modules remain the predominant method for achieving scale-out, and the company's PAM4 DSP stands as a leading product in this domain. The company has also implemented technological advancements across various areas, including copper cables, LPO/OBO, CPO, and all-optical interconnects.

The company's decision to upwardly revise its revenue guidance for fiscal years 2027 and 2028 is primarily attributed to robust demand in the interconnect sector. It anticipates that interconnect business revenue will surge by over 70% year-on-year in fiscal year 2027 (up from the previous guidance of 50%+) and will maintain rapid growth in fiscal year 2028.

3) Other Growth Drivers:

① Data center switch chips: Following the acquisition of Innovium, the company has further solidified its competitive edge in the Ethernet switch market. Its Ethernet switch-related revenue reached approximately $300 million in fiscal year 2026 and is projected to exceed $600 million and $1 billion in fiscal years 2027 and 2028, respectively, driven by AI demand.

② Comprehensive network layer capabilities: The company's recent acquisitions of XConn (PCIe/CXL switching), Celestial AI (photonic interconnects), and Polariton (silicon photonics) have endowed it with complete capabilities across the three major AI network layers: Scale-Out, Scale-Up, and Scale-Across. This enables the company to offer customers a comprehensive suite of high-speed interconnect hardware solutions, spanning from within racks to across data centers.

③ CXL memory expansion and pooling: The company's primary layouts include three categories: Structera A, Structera X, and Structera S, which function as near-storage accelerators, memory expansion controllers, and memory pooling and switching solutions, respectively.

Through a series of strategic acquisitions, Marvell has established a robust presence across Scale-Out, Scale-Up, and Scale-Across. The company is not merely selling individual chips but is focused on creating integrated solutions.

Marvell has also deepened its collaboration with NVIDIA, encompassing: (1) optical cooperation (extending the long-term supply of DSP, TIA, and drivers to silicon photonics, empowering scale-up networks); (2) NVLink Fusion integration (Marvell's custom chips and network semiconductors seamlessly interface with NVIDIA infrastructure, providing hyperscalers with the flexibility to mix and match); (3) AI-RAN (enhancing collaboration between OCTEON base station processors and NVIDIA GPUs, enabling operators to concurrently run 5G/6G and high-performance AI applications on the same software-defined platform).

During the current AI inference phase, connectivity capabilities are assuming increasing importance. This not only drives short-term performance enhancements but also fuels market expectations for the company's long-term sustained growth. At this juncture, interconnect products are poised to contribute the most significant growth to the data center business, with long-term prospects in ASICs, CXL memory expansion/pooling (Structera), and rack-level solutions.

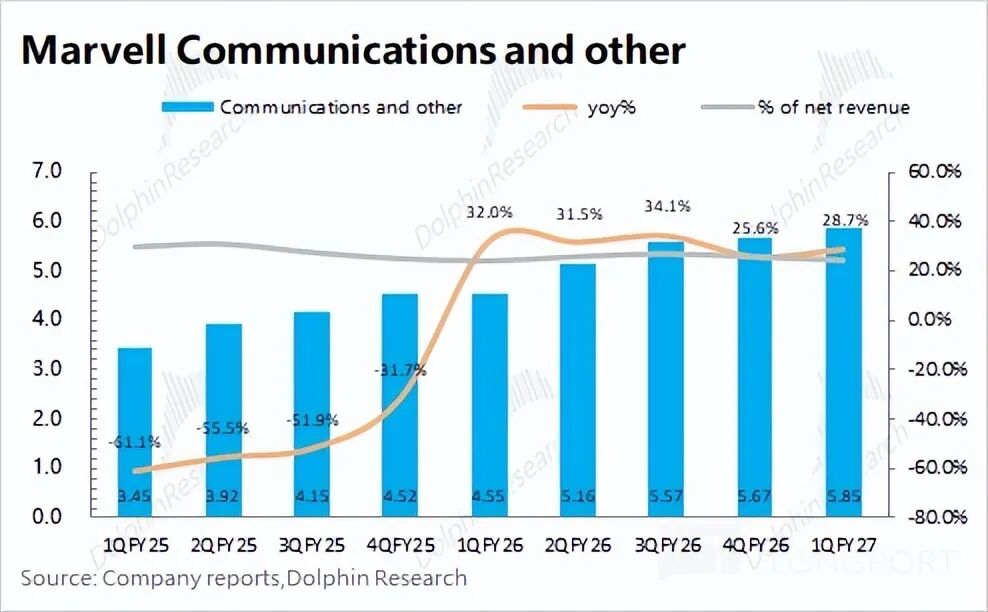

3.2 Communications and Other Business Segments

The company has restructured its business disclosure categories this quarter, reporting only Communications and Other Businesses without further segmentation into enterprise networks, operator infrastructure, consumer electronics, and industrial sectors.

Marvell reported revenue of $585 million in its Communications and Other Businesses for the first quarter of fiscal year 2027, marking a 28% year-on-year increase. With accelerated growth in the data center segment, the proportion of Communications and Other Businesses has contracted to 24%.

For Communications and Other Businesses, the company maintains its annual outlook: approximately 10% growth in fiscal year 2027 and low single-digit growth in fiscal year 2028.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires explicit authorization.

// Disclaimer and General Disclosure

This report is intended solely for general informational purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial status, or particular needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report assumes all associated risks. Dolphin Research shall not be held liable for any direct or indirect responsibilities or losses that may arise from using the data contained in this report. The information and data in this report are based on publicly available sources and are intended for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of the information and data.

The information or viewpoints mentioned in this report shall not, under any jurisdiction, be considered or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and data in this report are not intended for or prepared for distribution to jurisdictions where such distribution, publication, provision, or use of the information, tools, and data conflicts with applicable laws or regulations, or where it would require Dolphin Research and/or its subsidiaries or affiliates to comply with any registration or licensing requirements in such jurisdictions, or to citizens or residents of such jurisdictions.

This report reflects only the personal viewpoints, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and its copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle