Oracle’s Stellar Performance Drops by 10%—Is AI Turning into a Real Estate Venture?

06/12 2026

06/12 2026

365

365

On the morning of June 11th, Oracle, a key player in the AI sector, unveiled its financial report. The figures for the last fiscal quarter were striking: both earnings per share (EPS) and revenue surpassed expectations, the cloud business expanded by 93%, and backlog orders soared to $638 billion. Yet, the market reacted with a 10% drop, shocking the bulls. Wall Street's reasoning stemmed from another set of figures: Oracle's capital expenditures are projected to hit $56 billion next year and $70 billion the following year, with an extra $40 billion in borrowing, pushing free cash flow into the red.

The market's worry isn't whether Oracle can turn a profit, but whether it's turning into an "AI utility company"—drowning in orders but earning every dollar through massive infrastructure investments, ultimately becoming as crucial yet unprofitable as a power plant.

An X user, DD, provides a vivid analogy: AI isn't the internet; it's real estate. Oracle's current predicament resembles a property developer aggressively acquiring land, amassing pre-sale permits, but needing to buy two more plots for every unit sold, straining cash flow. The entire AI industry's rapid growth essentially mirrors Evergrande's high-turnover strategy: maximizing capital efficiency through rapid development, high leverage, and quick sales, prioritizing speed above all else.

This trend isn't unique to Oracle.

Data indicates that in 2026, the combined capital expenditures of Microsoft, Google, Amazon, and Meta are expected to exceed $700 billion, up nearly 80% year-on-year, with most funds directed towards AI data centers, GPU clusters, networking equipment, and power infrastructure. This expansion no longer relies solely on operational cash flow but heavily on external financing. Amazon recently secured a $17.5 billion syndicated loan and issued approximately C$14 billion in bonds in Canada to fund AWS and AI infrastructure growth; Google (Alphabet) launched its largest-ever equity financing plan totaling $80 billion, shunning traditional debt financing.

Real estate developers once relied heavily on borrowing; now tech giants do the same. While Xu Jiayin's empire survived on bank loans and buyer pre-payments, tech giants tap into market capital. They all discuss AI factories, which, like traditional factories, require land, energy, machinery, and emission pipelines—the only difference being AI factories need fewer workers. Over the past three years, Microsoft, Oracle, Google, and Amazon have behaved like developers: financing, acquiring land, building data centers, purchasing GPUs, laying networks, and leasing computing power.

Real estate sells square meters; AI factories sell teraflops. A developer's core competence is leverage—using others' money to buy land and profiting from price hikes. AI developers? They borrow hundreds of billions to fill racks with servers and sell computing power. Assuming AI applications explode and tokens are in short supply, computing power pricing will skyrocket, enabling AI developers to reap huge profits. Oracle's RPO backlog in its financials represents its "land bank"—impressive numbers indeed.

The allure of internet businesses lies in near-zero marginal costs—coding once serves 100 million or 10 million users at similar costs. AI isn't like that. Each additional user consumes more tokens, necessitating the advance construction of larger AI factories to meet escalating demand. Hence, tech giants have become the world's most aggressive infrastructure builders, frantically borrowing to pour money into data centers.

This has been my consistent argument.

The internet adheres to "Metcalfe's Law": network value scales with the square of users. No phones? No need for networks. The more WeChat users, the more valuable it becomes. Facebook, TikTok, Taobao—all internet applications thrive on network effects, where user growth increases per-user value while marginal costs approach zero, creating a virtuous cycle.

Thus, internet giants expand rapidly via "scale first," monetizing through ads, value-added services, and e-commerce once user scale crosses a threshold. AI reverses this: user growth complicates ad models (users reject AI results as ads), while computing power, storage, and bandwidth become scarcer with more users, raising token costs despite scaling. Scale, cost, and experience form a new impossible trinity in AI.

Doubao exemplifies this. ByteDance aggressively promoted it with an excellent user experience, but soaring computing costs forced a paid professional version to segment users. Sora, the video model pioneer, opened to the public but burned tokens faster than printing money, quickly shutting down.

Successful AI models like Claude and SeeDance rely on subscriptions, prioritizing quality over user scale, serving few paying users well to charge premium prices. OpenAI abandoned daily active user (DAU) targets after realizing free users contributed little; platform degradation drew backlash as user experience worsened with scale—a vicious cycle. Thus, scale is no longer an advantage in AI business models; it's a hindrance.

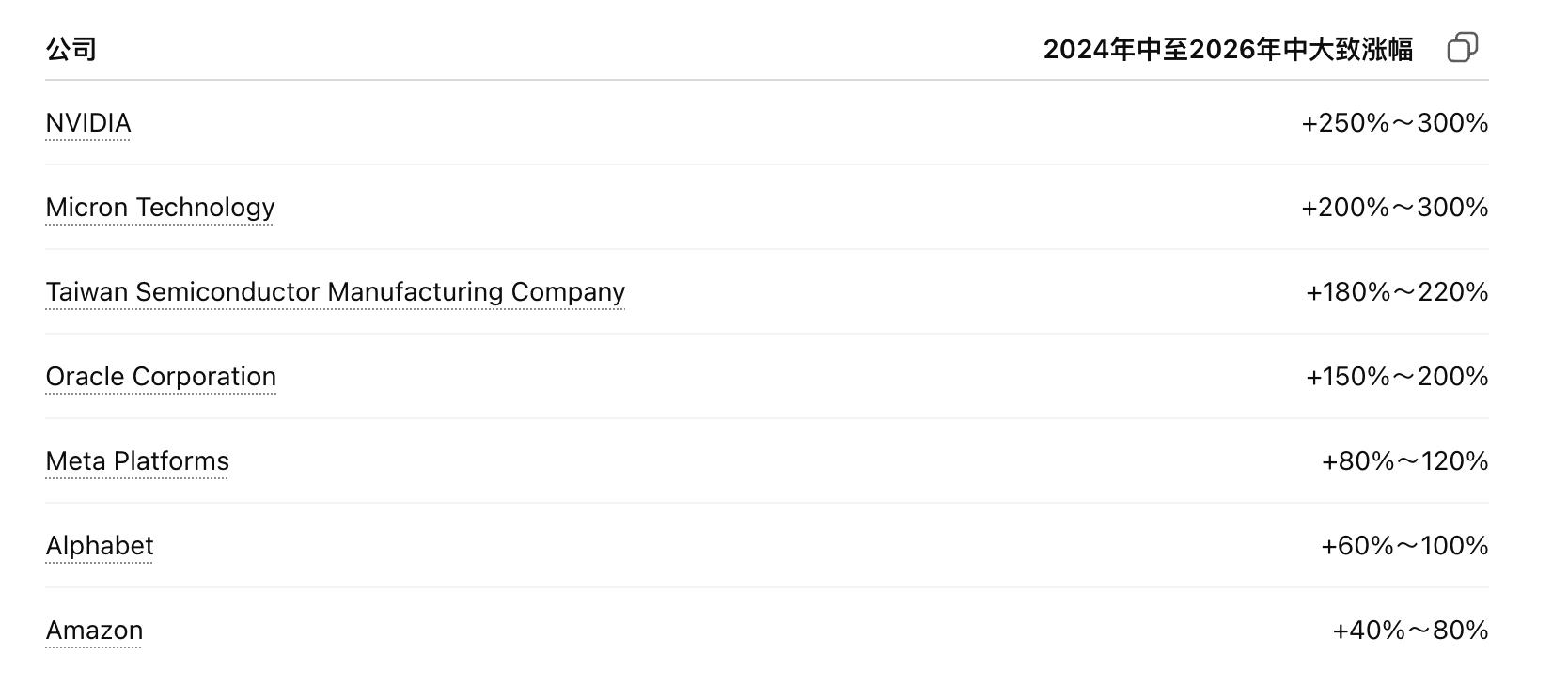

In real estate cycles, the biggest profits go to Sany Heavy, Anhui Conch, and Oriental Yuhong—not developers. The AI supply chain mirrors this: ASIC chips, storage, optical modules, liquid cooling, servers... Among Nvidia's "five-layer AI cake," upstream infrastructure suppliers profit first. Multiple trillion-dollar companies emerged in two years, with Nvidia becoming the world's first $5 trillion company by market cap, while developers like Google bear interest costs and demand risks. Shovel sellers just need to innovate and count money.

Over the past two years, Nvidia, Micron, and TSMC surged 2–4 times, while Google, Meta, and Amazon lagged.

(Source: ChatGPT)

Real estate has slumped in recent years. The fate of Xu Jiayin's cohort was inevitable as the industrial cycle ended: high-leverage land acquisitions, debt rollovers, perpetually tight cash flow, and asset prices that, once stagnant, made interest payments lethal. Supply-demand mismatches exacerbated this—prime locations remained scarce while third-tier cities drowned in inventory.

Could AI repeat this script? Uncertain, but caution is warranted. Leading cloud providers race to build data centers, snapping up "prime location" resources like power, land, and network bandwidth. Asset depreciation risks loom: GPU iteration cycles hit 18 months. Today's $30 billion H100 purchase may become obsolete within two years. Real estate debt crises stemmed from "short-term borrowing for long-term assets"—using short-term loans to fund illiquid assets, triggering chain collapses when refinancing failed. Oracle's $40 billion borrowing and Microsoft/Google's steeper capital expenditure curves have prompted market re-evaluations of their debt ratings.

Another player type avoids building infrastructure, instead renting computing power to develop AI models and sell tokens—akin to Hilton or HaiDiLao. The upside is asset-light operations without billions in capex; the downside is paying hefty "computing infrastructure taxes," with most profits (if any) siphoned upstream.

The sweet spot in AI ecosystems is being a "developer": leveraging existing computing power or even open-source models to create blockbuster applications like Manus. Small teams can build billion-dollar companies this way.

Why did Tencent's stock surge on unreleased WeChat AI rumors? Because WeChat epitomizes this "developer" model: with billions of users, social graphs, mini-program ecosystems, and payment closures, it merely needs to integrate AI into chats, Moments, and video feeds to monetize tokens—an asset-light AI developer approach.

-

WeChat’s AI Evolution: Tencent’s High-Stakes Gamble

-

![]()

How did the dot-com bubble burst 26 years ago?

-

![]()

Tencent is a Mirror Reflecting Alibaba's Dilemma

-

![]()

Global Robotaxi Race Steps into Mass Production Phase

-

618 Battle Report | Weekly 3C Digital Rankings (June 1-7)

-

![]()

52,500 Square Meters: Weina Xingkong’s New Headquarters to Rise Here→

-

![]()

AI Pet Language Translator Priced at 799 Yuan: Whose Mind Can It Read?

-

![]()

Following First Loss in 70 Years, Honda Veterans Unite to Demand CEO's Resignation, Citing Three Major Failures! They Directly March into Headquarters to Demand His Dismissal