The Decline of Scarcity Premium: A Transformation in Valuation Logic for China's AI Industry

06/23 2026

06/23 2026

340

340

The first cohort of pure large-scale AI model companies listed in Hong Kong has witnessed significant valuation corrections. Zhipu (02513.HK) and MiniMax (00100.HK) have seen their market values retreat notably from their peaks following their successful initial public offerings (IPOs). As market enthusiasm wanes, investors are no longer willing to pay a premium solely for "scarce listed assets." The domestic large-scale AI model industry has formally bid adieu to the era of parameter-driven narratives and scarcity premiums, with valuation benchmarks now firmly shifting towards commercialization capabilities, control over compute costs, and sustainable cash flow. The investment fervor that once mirrored the bull markets in the internet and new energy vehicle sectors is now being thoroughly reshaped by rational fundamental pricing.

Earlier this year, Zhipu and MiniMax made their debuts on the Hong Kong Stock Exchange, instantly sparking the initial frenzy reminiscent of China's domestic internet and new energy vehicle sectors. As the first batch of independent large-scale model companies to enter the secondary market, their scarcity value was amplified by investors, leading to a short-term doubling or even tripling of their share prices. Zhipu reached a high of HK$725 on February 20, with MiniMax hitting HK$970 on the same day. By May 29, Zhipu's stock price soared to an all-time high of HK$1,993, with its peak market capitalization surpassing HK$880 billion; MiniMax's market cap also briefly exceeded HK$300 billion during the same period. At that time, the market widely believed that domestic large-scale AI models had entered a window for capital revaluation, with scarce listed assets expected to command long-term valuation premiums.

However, the euphoria was short-lived. After reaching their zenith, market expectations swiftly reversed, triggering sustained and significant corrections in both stocks. Since then, the combined market capitalization of the two companies has shrunk by hundreds of billions of Hong Kong dollars. The sharp decline in their stock prices was not merely due to a single wave of capital outflows but rather a fundamental shift in the underlying market pricing logic: the scarcity premium that had propelled their earlier high valuations was rapidly dissipating, and investors began to objectively assess the true operational value of large-scale model companies. Long-standing issues, such as compute costs, monetization efficiency, and persistent losses, were now laid bare.

I. The Collapse of Scarcity Premium Logic: Supply Expansion Diminishes Asset Scarcity

The core foundation of this valuation bubble was the scarcity of independently listed large-scale AI model companies in Hong Kong. For an extended period, leading domestic large-scale model companies with complete self-developed capabilities had refrained from listing on the secondary market. Zhipu and MiniMax, as the first to list, became the only tradable pure AI large-scale model assets, with their scarcity directly driving price-to-sales ratios to astronomical levels.

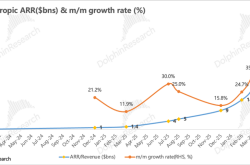

However, several short-term factors have completely dismantled the scarcity narrative. Firstly, the global supply of AI listings continues to expand, with overseas companies like Anthropic and OpenAI secretly filing for IPOs, planning to go public within the year. Mature overseas AI companies now provide clear valuation benchmarks, with their proven commercialization, controlled losses, and stable annual recurring revenue (ARR) starkly contrasting with the persistent large losses of domestic companies, thereby undermining the rationale for high multiples. Secondly, the domestic window for large-scale model listings has also opened, with several industry leaders initiating applications for Hong Kong and STAR Market listings, significantly increasing the future supply of AI assets on the secondary market and eroding the scarcity status of individual companies. Thirdly, cloud providers and internet giants continue to open up their self-developed large-scale models, with Baidu, Alibaba, and Tencent leveraging their proprietary compute power and customer channels to capture the B-end market, narrowing the technological differentiation barriers of independent large-scale model companies and diminishing the valuation premium based solely on self-developed capabilities.

Under these multiple supply shocks, investors have begun to reprice the true value of "scarcity." The capital market now recognizes that scarcity merely represents short-term trading opportunities and cannot conceal long-term operational weaknesses, marking the end of an era where valuation premiums were solely derived from listing status.

II. The Compute Cost Black Hole: High Losses Undermine the Basis of High Valuations

The rigid cost of compute power is the most fundamental constraint suppressing large-scale model valuations and a core driver of the recent sharp stock price corrections. Overseas companies like Walmart, Amazon, and Meta have already implemented measures such as setting usage caps, eliminating internal competitions, and cutting third-party platform expenditures to strictly control unnecessary internal AI compute consumption. In contrast, domestic pure large-scale model companies face even greater compute cost pressures.

Internet platforms enjoy a natural advantage of marginal costs approaching zero, where larger user bases continuously dilute unit operational costs. However, the large-scale model industry operates in the opposite manner: each model training session and every round of user inference generates rigid expenses such as GPU hardware depreciation, electricity, and bandwidth. Higher usage leads to linearly increasing costs without any economies of scale. Financial reports from the two companies reveal a persistent loss loop driven by cost pressures. In 2025, Zhipu reported annual revenue of RMB 724 million with an adjusted net loss of RMB 3.182 billion; MiniMax reported annual revenue of approximately RMB 560 million (US$79.038 million) with an adjusted net loss exceeding RMB 1.7 billion (US$250 million), with the bulk of these losses stemming from compute procurement and high salaries for top algorithm talent.

Commercialization at the enterprise level has also struggled to offset cost pressures. MiniMax focuses on C-end entertainment AI products, where massive user bases drive high inference expenses, but C-end payment willingness remains low, and user retention is volatile, resulting in a 25.4% gross margin in 2025. Zhipu primarily targets B-end MaaS services, with impressive API revenue growth, but industry-wide token pricing competition has driven down unit monetization efficiency, far below that of overseas leading models. On one side are ever-expanding compute expenses, and on the other, slow-growing, low-margin revenue and persistently negative cash flow—all of which have raised market doubts about the long-term rationality of hundredfold valuations.

Overseas cost-control strategies also provide a reference for the secondary market: Walmart, Amazon, and Meta manage enterprise AI expenditures by setting AI usage caps, distinguishing between high- and low-cost models, and eliminating meaningless compute consumption. In contrast, domestic independent large-scale model companies must continue investing in trillion-parameter model iterations while bearing massive user inference costs, creating a dual burden that pushes profitability far into the future and leaves high valuations without fundamental performance support.

III. Valuation Framework Reconstruction: From Narrative Hype to Three-Dimensional Fundamental Pricing

With the fading of scarcity dividends, a new valuation framework for China's AI industry has taken shape, where investor pricing no longer focuses on parameter scale, funding backing, or listing timing but instead on three core dimensions: revenue, costs, and cash flow.

Firstly, revenue quality has become the primary benchmark. The market no longer chases revenue growth alone but distinguishes between sustainable B-end standardized revenue and one-time custom project revenue. Standardized API and enterprise long-term subscription ARR revenue offer compounding benefits and can stably cover compute costs, while fragmented custom projects have long payment cycles and low marginal returns, making them unsuitable for long-term growth. Zhipu's higher proportion of B-end standardized services has resulted in a 41% gross margin, significantly higher than MiniMax's 25.4%, reflecting market pricing differentiation based on revenue structure and margin preferences.

Secondly, compute cost control capabilities have become a core competitive moat. Future industry competition will shift from "who has the stronger model" to "who can provide equivalent services at lower compute costs." Companies capable of self-developing lightweight models, building proprietary compute clusters, optimizing inference scheduling, and matching high- and low-compute models will receive long-term valuation premiums. Those that continue to consume compute power recklessly and fail to control unit token costs will face sustained valuation discounts.

Thirdly, cash flow health determines the valuation ceiling. The model of relying on large-scale financing to sustain operations is unsustainable, as the primary market financing environment tightens and the July 2025 Hong Kong lock-up expiration peak approaches, placing pressure on Zhipu, MiniMax, and other stocks from existing shareholders looking to sell. Investors now prioritize companies with self-sustaining potential, narrowing losses, and steadily improving operational cash flow, while those entirely dependent on financing will face sustained valuation pressure.

Comparing with mature overseas AI company valuation frameworks, the median P/ARR valuation multiple for global AI listed companies is approximately 20-25x, whereas Zhipu and MiniMax reached over 100x at their peaks. As valuations normalize, the market is gradually closing the valuation gap between domestic and overseas companies, squeezing out the high-premium bubble.

IV. Long-Term Industry Implications: AI Transitions Beyond Expansionary Growth into a Value-Verification Phase

The sharp retraction in Zhipu's and MiniMax's market values does not negate the long-term development potential of domestic large-scale models but rather signals a shift in the industry's development stage. In the previous two years, the industry was in a crucial phase, where investors were willing to pay a premium for technological imagination and sector scarcity. Now, as the industry enters the deep waters of commercialization, technological gaps continue to narrow, and the market demands verifiable operational results from companies.

For the industry, the era of extensive money-burning to stack compute power and parameters is over. All large-scale model companies must now establish cost awareness and balance technological investment with commercialization. C-end entertainment AI products need to optimize payment systems and reduce inefficient compute consumption, while B-end service providers must deepen vertical industry expertise, create high-margin standardized solutions, and rely on scalable revenue to offset rigid compute costs.

For secondary market investors, the trading logic of hyping AI concepts and betting on scarce listed assets has completely failed. Future investments in domestic large-scale model companies will require penetrating through technological narratives to focus on genuine profit potential, compute cost control capabilities, and long-term customer value, abandoning short-term thematic speculation.

From a macro industry perspective, domestic large-scale models remain a core sector of the digital economy with certain long-term growth potential, but the pace of capital returns will significantly slow. The short-term valuation dividends driven by scarcity are gone for good. Only leading companies that truly achieve a balance between technology, costs, and commercialization will receive long-term stable premiums under the new valuation framework.

Conclusion

From a peak market capitalization exceeding HK$1 trillion to a 40% contraction in just two weeks, the stock price volatility of Zhipu and MiniMax represents a crucial value recalibration in China's AI capital market. When scarce listed assets are no longer a universal logic for investor speculation, and compute costs, commercialization capabilities, and cash flow become the core pricing factors, it signifies that the industry has officially bid farewell to bubble-driven hype and entered a rational, sustainable high-quality development phase. In the future, domestic large-scale model companies will no longer compete on who lists first or who has larger parameters but on who can truly transform AI technology into stable profits and find a long-term balance between compute costs and commercial returns.

Source: Investor Network

-

Three-Year Cumulative Losses Reach 4.4 Billion! Can AI Revolutionize Yonyou’s Future?

-

![]()

Zhipu: Trillion-dollar Market Cap, Is China's Anthropic Really Here?

-

![]()

Why Are Automakers Hesitant to Offer Consumer Guarantees?

-

![]()

Targeting 12 Million in Exports! China’s Auto Industry Faces a Pivotal Test of Maturity

-

![]()

One in Six Employees at Volkswagen Faces Layoffs Amidst Largest Strategic Retrenchment in 88 Years

-

![]()

Breaking Free from Involution: How These Four Automakers Are Charting New Courses

-

![]()

From National Pride to WPS Controversy: The Dilemma Faced by Zou Tao of Kingsoft Office

-

![]()

He Xiaopeng: Ant Group's 'AI Visionary'