Ranked First in Shipments, but Lagging in Valuation: The 'Dexterous Hand Paradox' of InTime Robot

07/02 2026

07/02 2026

333

333

Produced by | He Xi

Layout by | Ye Yuan

In my previous article, I dissected 'Lingxin Qiaoshou,' valued at 40 billion yuan. Today, let’s examine 'InTime Robot,' the leader in shipments.

Previously, we dissected Lingxin Qiaoshou’s 40 billion yuan valuation—a premium from the capital market for the certainty of being a 'shovel seller,' a valuation of the technological barriers of the 'impossible trinity,' and a vote of confidence in the strategic ambition of being the 'Anthropic of the physical world.' After that article was published, a recurring question from the industry arose: Who is the dexterous hand enterprise with the highest shipments, and how much is it worth?

The answer is InTime Robot—in 2025, its annual deliveries of dexterous hands exceeded 10,000 units, firmly securing its position as China’s leader in dexterous hand shipments. However, its valuation was dramatically surpassed by Lingxin Qiaoshou, which ranked second in shipments.

Thus, a 'dexterous hand paradox' emerges: Why does the enterprise with the highest shipments fail to rank in valuation?

Founded in 2016, InTime has been quietly working in the dexterous hand sector for seven years; Lingxin Qiaoshou was established in 2023, riding the wave of humanoid robots. One proved over a decade that 'dexterous hands can be mass-produced,' while the other demonstrated in two years that 'dexterous hands can be sold at a premium.' This is no coincidence. It reflects how the capital market prices two entirely different business logics—pricing for 'certainty' versus pricing for 'imagination.' InTime represents the former, while Lingxin Qiaoshou represents the latter.

As the second article in the 'Dexterous Hand Series,' this piece will dissect InTime Robot’s 'dexterous hand paradox' from three dimensions: shipments, valuation, and competitive landscape—how did it achieve first place in shipments? Why doesn’t the capital market offer a premium to the 'shipment king'? And can this paradox be resolved?

01 Ranked First in Shipments: A Decade of Perseverance, 10,000 Units Delivered

InTime Robot’s top position in shipments wasn’t achieved by riding a trend—it was built unit by unit.

In 2025, InTime Robot delivered nearly 10,000 five-fingered dexterous hands in a single year—a figure that marks the first time in the nearly 20-year commercial history of dexterous hands. Fang Hainan, CMO of InTime Robot, described this steep growth trajectory with a set of numbers: from 2016 to 2023, over nearly seven years, the company delivered fewer than 1,000 dexterous hands in total, with a single-year high of no more than 300-400 units. In 2024, shipments nearly reached 2,000 units in a single year, which the team already considered 'incredible.' When planning for 2025 at the end of 2024, the team’s most optimistic forecast was 4,000 units, but the actual deliveries approached 10,000 units—five times the previous year.

In 2026, InTime Robot set a shipment target of 30,000 to 50,000 dexterous hands—a goal explicitly disclosed by CMO Fang Hainan on multiple public occasions. The company’s current annual production capacity for dexterous hands exceeds 50,000 units, with supporting capacity for micro servo cylinders reaching over 500,000 units. Its new factory in Suzhou will open next month, with production capacity expected to rise to more than four times the current level.

InTime didn’t achieve first place in shipments by luck—it relied on full-stack self-research.

InTime’s most fundamental technological barrier is the micro servo cylinder—the core driving unit of the dexterous hand. This finger-sized component integrates a motor, reducer, lead screw, sensors, and a servo drive controller, all developed through full-stack self-research. 'It’s like fitting an elephant into a matchbox.' The micro servo cylinder solves the challenges of miniaturization, high power density, and mass production of actuators—'without this module, dexterous hands couldn’t be made small enough, nor could they achieve low-cost mass production.'

InTime is one of the few full-stack self-research enterprises in the industry, with its own front-end factory and assembly center. 'The motors, reducers, sensors, and drive controls inside are all truly self-developed, not just integrators of dexterous hands.' From 2016 to 2019, the team repeatedly refined the first-generation micro servo cylinder and dexterous hand prototype. In 2020, it launched China’s first commercially available mass-produced dexterous hand, reducing the price from the million-yuan level to tens of thousands of yuan, truly filling a domestic gap. The company is now a national 'Little Giant' enterprise specializing in innovation.

In 2025, InTime’s dexterous hand customer base grew fivefold year-on-year, covering nearly 700 enterprises. Its client list includes leading humanoid robot manufacturers such as Unitree, Zhiyuan, and Ubtech. Products have been exported in bulk to Europe, North America, Japan, South Korea, Southeast Asia, and other global regions. During the 2026 Spring Festival Gala, InTime’s F1 series dexterous hands appeared in the sketch 'Grandma’s Favorite'—the first dexterous hands to ever feature on the gala.

GGII data shows that InTime Robot ranks first in China for dexterous hand shipments. In 2025, China’s dexterous hand market sold approximately 19,200 units, with InTime accounting for more than half.

InTime Robot’s first-place shipment ranking is the result of a decade of technological accumulation and production capacity ramp-up. It isn’t an opportunist riding a trend but a 'long-termist' ahead of the industry’s explosion. The problem, however, is that the capital market values 'long-termism' far less than 'trend-driven imagination.'

02 Valuation Lagging Behind: Why Doesn’t the Capital Market Offer a Premium to the 'Shipment King'?

Being first in shipments doesn’t equate to being first in valuation. The valuation gap between InTime and Lingxin Qiaoshou reveals starkly different pricing logics in the capital market for the dexterous hand sector.

In the first quarter of 2026, financing for dexterous hand-related enterprises reached nearly 5 billion yuan, nearly 70% higher than the total for all of 2025. Capital is flooding into this sector at an astonishing rate. But the money isn’t flowing evenly.

Lingxin Qiaoshou has completed seven rounds of financing, reaching a valuation of 3 billion USD (approximately 20.5 billion yuan), with its next funding round targeting a valuation of 6 billion USD (approximately 41 billion yuan)—a dramatic lead over the other five leading enterprises. What does 6 billion USD mean? Unitree Technology’s valuation after its Sci-Tech Innovation Board IPO was around 42 billion yuan. Lingxin Qiaoshou’s target valuation is approaching Unitree’s post-IPO market cap.

InTime Robot, meanwhile, has completed two rounds of financing (C1 and C2), raising several hundred million yuan in total. The investor lineup is impressive—China Mobile’s Lead Industry Fund, Shenzhen Innovation Investment Group, Beijing AI Industry Investment Fund, Qiming Venture Partners, and TCL Ventures. However, the gap between 'several hundred million yuan' and '6 billion USD' spans nearly two orders of magnitude.

What exactly is the capital market pricing?

InTime’s certainty is 'verifiable': first in shipments (10,000 units/year), customers include leading OEMs (Unitree, Zhiyuan, Ubtech), full-stack self-research (from cylinders to whole hands), and annual production capacity of 500,000 micro servo cylinders. These are hard facts.

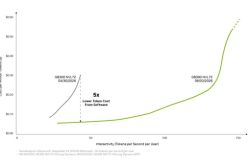

Lingxin Qiaoshou’s imagination is 'narrative-driven': over 80% market share in global high-DOF dexterous hands, full coverage of three major technical routes, and the narrative of being the 'Anthropic of the physical world.' Capital is willing to pay a premium for 'narratives' but not for 'mass production'—this is the fundamental reason for the stark valuation gap between Lingxin Qiaoshou’s 40 billion yuan and InTime’s valuation.

InTime’s dilemma is this: 'Rampant shipment growth doesn’t equate to industry maturity.' In 2025, China’s dexterous hand market sold only about 19,200 units. InTime accounted for more than half, but the market itself isn’t large enough yet. Being 'first' in a market of just 20,000 units inevitably raises questions about the value of that leadership.

Even more awkwardly, the entire dexterous hand industry is generally unprofitable. InTime’s micro servo cylinder business is profitable, but its dexterous hand business is still in the stage of scaling up investments. The capital market tolerates 'losses with high growth' far more than 'small profits with stability.'

However, the entry of 'national team' investors is still noteworthy. China Mobile’s Lead Industry Fund stated that InTime Robot has long-term, systematic technological accumulation in the dexterous hand field, and 'its leading industry shipments also guarantee continuous product iteration.' These institutions’ involvement indicates that InTime’s 'first-place shipments' are recognized at the industrial level—a confirmation by the 'national team' of the strategic value of the dexterous hand sector.

InTime is the 'hidden champion' of the dexterous hand sector, but 'hidden' means the capital market doesn’t see it—or if it does, it’s unwilling to pay a premium. The capital market’s logic is: When an industry is still small, those with 'imagination' are more valuable.

03 The 'Impossible Trinity' of Dexterous Hands: Can InTime Bridge the Gap from 'Shipments' to 'Pricing Power'?

Being first in shipments is a fact; lagging in valuation is also a fact. InTime Robot’s real challenge is whether it can translate 'shipments' into 'pricing power.'

Fang Hainan puts it bluntly: 'A good dexterous hand perfectly solves performance, cost, and reliability. To this day, no product meets all three requirements. This is the 'impossible trinity' of dexterous hands.'

Achieving high performance sends costs soaring; achieving low costs makes basic grasping difficult; achieving high reliability compromises performance. InTime’s strength lies in 'mass production' and 'reliability'—its flagship product has achieved a lifespan of one million grasping cycles under load; its weakness lies in 'high degrees of freedom' and 'high added value'—areas where Lingxin Qiaoshou excels.

From the perspective of dexterous hand deployment, Fang Hainan shares a set of industry data: Currently, out of about 5,000 robots, fewer than 2,000 are equipped with dexterous hands, and some scenarios lack them entirely. This aligns with her judgment: the industry is still in its early stages.

'At the practical application level, the entire industry was still solving single-point problems last year and hasn’t yet achieved mature applications or bulk replication.' Fang Hainan predicts that the first area for bulk replication will likely be 'last-mile' logistics sorting. She emphasizes that the core role of dexterous hands isn’t to replace grippers.

The competitive landscape is also evolving rapidly. The dexterous hand sector has formed three major camps: independent integrators, OEMs’ in-house R&D, and component extenders. InTime faces 'pressure from both sides': above, OEMs like Zhiyuan and Unitree are encroaching on the high-end market with in-house R&D (Zhiyuan Critical Point, Unitree Dex5); below, new entrants are capturing niche markets with differentiated strategies. Public reports indicate that competitors are already undercutting InTime by 1,000 to 2,000 yuan per unit. Fang Hainan is clear on this: 'Blind price wars are all ineffective competition.'

InTime’s current approach is 'walking on two legs': alongside its linkage-based solutions, it is simultaneously advancing tendon rope (tendon-rope) and direct-drive technologies across the full stack. Fang Hainan predicts that the dexterous hand industry will mature in the next 2-3 years, with mass production capacity, cost control, and scenario deployment efficiency becoming core competitive factors. The company’s next goal is to push its products into more real-world end applications and achieve annual shipments at the 100,000-unit level.

InTime resembles not Lingxin Qiaoshou (a valuation-driven star) but CATL (a capacity-driven leader). CATL’s rise wasn’t driven by 'high-growth narratives' but by 'scale effects + cost advantages + customer lock-in.' If the dexterous hand market truly explodes, InTime’s capacity advantages and customer network will become its deepest moat.

But the prerequisite is that the market must explode.

InTime Robot’s 'dexterous hand paradox' is essentially a pricing gap between 'certainty' and 'imagination.' InTime chose 'certainty'—first in shipments, full-stack self-research, customers including leading OEMs—but the capital market is more willing to pay a premium for 'imagination.' What InTime needs to prove is that when the dexterous hand market truly explodes, its moat as the top shipment leader will be more valuable than the narrative of being top in valuation.

Conclusion

InTime Robot’s story is one about 'waiting.'

It waited seven years for the humanoid robot trend; it waited a decade to achieve over 10,000 annual dexterous hand deliveries. But the capital market doesn’t like to wait—it prefers to pay a premium for 'already exploded' narratives rather than 'about to explode' production capacity.

Earlier, we dissected Lingxin Qiaoshou’s 40 billion yuan valuation—a premium for the certainty of being a 'shovel seller,' a valuation of the technological barriers of the 'impossible trinity,' and a vote for the strategic ambition of being the 'Anthropic of the physical world.' But when we turn to InTime Robot, we see a different story: being first in shipments doesn’t earn a valuation premium.

InTime Robot’s 'dexterous hand paradox' is a common dilemma for all 'pragmatic' enterprises in the dexterous hand sector: first in shipments but lagging in valuation; customers include leading OEMs but capital remains unimpressed; a decade of technological accumulation but the market only recognizes two years.

But the flip side of the paradox is this: When the dexterous hand market transforms from a 'small pond' into an 'ocean,' the moat of being first in shipments will be more valuable than the narrative of being first in valuation.

The dexterous hand sector is far from reaching its conclusion. Whether InTime Robot’s 'first-place shipments' are a temporary advantage or the ultimate moat will be answered not in today’s valuation tables but in the shipment data of the next three years.

-

![]()

Is Baidu Now Fostering Its Own 'Yao Shunyu'?

-

![]()

NVIDIA Goes Wild! DeepSeek V4 Inference Costs Slashed by 80%

-

![]()

Preparing for the 6G Era: US Completely Shuts Down 2G Networks, China Unicom Initiates Gradual Decommissioning of WCDMA 3G Networks

-

![]()

Mid-year 2026 Sales Review: Auto Market Shifts from Scale Expansion to Systemic Capabilities for Long-term Positioning

-

![]()

From the ARD Protocol, the Turning Point for the Agent Industry Has Arrived

-

Pinduoduo's Strategic Leap in Xiong'an: Beyond Investment, a Pledge to Flourish

-

Liang Wenfeng Has No Desire to Become Another Sam Altman

-

![]()

Revenue Soars, Losses Mount in Billions, Sales Stumble: Avatr's Hong Kong IPO Bid Amid Breakthroughs and Anxieties