Revenue Soars, Losses Mount in Billions, Sales Stumble: Avatr's Hong Kong IPO Bid Amid Breakthroughs and Anxieties

07/02 2026

07/02 2026

350

350

Written by | Duoke

Source | Beiduo Business & Beiduo Finance

On June 30, Avatr Technology (Chongqing) Co., Ltd. (hereinafter referred to as "Avatr") filed its listing application with the Hong Kong Stock Exchange. This marks the company's second attempt at an IPO on the Hong Kong stock market, following the expiration of its initial application in November 2025. Avatr aims to harness the capital market to bolster resources for its subsequent large-scale expansion.

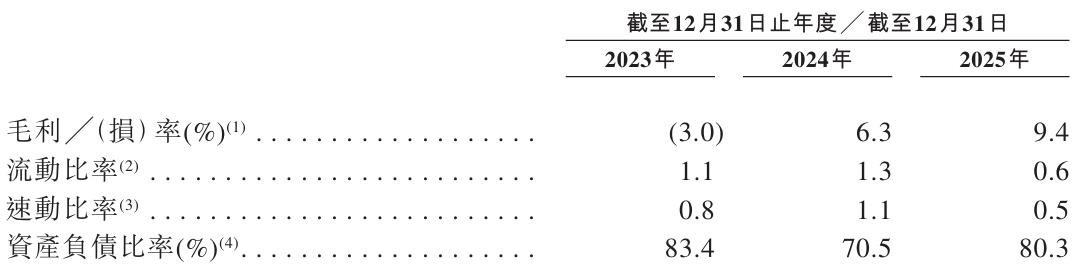

A review of the latest financial data indicates that Avatr's revenue in 2025 surged by nearly 70% year-on-year, accompanied by a steady improvement in gross margin, underscoring the initial success of its premium product pricing strategy. However, since 2026, the company's sales have encountered significant headwinds, with cumulative unrecovered losses exceeding 10 billion yuan continuing to undermine its already fragile profitability.

As the allure of the three major "prestigious partners"—Changan Automobile, CATL, and Huawei—clashes with the race between scaling up operations and restoring profitability, Avatr's current bid for a Hong Kong listing raises a critical question: Is it leveraging the secondary market to establish a closed-loop financing system, or is it merely seeking to passively replenish capital amidst an industry price war? The market awaits a definitive answer.

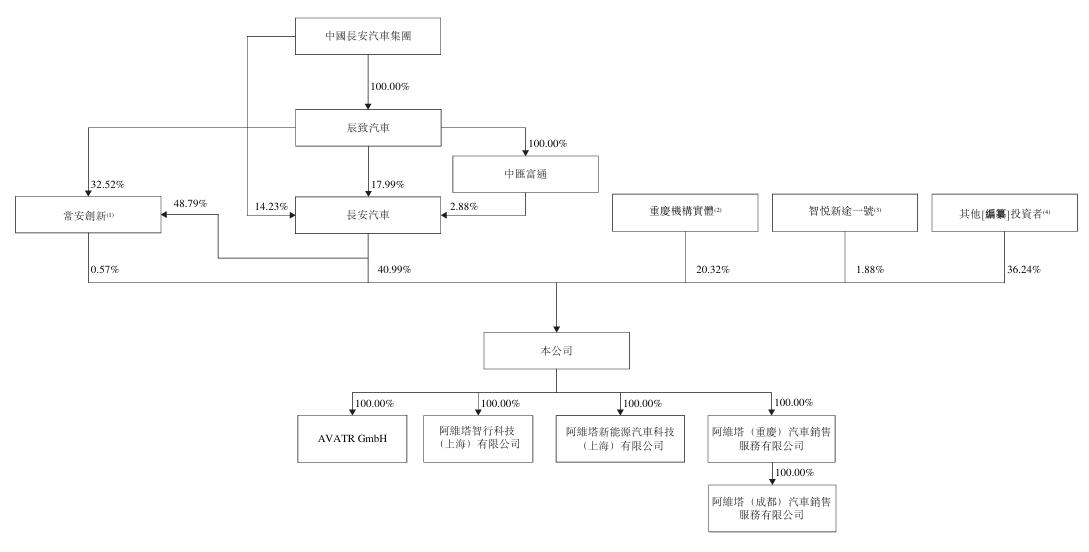

According to Tianyancha and the prospectus, Avatr (AVATR) is a new energy passenger vehicle brand jointly created by Changan Automobile (SZ: 000625) in collaboration with strategic partners CATL (SZ: 300750, HK: 03750), Huawei, and other ecosystem partners through market-oriented management.

After securing a Series C funding round exceeding 11 billion yuan in 2024, Avatr's shareholding structure gradually took shape. As of this IPO, Changan Automobile, the largest shareholder, holds a 40.99% stake, spearheading vehicle manufacturing and production systems; CATL, the second-largest shareholder, holds a 9.17% stake, providing support for battery technology and core three-electric system supplies.

Although Huawei does not directly hold shares in Avatr, it is deeply integrated into the company's vehicle R&D and manufacturing processes through the "HI PLUS mode," offering a comprehensive intelligent automotive solution encompassing intelligent driving, cabins, and connectivity. Meanwhile, Avatr has acquired a stake in Huawei's intelligent automotive subsidiary, AITO, holding a 10% share.

Empowered by these "three industry giants," Avatr has cultivated core competencies across the entire value chain, from product definition, R&D, and manufacturing to marketing, user systems, automotive sales, and after-sales support. It has become the industry's first emerging new energy passenger vehicle brand to achieve a dual-power layout of battery electric vehicles (BEVs) and range-extended electric vehicles (REEVs) across all models.

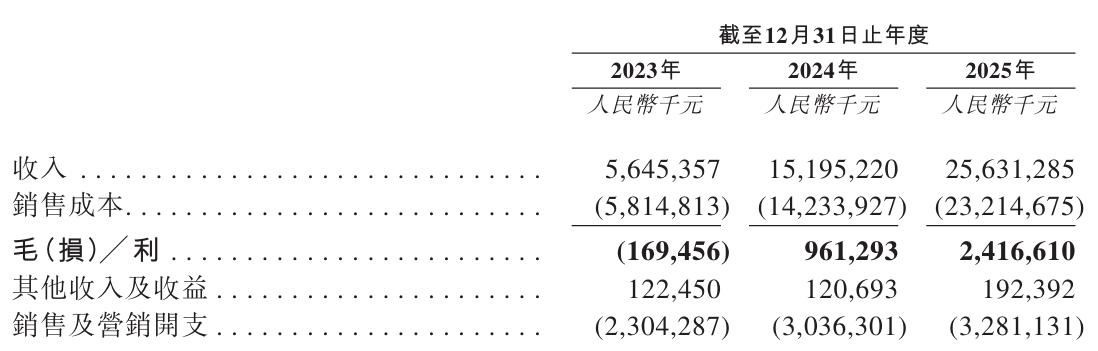

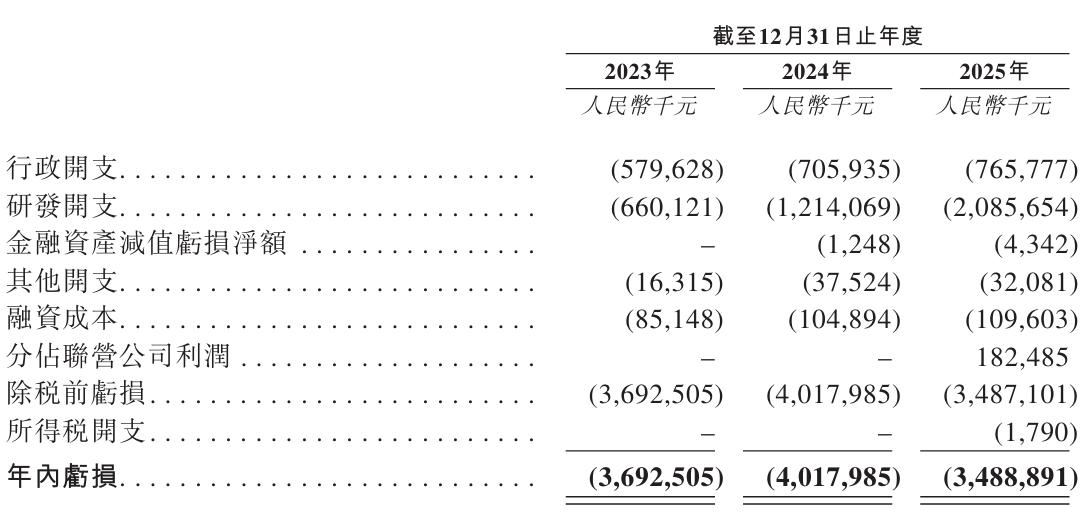

From a financial performance perspective, from 2023 to 2025 (the "reporting period"), Avatr reported revenues of 5.645 billion yuan, 15.195 billion yuan, and 25.631 billion yuan, respectively, with its revenue scale expanding more than 4.5 times over three years. In 2025, revenue increased by 68.7%, ranking among the highest growth rates among new-force automakers during the same period.

Avatr's gross margin also showed continuous improvement during the reporting period, rising from -3.0% in 2023 to 6.3% in 2024 and further to 9.4% in 2025. Gross profit doubled from 169 million yuan to 2.417 billion yuan, with scale effects gradually translating into a solid foundation for profitability.

Avatr also disclosed in its prospectus that after acquiring a 10% stake in Huawei's AITO for 11.5 billion yuan in 2025, the company recognized a profit share of 182 million yuan from its associated company in the first year, achieving positive investment returns. This profit contribution from a strategic partner added a positive dimension to its financial statements.

Despite this, Avatr's path to profitability remains sluggish, with losses of 3.693 billion yuan, 4.018 billion yuan, and 3.489 billion yuan recorded during the reporting periods, respectively. Cumulative losses over three years exceeded 13.2 billion yuan, with its cash-generating speed yet to match its spending pace, leaving the breakeven point still on the horizon.

Avatr acknowledged in its prospectus that with the continued expansion of future business and R&D investment, its costs will further escalate. If the appeal of existing models wanes or new models fail to launch as scheduled or meet market expectations, the company's sales will be impacted, adversely affecting its business and operating performance.

Against the backdrop of NIO, XPeng, Leapmotor, and Li Auto achieving quarterly profitability in the fourth quarter of 2025, with new-force automakers successively crossing the breakeven "watershed," Avatr, which has yet to escape its loss-making situation, faces not only scrutiny of its operational efficiency but also the pressure to catch up amidst dual pressures from the capital market and industry peer performance.

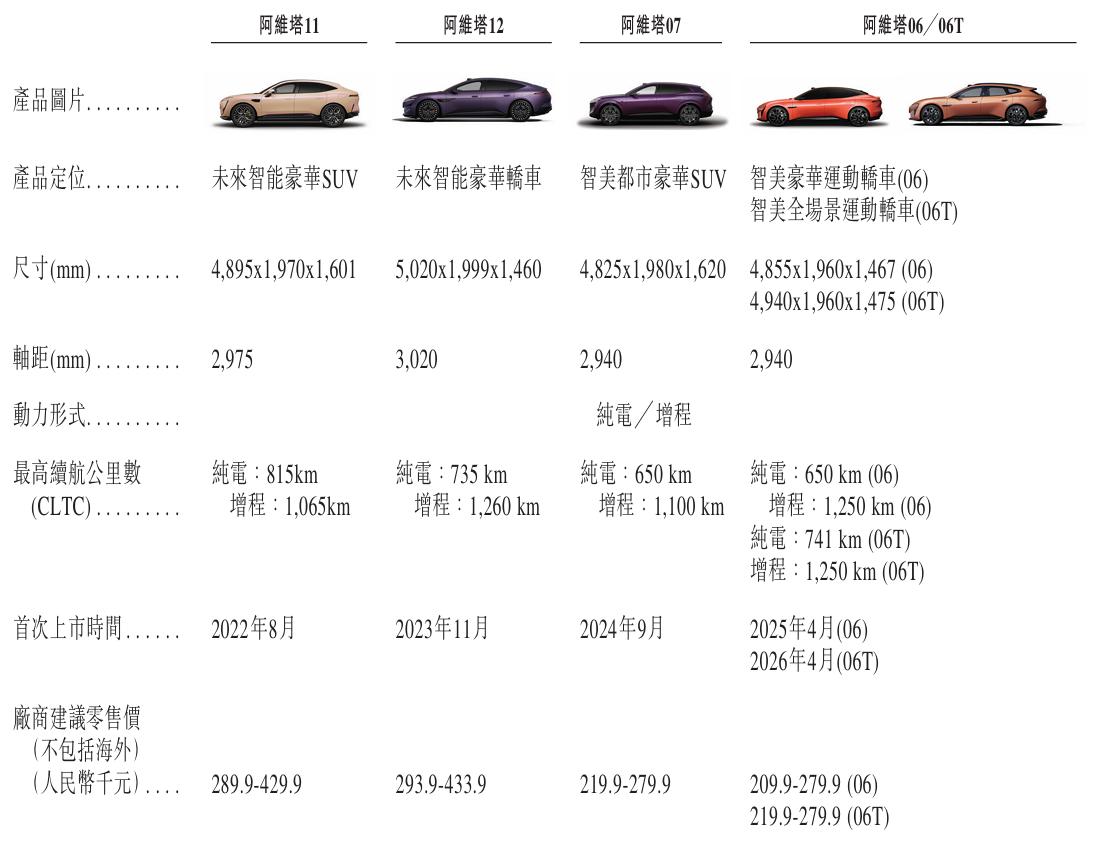

Focusing on the product side, as of the last practical date, Avatr has established a four-model lineup consisting of the Avatr 11, Avatr 12, Avatr 07, and Avatr 06/06T, with prices ranging from 200,000 to 700,000 yuan, covering the two mainstream segments of SUVs and sedans.

In 2025, Avatr delivered a cumulative total of 122,700 new vehicles, achieving a "triple jump" in annual sales since mass deliveries began in 2023. In the Chinese new luxury new energy passenger vehicle market for vehicles priced above 200,000 yuan, Avatr ranked eighth in sales, with several models ranking among the top sellers in their respective target segments.

However, since 2026, Avatr's sales have encountered a "cold snap," with approximately 24,000 vehicles delivered in the first five months, nearly halving from 43,700 vehicles in the same period in 2025. Even though sales rebounded to 7,336 vehicles in May, the best level so far this year, it was insufficient to reverse the overall downturn in the first five months.

Compared to leading new-force brands, Avatr's sales volume is significantly lower. In the first five months of 2025, Leapmotor led with cumulative sales exceeding 260,000 vehicles; Li Auto reached 162,400 vehicles, while NIO, XPeng, Xiaomi, AITO, and other brands also surpassed 100,000 cumulative sales, creating a substantial gap with Avatr.

Nevertheless, Avatr remains optimistic about a sales recovery. The company plans to launch the intelligent and stylish large five-seat luxury SUV, the Avatr 07L, in the third quarter of 2026 and introduce a flagship large six-seat SUV featuring CATL's Qilin condensed matter battery later in the year, further boosting market performance through product expansion.

Avatr also revealed that it will launch three new SUVs through Huawei AITO's joint innovation model before 2028, with subsequent flagship models incorporating Huawei AITO's next-generation intelligent technologies, achieving synchronous iteration of full-stack capabilities in intelligent driving, cabins, and vehicle control, becoming one of the first automotive brands to adopt Huawei's next-generation assisted driving system.

Avatr will also continue to integrate advanced autonomous driving hardware and debut L3/L4 autonomous driving solutions in future new models. On July 1, Avatr announced the acquisition of an L3 autonomous driving test license and is currently verifying system reliability through real-world road tests in multiple scenarios, laying the groundwork for subsequent mass production.

However, between licensing and mass production, technological verification and consumer adoption introduce multiple variables, including regulatory implementation timelines, consumer trust costs, and product pricing strategies. For Avatr, L3 is undoubtedly a "technological narrative" that enhances its brand, but it is far from being the "core engine" driving scale.

As of April 2026, Huawei's ADS has partnered with 25 automotive brands, covering over 50 mass-produced models. This means that even if Avatr enjoys priority access to technologies, its technological differentiation advantage will inevitably be gradually diluted as the "Huawei ecosystem" continues to expand.

Currently, leading new-force automakers have collectively crossed the breakeven line, and capital market scrutiny of the new energy sector has shifted from "evaluating stories" to "examining financial statements." Avatr must not only confront its own challenges in scaling sales but also prove its ability to operate independently amidst industry price wars and the scale effects of leading competitors.

While the L3 license, new product planning, and technological priority are part of Avatr's differentiated narrative, what truly drives capital valuation logic remains the gradual improvement of its financial fundamentals. On this front, Avatr has little room for trial and error.

-

![]()

Giants Enter the Arena One After Another: The Embodied AI Battle Commences

-

![]()

Is It More Profitable to Build 'Hands' for Robots Than 'Humans'?

-

![]()

Yunling Optoelectronics Accelerates Its Listing on the Beijing Stock Exchange: Secures 989 Million Yuan to Bolster Production of Computing Optoelectronic Chips

-

![]()

From Drill Bits to Optical Coatings: A 200-Billion-Yuan Behemoth Quietly Unveils a New Business Front!

-

![]()

New Energy Vehicle Growth Slows: Are 370 Million Existing Cars the Next Lucrative Market?

-

![]()

Is Baidu Now Fostering Its Own 'Yao Shunyu'?

-

![]()

NVIDIA Goes Wild! DeepSeek V4 Inference Costs Slashed by 80%

-

![]()

Preparing for the 6G Era: US Completely Shuts Down 2G Networks, China Unicom Initiates Gradual Decommissioning of WCDMA 3G Networks