Zhipu’s Valuation Soars, MiniMax Faces Challenges

07/13 2026

07/13 2026

548

548

MiniMax Sees 18% Drop, Exhausts All Strategic Moves

Author|Dingshan

Editor|Xiaobai

Cover Image|AI Generated

Produced by|QiangdiaoNext

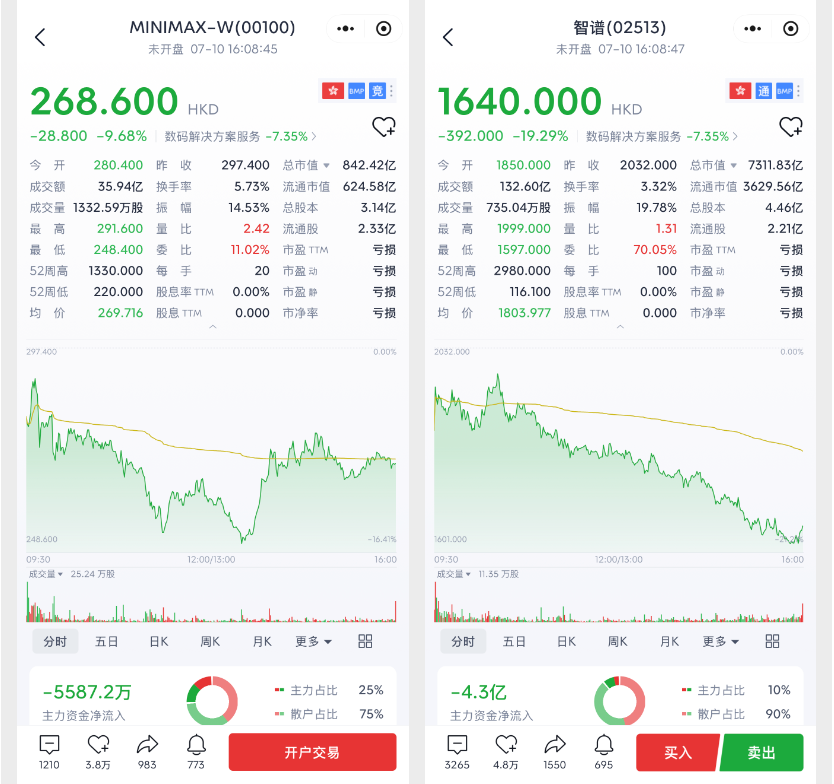

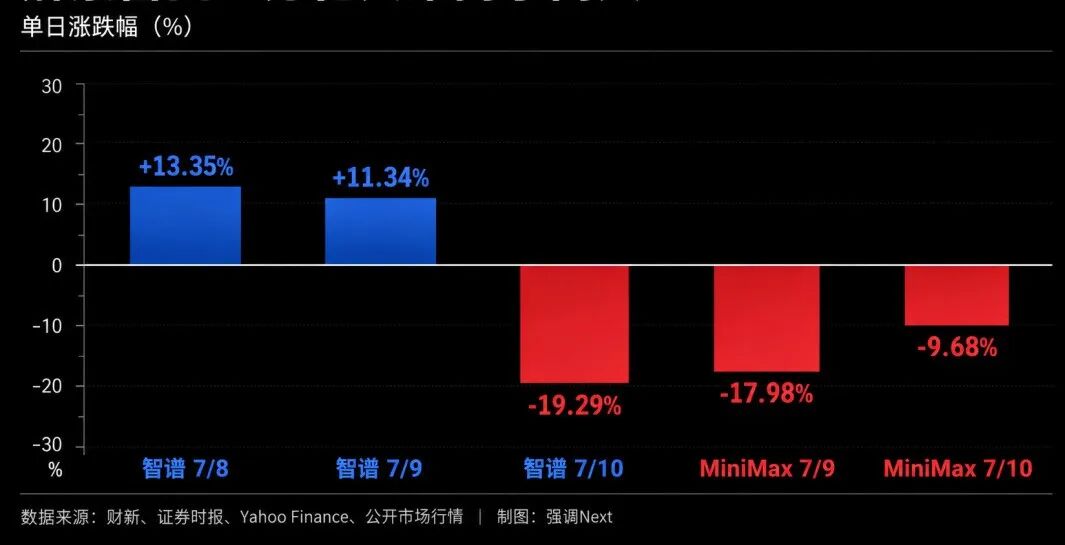

On July 9, MiniMax encountered its inaugural lock-up expiration following its public debut, experiencing a substantial 17.98% decline in its stock price on the same day, which subsequently pushed its total market capitalization below HK$100 billion.

The following day, founder and CEO Yan Junjie addressed all employees in a letter, revealing his decision to forgo a salary until the company achieves Artificial General Intelligence (AGI). He also announced plans to allocate 5% of his personal shares for employee incentives and the development of an open-source ecosystem. On the same day, MiniMax unveiled its intention to raise approximately HK$16 billion.

With the suspension of salaries, distribution of shares, and fundraising initiatives, MiniMax has employed nearly all available strategies to stabilize market expectations simultaneously. Nevertheless, the stock price continued its downward trajectory, plummeting by another 9.68% on July 10.

It is evident that the letter to employees underscored the founder's steadfast commitment, while the financing plan altered the company's shareholding structure. The placement price was nearly 10% lower than the previous day's closing price, and the convertible bonds had the potential to be converted into new shares in the future, exerting initial dilution pressure on existing shareholders.

During the same week, Zhipu also navigated through lock-up expiration, fundraising activities, and significant stock price fluctuations. Its stock surged by 13.35% and 11.34% over the two trading days post-lock-up expiration, with its market value briefly rebounding to HK$900 billion. However, on July 10, it witnessed a decline exceeding 19%, nearly reverting to its pre-lock-up valuation.

The divergence between the so-called "Big Model Duopoly" persisted for a mere two days. Ultimately, the market's focus extended beyond lock-up expiration, delving into the capital requirements of both companies, their fundraising capacities, and whether their existing revenues could justify such lofty valuations.

01. Diverse Lock-up Expirations, Uniform Pressure

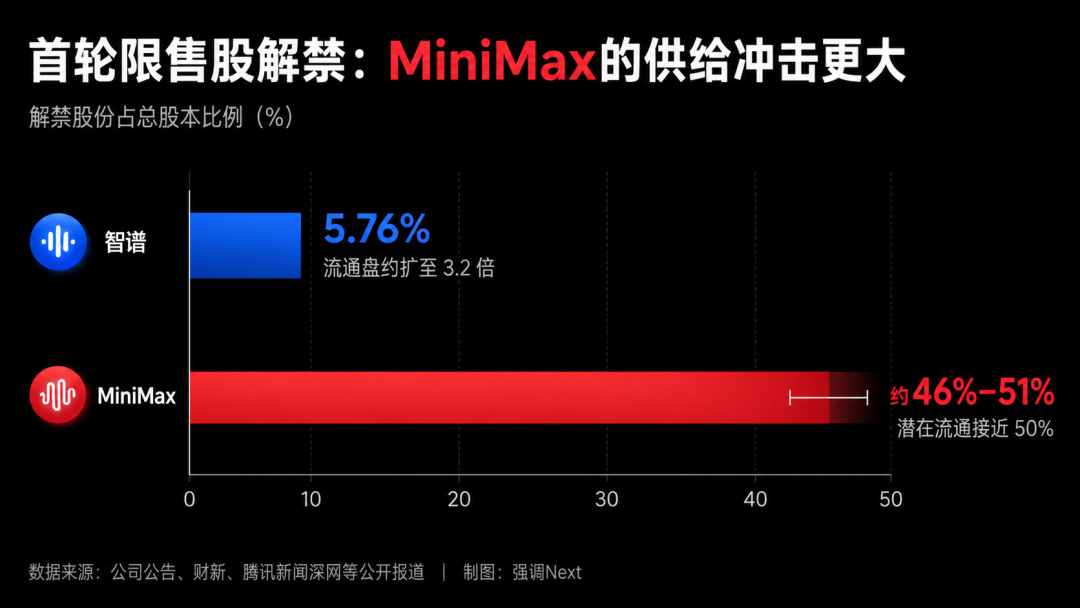

Zhipu's lock-up period concluded on July 8, releasing approximately 25.6816 million shares (5.76% of the total share capital), predominantly held by 11 cornerstone investors. Although the proportion of released shares was relatively modest, the tradable shares expanded to roughly 3.2 times the original volume due to the previously limited free float.

MiniMax's scale of share release was significantly larger. According to Caixin statistics, approximately 153 million shares were unlocked, accounting for over 48% of the total share capital. Initially, its free float was less than 6%, but post-lock-up expiration, the potential free float surged to nearly 50%.

Prior to the lock-up expiration, both companies organized shareholders to publicly declare their intentions. Approximately 70% of Zhipu's cornerstone investors indicated their intention to maintain their holdings, while MiniMax claimed that over 80% of its Pre-IPO and cornerstone shareholders had no plans to reduce their stakes. However, verbal assurances could not alter the fundamental nature of the shares.

Zhipu's lock-up release primarily involved cornerstone investors, including state-backed institutions, industrial funds, and long-term capital. MiniMax's lock-up release was more extensive, encompassing not only cornerstone investors but also a substantial number of pre-IPO financial investors. For venture capital and private equity firms with low holding costs and fund exit cycles, even with significant stock price retracements, substantial floating profits could still be realized.

Consequently, Zhipu's short-term stock price surge post-lock-up expiration cannot be solely attributed to "superior fundamentals." Similarly, MiniMax's decline does not entirely signify concentrated shareholder exits. The more direct disparities lie in the scale of new shares, the holder structure, and the secondary market's capacity to absorb these shares.

Zhipu's significant drop on July 10 also illustrates that a low free float can inflate stock prices but equally amplify declines. Lock-up expiration does not represent a one-time release of negative news but rather restores the two companies' stock prices to more fully traded market conditions.

02. Zhipu’s Revenue Model is More Transparent, MiniMax Still Proving Efficiency

The capital market's preference for Zhipu primarily stems from its relatively transparent revenue model.

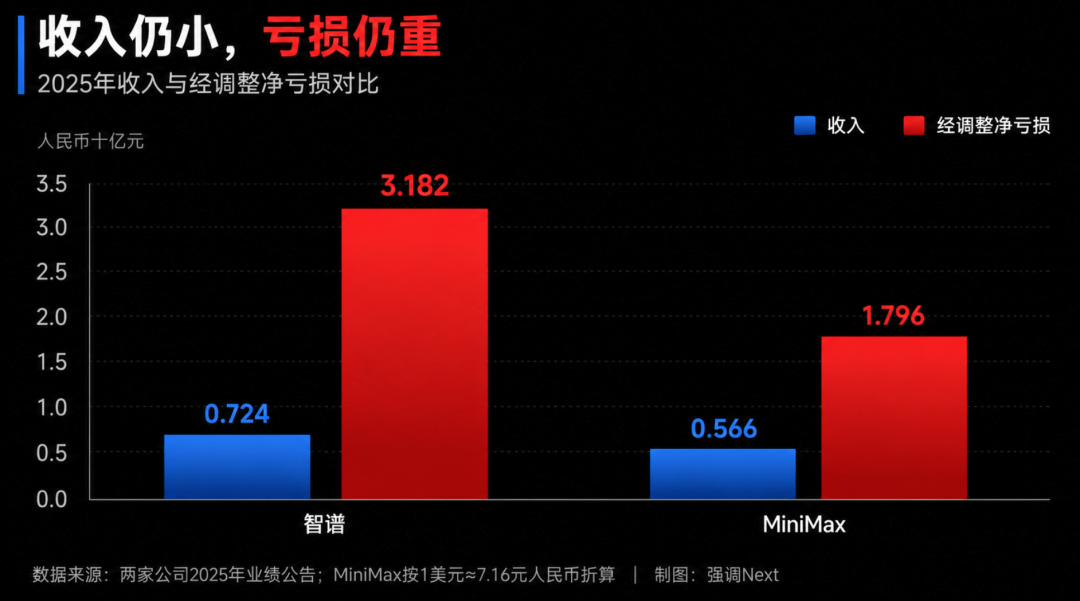

In 2025, Zhipu achieved revenue of RMB 724 million, marking a year-on-year increase of 131.9%. Revenue from its open platform and APIs surged by 292.6% to RMB 190 million, enterprise-grade agent revenue grew by 248.8% to RMB 166 million, and enterprise-grade general large model revenue reached RMB 366 million.

Its MaaS API platform's Annual Recurring Revenue (ARR) reached RMB 1.7 billion. The company also disclosed that after raising API prices by 83% in Q1 2026, call volume increased by 400%. For a large model company, this at least demonstrates that certain enterprise clients are willing to continually pay for model capabilities.

However, Zhipu's revenue certainty is far from sufficient to fully justify its valuation. In 2025, the company reported an adjusted net loss of RMB 3.182 billion, with R&D investment amounting to RMB 3.18 billion. Based on a rough calculation of its market value of approximately HK$906 billion on July 9 and its 2025 revenue, its price-to-sales ratio still exceeds 1200 times. The market is clearly investing not just in existing revenue but also in the scarcity of domestic foundational models and future market share.

In contrast, MiniMax reported revenue of approximately $79.04 million (approximately RMB 560 million) in 2025, reflecting a year-on-year increase of 158.9%. While this growth appears faster, its revenue structure is more fragile.

MiniMax's C-end revenue accounted for 67%, with a paid conversion rate of less than 1%. Its adjusted net loss was $251 million (approximately RMB 1.7 billion), continuing to widen year-on-year. Its flagship model M3, launched in June of the same year, faced consumer resistance due to its pricing strategy and was compelled to reduce prices by 50% within a week of its debut, with its stock price dropping more than 10% on the release day.

The video model Hailuo AI has experienced a significant decline in presence amid competition from Kuaishou Kling AI's independent financing and ByteDance's Seedance 2.0 gaining popularity. More critically, in April, five departments issued a notice prohibiting the provision of virtual intimate relationship services to minors, with formal enforcement commencing on July 15, directly impacting the core monetization scenarios of MiniMax's emotional companionship apps like Xingye.

The capital market's stance is already evident through its actions. JPMorgan raised Zhipu's target price from HK$400 to HK$1,800, while for MiniMax, Citi reduced its target price from HK$1,330 to HK$533 and placed it on a short-term downward watchlist. JPMorgan also downgraded its rating from "Overweight" to "Neutral" and cut its target price from HK$1,100 to HK$400.

Thus, the lock-up expiration ratio merely served as a trigger; the true catalysts for this divergence were the certainty of share quality and business models. Zhipu needs to demonstrate that its high growth can be sustained, while MiniMax must first prove that its rapid growth can gradually narrow losses.

03. Salary Suspension is Symbolic, Financing is Paramount

On July 10, Yan Junjie dispatched an internal letter to all employees in response to market volatility, conveying a long-term commitment to the team and the market while leveraging new financing to alleviate cash flow concerns arising from lock-up expiration. This move aimed to shift the narrative from "shareholder selling pressure" back to "technological endurance."

However, for investors, the financing plan holds greater significance.

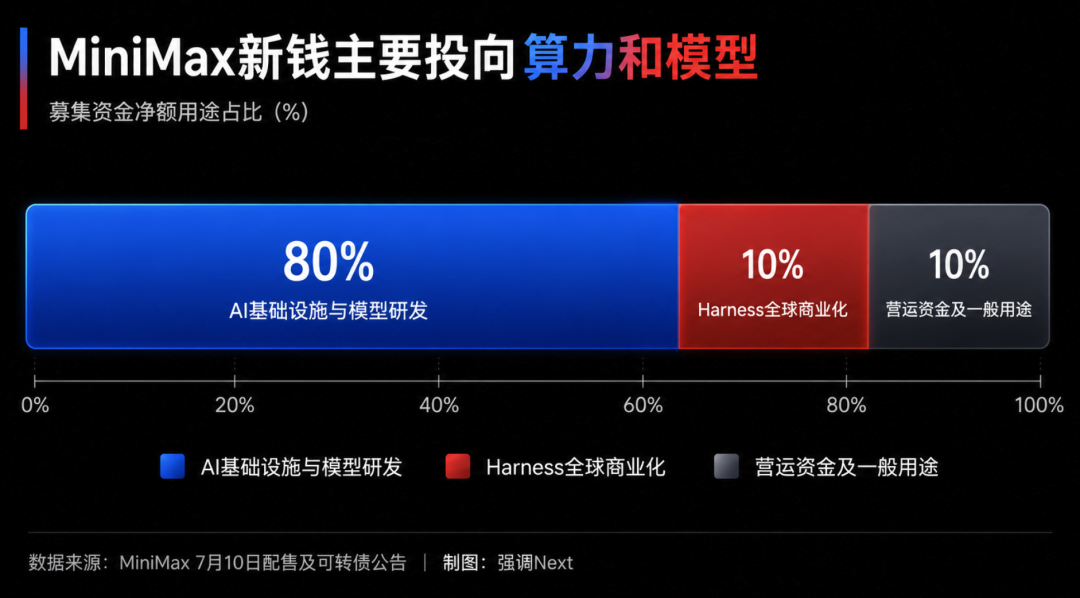

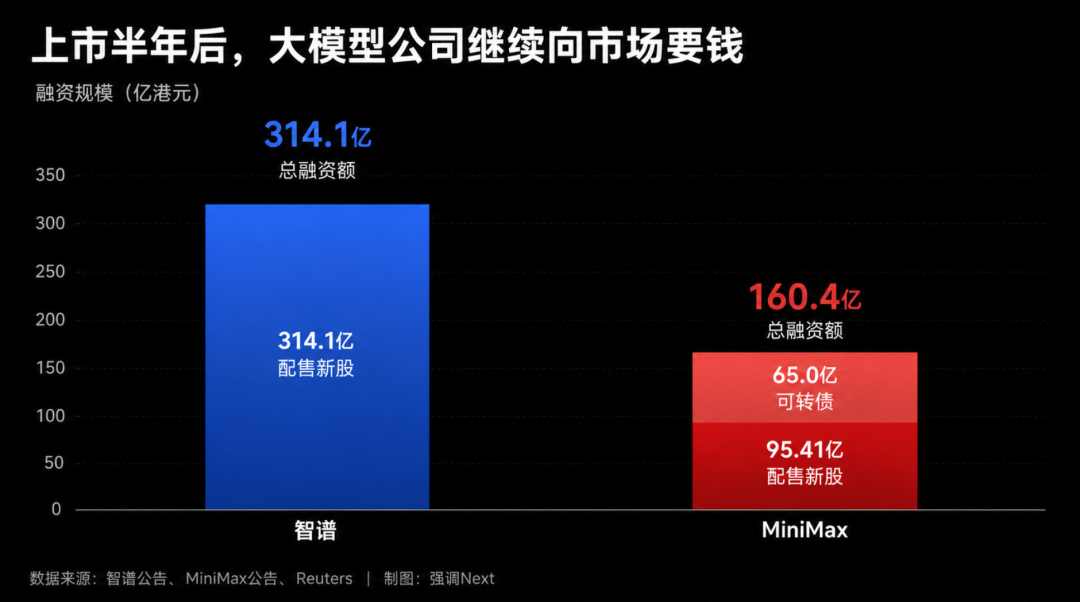

MiniMax priced new shares at HK$268 each, representing a discount of approximately 9.9% from the July 9 closing price. The initial conversion price for the HK$6.5 billion convertible bonds was set at HK$335, a premium of about 12.6% from the previous day's closing price. The total financing from both components amounted to approximately HK$16.04 billion, earmarked for R&D, commercialization, working capital, and general corporate purposes.

While this infusion of funds undoubtedly replenishes resources, it also underscores the substantial capital requirements of large model companies.

Zhipu's maneuvers were even more aggressive. On July 9, the company announced the placement of up to 19.78 million new H-shares at HK$1,588 each, raising approximately HK$31.41 billion. Zhipu's IPO in early 2026 generated a net amount of approximately HK$4.896 billion, with about HK$4.588 billion (approximately 93%) already utilized by the placement date.

In essence, just half a year after going public, Zhipu and MiniMax have collectively raised approximately HK$47.4 billion from the Hong Kong stock market. The concentrated fundraising by both companies during the lock-up window is no coincidence. Model training, inference computing power, R&D personnel, and product promotion all necessitate continuous investment. Going public merely provides a financing entry point but does not resolve the issue of capital consumption.

They are also simultaneously preparing to return to the STAR Market. Zhipu's IPO Tutoring status has entered "counseling acceptance," aiming to raise no more than RMB 15 billion. MiniMax also signed a counseling agreement in late May to prepare for an A-share listing. Capital demand is clearly one of the pivotal reasons for both companies to establish "A+H" financing channels.

Thus, this lock-up expiration did not determine a definitive winner.

Zhipu currently boasts clearer enterprise revenue but also carries a more challenging valuation to justify. MiniMax's global user base and multimodal products retain growth potential but require urgent improvements in revenue quality and loss efficiency.

A letter to all employees can stabilize the team but cannot replace financial reports. HK$16 billion can extend the R&D cycle but cannot automatically translate into a higher valuation.

What truly matters next are the two companies' revenue growth rates, gross margins, and cash consumption post-financing. Zhipu must demonstrate that HK$31.4 billion can continue to amplify commercialization, while MiniMax must prove that HK$16 billion buys more than just time. The interim reports to be disclosed by both companies in August and the larger lock-up expiration in January next year will be the critical junctures determining the trajectory of this "duopoly competition" in the latter half of the year.

· Data Sources and Notes: The data presented in this article is sourced from company announcements and public market reports as of July 10, 2026, for industry observation purposes only and does not constitute any investment advice.

- END -

-

![]()

Apple's Lawsuit Could Set Back OpenAI's Hardware Ambitions by Years

-

![]()

Domestic EVs Lead, Overseas PHEVs Flourish

-

![]()

Anthropic Engages with Samsung for Self-Developed AI Chips, Trend of Large Model Companies Collectively 'Building Chips' Emerges

-

![]()

Why Has Continental Evolved into a Pure Tire Company Post-'Downsizing'?

-

![]()

Zhipu’s Valuation Soars, MiniMax Faces Challenges

-

![]()

Weekly Stock Review | Who Dominates the Market: Hedge Funds, Quant Traders, Institutions, or Hot Money?

-

![]()

Sales Slump Again: Why Are Affluent Buyers No Longer Exclusively Opting for Porsche?

-

![]()

Xiaomi’s New Auto Brand Launch Sparks Stock Rebound: Is a Trend Reversal on the Horizon?