In the AI Era, Are There Only Volcano Engine and Alibaba Cloud Left in the Cloud Market?

05/09 2026

05/09 2026

738

738

Tencent Cloud and Huawei Cloud are not on the list

The semi-annual MaaS market exam is here again.

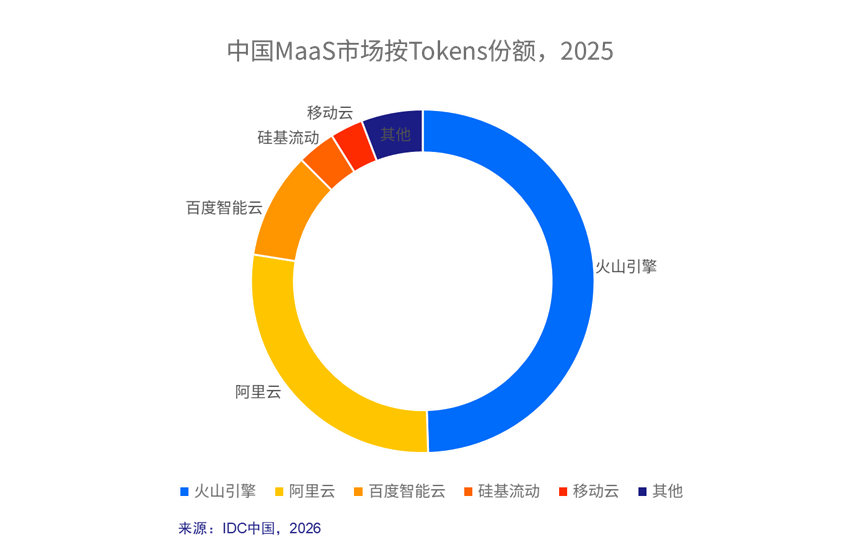

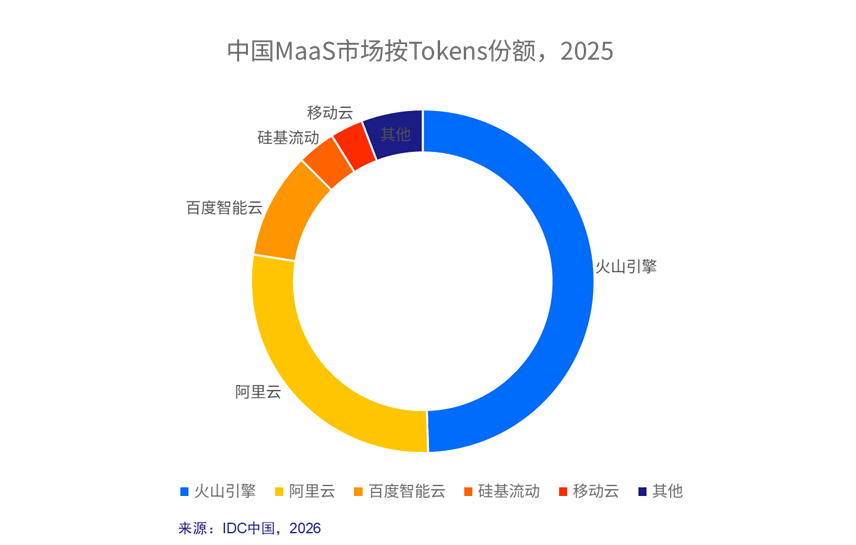

On May 7, IDC released the "Latest Analysis Report on the Market Landscape of Enterprise-Level MaaS in China," which shows that the volume of large model calls on China's public clouds will reach 1,944 trillion tokens in 2025, a 16-fold increase year-on-year.

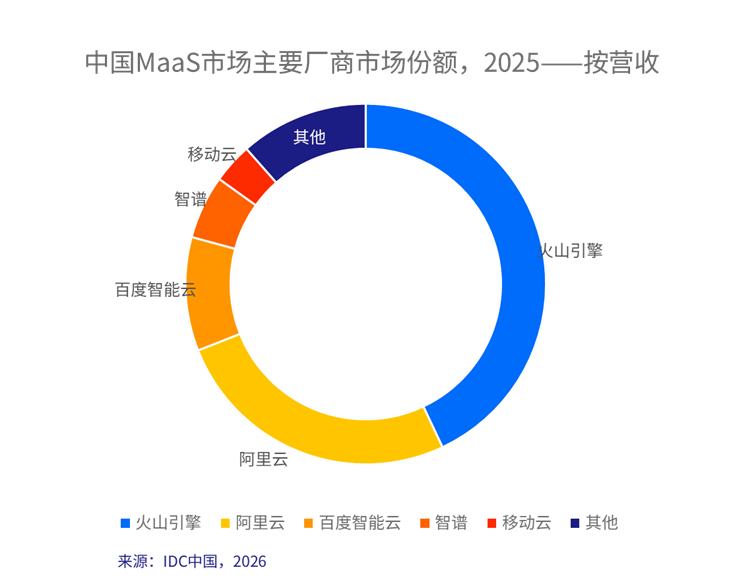

Among them, Volcano Engine leads the Chinese market with a 49.5% share. Alibaba Cloud and Baidu Intelligent Cloud, ranked second and third, respectively, capture 28% and 10% of the market share, with the three companies together accounting for nearly 90% of the market.

So, how have the top three cloud companies performed, given that nearly 90% of the market is dominated by them? Besides AI cloud providers, which other companies are worth paying attention to in the MaaS era?

01

Volcano Engine

Becomes the 'Biggest Winner' in the MaaS Era

To be honest, seeing Volcano Engine's 49.5% share was somewhat beyond my initial expectations.

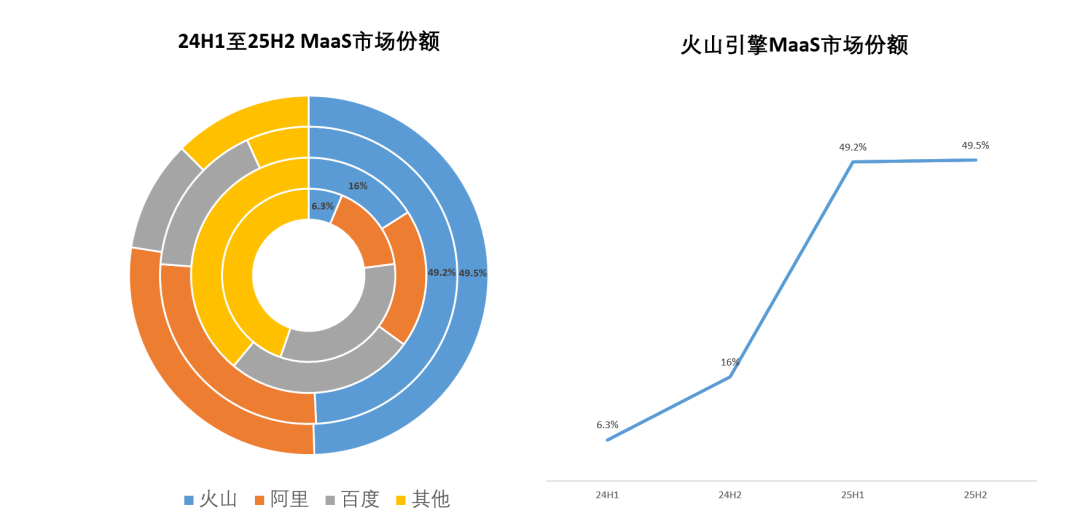

In the first half of 2025 (25H1), Volcano Engine's MaaS share rapidly grew from 16% in the second half of 2024 (24H2) to a high of 49.2%, firmly taking the top spot. At the time, Superfocus communicated with researchers from various cloud companies, and there was a general consensus that the competition in the MaaS market had only just begun. Alibaba, Tencent, and even Huawei Cloud had not yet made significant bets—only Volcano Engine was going all-in on this track.

According to Caizhongshe, Tan Dai, President of Volcano Engine, stated in an interview with LatePost that in the early days of ByteDance's cloud entry in 2020, management required a forecast of the cloud market landscape by 2030. Internally, it was believed that traditional cloud services would no longer be the ultimate form of future clouds, ultimately leading to a focus on 'AI.' This is also why the word 'cloud' is absent from Volcano Engine's name.

In 2024, when MaaS was officially established as the future direction, Volcano Engine adjusted the performance evaluation rules for its sales team, prioritizing the sales of MaaS products above all else. It even explicitly stipulated that selling products at the same price would yield far higher returns from MaaS than from traditional cloud services.

The results were positive. Through efforts in 2024 and the first half of 2025 (25H1), Volcano Engine's MaaS market share grew from 6.3% to 49.2%, making it the top MaaS cloud provider in China.

However, in the fast-paced AI sector, first-mover advantage is hard to quickly translate into an absolute security barrier. Thus, the market generally believed that as other cloud giants fully reacted and intensified their efforts in the second half of the year, Volcano Engine's share would likely be diluted to varying degrees by latecomers.

But the outcome was surprising. In the fierce market competition of the second half of 2025 (25H2), Volcano Engine's market share not only did not decline but instead increased slightly. Although the growth was almost negligible, it became particularly valuable against the backdrop of a 16-fold year-on-year increase in the overall market.

The apparent reason for Volcano Engine's rapid growth in MaaS share is its role as a driver of price wars in the AI era.

Looking back over the past three years, Volcano Engine's price reduction strategy followed a clear three-step rhythm. In May 2024, it entered the market with an ultra-low price, offering a 99.3% reduction to open up the market. Then, in June 2025, it promoted agent adoption through tiered pricing and free deep thinking/multimodal capabilities. By the end of the year, it introduced tiered discounts to lock in long-term usage from major clients.

However, beyond the appearance (surface-level appearance) of price wars, Volcano Engine's core competitiveness in outmaneuvering giants and capturing the largest share of incremental growth lies not in tactical success but in being an 'AI-native cloud' born at the right time.

In 2025, as the AI landscape gradually solidified, many traditional cloud giants found themselves trapped in a 'tug-of-war' between IaaS and MaaS.

For most established cloud providers, their underlying DNA is 'cloud-native AI,' meaning AI is merely a new project grafted onto a massive traditional IaaS infrastructure.

Under this architectural and organizational inertia, when MaaS businesses need to break into the market with extremely low profits or even losses, direct conflicts of interest and KPIs arise with IaaS departments, which bear the core responsibility for profitability. This inevitable historical burden leads to distorted actions and resource inefficiencies among traditional cloud providers when facing MaaS strategies.

In contrast, Volcano Engine, as the latest core player to enter China's public cloud market, carries no heavy traditional cloud baggage. What was once a disadvantage has now become its trump card in the era of large models.

Without the burden of traditional clouds, Volcano Engine does not need to consider IaaS share. Instead, it demonstrates an extremely clear business logic—using MaaS as the 'locomotive' to drive the entire cloud.

Under this 'AI-native' strategy, MaaS is no longer an isolated product requiring independent profitability calculations. When enterprises flock to Volcano for low-priced tokens and convenient model tools derived from ByteDance's internal ecosystem, they naturally generate demand for high-throughput storage, vector databases, heterogeneous computing clusters, and even traditional computing networks as they implement and operationalize AI businesses.

By using MaaS products to create front-end traffic entry points and go with the flow ( go with the flow 而为, taking advantage of the situation) packaging and delivering previously hard-to-sell IaaS computing power and PaaS tools from the underlying layer, Volcano Engine achieves reverse penetration. This 'MaaS-driven IaaS/PaaS' approach not only avoids the quagmire of internal consumption seen in traditional clouds but also establishes a genuine moat in the new MaaS business.

02

Alibaba Cloud Focuses on Token Consumption

But More on Value Creation

If Volcano Engine completed a surprise attack on the existing market through the 'express train' of MaaS, then Alibaba Cloud, as an established leader, delivered a more deliberate 'value reflection' in this round of exams.

From the perspective of MaaS market share alone, Alibaba Cloud seems to have reacted a step slower and has even been outpaced by latecomers in terms of absolute token call volume.

However, this is not due to the clumsiness of a giant's turn but rather a strategic choice rooted in Alibaba's understanding of the commercial essence of AI: instead of getting bogged down in a low-margin 'token consumption war,' Alibaba opts to build a high-value ecological niche.

Liu Weiguang, Vice President of Alibaba Cloud Intelligence Group, explicitly stated in a previous interview with LatePost, 'The quality of tokens matters more than the quantity.'

'In his view, this is the fundamental difference between enterprises using large models and individual users. While individual users may consume tokens for entertainment, efficiency-driven enterprises incur costs for every token exchange. They pay not only for tokens but also for the human resources and time invested in their business lines.'

This may seem like a public relations statement to explain Alibaba's 'lag' in token consumption, but we believe it reflects a deeper 'subtext' based on Alibaba's profound understanding of the enterprise market.

For individual users, token consumption from watching short videos or chatting may be largely recreational, with extremely low cost sensitivity. However, for enterprise clients pursuing ROI, every 100 million token exchanges correspond to significant business labor, time investment, and computing costs. If tokens lack value, high call volumes are merely bubbles.

Based on this logic, Alibaba underwent significant organizational evolution, establishing the ATH Business Unit to reshape the value chain in the AI era.

The ATH Business Unit aims to create, deliver, and apply tokens, focusing more on the value each token brings to users—which is also the deeper goal of the MaaS model.

Although this approach makes Alibaba seem less aggressive in the single dimension of 'token call volume' in the short term, it has stabilized its position in the broader AI infrastructure market.

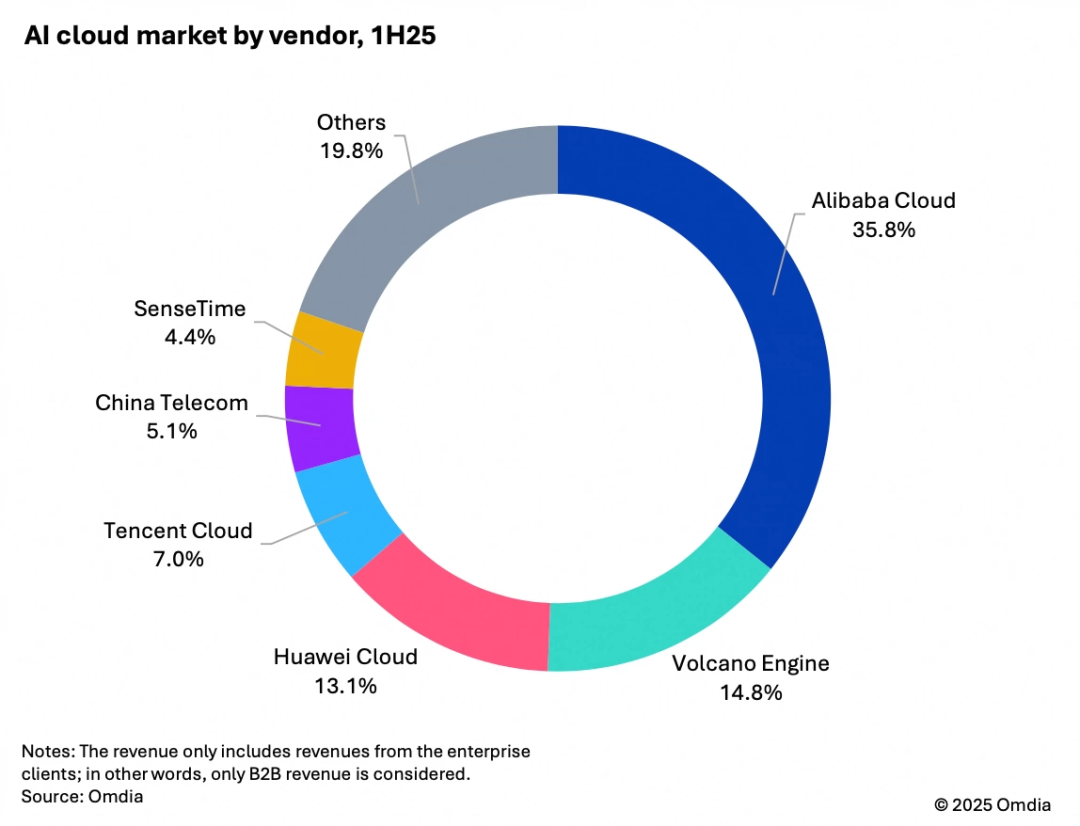

This also explains why Alibaba prefers to evaluate itself using another framework. According to Omdia data, in the first half of 2025, Alibaba Cloud dominated the overall Chinese AI cloud market, which includes AI IaaS, PaaS, and MaaS, with a 35.8% share—exceeding the combined share of the second to fourth-ranked providers.

Alibaba's strategic intent is clear: while Volcano Engine focuses on token consumption, Alibaba Cloud aims to build the most complete and robust 'power and water supply network' in the AI era, becoming the highest-quality and most comprehensive computing power provider.

03

Baidu Steadily Defends Its Core Business

The MaaS Market Welcomes 'New Variables'

Compared to Volcano Engine's rapid growth and Alibaba Cloud's value reshaping, Baidu Intelligent Cloud, ranked third with a 10% MaaS market share, delivered a more steady performance.

As the earliest cloud provider to deeply cultivate large model capabilities for enterprise-level B-end markets in China, Baidu has reaped the early benefits of industrial intelligence. This first-mover advantage is reflected not only in technology but also in commercial implementation. Its deep business understanding and customer reach in traditional sectors such as government, transportation, and finance continue to form a solid foundation that is difficult to shake.

Moreover, what makes this MaaS market ranking distinct from the traditional cloud era are the names ranked after the 'Big Three.'

If we shift our focus from the top players and compare IDC's two charts—'Market Share by Tokens' and 'Market Share by Revenue'—we will find that the power landscape of the traditional cloud era is being reshuffled.

Based on token consumption, Silicon Flow, a startup specializing in large model computing infrastructure, has forcefully entered the market, becoming the fourth-largest MaaS provider after Volcano, Alibaba, and Baidu.

However, when calculating actual revenue from MaaS businesses, Zhipu AI, a domestic large model unicorn, replaces Silicon Flow in fourth place.

In this core ranking representing the growth engine of cloud computing for the next decade, Tencent Cloud and Huawei Cloud—once dominant first-tier players in the traditional cloud era—are nowhere to be seen.

Instead, pure AI-native companies like Silicon Flow and Zhipu AI, along with operators like China Mobile Cloud leveraging strong underlying computing power and government-enterprise networks, have entered the fray.

This conveys a harsh reality to the market: AI, a new variable in the cloud era, is reshaping the entire market.

The battle for the MaaS market is no longer an 'internal war' among traditional cloud giants dividing the pie. Under these new rules, the scale of existing cloud infrastructure and historical track records are no longer absolute moats. New faces born and bred in AI are aggressively tearing through the defenses of traditional giants with pure AI DNA and ultimate (jízhì, extreme) efficiency.

The ultimate outcome of the MaaS market may be far more uncertain than we imagine.

- END -

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action