SpaceX: From the Aerospace 'Mixue Ice Cream & Tea' to a Wall Street Enchantress

06/22 2026

06/22 2026

459

459

Wall Street's infatuation with SpaceX has reached a fever pitch.

Raising $75 billion by issuing only 4.2% of its stock. This is 2.6 times the amount raised by Saudi Aramco, previously the largest IPO.

Within three days of listing, its market capitalization surpassed Amazon's, despite having only 2.6% of Amazon's annual revenue.

SpaceX has become the perfect debate topic: proponents fully unleash their imagination on its space narratives, while opponents raise eyebrows at its sky-high valuation.

The Aerospace 'Mixue Ice Cream & Tea'

What story does SpaceX tell? We believe it's a story of technological leadership fueling imagination.

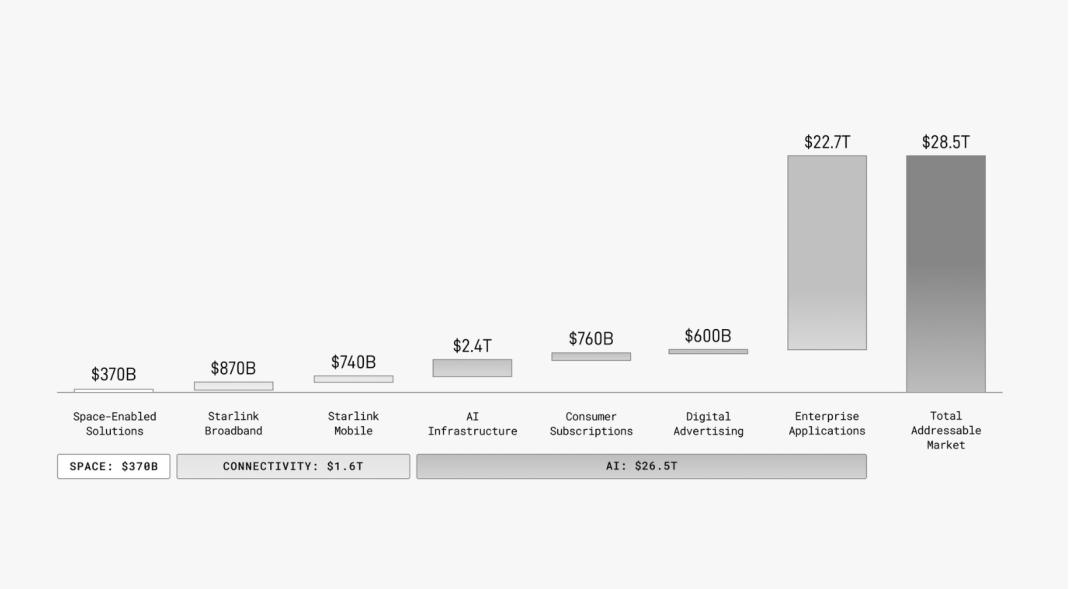

Its business primarily consists of three segments: launch services, Starlink, and AI. Tesla has drawn a pie worth $28.5 trillion (approximately 194 trillion RMB) from these three areas.

How big is this pie? It's larger than China's current GDP.

This seems absurd, but let's examine why this figure is so extreme.

The first business segment, launch services, features Falcon and Starship with remarkably rational and even conservative market estimates. SpaceX projects a $370 billion market for space-enabled solutions.

According to the prospectus, launch services revenue will reach $4.1 billion in 2025, up 7.6% year-on-year. While this growth rate isn't outstanding, the first quarter saw a decline from $870 million to $620 million, a 28.4% YoY drop.

However, launch services represent the beginning of all stories and the foundation of SpaceX's ecosystem. Key advantages include:

Low cost, initially derived from vertically integrated manufacturing. SpaceX independently develops and produces rocket engines, applying automotive casting processes to aerospace engines. Materials have been significantly optimized, with 30X stainless steel at $2,500/ton replacing carbon fiber at $30,000/ton. The early Falcon 9 shared 80% of its components with the Falcon Heavy, reducing manufacturing and machining costs.

Reusability. While not the first to achieve recoverability, SpaceX became the first private company to successfully launch and recover orbital-class rockets. A decade ago, Falcon 9 achieved first-stage recovery using landing legs, making Musk a legend overnight.

Recently, the heavy-lift Starship developed the 'chopstick rocket capture' technology, continuously validating its reliability. The spacecraft has achieved soft landing and destruction, with full reusability on the horizon. Given time, this technology will likely match Falcon 9's reliability, further reducing launch costs.

From manufacturing to launch, SpaceX has dramatically reduced rocket costs. According to Sinolink Securities, a brand-new Falcon 9 costs about $50 million to manufacture, with the $30 million first stage being recoverable. This brings the marginal cost of internal launches down to nearly $15 million.

SpaceX's cost calculations show that from 1970 to 2000, the global average cost for near-Earth orbit payload launches was $18,500/kg. Falcon 9 reduced this to $2,700/kg, while Falcon Heavy further lowered it to $1,400/kg—a 92% reduction. Full rocket reusability could reduce costs by over 99%.

Not only cheap but also user-friendly. Landing legs significantly shorten launch cycles, with recovered rockets ready for reflight after about 50 days of preparation. The 'chopstick' method could reduce this to just 1 hour—remarkably efficient.

Currently, SpaceX has completed over 650 launches, with Falcon 9 achieving a 99% success rate.

Its carrying capacity is equally impressive. Falcon 9 can lift 23 tons, Falcon Heavy 64 tons, and the third-generation Starship will soon reach 100 tons—completely surpassing traditional rocket concepts.

Affordable, reliable, and high-capacity: calling SpaceX the aerospace 'Mixue Ice Cream & Tea' isn't an exaggeration.

In the space narrative, Earth resembles an isolated island in the ocean, with SpaceX controlling the cheapest transportation off the island. While not everyone will use it, many will choose this option. If humanity enters a space exploration era, SpaceX will command significant market share and 'pricing power' for an extended period.

Around this aerospace core, Musk continuously enhances Wall Street's recognition of space narratives.

Exploiting Capitalism's Wool

Starlink represents Musk's first validated narrative.

With dramatically reduced launch costs and extremely high carrying capacity, SpaceX has taken over numerous launch missions. According to SpaceX data, in 2025 it conducted 165 launches, accounting for 85% of US and 51% of global launches; it deployed about 3,150 satellites, representing 85% of US and 70% of global satellite launches. By late 2025, SpaceX had 9,395 satellites in orbit—two-thirds of the global total.

A significant portion supports Starlink deployment.

By late March, SpaceX had deployed over 9,600 Starlink satellites with 10.3 million users.

Starlink has achieved profitability, becoming SpaceX's cash cow. In 2025, it generated $11.387 billion in revenue (+49.8% YoY) and $4.423 billion in operating profit (+120.4% YoY).

SpaceX pioneered this business, making space security increasingly important.

Examining Starlink's user base:

Individual and family users now cover 164 countries and regions, particularly in rural, remote, maritime, and aerial scenarios where terrestrial networks struggle. Monthly fees range from $40-80—not cheap in terms of speed or price.

This creates a contradiction: remote areas have limited purchasing power. Starlink offers a possibility but its high pricing may affect customer acquisition. Lower customer numbers mean reduced revenue.

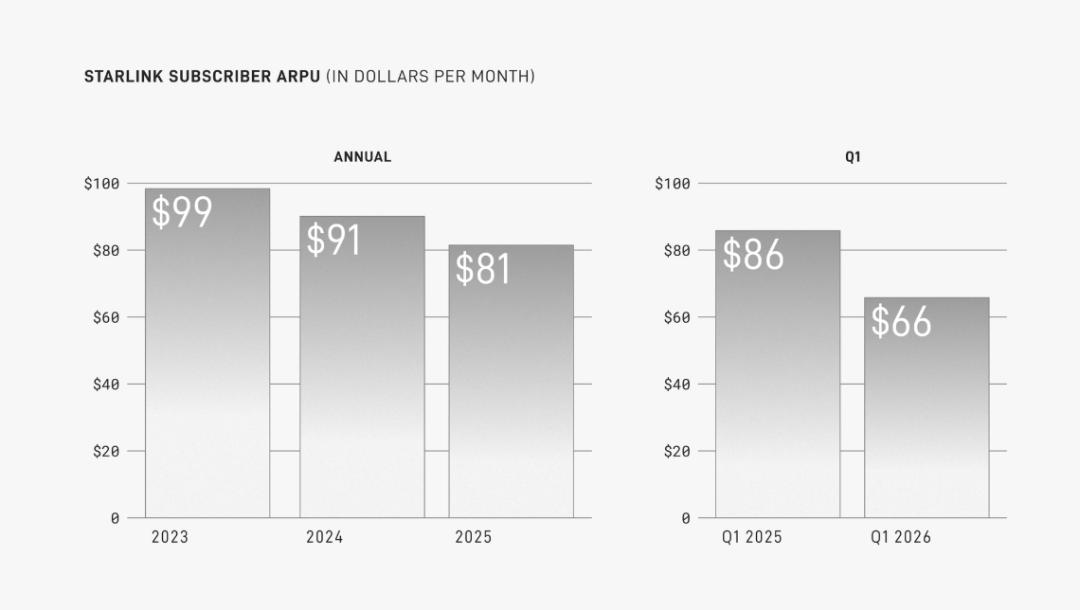

Currently, SpaceX offers lower monthly fees for remote areas. Starlink's ARPU (Average Revenue Per User) has declined yearly, from $99 in 2023 to $81 in 2025, dropping sharply to $66 in Q1 2026 to capture long-tail markets.

Enterprise, maritime, and aviation users receive dedicated network services. As corporate or government clients, SpaceX charges up to $500/month—their primary profit contributors.

Government and military users receive encrypted communication services for US defense agencies and some space traffic monitoring services.

SpaceX also envisions direct satellite-to-phone connectivity, requiring operator partnerships already in progress.

SpaceX estimates Starlink's market potential at $16 trillion (108 trillion RMB)—higher than Switzerland's GDP and ranking among the world's top 20 economies.

This estimate seems high but not entirely unreasonable.

Comparing major operators: AT&T's annual revenue is $125.648 billion, T-Mobile's $213.957 billion, and Verizon's $138.191 billion—totaling about $352.148 billion. Considering global operators, this market size could reluctantly be achieved.

However, market potential doesn't equal captured share. With only billions in revenue, Starlink faces a long path to unlock a $16 trillion market.

Starlink's true value lies in orbit resource acquisition. According to media reports, Hu Haiying, chief commander of the Qianfan constellation satellite system, noted that Starlink's 42,000 planned satellites will occupy nearly 70% of optimal low-Earth orbit positions. Space orbits and communication frequencies are non-renewable resources following first-come, first-served international rules—eliminating competitors' options.

In this scenario, Starlink may establish deep market moats in global communications, ensuring stable revenue and cash flow.

Through Starlink, Musk proved: as long as SpaceX maintains absolute pricing and efficiency advantages in satellite launches, it can craft unique narratives.

With Starlink validated, AI becomes the true dream-weaving spectacle.

Wall Street's Enchantress

According to its prospectus, SpaceX estimates the AI-related market at $26.46 trillion—equivalent to China's mainland plus Germany's GDP. Most of SpaceX's grand vision relies on AI.

Specifically: AI enterprise super-apps ($22.7 trillion); AI computing infrastructure ($2.4 trillion); consumer-end AI subscription markets ($760 billion); and AI digital advertising ($600 billion).

These four segments correspond to agents, data centers, large models, and social platforms. The latter two relate to xAI and X platform. Currently, the agent focus appears to be AI programming tool Cursor.

On June 16, SpaceX announced acquiring Cursor's parent company Anysphere through an all-stock deal, valuing Cursor at $60 billion post-acquisition.

Cursor has been a popular AI product in recent years, leading the Vibe Coding trend. However, its core experience relies on Anthropic and OpenAI models. After joining SpaceX, Cursor gains both computing power and large model support for direct code model training.

Yet from Cursor to xAI and social platforms, these remain Earth-bound activities difficult to connect with SpaceX's space narrative.

The true SpaceX connection lies in data centers.

Unlike OpenAI and Anthropic focusing solely on large models, or NVIDIA merely 'selling water,' xAI both sells water and builds large models.

Musk has proven Tesla can successfully sell water: according to the prospectus, Anthropic spends $1.25 billion monthly on SpaceX/xAI computing power. If contracts continue until May 2029, theoretical total spending could exceed $40 billion.

Computing power represents the AI industry's most scarce resource—where demand always exists. The challenge lies in building this capacity.

The current consensus is that while the US doesn't lack chips, infrastructure like electricity struggles to meet tech giants' needs, and cooling water requirements face environmental opposition. Musk proposes space-based computing power.

In March, Musk launched the ambitious Terafab project. Jointly developed by Tesla, SpaceX, and xAI, it aims to build history's largest chip factory producing 1 terawatt (TW) of AI computing chips annually—50 times current global capacity—primarily for space deployment.

To achieve this, SpaceX plans to deploy up to 1 million satellites for orbital AI data centers.

Musk's renderings show this orbital data center comprising massive satellites with enormous solar arrays. When deployed, these exceed 170 meters in length, each providing 100 kW of power exclusively for onboard AI processors.

This concept has ignited the space computing power market. According to Musk, deploying computing power in space offers major advantages: 24/7 solar energy with higher radiation intensity, no clouds or rain, and weather independence.

Additionally, it eliminates cooling water needs by using vacuum environments for radiative cooling. However, this remains controversial, with uncertainty about its feasibility. Nevertheless, the concept has gained traction, with space computing power becoming crucial for valuations and market prospects.

In summary, SpaceX's low-cost, reliable satellite launches have built formidable market moats. Starlink validated that space narratives can generate profits effortlessly. Leveraging today's hot AI trends, SpaceX comprehensively boosts its valuation.

But can SpaceX's grand vision truly match reality?

From $18.7 Billion to $1 Trillion

On foreign social media, Musk responded to a financial commentator, saying, 'I'd be surprised if revenue doesn't exceed $1 trillion by 2030.'

Assuming Musk speaks realistically, at 2025 revenue levels, SpaceX needs 121.7% CAGR over five years. Its past two-year CAGR was 34.05%, with Q1 2026 revenue growth at only 15.42%.

While no one denies Musk and SpaceX's greatness, objectively speaking, SpaceX remains largely speculative. Musk isn't infallible—consider SolarCity or Hyperloop. However, his enormous successes with Tesla, Starship, Falcon, and Starlink overshadow these failures.

Dissecting SpaceX's current main businesses.

There is indeed a generational advantage in the launch business. However, this does not mean there is no possibility of catching up.

In addition to Blue Origin, the main competitors also include Chinese companies. The former is already the world's second company to master orbital-class rocket recovery technology.

The inaugural flight of China's heavy-lift launch vehicle, the Long March 9, is scheduled for 2028, with a vehicle body that surpasses the Starship V3. In the commercial space sector, models such as the Zhuque-2 and Zhuque-3 are also catching up. Among them, the Zhuque-3 rocket attempts to integrate the architecture of the Falcon 9 with Starship technology (stainless steel body + liquid oxygen methane), although its inaugural flight and recovery failed last December.

Musk assessed that it would take 'more than five years to achieve the reliability of the Falcon 9.' However, in five years, China will be able to see SpaceX's back.

In terms of launches, SpaceX is known for its high launch efficiency and low launch costs, but it is not the only launch provider. Chinese aerospace is already renowned for its low costs, stability, and reliability. As long as there is market demand to catalyze growth, even if it cannot compress costs as much as SpaceX in the short term, Chinese aerospace can still establish its own launch capabilities.

Taking Starlink as an example, although Musk's Starlink is being built very rapidly, the deployment of the 'Chinese Starlink' will not be slow either. The reason it is slower than Starlink is that China's base station infrastructure is very well-developed, and the demand for satellite networks is not as strong.

After Starlink introduced the 'Starlink Direct to Cell' feature, the traditional operator ecosystem is facing changes, and the business prospects are becoming clearer. The 'Chinese Starlink' Qianfan constellation has already begun intensive launches, with a Phase 1 target of 1,296 satellites to be completed by 2027; Phase 2 will add approximately 10,000 satellites, with the network of over 10,000 satellites to be completed by 2030; and the final phase will exceed 15,000 satellites, integrating into the 6G ecosystem.

Therefore, if the market space is validated, commercial competition at the Starlink level may have just begun. Starlink aims to seize market share from traditional operators and will then face competition from across the ocean. This market will not allow SpaceX to easily monopolize it.

AI represents an even more long-term competition. Starting with large models, xAI struggles to rank among the top in the United States, lagging behind competitors such as Anthropic, OpenAI, and Google.

In the Terafab project, whether the chip manufacturing factory can be competitive remains highly uncertain. This may be the most challenging business on the planet. It requires not only capital but also deep process technology accumulated through years of large-scale production. Even if the factory is successfully built, controlling yield rates will be a significant challenge.

Morgan Stanley believes that such a project could cost over $20 billion and take several years to complete. Integrating logic, memory, and advanced packaging technologies runs counter to the decades-long trend of industry specialization.

In addition, Terafab faces issues of supplier concentration and talent bottlenecks. Advanced extreme ultraviolet lithography systems rely on a few suppliers, and there is a gap in semiconductor engineering talent reserves, fab construction experience, and supply chain maturity compared to TSMC and Samsung. Therefore, on the Terafab project, SpaceX has to collaborate with Samsung, Intel, and others.

As for the space data center, on the one hand, this project still needs validation, and on the other hand, SpaceX is not the only one optimistic about it.

Space-based computing power has also been recognized by Amazon's Bezos. Bezos predicts that gigawatt-scale facilities will take to the skies within 10 to 20 years, firmly believe (he firmly believes) that space data centers will 'defeat ground-based facilities in terms of cost.' Considering that Amazon Web Services holds over 30% of the global cloud computing market share, Amazon could deeply integrate space data centers with AI cloud services in the future, building an orbital version of AWS, which would be more competitive and have clearer business prospects than SpaceX.

SpaceX may be the most unique entity on the planet to date. It is nearly impossible to find any comparable company or business model. Rooted in rocket launches, it provides a narrative of space exploration, aiming for the stars and the sea. Leading humanity in a great voyage into space gives SpaceX a certain inherent 'nobility.'

However, returning to rationality, the scenarios Musk depicts are incredibly grand but must ultimately come down to the 'mundane' aspects of daily life. The reality for SpaceX is that its revenue is in the tens of billions, and from launches to Starlink to AI, it faces no shortage of competitors and consumes vast amounts of capital. The fervent AI boom represents the best opportunity for SpaceX to replenish its resources at this stage.

-

![]()

Oil Prices Revert to 7-Yuan Range: Are Gasoline Cars Getting a Reprieve?

-

![]()

Momenta Secures CSRC Approval: Is It Poised to Be the 'Pioneer in Physical AI Stocks'?

-

![]()

What's the Use of Having a General-Purpose Motion 'Cerebellum' for Humanoid Robots?

-

![]()

Volkswagen Starts Operating at a Production Capacity of 9 Million Vehicles

-

![]()

Interpretation of China's Auto Market in May: A Fig Leaf, Two Fault Zones, and Three Surprises

-

![]()

China's Auto Industry Accelerates Expansion in Spain: From Vehicle Sales to 'Local Manufacturing in Europe'

-

![]()

Momenta | Going Public Not for Money

-

![]()

How Much Can Doubao Make by Charging Fees?