OPPO and Vivo Raise Prices Together: A Major Upheaval in the 2026 Smartphone Market

03/17 2026

03/17 2026

608

608

Where Will Smartphone Makers Turn Amid the Price Hike Wave?

Who could have imagined that the smartphone industry would face its fiercest and most widespread wave of price hikes in five years in 2026?

On March 16, OPPO's official website showed significant price increases for some of its phones; among them, the OnePlus 15 and Ace 6 rose by 500 yuan; the Ace 6T, Turbo 6, and Turbo 6V increased by 200 yuan; and the K series saw hikes ranging from 200 to 500 yuan.

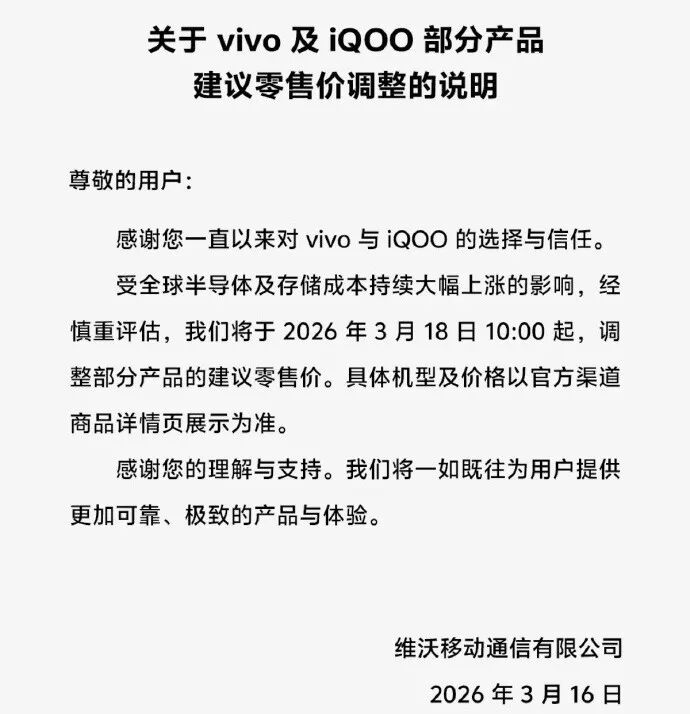

Additionally, Vivo and iQOO released pricing adjustment notices on the same day, announcing that they would revise the suggested retail prices of certain products on March 18.

Image Source: Vivo

The sharp rise in memory chip prices has significantly driven up the overall costs in the smartphone industry, with many leading manufacturers signaling impending price increases. Currently, Xiaomi, Huawei, and Honor have not officially announced specific price hikes, though some Xiaomi store employees noted that many models are already out of stock. Lei Jun, during the recently concluded "Two Sessions," publicly responded that they would "explore various methods to minimize the difficulty for consumers in accepting (price increases)."

Under cost pressures, leading manufacturers are adjusting their strategies. Where will the industry's new growth points emerge? How long will this wave of significant price hikes last, and how can mid-tier smartphone manufacturers with limited market share find new ways to survive?

01. Reshuffling in the Smartphone Market

Memory chips are a must-have for smartphones, accounting for 10%-15% of costs across models from low-end to high-end and flagship devices. However, since last year, due to surging demand for AI computing power, memory chip suppliers have had to prioritize supply for large model manufacturers, significantly squeezing consumer-grade smartphone memory production capacity and sending prices soaring.

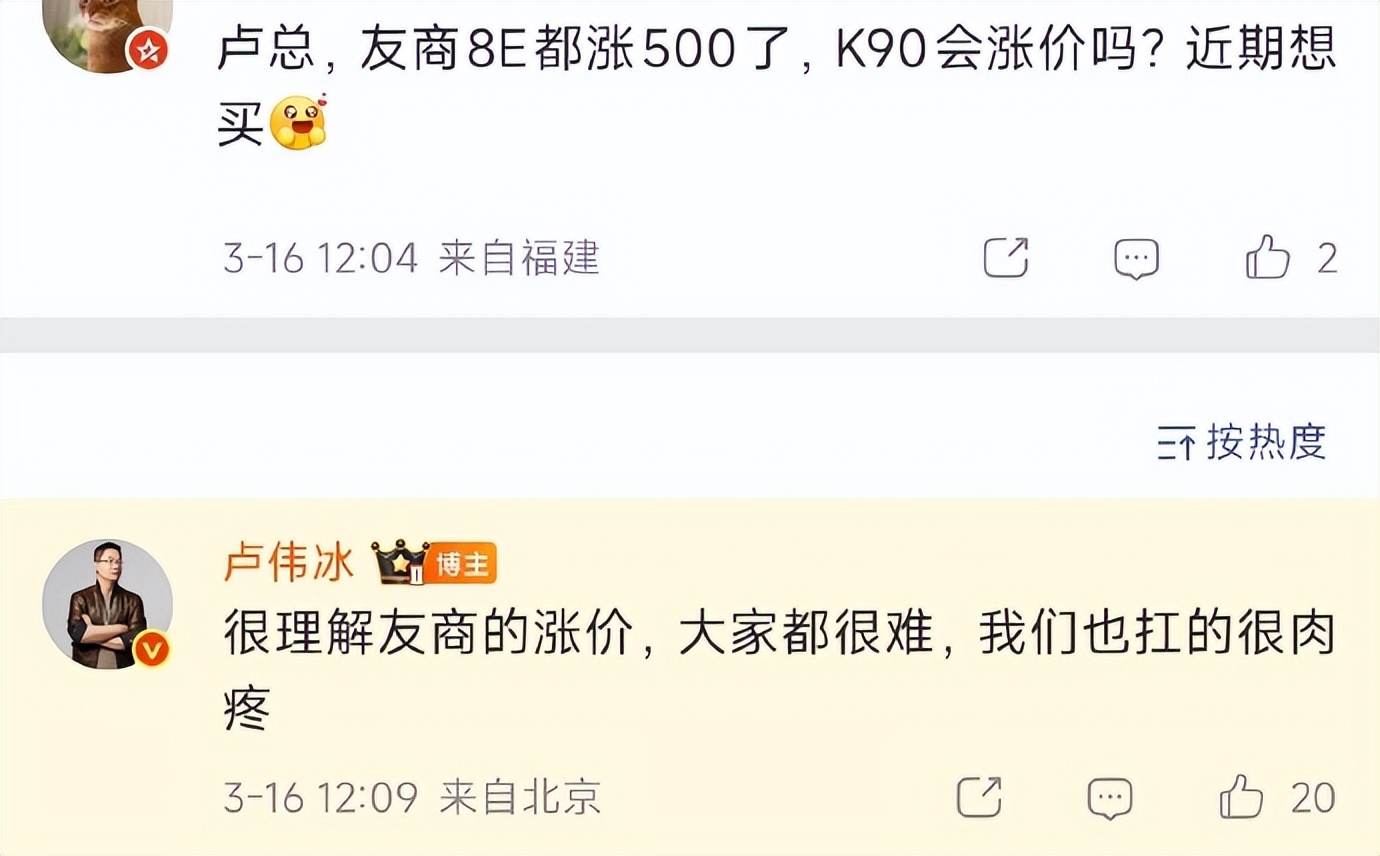

Lu Weibing, Partner and President of Xiaomi Group, stated in an interview that the current upward trend in memory prices has been exceptionally rapid, with quotes in the first quarter of this year nearly four times those of the same period last year.

Image Source: Weibo Screenshot

According to a Counterpoint research report, memory costs will account for up to 43% of low-end smartphones priced under 1,000 yuan, with DRAM (memory) and NAND (storage) costs rising to 20% and 16%, respectively, for mid-range models. For flagship models with wholesale prices exceeding $800, DRAM and NAND will account for 23% and 18% of total costs, respectively.

Notably, besides memory chips, core components such as high-end OLED screens, large-capacity high-density batteries, and thermal materials are also rising in price, pushing the smartphone industry into a cycle of cost increases across the entire supply chain. Cost pressures from upstream suppliers are being passed down through the supply chain to end consumers. To manufacturers' dismay, this round of price hikes is not a short-term fluctuation but a sustained cost pressure.

According to the latest supply chain news, global memory giants Samsung Electronics and SK Hynix have officially issued notices planning to continue raising DRAM memory prices in the second quarter of 2026, with a unified increase of about 40% expected for DDR5 particles (core memory units). Industry insiders predict that this round of price hikes, which began in the second half of 2025, will continue until the end of 2027.

Mid-to-low-end models are the hardest hit by the price hikes. OPPO's first price adjustments were for its A and K series products priced between 1,000-2,500 yuan; the topic "Xiaomi's Redmi Turbo 5 to increase by 100 yuan" also recently trended on social media. Realme, which has long focused on the mid-to-low-end market, announced its return to OPPO, a move seen by many as a response to cost pressures and a realignment of business lines.

Additionally, some high-end and flagship models have also been affected. While Honor maintained the starting price of its foldable flagship Magic V6, larger storage versions saw a direct increase of 1,000 yuan compared to the previous generation.

Image Source: Weibo Screenshot

Yuan Shuai, co-founder of the New Intellectual Productivity Salon, believes that prioritizing adjustments to mid-to-low-end models is because these users are price-sensitive but less dependent on brand premium, allowing for effective cost pressure transmission with minor price increases. Flagship models, as the core of brand image, benefit more from stable pricing to consolidate their position in the high-end market.

Currently, the domestic smartphone market is a red ocean of inventory competition. Despite ongoing government subsidies, smartphone shipments are declining; IDC reports show that China's smartphone market shipped approximately 285 million units in 2025, down 0.6% year-on-year. With widespread price hikes across all phone tiers, consumer enthusiasm for upgrades may further diminish, especially in the price-sensitive mid-to-low-end market.

This poses a significant challenge for mid-tier smartphone manufacturers. Domestically, Huawei, OPPO, Vivo, Xiaomi, Honor, and Apple account for nearly 80% of the market share. Mid-tier manufacturers are already at a disadvantage in supply chain bargaining power, channel coverage, and brand recognition. Now, facing the dual pressures of soaring costs and shrinking demand, their survival space is being further compressed.

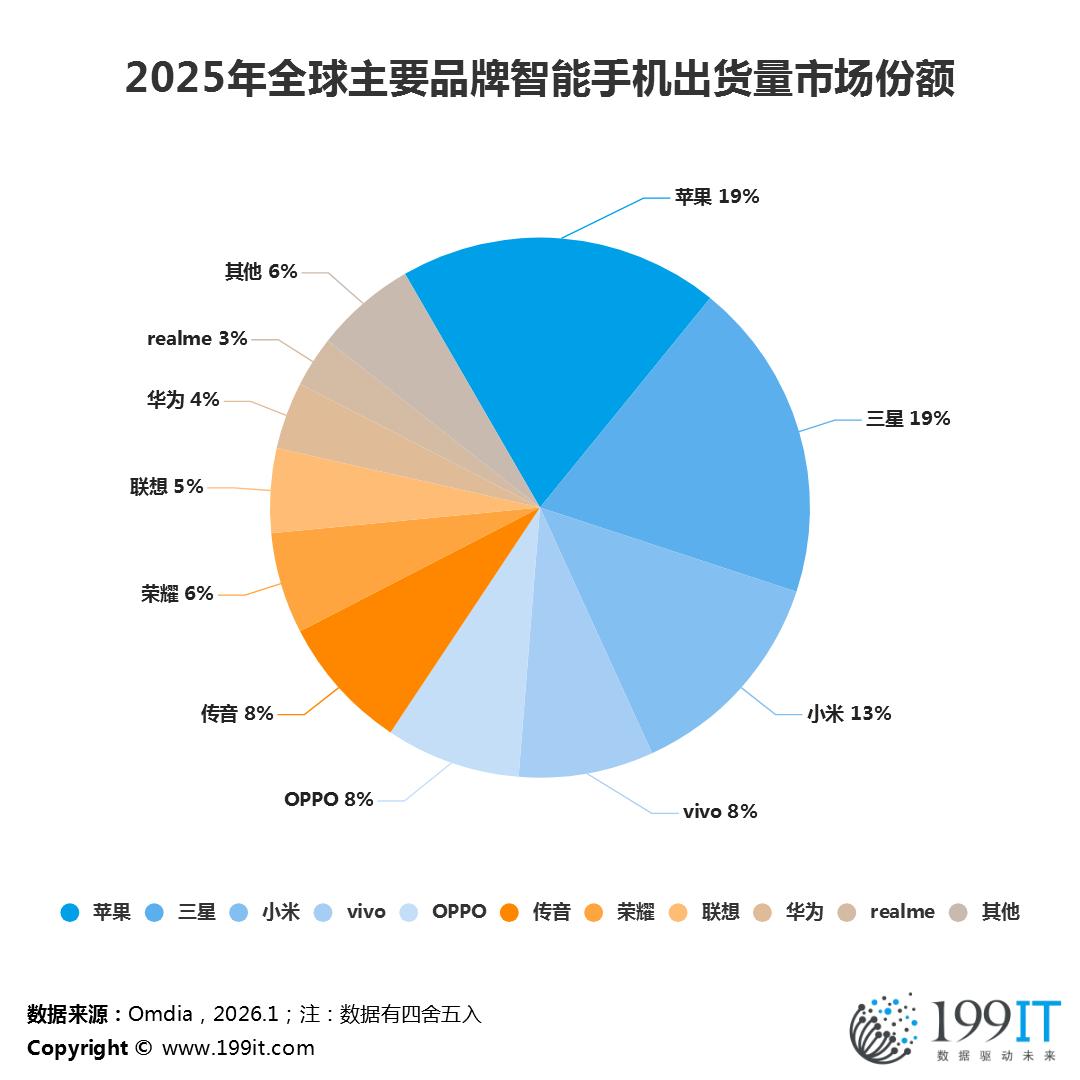

Image Source: 199IT Internet Data Center

In February of this year, Meizu officially announced the suspension of independent research and development of new domestic smartphone models, marking a symbolic exit signal in this round of market consolidation. Other mid-tier manufacturers, such as ZTE's RedMagic and Nubia, which have carved out niches through differentiated competition, will face severe tests of their parent companies' procurement capabilities and bargaining power to survive this prolonged wave of price hikes.

02. Is AI the New Battleground?

In recent years, smartphone manufacturers' focus on camera and battery life improvements has struggled to reignite consumer enthusiasm for upgrades. To find new growth opportunities, the smartphone industry's competition is gradually shifting toward AI—evolving from "passive command execution tools" to on-device AI agents capable of understanding, planning, and acting on behalf of users.

In December last year, ByteDance launched an AI phone assistant based on its large model Doubao, integrated into the Nubia M153 developed in collaboration with ZTE. Priced at 3,499 yuan, the phone sold out quickly in a limited release, and ZTE's stock price surged by the daily limit on the same day. Ni Fei, CEO of Nubia, publicly stated that the development trend of AI phones is irreversible and emphasized "open collaboration" as the path forward.

Image Source: Weibo Screenshot

For small and medium-sized manufacturers, focusing on hardware adaptation and mass production without incurring huge R&D costs to quickly ride the AI phone wave is undoubtedly a cost-effective choice.

Media reports suggest that for manufacturers with low domestic market share, such as Transsion and Lenovo, Doubao Phone's collaboration model involves setting up a direct Doubao AI entry point within their phones, similar to the "Seres-Huawei" partnership model. These manufacturers would need to pay technology licensing fees and AI service subscription fees to Doubao.

For leading smartphone manufacturers with well-established self-developed ecosystems, the preference is to maintain control over the system layer and AI entry points rather than collaborate with model providers.

Leading manufacturers have long explored system-level AI assistants. Xiaomi fully integrated AI capabilities with the release of HyperOS in 2023; OPPO debuted its on-device Andes large model with the Find X7 series in 2024; Huawei laid the groundwork for its Xiaoyi assistant as early as 2018. By the second half of 2025, flagship models from leading manufacturers had upgraded their AI capabilities from voice assistants to intelligent assistants capable of cross-application execution.

The buzz around Doubao Phone stems from its ability to autonomously handle full-process tasks. Through a system-level GUI Agent, the AI assistant can accurately identify screen content, simulate clicks, swipes, and inputs like a real person, and independently complete complex cross-APP, multi-step tasks without relying on third-party API access—such as placing orders via voice commands, comparing prices, and ordering food delivery (only the payment step requires manual operation).

However, Doubao Phone's GUI Agent technology, which requires high system permissions to simulate clicks, swipes, and inputs, has sparked significant privacy concerns and even faced bans from internet platforms. Applications under Alibaba's ecosystem, such as Taobao, Xianyu, and Damai, as well as social platforms like WeChat and Xiaohongshu, experience login abnormalities when used with Doubao Phone. Industry insiders point out that the simulated operation method closely resembles the operational logic of black-market botnets and cheat scripts, raising platform concerns about permission abuse leading to account theft, financial fraud, and privacy breaches. Nevertheless, some security researchers argue that Doubao Phone's risk control and identification issues are not particularly difficult to resolve.

Image Source: Weibo Screenshot

Currently, there are two mainstream technical routes for AI phones. Besides Doubao Phone's GUI Agent approach, Huawei and OPPO have adopted the A2A route, which eliminates the need for an AI operation interface and instead invokes App capabilities through standardized interfaces, leaving execution to the Apps themselves. This method is more secure and stable but highly dependent on Apps granting permission. The primary challenge for this route will be how smartphone manufacturers can establish deep collaborations with more applications.

Overall, the upcoming AI phone era will test not just algorithmic capabilities or hardware integration but also the breadth and depth of ecosystem building. Whoever can deploy stronger on-device models and break down app silos to establish cross-platform service loops will gain the discourse power to define the next generation of intelligent terminals.

Beyond software and system AI integration, some smartphone manufacturers are also innovating in hardware form factors. For example, Honor's recently released ROBOT Phone adds a stabilized gimbal to its rear camera, attracting many professional filmmakers. Additionally, this camera integrates with Honor's "AI Agent Brain," enabling the phone to capture external information from different angles like an eye, providing data support for the system's AI assistant.

Image Source: Weibo Screenshot

It is evident that smartphone manufacturers are exploring survival strategies for the AI era on multiple fronts. While the price hike wave compresses profit margins, it also accelerates innovation cycles. The 2026 smartphone market will no longer be a simple competition of specs and prices; who can deliver more hardcore achievements in AI experiences, ecosystem collaboration, and hardware innovation warrants further attention.

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan