Goertek: Conquering Vietnam's 'Recruitment Hurdle', Can Gross Margin Rebound and Growth Break Free from Stagnation?

04/27 2026

04/27 2026

447

447

On the evening of April 23, 2026 (Beijing Time), following the close of A-share market hours, Goertek Inc. unveiled its Q1 2026 financial report along with the 2025 annual report (as of March 2026). Here are the key takeaways:

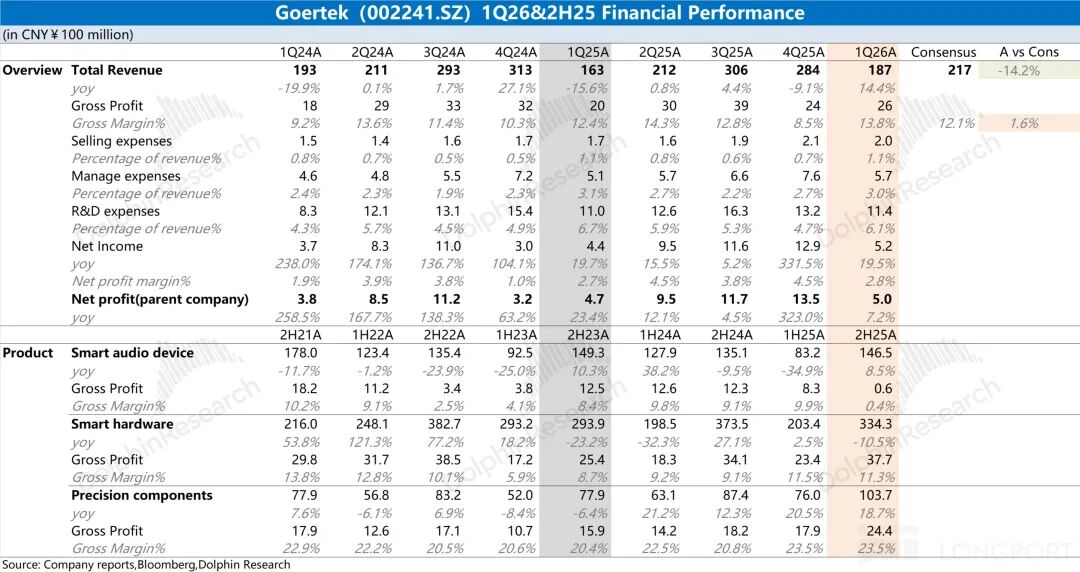

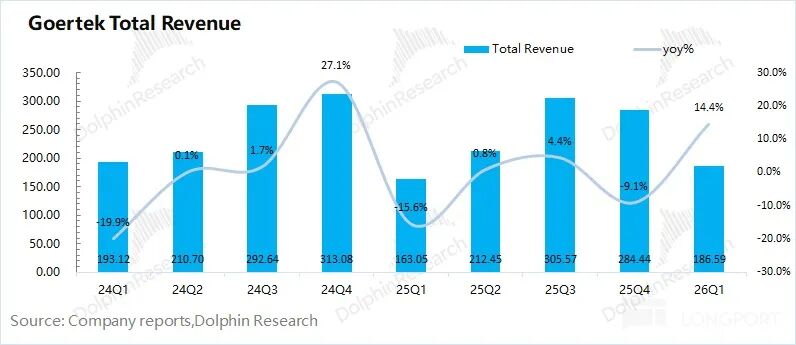

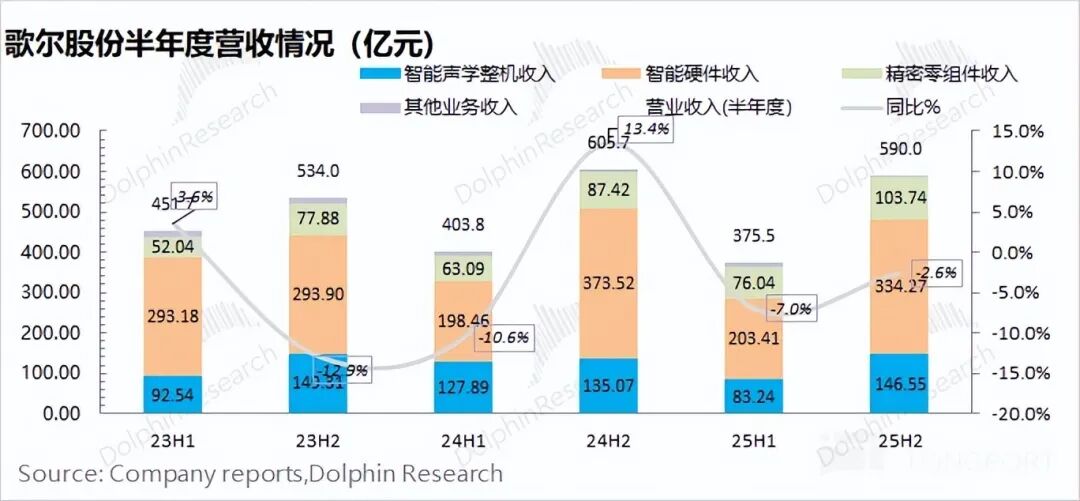

1. Overall Performance: $Goertek Inc.(002241.SZ)$ reported a total revenue of RMB 18.7 billion in Q1 2026, marking a 14% year-on-year increase. While revenue rebounded this quarter, primarily buoyed by growth in smart components and other businesses, it still fell significantly short of market expectations (RMB 21.7 billion).

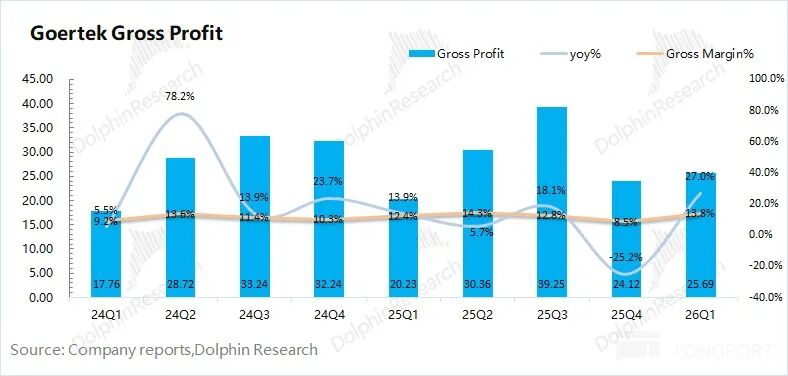

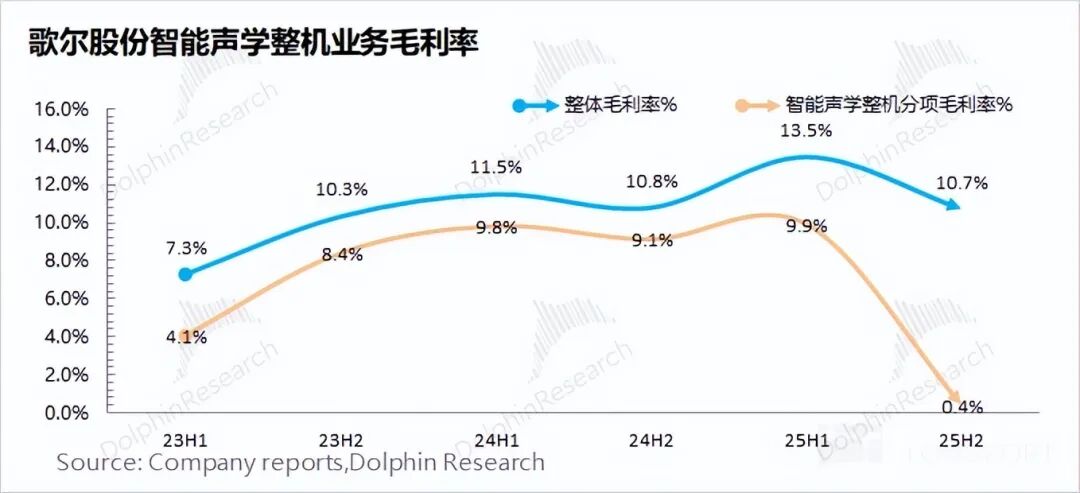

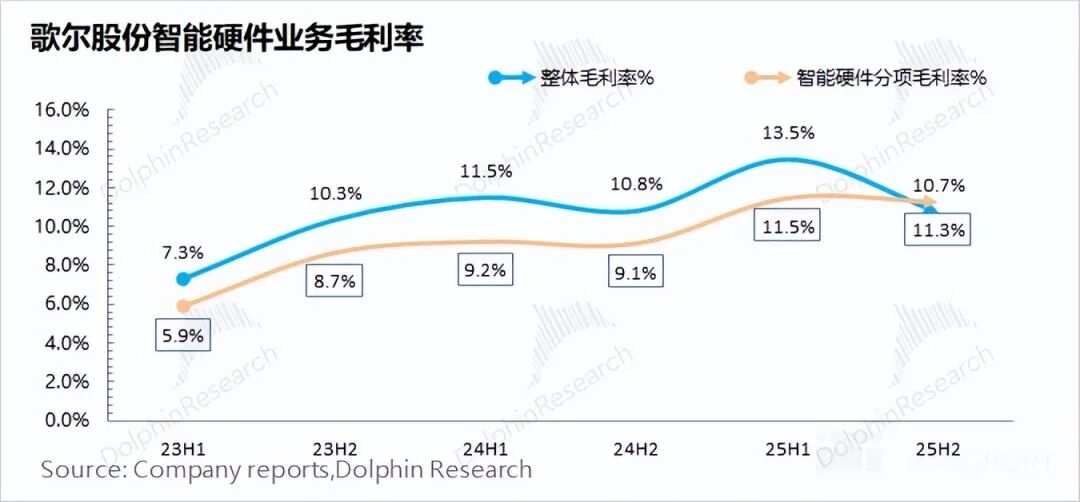

The company's gross margin for the quarter stood at 13.8%, up by 1.4 percentage points year-on-year. The notable fluctuations in gross margin over the past two quarters were largely influenced by substantial swings in the gross margin of the smart acoustic device business. The significant recovery in the overall gross margin underscores the restoration of order share.

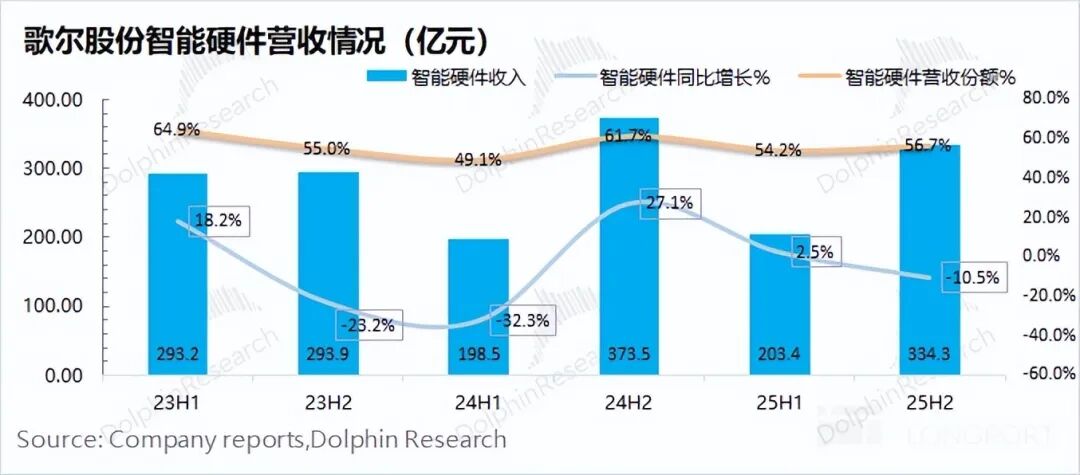

2. Smart Hardware Business: Revenue in the second half of 2025 amounted to RMB 33.4 billion, a 10% year-on-year decline. This contraction was attributed to shrinking shipments of the company's older product lines (PS series, older Quest models), coupled with the absence of 'star' products in the new product lines (AI glasses, next-gen MR).

3. Traditional Hardware and Components

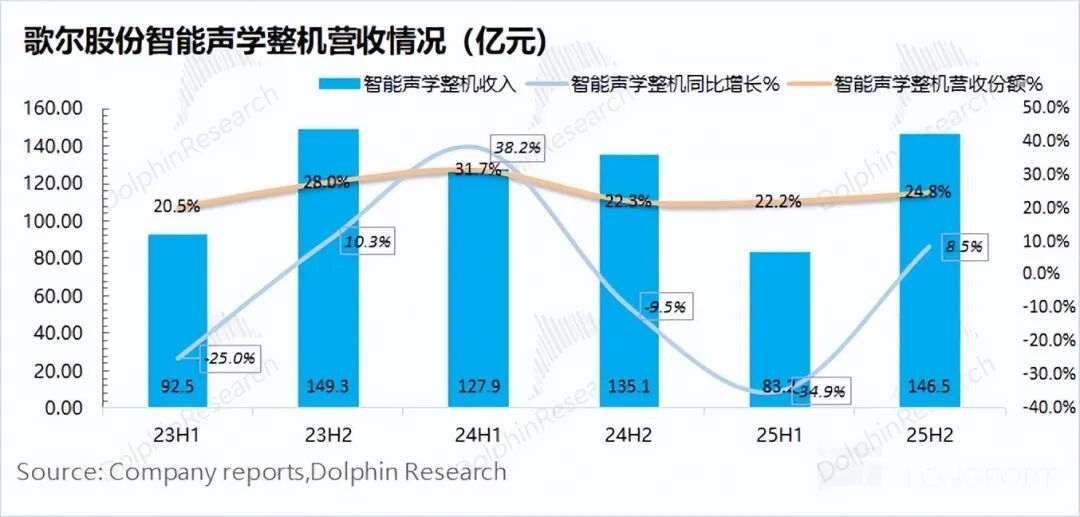

① Smart Acoustic Devices: Generated RMB 14.6 billion in revenue in the second half of 2025, an 8.5% year-on-year increase, primarily driven by product iteration cycles. The launch of the 2025 new AirPods model spurred demand but did not significantly boost sales volume. Regarding the gross margin of smart acoustic devices—a focal point of market attention—it has largely rebounded to around 10%, signaling a significant recovery in the company's market share.

The sharp decline in gross margin to around 0.4% in the second half of 2025 was primarily attributed to the impact of 'U.S.-China tariff policies.' This led the company to shift relevant production capacity to its Vietnam factory. Concurrently, many peers also set up factories and recruited workers in Vietnam, prompting the company to adopt a 'high-cost recruitment' strategy. This substantially increased labor costs and temporarily depressed the company's gross margin.

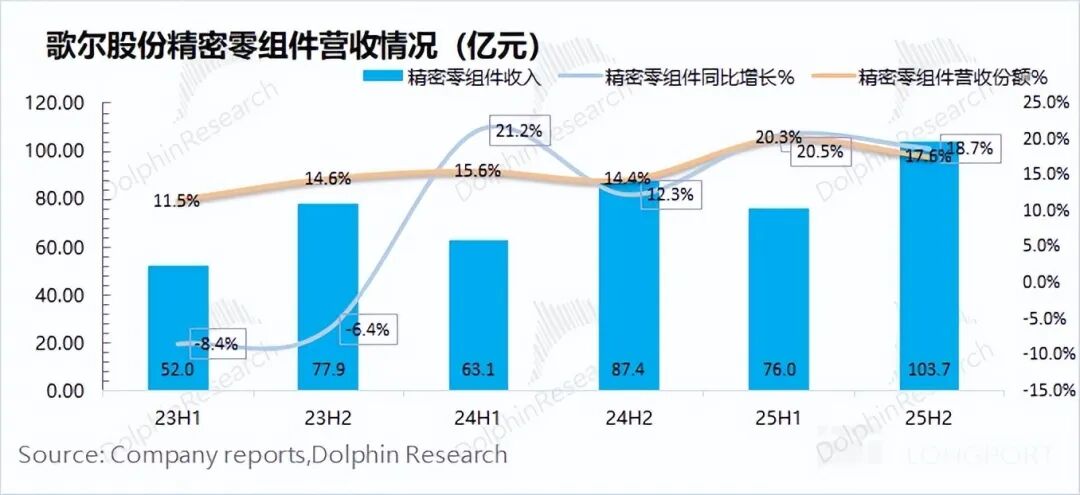

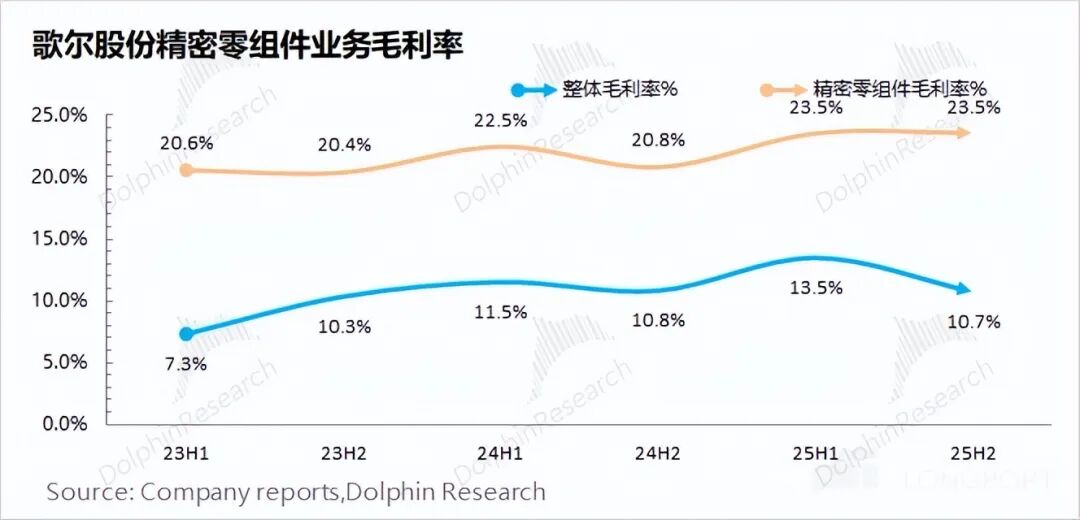

② Precision Components: Generated RMB 10.4 billion in revenue in the second half of 2025, an 18.7% year-on-year increase. This business segment remains the most stable. Despite relatively sluggish downstream electronics demand due to tightened national subsidies, market demand for high-end components continues to drive growth through product upgrades.

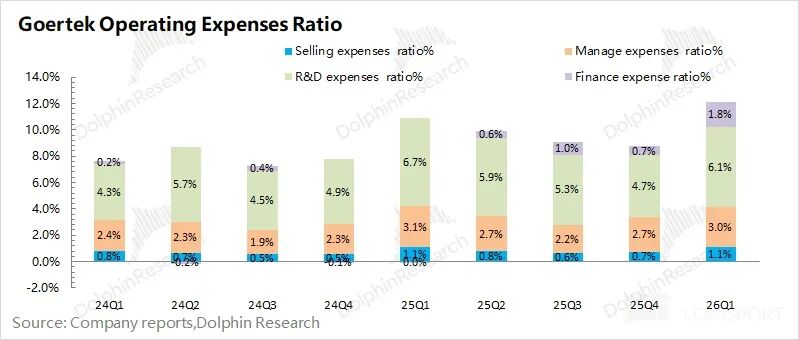

4. Expenses and Operating Conditions: The company's three core operating expenses totaled RMB 1.9 billion this quarter, with a core expense ratio of 10%, remaining relatively stable year-on-year. Inventory stood at RMB 13.56 billion this quarter, up by RMB 480 million quarter-on-quarter. The inventory-to-revenue ratio was 0.73, indicating a rise in inventory levels.

Dolphin Research's Overall View: Gross Margin 'Resurrected,' but Growth Engine Still in 'Transition'

Goertek's Q1 financial report was relatively unremarkable. While revenue and gross margin improved year-on-year, revenue fell short of market expectations. On a positive note, the rebound in gross margin this quarter suggests that the decline in the second half of 2025 was a sudden 'short-term impact.'

Given the limited data in the Q1 report, combined with insights from the company's annual report:

a) Smart Acoustic Device Business: Although it rebounded, it remains sluggish, primarily because the new AirPods models released by the company's major client (Apple) in September did not become market sensations.

b) Smart Hardware Business: Experienced a double-digit decline, mainly due to being in a 'transition' phase between old and new products. Within smart hardware, the company's largest revenue sources are gaming consoles and VR/MR, being a primary supplier for PS5 and Oculus. However, PS5 is now in the latter stage of its lifecycle, and Oculus 3S has underperformed.

On the other hand, AI smart glasses are still in the early stages of their product cycle, with no 'star' products yet, contributing to the company's lackluster smart hardware performance.

c) Precision Components Business: Maintained double-digit growth and remains the company's most stable segment. Even amid relatively weak downstream electronics demand, the precision components business is expected to benefit from value upgrades and increased penetration of proprietary components.

The most significant concern in the annual report was the sharp decline in the gross margin of smart acoustic devices to 0.4%.

The 'sudden collapse' in gross margin in the second half of 2025 was primarily due to: (1) the impact of U.S.-China tariff policies, which led many electronics manufacturers to expand production/recruit workers in Vietnam in the second half, causing a 'temporary labor shortage' in the Vietnamese labor market and necessitating 'high-cost recruitment'; (2) the concentration of smart acoustic device production in Vietnam, which is inherently labor-intensive assembly work; and (3) the peak shipment period for smart acoustic devices (AirPods) occurring in the second half.

Dolphin Research views this as a temporary impact caused by 'labor misallocation' in the short term. The Q1 gross margin confirms that this is not a long-term effect.

Overall, Goertek's gross margin rebound this quarter indicates a restoration of market share among major clients and the elimination of labor cost impacts. However, even with this recovery, the company's growth trajectory remains uncertain.

The current end-of-lifecycle status of PS5 and the sluggish performance of Oculus will continue to exert pressure on the company, while AI glasses have yet to produce a 'hit' product, leaving smart hardware in a 'transitional' phase. Coupled with the headwind of USD depreciation (nearly 90% of revenue comes from overseas), the company's performance and valuation will remain under pressure.

Below are Goertek's financial report and related data charts:

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting requires authorization.

// Disclaimer and General Disclosure

This report is intended solely for general comprehensive data purposes, catering to the general reading and data reference needs of users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses arising from the use of the data in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives but does not guarantee the reliability, accuracy, or completeness of the information and data.

The information or views mentioned in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and data in this report are not intended for distribution to or use by individuals or residents of jurisdictions where such distribution, publication, provision, or use contradicts applicable laws or regulations or requires Dolphin Research and/or its subsidiaries or affiliates to comply with any registration or licensing requirements in such jurisdictions.

This report reflects only the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, with copyright solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all related rights.

-

How can we elevate autonomous driving scene understanding from 2D to 3D?

-

![]()

DeepSeek V4: Chinese Computing Power, Chinese Model, Chinese Pace

-

AI Adoption Becomes a Stringent Benchmark: Big Factory Workers Find Themselves 'Ensnared' by AI

-

![]()

Beijing Auto Show: No Dominant 'Star Car', but Three Key Tech Battles That Shape the Future

-

![]()

Is the Prompt Outdated? GPT-5.5 Now Has Intuition—Just Specify the Goal and AI Takes Over Automatically

-

![]()

Cook Passes the Torch: Apple Bolsters Its Position in China’s Competitive Market

-

![]()

Cash Flow Soars by 1147%! Delving into O-Film Tech's Q1 Financial Report

-

![]()

60,000 Domestic Cards Train Trillion-Parameter Models: What Do LongCat and DeepSeek Validate?