Cook Passes the Torch: Apple Bolsters Its Position in China’s Competitive Market

04/27 2026

04/27 2026

551

551

By Xiaofeng

Source: Bowang Finance

Apple welcomes a new leader, but the competitive landscape it leaves behind in the Chinese market is more intense than ever.

Tim Cook will officially step down as Apple's CEO on September 1 and take on the role of Executive Chairman of the Board. This news left many long-time Apple fans in attendance in disbelief, especially considering that Apple, despite this leadership transition, achieved 4% growth last year. This made it one of only two mainstream brands to see positive growth in 2025.

This accomplishment was achieved while Apple focused solely on high-end models priced above 4,000 RMB. A CEO on the brink of retirement managed to deliver one of Apple's most remarkable performances in the Chinese market before his departure.

Despite years of external criticism regarding Apple's incremental innovation approach, the success of the iPhone 17 series demonstrates that Apple still holds significant sway in the Chinese market, built on years of cultivating user loyalty.

As Cook hands over the reins to hardware engineer John Ternus, the Chinese smartphone market has quietly entered a new phase: the decade-long narrative of "domestic brands catching up" has concluded, and what lies ahead is an even more intense direct competition between Apple and Chinese manufacturers in the high-end market.

01

Apple Ups the Ante in China

Apple's market share trajectory in China has been a rollercoaster ride. In 2023, it was relegated to the "Others" category by domestic brands; in 2024, it managed to hold its ground with minor upgrades to the iPhone 16 series; in the fourth quarter of 2025, it made a strong comeback with robust single-quarter performance; and in the first quarter of 2026, Apple surged directly into the top two domestic rankings, according to IDC.

Behind this performance lies Cook's final, strategic move in a key market. Rather than pursuing radical innovation, Apple opted for the safest and most effective strategy: price adjustments.

The iPhone 17 series maintained its starting price of 5,999 RMB while introducing the most affordable iPhone ever—the iPhone 17e, priced at 3,999 RMB, directly entering the core price range of domestic flagship models. On the evening of January 23, Apple announced a 2,000 RMB price cut for the iPhone Air, bringing its starting price down to 5,499 RMB after national subsidies. At a time when domestic manufacturers were raising prices due to increased chip and storage costs, Apple offered "more for the same price," sacrificing some brand premium for market share.

More critically, Cook's decade-long efforts in building a Chinese supply chain ecosystem proved pivotal. From Foxconn in Zhengzhou to component suppliers in Shenzhen, deep integration gave Apple unparalleled advantages in cost control and production flexibility.

What Cook leaves Ternus is a Chinese market that appears stable but is actually fraught with challenges. Apple boasts approximately 270 million active users in China, forming a high-value, highly loyal customer base.

This tug-of-war reveals a harsh reality: Apple's once-unchallenged dominance in the Chinese market is a thing of the past. In the past, a new iPhone release could easily capture significant high-end market share. Now, Apple must humble itself and compete with domestic brands at every price point.

The market never waits for anyone's departure. Cook's exit marks the end of Apple's "supply chain-driven" era. Ternus, the new CEO with a hardware engineering background, will lead Apple into a "technology innovation" phase, with the Chinese market serving as his first major test.

02

Domestic Smartphone Brands Lack Cohesion

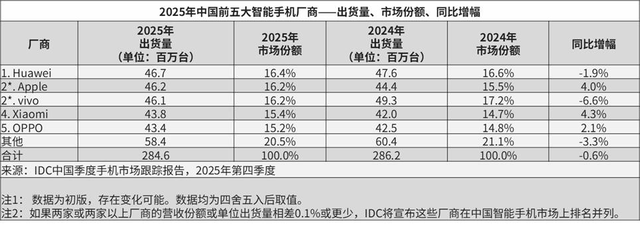

While Apple surges ahead, the domestic smartphone camp is mired in unprecedented internal competition. IDC data shows that in 2025, total smartphone shipments in China reached approximately 285 million units, down 0.6% year-on-year, with an expected 10% decline in the current year. This represents a mature, stagnant market where no brand can remain unscathed, and there is no such thing as a "domestic alliance."

Competition among manufacturers has reached the point of fighting over every unit sold. IDC's 2025 rankings show Huawei, Apple, Vivo, Xiaomi, and OPPO in the top five. Notably, the gap between these leading brands is minimal, with all holding over 15% market share and the difference between first and fourth place being less than 3 million units. Growth for any manufacturer comes at the expense of others.

Competition is particularly fierce in the high-end segment, though results have been underwhelming.

In other words, despite years of "premiumization" rhetoric from domestic brands, only Huawei has achieved true scale in this area. In the 4,000 RMB+ segment, Huawei and Apple dominate nearly 80% of the market, forming an entrenched duopoly built on years of system and chip development and brand loyalty. Moreover, Apple's 4% shipment growth in 2025 made it the second-fastest-growing brand in China, putting pressure on other manufacturers.

The remaining high-end market share is fragmented among various brands. While domestic manufacturers collectively match Apple in overall shipments, they lag significantly in profitability and brand value. For example, the OPPO Find X9 Pro debuted with Hasselblad 8K photography capabilities, but such features remain incremental in the broader premiumization effort.

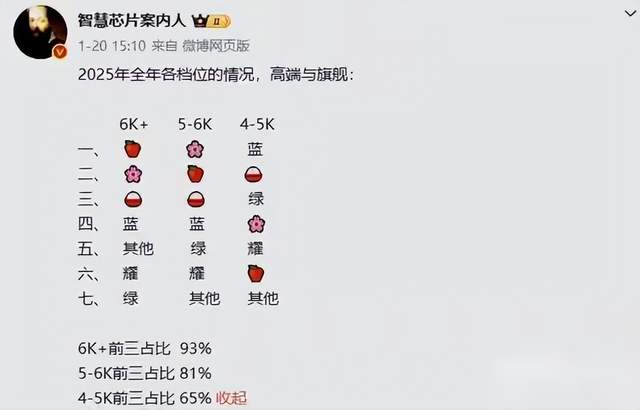

Similarly, Xiaomi, ranked fourth by IDC in 2025, has seen its flagship models gain momentum from its automotive business, with the Xiaomi 14, 15, and 17 series performing well. However, it still trails Apple and Huawei. According to CNMO Technology, citing a tech blogger's leaks, Apple dominates the 6,000 RMB+ ultra-premium segment with 93% market share, followed by Huawei and Xiaomi. In the 4,000–5,000 RMB range, competition is more dispersed, led by Vivo, Xiaomi, and OPPO, who collectively hold 65% share.

Why have domestic brands struggled in the high-end market?

The fundamental issue lies in the fact that core technologies and brand prestige required for premium smartphones represent a long-term battle. The market is the ultimate judge. While consumers willingly pay a premium for Apple's brand, some domestic manufacturers remain trapped in the low-to-mid-end market. Until this changes, domestic brands will continue to play second fiddle to Apple.

03

The Apple-Domestic Rivalry Will Persist

The rise of AI has introduced new variables to this competition. IDC projects that AI smartphone shipments in China will reach 147 million units in 2026, up 31.6% year-on-year, accounting for 53% of the market. AI has evolved from a marketing buzzword to a standard feature. Both Apple and domestic manufacturers now view AI as their next battleground, with a fierce contest for intelligent experiences underway.

Apple's AI strategy emphasizes "slow and steady refinement." While it lagged domestic rivals by nearly a year in launching generative AI features, iOS 19's deep integration of Apple Intelligence offers clear advantages in privacy and system fluidity. Apple's approach is to weave AI capabilities seamlessly into the OS, enhancing user experience subtly.

Domestic manufacturers, in contrast, adopt an "aggressive offensive" strategy. Huawei leverages its HarmonyOS ecosystem to establish an early lead in AI smartphones. Xiaomi, Vivo, and OPPO have also introduced AI-driven innovations, from imaging to productivity tools, rapidly incorporating the latest technologies into their products. While this agility is an advantage, the industry also suffers from feature overload and inconsistent user experiences.

This AI battle essentially pits different development models against each other.

What is certain is that the direct competition between Apple and domestic manufacturers in the high-end market will persist for the next three to five years. Apple will continue leveraging its brand and ecosystem to solidify its premium position, while domestic brands will seek breakthroughs in AI, foldable displays, and other emerging areas to challenge Apple's dominance.

Cook may step down as CEO in a few months, but Apple's story is far from over. The rise of domestic smartphones also has a long way to go. The tug-of-war in China's smartphone market will continue unabated.

-

How can we elevate autonomous driving scene understanding from 2D to 3D?

-

![]()

DeepSeek V4: Chinese Computing Power, Chinese Model, Chinese Pace

-

AI Adoption Becomes a Stringent Benchmark: Big Factory Workers Find Themselves 'Ensnared' by AI

-

![]()

Beijing Auto Show: No Dominant 'Star Car', but Three Key Tech Battles That Shape the Future

-

![]()

Is the Prompt Outdated? GPT-5.5 Now Has Intuition—Just Specify the Goal and AI Takes Over Automatically

-

![]()

Cook Passes the Torch: Apple Bolsters Its Position in China’s Competitive Market

-

![]()

Cash Flow Soars by 1147%! Delving into O-Film Tech's Q1 Financial Report

-

![]()

60,000 Domestic Cards Train Trillion-Parameter Models: What Do LongCat and DeepSeek Validate?