Spotify: 'Plunge' Caused by Unmet Expectations, Streaming Becomes Old Flame

04/30 2026

04/30 2026

377

377

Spotify's Q1 2026 earnings report was released before the U.S. stock market opened on April 28. The main issue in the report lies in the guidance. The market still expects the traditional logic of 'raising prices to boost profits' for streaming services. However, in Spotify's Q2 guidance, key metrics such as net new subscription users and gross margin failed to fully 'meet expectations,' triggering a disappointment-driven withdrawal of funds.

However, considering management's consistently cautious guidance, Dolphin Research believes that the actual problems are not as significant as imagined. The volatile market reactions to Spotify over the past few quarters are primarily due to the persistent issue of high valuations, compounded by the looming shadows of short-form video and the AI disruption narrative.

Let's take a closer look:

1. Uninspiring Guidance, Key Metrics Fall Short of Expectations: Two key tracking metrics for the logic of streaming price increases are net new subscription users and gross margin.

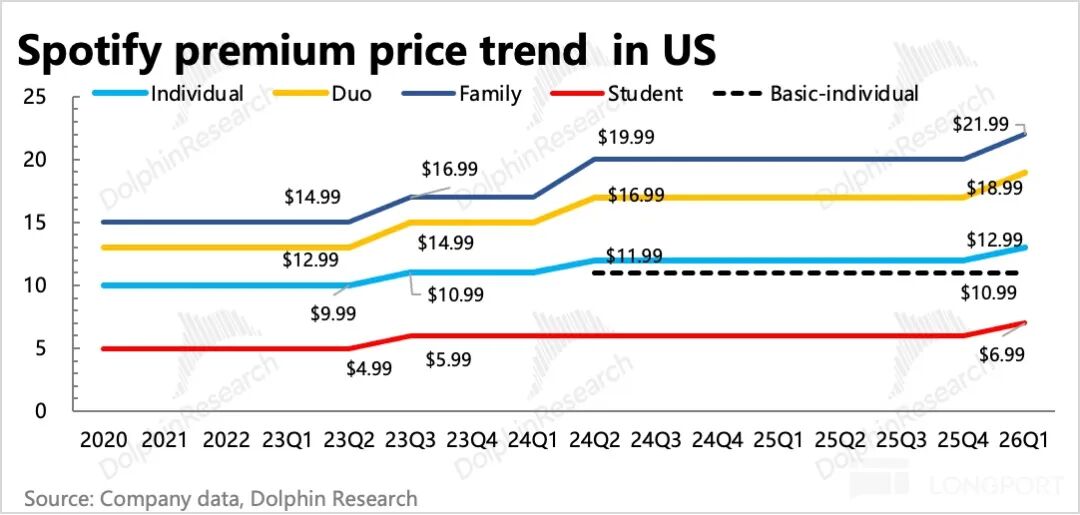

(1) Low Net New Subscription Users: Q2 is expected to see an increase of 6 million paying users, falling short of the more optimistic estimate of ~7 million based on historical Q2 growth trends. Therefore, the user growth falling short of expectations raises doubts among investors about whether the price increases in core regions over two consecutive quarters have led to user churn.

During last quarter's earnings call in February, management stated that churn rates were within estimates and retention was not poor. From a regional perspective, Q1 saw relatively low net growth primarily in North America. Spotify raised prices in the U.S. market at the end of January, but North America remains a highly competitive market, with Spotify currently being almost the most expensive digital music platform. Therefore, short-term user churn following the price increase is inevitable, and the company's ability to recall users through enriched features and membership benefits will be crucial.

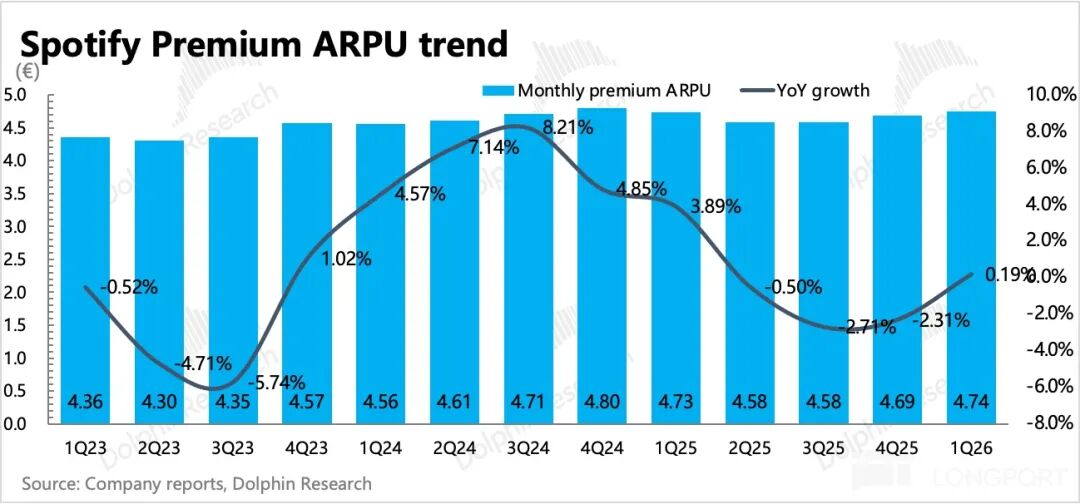

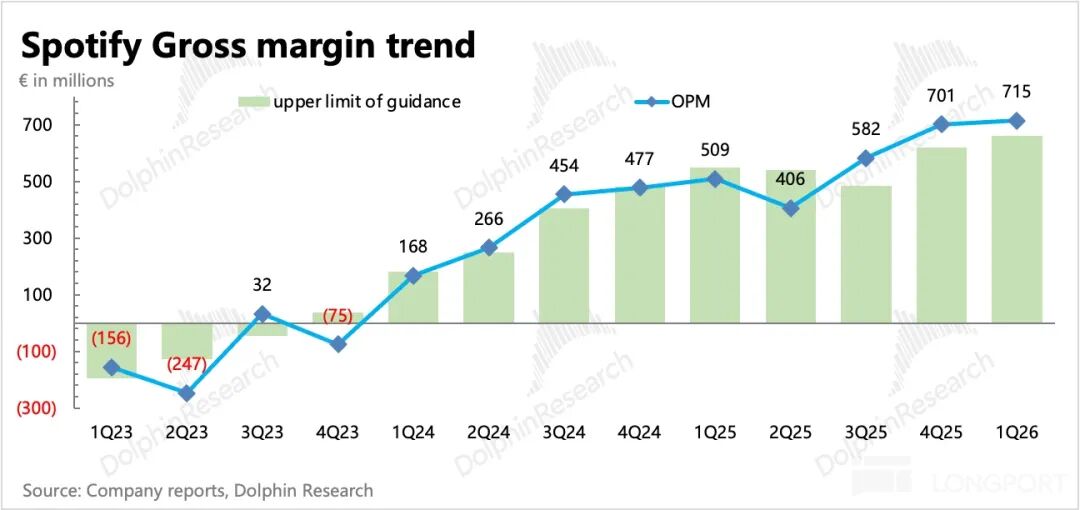

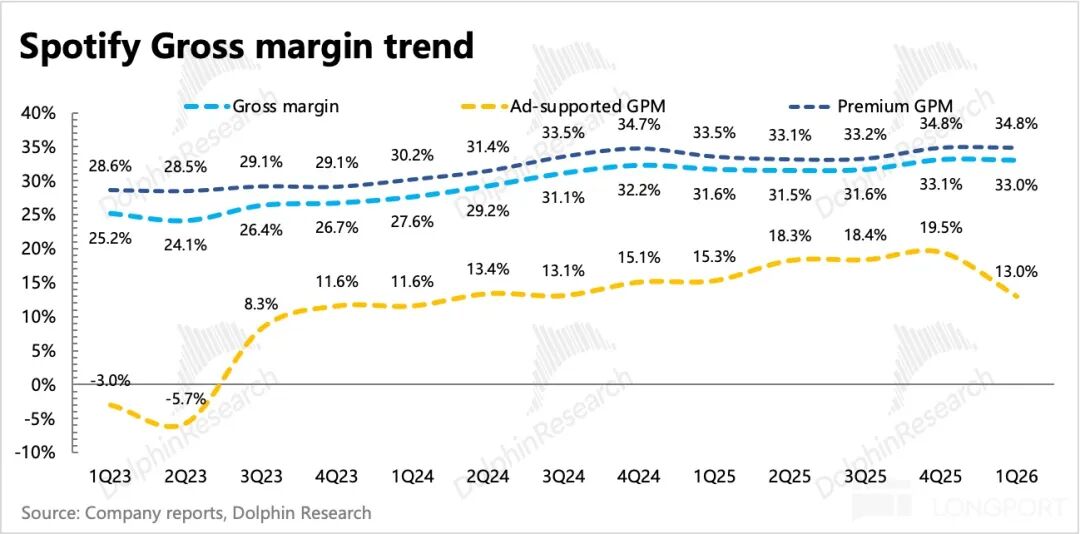

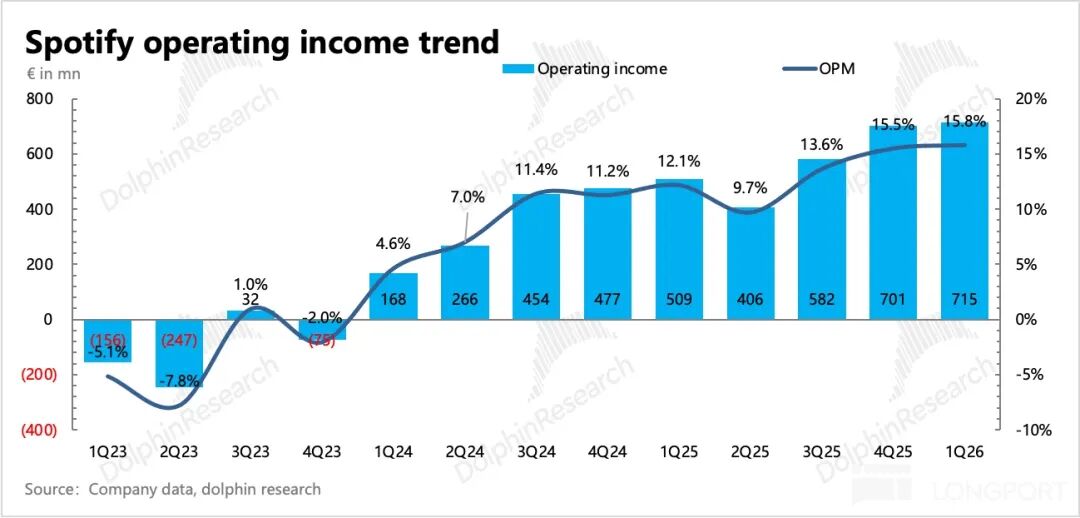

(2) Slow Gross Margin Improvement: Q1's gross margin of 33% was good, exceeding the guided 32.8%. However, the company expects only a 0.1% sequential increase in gross margin for Q2. Q2 is the first full quarter to benefit from the 'North American price increase dividend,' and investors had higher expectations for gross margin improvement.

Conversely, management's conservative gross margin expectations may reflect a lack of confidence in the stable increase of subscriptions despite the price hikes, unable to fully offset the impact of increased licensing costs under the new authorization agreement cycle.

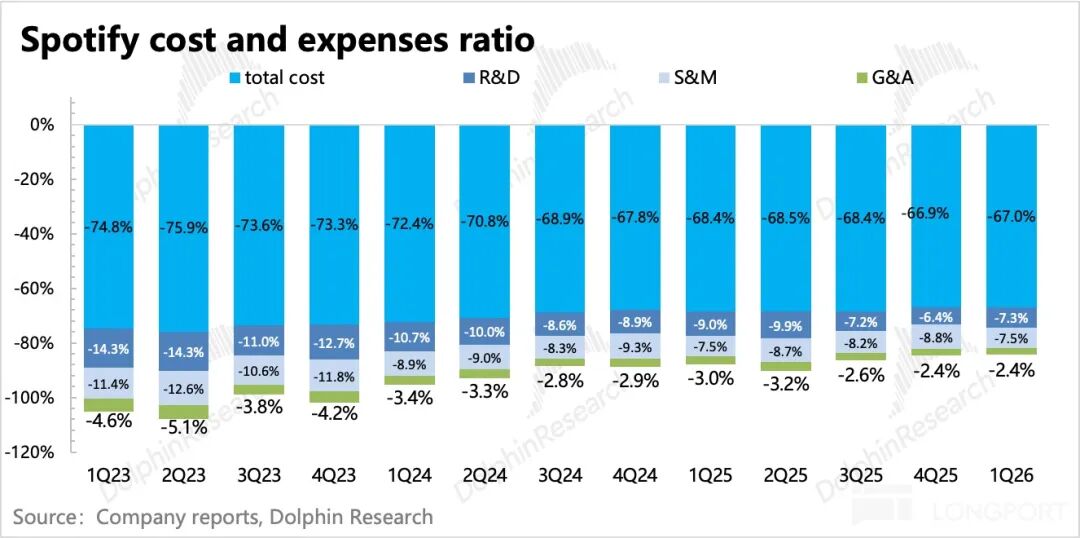

(3) Significant Increase in Expenses: Q2's operating profit guidance fell short of expectations. In addition to the gross margin reasons mentioned above, expenses are also expected to be higher than anticipated, indirectly reflecting management's commitment to investments for this 'ambition year.'

2. Q1 Overall Met Expectations, but Advertising Remained Sluggish: In Q1, apart from the underperforming advertising segment (which continues to 'surpass expectations' in its decline), the subscription business and profitability were satisfactory. However, this obviously did not alleviate market dissatisfaction with the Q2 guidance.

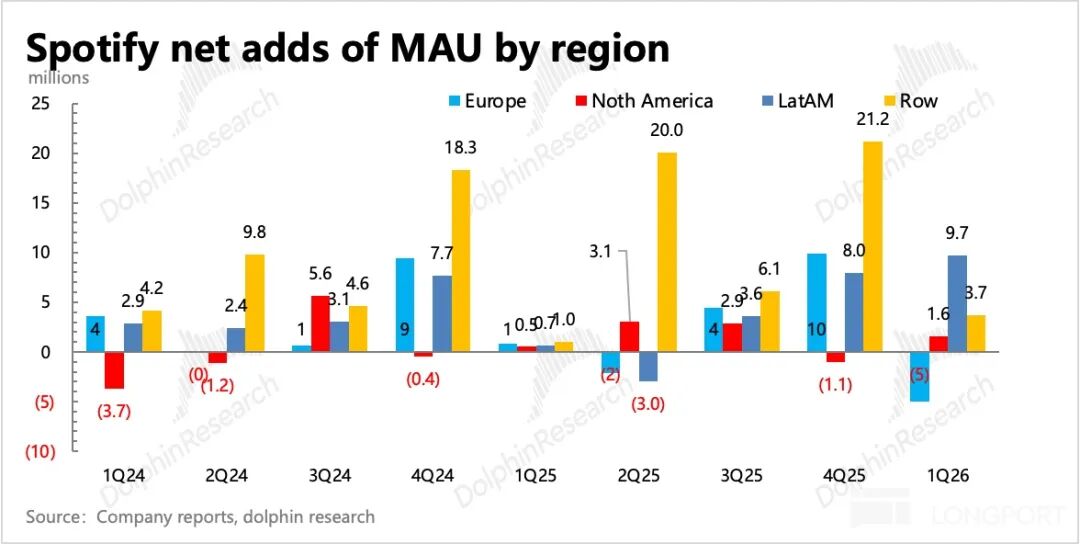

(1) Stable Ecosystem, Low-Value Users Contributing to Growth: In Q1, the platform's monthly active users (MAUs) reached 760 million, with Q2 guidance approaching 780 million. Even considering last year's record-breaking Q4 growth, this year's growth remains impressive. Regionally, the increase primarily came from the Asia-Pacific region, while user growth in core revenue-generating regions, especially Europe, was average, with a sequential decline. This resulted in user growth not being fully reflected in financial performance. Although this trend remains healthy and beneficial in the medium to long term, it also poses short-term financial growth pressures.

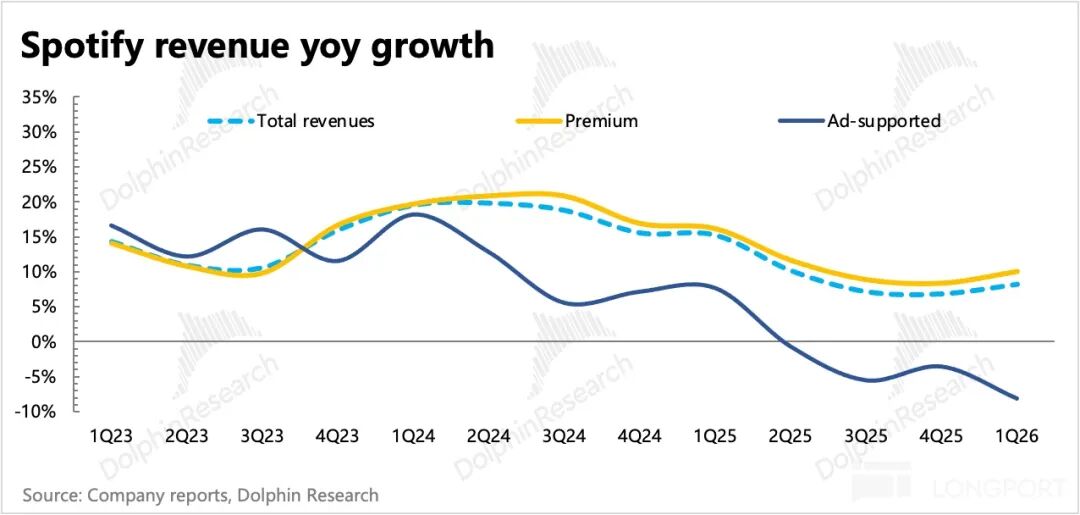

(2) Gradual Alleviation of Currency Headwinds: Since Spotify's financial reports are denominated in euros, but the U.S. dollar has been continuously depreciating against the euro, the North American market, which accounts for nearly 35% of total revenue, is significantly affected by exchange rate fluctuations, accounting for 6% of current revenue impact. Therefore, the 8% revenue growth would have been 14% in real terms, excluding exchange rate effects.

However, starting in Q2, with the stabilization and rebound of the U.S. dollar, the currency headwinds have significantly eased, reducing to only 0.8 percentage points.

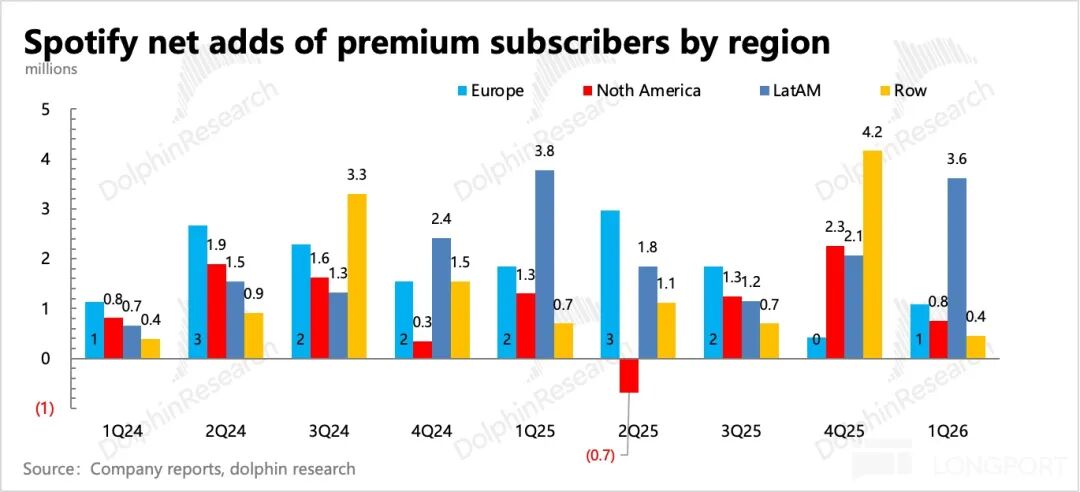

(3) Advertising Still Adjusting: The 14% internal revenue growth was primarily driven by paid subscription revenue, while advertising continued to face pressure. Q1 saw a net increase of 3 million subscription users, meeting guidance. Average Revenue Per Paying User (ARPPU) returned to growth under the influence of price increases, despite greater exchange rate impacts compared to Q4.

(4) Profits Exceeded Expectations: Q1 profits surpassed expectations, not only due to the slightly higher gross margin than guided but also because of a more than 10% year-over-year decline in research and development and administrative operating expenses. This includes Social Charges related to Stock-Based Compensation (SBC). In Q1, the company's stock price was low, resulting in reduced corresponding expenses.

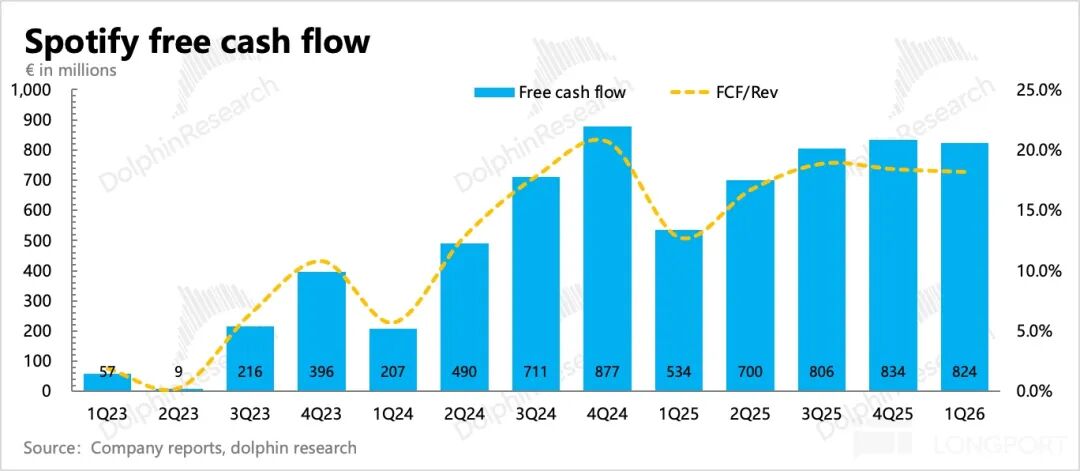

6. Stable Cash Flow: Due to stable business growth and investments, Q1 free cash flow remained at €820 million. As of the end of Q1, the company had accumulated nearly €8.6 billion in cash + short-term investments, a decrease of €800 million sequentially, primarily used to repay a portion of notes.

Share repurchases in Q4 amounted to €300 million, €80 million less sequentially. On an annualized basis, the return rate is relatively low and insufficient to support valuations during adjustment periods.

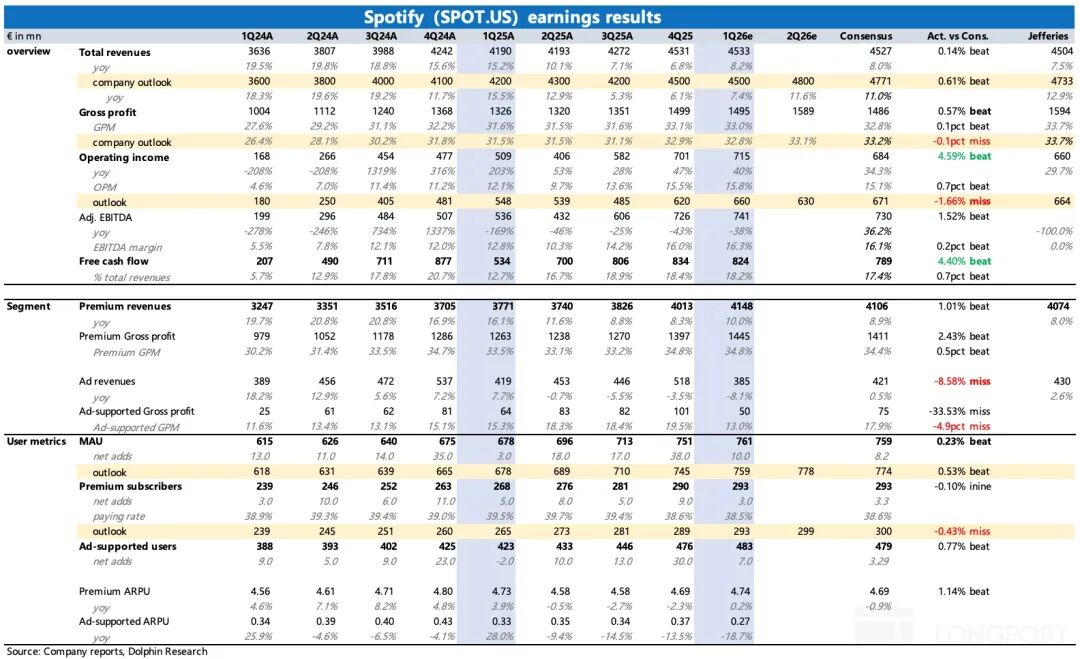

7. Performance Overview

(The performance expectations in the chart below are somewhat outdated. Dolphin Research has extracted Jefferies' performance expectations from mid-April, which are more optimistic about profit metrics compared to the BBG consensus.)

Dolphin Research's Viewpoint

Last quarter saw a 'correction' of pessimistic expectations amid the peak of the AI disruption narrative. This quarter, after absorbing the benefits of price increases, the market began expecting Spotify to quickly return to the traditional price increase logic of streaming services. However, with the Sword of Damocles of AI disruption still hanging overhead, the market has discounted valuations for the same financial performance.

If the price increase logic encounters any setbacks, short-term valuations are likely to suffer significantly. Regarding the Q2 guidance issues, Dolphin Research believes they may not be as severe as reflected in the stock price. After short-term capital disappointment and withdrawal, due to the shadow of AI, fewer funds are willing to blindly step in compared to previous years.

Unless valuations continue to digest and come down from their pedestal, similar to Netflix's back-and-forth acquisition drama, which saw valuations fall from 35x-40x forward P/E to around 30x. Spotify, which has traditionally been valued higher, is now back to 24x P/FCF, corresponding to 32x P/E (based on this year's revenue growth of 14%, operating profit growth of 40%, and a tax rate of 15%). Despite decent growth and improving profit margins, given the decreased certainty of future cash flows due to AI, the current valuation is at best reasonable but still not absolutely cheap.

If the stock continues to adjust downward in the short term after the earnings report to around 30x P/E, similar to Netflix's valuation, reaching €81 billion, then attention can be paid to potential rebound opportunities driven by sentiment recovery in May. This will be another Investor Day since 2022, and management often discloses the company's three-year medium-term development strategy and growth targets. We believe this could serve as a short-term catalyst for sentiment recovery, as a three-year medium-term guidance, regardless of whether the company can achieve it as planned or exceed expectations like last time, will increase confidence in the growth trajectory in the short term.

Below are detailed charts:

I. Stable Platform Expansion

User metric growth in Q1 was not bad (decent), with a net increase of 10 million MAUs reaching 761 million users. Latin America and the Asia-Pacific region remained the main growth drivers this quarter, while core regions like Europe and North America underperformed.

Current paid subscription users saw a net increase of 3 million, meeting guidance and expectations. Q2 guidance includes a net increase of 17 million MAUs and 6 million subscription users, falling short of the market's expectation of around 7 million net new subscriptions.

II. Growth Driven by Subscriptions, Advertising Still Dragging

Q1 revenue grew by 8%, with an 8 percentage point impact from currency headwinds, greater than the impact in Q4. However, Q2 saw significant relief with the rebound of the U.S. dollar, only dragging by 0.8 percentage points.

In terms of business segments, subscription revenue grew by 10%, while advertising declined by 8% year-over-year, still facing significant pressure from exchange rate impacts. Market expectations were originally higher for advertising recovery.

Management guided Q2 revenue of €4.8 billion, a 14.5% growth rate, with significantly reduced currency headwinds. Excluding exchange rate effects, the guided growth rate is 15.3%.

The company raised prices in the U.S. and Estonia regions in Q1, but judging by Q2's revenue and gross margin guidance, the effect of price increases driving profit expansion seems lower than market expectations.

III. Slowing Gross Margin Improvement, Can Price Increases Continue Smoothly?

Q1 profits exceeded expectations, driven by stable gross margin improvements, ongoing operational efficiency enhancements, and a decline in SBC and related Social Charges due to the stock price decline.

However, judging by Q2's operating profit guidance, the company is still adhering to management's earlier stated 'Year of Raising Ambition,' with investment directions including the launch of various new features, the expansion of audiobooks to more regions, and increased AI investments to enhance algorithmic recommendation capabilities.

Meanwhile, the new authorization agreement cycle with the three major record labels, which began in 2025, implies short-term increases in licensing costs. Therefore, increasing the subscription user base and raising prices (or introducing Superfan membership packages) are the primary ways to offset rising content costs.

However, user feedback on price increases is not consistently positive. After all, in the relatively competitive North American market, although Spotify remains the leader, its membership prices are already the highest among peers. This not only means that subsequent price increase rhythms may need to slow down (waiting for peers) but also requires attention to short-term user backlash effects.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or viewpoints mentioned in this report shall not be considered or construed as an offer to sell securities or an invitation to buy or sell securities in any jurisdiction. They also do not constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and materials in this report are not intended for distribution to or use by individuals or residents of jurisdictions where such distribution, publication, provision, or use contradicts applicable laws or regulations or requires Dolphin Research and/or its affiliates or associated companies to comply with any registration or licensing requirements in such jurisdictions.

This report only reflects the personal views, insights, and analytical methods of the relevant creative personnel and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research will reserve all related rights.

-

![]()

Why Has There Been a Sharp Decline in the Weekly Utilization Volume of China’s AI Large Models?

-

![]()

$600 Billion Poured into AI, But No One Can Say When It Will Pay Off

-

![]()

2026 Beijing Auto Show: Joint Venture Automakers Unleash a Counteroffensive

-

![]()

From '60,000 Yuan Daily Pay' to 'Top Talents Returning to the Job Market': Has the Heyday for Short Drama Actors Faded?

-

![]()

Spotify: 'Plunge' Caused by Unmet Expectations, Streaming Becomes Old Flame

-

![]()

The Irony of 20 Million Automotive Elites Vying for Meager Profits

-

![]()

The AI Fortune Dream Crumbles in Singapore: The Enigma Even Zuckerberg Can't Solve

-

![]()

DeepSeek's Image Recognition Debut Rocks the AI World: I Pushed Its Limits with 12 Tricky Images