The Irony of 20 Million Automotive Elites Vying for Meager Profits

04/30 2026

04/30 2026

625

625

Lead

Introduction

Perhaps the automotive industry truly needs to hit the brakes.

The recently released profit margin figures for the automotive industry in the first quarter of 2026 have left many astounded.

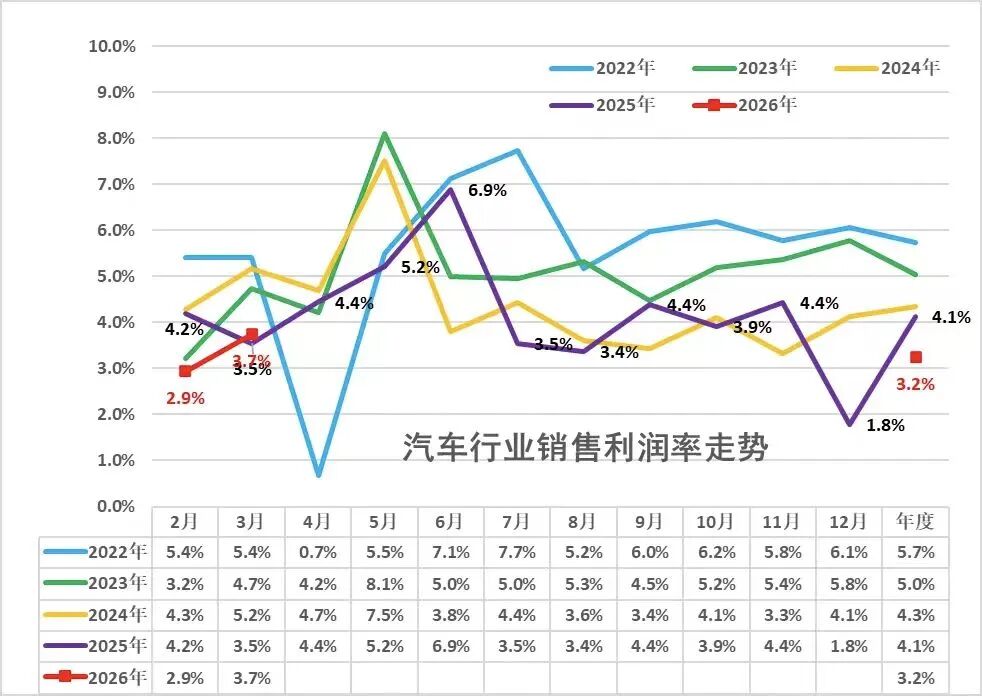

Data from the China Passenger Car Association reveals that in the first quarter of 2026, the automotive industry's profit reached 78.4 billion yuan, marking an 18% year-on-year decline. The profit margin stood at a mere 3.2%. Even this slim 3.2% represented a slight improvement over the 2.9% profit margin recorded in the first two months, buoyed by the 3.7% profit margin in March.

Simultaneously, the automotive industry's revenue for the first quarter was 2,412.8 billion yuan, a 0.2% year-on-year decrease, while costs rose slightly by 0.7% to 2,140.6 billion yuan.

Of course, by the end of April, everyone in the automotive industry was preoccupied with the Beijing Auto Show. Many might not have immediately noticed the first-quarter profit margins—automakers were busy showcasing their latest models; dealers were engaged in negotiating collaborations; media outlets were reporting on the latest developments; salespeople were actively selling cars; and car enthusiasts were busy attending the show and making purchases. Everyone was fully engaged in their respective roles.

However, behind this bustling activity, the 3.2% profit margin punctured the surface excitement of the automotive industry. It highlights the low profitability in the auto market and leaves automotive professionals constantly lamenting: despite the intense competition and everyone rushing in, they end up with only meager, almost negligible profits. To paraphrase a line from director Stephen Chow's movie A Chinese Odyssey: "He looks like a dog."

This sense of fatigue from working hard yet earning little is not confined to any one role but permeates the entire automotive supply chain. From upstream suppliers, midstream automakers, and downstream dealers to supporting PR firms, automotive media, and even end consumers, no party is spared from the intense internal competition. Each role faces its own set of unspoken industry dilemmas.

01 An Industry-Wide Problem, Felt Industry-Wide

Among them, automakers, at the core of the industrial chain, bear the brunt of this intense competition most directly.

Today's automakers have long moved beyond the era of "huge profits." For instance, SAIC-GM, a leader among joint-venture brands, saw its peak profit in 2013, with net profit attributable to shareholders reaching 26.616 billion yuan. However, facing market and era changes, it now has to sacrifice profits and adopt strategies like "fixed pricing" to stabilize market performance. Among the new forces, NIO, which has performed well, took eight years, from 2015 to 2023, to become the first domestic new car-making force to achieve annual profitability.

If this is the case for leading automakers, the situation for those in the middle and lower tiers is even more dire. Currently, most automakers are trapped in a vicious cycle of constantly launching new products, weak sales, and dismal profits. To gain a foothold in the market, major automakers go all out to generate buzz, from new product launches to marketing campaigns. But cruelly, the speed of new car iterations far exceeds the market's absorption capacity, making a decline in terminal sales inevitable.

Additionally, automakers face multiple pressures, including performance KPIs, R&D costs, and rising upstream raw material prices. In the new energy era, the prices of core raw materials like lithium carbonate have fluctuated sharply and continued to rise. Compounded by the relentless price wars in the industry, automakers' profit per vehicle is continuously being compressed. There has long been a biting industry joke: automakers work hard building and selling cars, only for suppliers to reap the profits, reducing them to mere "assembly plants" with little profit left after all their hard work.

Upstream component suppliers illustrate the Matthew effect in the industry. The entire supplier landscape is highly fragmented and intensely competitive, with only a very few leading companies like CATL able to rely on technological and scale advantages to maintain high profitability and earn the vast majority of industry profits. Examples include CATL for batteries, Fuyao for glass, and Huawei's ecosystem for intelligent driving assistance and smart cockpits...

However, there are many more small and medium-sized suppliers without technological barriers or stable cooperation resources, who can only passively bear the pressure of industry competition. Price cuts by automakers, fierce market competition, and rising raw material costs transmit layer by layer, continuously squeezing the profits of small and medium-sized suppliers. They struggle year-round to maintain production capacity and sustain cooperation, busy yet earning meager profits, teetering on the brink of profit and loss.

Additionally, dealers at the terminal distribution level are even more severely affected by industry competition. In recent years, the closure and delisting of automotive dealers have become commonplace in the industry. Data shows that in 2025, nearly 5,000 4S stores withdrew from the network, with over 80% of dealers selling cars at a loss.

This situation is not surprising. Currently, the auto market has high inventory, with large numbers of new cars piling up in dealerships unable to be sold. To clear inventory and recoup funds, dealers are forced to sell cars at discounted prices. However, the price wars continuously erode profit margins, with dealers' profit per vehicle plummeting to rock bottom. Many dealerships not only fail to make money selling a car but even incur losses. On one side are high dealership rents and labor costs, and on the other, sluggish sales and meager profit per vehicle. The survival dilemma of terminal dealers is visible to the naked eye.

Meanwhile, automotive media and PR firms, as part of the industry's supporting ecosystem, are also deeply trapped in the quagmire of intense competition.

For automotive media, traveling to exhibitions nationwide, participating in product launches, and producing report content means a relentless schedule of event after event, with densely packed itineraries and year-round exhaustion. But as industry dividends fade, media profits continue to shrink, to the point where some joke about not being able to get reimbursement for taxi fares for three to five years, primarily "working for love."

PR firms face similarly tough conditions. When participating in bids for automaker projects, many automakers seem to have abandoned the "quality first" competition logic, with low-price bids becoming the norm. High-quality proposals lose out to low-price quotes, and industry competition has completely disrupted survival rules.

Not only industry practitioners but also end consumers have become victims of industry competition. Some time ago, a video circulating online showed: a consumer who bought a car for 140,000 yuan last year and earned 50,000 yuan driving it for ride-hailing found that the terminal price of the model had plummeted to 90,000 yuan in just one year, meaning the user had worked for a year for nothing.

Three years ago, Automobile Magazine lamented in an article titled "You All Ask Me How Many Cars I Sold in the First Half of the Year, Only My Mom Asks If I Slept Well!": For a 2.7% retail growth in the first half of 2023, automotive professionals endured 182 days of upheaval. Now, with the industry's 3.2% profit margin, it still doesn't justify the relentless efforts of millions of automotive professionals.

02 The Automotive Industry Needs a Brake

What has caused the massive Chinese automotive industry to fall into a dilemma where everyone is busy, everyone is in intense competition, and no one is making money?

The reasons are naturally multifaceted.

The disorderly price wars in a mature market are undoubtedly the most visible factor.

The domestic auto market has long bid farewell to the era of growth, with the market pie stabilizing, but the number of automakers and models continues to increase, leading to severe overcapacity. To seize market share, clear inventory, and meet performance targets, automakers are forced into price wars, with the intensity of competition continuously escalating. This vicious cycle of trading price for volume continuously compresses profit margins across the entire industrial chain, causing the industry's overall profitability to keep declining.

In May 2025, the China Association of Automobile Manufacturers issued an Initiative on Maintaining Order in the Automotive Market, explicitly opposing disorderly price cuts; the Ministry of Industry and Information Technology subsequently stated its support for addressing intense competition, emphasizing the need to guide the industry toward high-quality development. A year has passed, and some internal industry issues have eased, but a complete resolution still requires time.

Additionally, the imbalanced profit structure across the industrial chain also affects industry development. In the new energy era, vehicle manufacturing is highly dependent on core components like power batteries, and the battery sector is highly concentrated, with leading suppliers controlling core technologies and pricing power, occupying the vast majority of profits in the industrial chain. In comparison, automakers seem more like "workers."

Data shows that in the first quarter of this year, the profit margin for the upstream non-ferrous metals industry was as high as 39.4%, and for the oil industry, it reached 32.9%, while the profit margin for the automotive manufacturing industry was only 3.2%, far lower than the 8% in 2017.

Besides, the industry's rapid iteration and high costs are also core pain points. Under the wave of new energy and intelligent transformation, automakers need to continuously invest huge sums in R&D for intelligent driving, cockpits, and battery technologies, while marketing, channel, and operational costs remain high.

Rapid technological iteration and frequent new car launches continuously strain industry capacity and profits, with market demand growth unable to keep pace with industrial iteration, ultimately causing wasted capacity, resource depletion, and further depressing overall industry profits.

A few days ago, an industry insider lamented helplessly: Nearly 20 million industry elites are competing fiercely for the automotive industry's meager 3.2% profit. Is it really worth it?

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket

-

![]()

Doubao Goes 'Professional', Volcano Rolls the Snowball

-

AI: No Sign of a Bubble!

-

![]()

NVIDIA-Backed AI Unicorn Secures $1.5 Billion Funding: Revenue Soars 2000%

-

![]()

Doubao Pro is Here: How Can Seed 2.1 Be Integrated into Real Processes?

-

"PCB Juice" Sees Four Consecutive Declines: Even Computing Power Material Suppliers Can't Lift This "Old Stock"

-

![]()

Potential 'Seismic Shift' in the U.S. TV Industry: Competition Shifts from Hardware Sales to Traffic Entry Points

-

![]()

Audi A6L's Defense in the Luxury C-Class Market: Following Huawei's Smart Driving Integration, Is Large-Battery HEV the Next Move?