OnePlus and realme Unite as OPPO Braces for Industry Challenges

05/05 2026

05/05 2026

506

506

Following their return to OPPO, OnePlus and realme have embarked on a journey of deep integration.

On the evening of April 29, 2026, Lei Feng Network exclusively reported that OPPO had internally announced the merger of OnePlus and realme to form a new sub-series business unit. realme founder Li Bingzhong will helm this unit, with realme Global Marketing President Xu Qi overseeing marketing, and OnePlus China President Li Jie leading the product center.

In response, Wang Teng, the former General Manager of Xiaomi's China Marketing Department, remarked that the merger of OnePlus and realme represents a "strategic move to optimize resource allocation amid a market downturn. With escalating upstream costs, the smartphone market is unlikely to witness short-term growth, prompting major manufacturers to streamline their workforce this year."

In recent years, as incremental market benefits have dwindled and memory prices have soared, numerous small and micro smartphone brands have grappled with immense survival pressures. In light of this, OPPO's decision to integrate internal resources and enhance collaborative efficiency is a prudent one.

However, it's crucial to acknowledge that the industry's growth ceiling is becoming increasingly apparent. This means that companies will find it challenging to achieve significant leverage effects through sustained investment. The upper limit of return on investment is becoming a formidable barrier that companies struggle to overcome.

If OPPO solely relies on "endogenous" adjustments through resource integration without exploring new growth avenues beyond its smartphone business, it will be arduous for the company to weather the downturn.

01. Vanishing Benefits in the Smartphone Industry: OnePlus and realme Reach Their Growth Limits

Despite their distinct brand positioning, OnePlus and realme were initially tasked with helping OPPO tap into new markets.

Around 2013, fueled by Xiaomi's success, the internet smartphone market boomed, while OPPO, with its focus on offline channels, was preoccupied elsewhere. To seize the internet smartphone opportunity, Liu Zuohu resigned as OPPO's Deputy General Manager at the end of 2013 to establish OnePlus, aiming to create a "brand revered by global users."

With its innovative design, superior feel, and cost-effectiveness, OnePlus swiftly ascended to the upper echelons of the high-end smartphone market. In October 2019, Liu Zuohu disclosed that OnePlus ranked fourth globally in the high-end smartphone segment (priced over 3,000 yuan).

In contrast to OnePlus's strong performance in developed markets like Europe and the U.S., driven by its "Never Settle" product philosophy, realme, founded in 2018, rapidly expanded in emerging markets such as India and Vietnam with its "Dare to Leap" core selling point.

For instance, in May 2018, realme launched the realme 1 in India, selling over 400,000 units in just 40 days. In August of the same year, realme swiftly followed up with the realme 2, selling 200,000 units in a mere 5 minutes on India's e-commerce platform Flipkart, setting a new sales record for the platform.

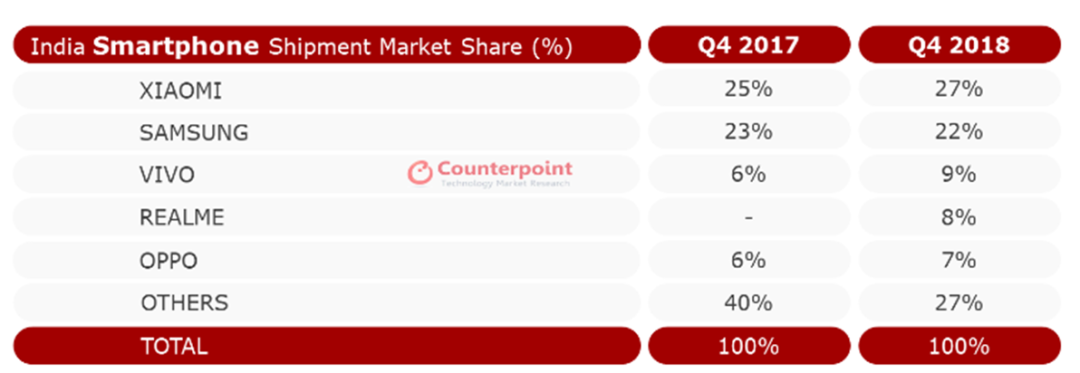

Counterpoint data revealed that in Q4 2018, realme held an 8% share of India's smartphone market, ranking fourth and becoming the fastest brand to surpass 4 million units sold in the market.

Regrettably, OnePlus and realme have not sustained their rapid growth trajectory. In recent years, as global smartphone market benefits have diminished, both brands have encountered growth bottlenecks.

After seven years, OnePlus has maintained a "small but beautiful" status, with annual sales failing to surpass the 10 million unit mark. Omdia data indicates that in 2022, realme sold 53 million units, marking an 8.62% year-on-year decline.

02. Soaring Memory Prices: OPPO Tightens Its Belt

The primary impetus behind OPPO's deep integration of OnePlus and realme is the weakening growth momentum of both brands, with the direct catalyst being the rapid surge in memory prices.

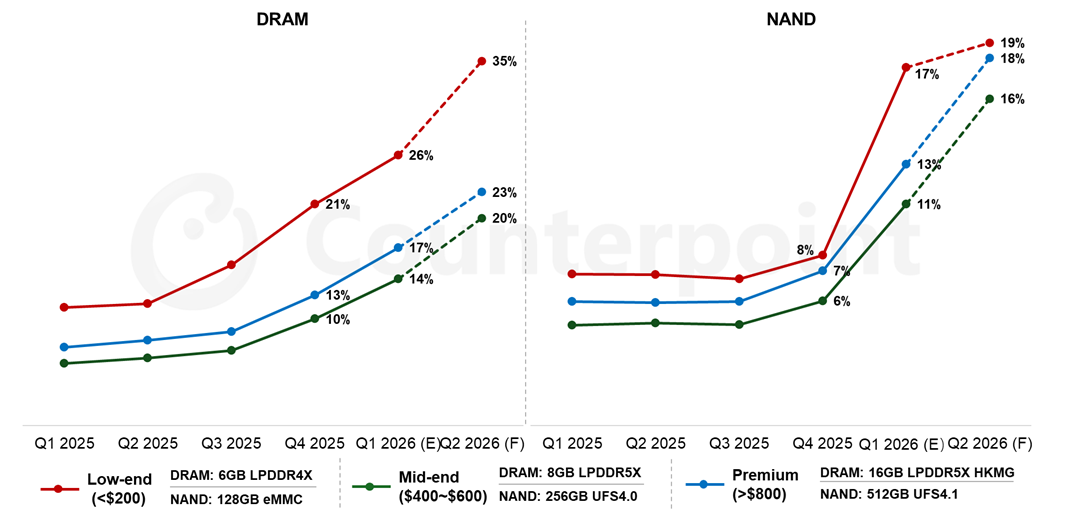

Counterpoint data shows that in Q1 2026, DRAM prices soared over 50% quarter-on-quarter, while NAND prices skyrocketed over 90%. Memory prices are anticipated to continue rising by approximately 20% in Q2.

The sharp increase in memory prices has significantly dampened consumer demand, further exacerbating the smartphone market environment. Sigmaintell research projects that global smartphone shipments will reach 1.12 billion units in 2026, a 6.4% year-on-year decline.

Against this backdrop, numerous cost-effective small and micro brands face significant downward pressure due to their lack of scale advantages. A case in point is Meizu, which announced in February 2026 that it would suspend domestic self-developed hardware projects for new smartphone models.

In light of this, OPPO has recalled and deeply integrated OnePlus and realme, aiming to enhance overall operational efficiency through resource reuse while clarifying brand positioning to establish a tiered, well-defined market hierarchy, enabling more agile responses to intense competition.

Take OnePlus as an example. Previously focused on the high-end market, after returning to OPPO, it transformed into a "performance-focused pioneer brand." Leveraging OPPO's R&D, channels, and after-sales resources, OnePlus made the leap from "small but beautiful" to a "mainstream brand."

In January 2022, Li Jie revealed in an interview that OnePlus's global smartphone sales reached 12 million units in 2021, doubling from the previous year, with China accounting for over 20% and experiencing an 80%-90% year-on-year growth.

Given realme's existing market influence, after returning to the OPPO ecosystem and deeply integrating with OnePlus, it is also poised to leverage the group's abundant resources and more precise brand positioning to regain strong growth momentum.

03. Beyond Smartphones: OPPO Urgently Needs a New Growth Narrative

While the deep integration of OnePlus and realme may temporarily bolster OPPO's smartphone market competitiveness, it is unlikely to fundamentally address the structural challenge of the smartphone market's declining ceiling in the long run.

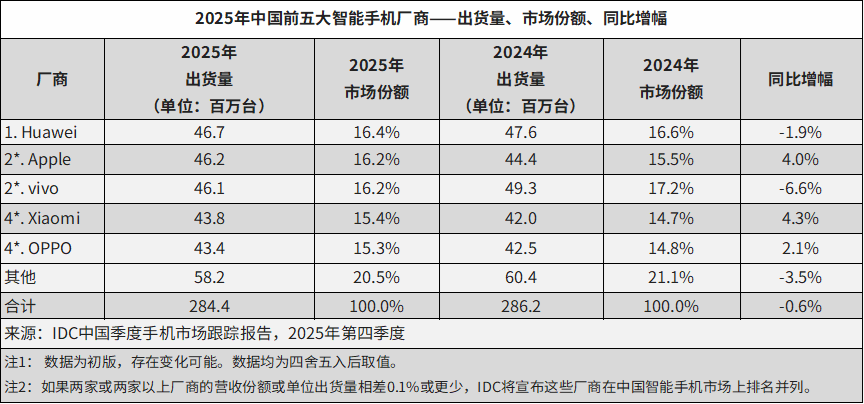

IDC data reveals that from 2019 to 2025, annual smartphone shipments in China declined from 370 million to 285 million units, with a compound annual decline rate of 4.26%.

Against this backdrop, even a formidable player like Huawei has struggled to maintain positive growth. In 2025, Huawei's smartphone shipments in China reached 46.7 million units, a 1.9% year-on-year decline.

To circumvent growth bottlenecks, smartphone manufacturers like Huawei and Xiaomi are actively diversifying into more promising new businesses such as IoT, smart cars, and AI.

Take Xiaomi as an illustration. In 2025, its smartphone × AIoT segment revenue grew just 5.4% year-on-year, while its innovative businesses segment, including smart electric vehicles and AI, generated 106.1 billion yuan in revenue, surging 223.8% year-on-year and becoming the company's new growth engine.

In response, Wang Teng remarked, "The smartphone market is down, and everyone is struggling, but Xiaomi has automotive and AIoT businesses, and in the AI era, there are new growth points like large models, embodied AI, and self-developed chips. I believe Xiaomi will return to growth." Confident in Xiaomi's future, Wang Teng has increased his stake in Xiaomi's stock.

In contrast, although OPPO began布局 (laying out) IoT-related businesses around 2018, its IoT ecosystem remains highly constrained, with only earphones, wearables, and accessories product lines. Its smart TV business has stalled, and it has not ventured into the smart car sector.

In September 2024, Liu Bo, OPPO's China President, stated, "We must focus on smartphones and our core peripherals like earphones, Pads, and watches. From OPPO's strategic perspective, focus is crucial." "Focusing on the smartphone business aligns with OPPO's consistent 'integrity' values. However, for tech companies, 'focus' is not a static concept but a dynamic capability that requires constant calibration with the times.

Had Apple remained solely focused on computers, it would not have created revolutionary products like the iPod, iPhone, or iPad and become a global tech behemoth.

Through the deep integration of OnePlus and realme, OPPO may indeed enhance resource allocation efficiency in the short term, thereby mitigating downward pressure in the smartphone industry. However, this strategy essentially remains an internal optimization within the existing market and is unlikely to fundamentally unlock long-term growth potential.

Now, as AI technology transitions from concept to large-scale implementation, the tech industry is entering another pivotal "gear shift" period, with tech giants racing to create innovative products. If OPPO hopes to navigate the cycle, it cannot stop at a defensive "tightening the belt for winter" strategy but must adopt a proactive stance to identify and bet on the next-generation mass computing platform.

-

![]()

High-Speed Toll Collection via Mobile Phones & Cardless License Plate Recognition: Are License Plates at Risk of Misuse? Official Reply: Safeguarded by Domestic Encryption Algorithms

-

![]()

Insta360 Enters a Challenging Growth Phase Less Than a Year After Its IPO

-

![]()

The Real Race for Robotaxi Begins When the Steering Wheel Comes Off

-

![]()

China’s AI is Embroiled in a Token Price War, Leaving the U.S. Far Behind, with Prices at a Mere 0.6%

-

![]()

April Witnesses Major Shifts Among Emerging Automakers: Leapmotor Tops 70,000 Units, Xiaomi, Li Auto, and Xpeng Surpass 30,000 Units

-

![]()

OnePlus and realme Unite as OPPO Braces for Industry Challenges

-

![]()

2026 Beijing International Automotive Exhibition: Who Will Shape the Future of Cars?

-

Who Will Succeed Gree’s Dong Mingzhu?