Insta360 Enters a Challenging Growth Phase Less Than a Year After Its IPO

05/05 2026

05/05 2026

412

412

Recently, Insta360 (hereinafter referred to as "Insta360"), a frontrunner in the panoramic action camera sector, unveiled its financial results for 2025 and the first quarter (Q1) of 2026. Both reports highlight a notable trend of "revenue growth without corresponding profit increases." Despite experiencing rapid revenue expansion, the company is grappling with significant profit pressures, essentially meaning it is earning less despite selling more.

To be frank, the two financial reports released by Insta360 less than a year after its initial public offering (IPO) present both promising aspects and potential challenges. Let's delve deeper:

Firstly, the promising aspects, which I summarize in three key points:

1. Rapid Revenue Growth and Emerging Economies of Scale

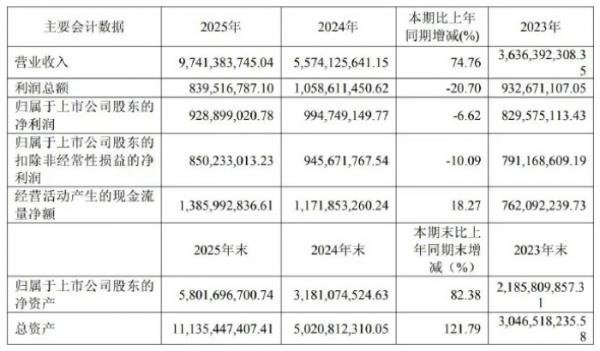

In 2025, Insta360 achieved revenue of RMB 9.741 billion, marking a year-on-year increase of 74.76% and setting a new historical record, nearing the RMB 10 billion milestone. This high-speed growth momentum persisted into Q1 of this year, with quarterly revenue reaching RMB 2.481 billion, up by 83.11% year-on-year. The company's revenue surged from RMB 2.041 billion in 2022 to RMB 9.741 billion in 2025, nearly quadrupling over three years, showcasing its robust market expansion capabilities.

2. Strong Core Business with Significant Globalization Achievements

According to IDC data, in 2025, Insta360 secured global market shares of 66% and 57% in the two core categories of panoramic cameras and thumb cameras, respectively, maintaining its global leadership and nearly monopolizing these niche markets. Its globalization foundation is solid, with overseas revenue accounting for a substantial 69.03% in 2025, and its sales network spanning over 70 countries and regions worldwide.

Simultaneously, Insta360 has made positive strides in channel expansion. Offline specialty stores surged from 36 at the beginning of 2025 to nearly 300 by year-end, with per-store sales increasing by nearly 50%, significantly enhancing channel efficiency and brand penetration.

3. Aggressive R&D Investment with a Focus on Long-Term Technological Advancement

Insta360 has adopted a high-profile strategy in R&D investment. In 2025, R&D expenses reached RMB 1.53 billion, up by 96.95% year-on-year. In Q1 of this year, R&D investment was RMB 465 million, a year-on-year increase of 100.59%, with R&D investment growth consistently outpacing revenue growth.

Insta360 is accelerating its transformation from a hardware manufacturer to an imaging ecosystem builder, making increased R&D investment essential. This not only solidifies its existing businesses but also strategically invests in R&D for two new drone models (including the already launched Yingling A1), gimbal cameras, wireless lavalier microphones, and other new categories, expected to be launched within the next year, along with the custom development of three chip models.

In a letter to investors, Insta360 founder Liu Jingkang articulated for the first time the long-term technological vision of creating a "photography robot," aiming to achieve seamless integration of shooting and editing through the holistic capabilities of "hardware + software + data." This suggests that Insta360's heavy investment in R&D with a focus on long-term technological advancement may become the norm.

Now, let's discuss the potential challenges, which are primarily reflected in the following four aspects:

1. Significant Profit Decline with Increasingly Apparent Revenue Growth Without Profit Increases

In 2025, Insta360's net profit was RMB 929 million, a year-on-year decrease of 6.62%, marking its first annual negative growth since going public. In Q1 of this year, the profit decline intensified, with net profit at only RMB 84.6202 million, a sharp year-on-year decrease of 52.02%, nearly "halved," and marking its third consecutive quarter of year-on-year net profit decline.

From my observation, the decline in Insta360's profitability is closely tied to two reasons. Firstly, rising costs. Affected by the price increases of raw materials such as memory chips, the company's operating cost growth far exceeded revenue growth. The gross profit margin in 2025 was 45.74%, the lowest level since 2017 and lower than the 52.2% in 2024, further declining to 45.2% in Q1 of this year.

Secondly, intensified industry competition. Insta360 and industry giant DJI have engaged in a price war, putting pressure on product pricing and further squeezing profit margins. For example, during last year's Double 12 shopping festival, the Insta360 Ace Pro was directly reduced by RMB 1,400, and the Ace Pro 2 Play Package was reduced by RMB 500, showcasing significant price reductions. The consequence of trading price for volume was a negative impact on gross profit, with profit loss inevitable.

2. Soaring Expenses Eroding Short-Term Profits

Insta360 is facing a situation of "dual-front spending" on the expense side. On the one hand, to position itself in new markets and develop custom chips, R&D investment has nearly doubled, directly consuming a significant amount of profit. On the other hand, sales expenses remain high, reaching RMB 1.679 billion in 2025, a year-on-year increase of 103.31%, with growth significantly outpacing revenue, mainly due to increased channel expansion and marketing investments.

This means that in 2025, Insta360's combined R&D and sales expense ratio exceeded 32%, squeezing profit margins. In Q1 of this year, sales expenses continued to surge by 75.54% year-on-year to RMB 449 million. In response, Insta360 admitted in its annual report that if it fails to effectively control sales expenses across various channels in the future, it may adversely affect the company's operating performance.

Liu Jingkang stated in the letter to investors that high-intensity strategic investments support the company's long-term development layout but also lead to a decline in short-term profit indicators. It is evident that although Insta360 is aware of the drawbacks of dual-front spending, it seems to lack effective cost-reduction strategies for now.

3. Deteriorating Cash Flow and High Inventory Levels

In 2025, the net cash flow generated from Insta360's operating activities managed to maintain positive growth, increasing by 18.27% year-on-year to RMB 1.386 billion. However, in Q1 of this year, it plummeted to -RMB 1.471 billion, a significant deterioration from -RMB 381 million in the same period last year, mainly due to stockpiling new products and purchasing raw materials such as chips.

Behind the drastic change in cash flow is the rapid expansion of Insta360's inventory. As of the end of Q1 of this year, the company's inventory surged to RMB 3.794 billion, an increase of nearly RMB 900 million from the end of last year. In the fast-paced consumer electronics industry, high inventory levels often imply potential risks of price declines and asset impairment, a negative signal that Insta360 should be vigilant and take seriously.

4. New Business Expansion Falling Short of Expectations, Intensifying Competition, and Legal Risks

As a flagship product for the second growth curve, the panoramic drone Yingling A1 has underperformed since its launch, accounting for less than 5% of revenue in Q1 of this year, with market estimates suggesting a quarterly loss of approximately RMB 160 million for this business. Its entry into the red zone is related to both hardware cost inversions and high R&D investment, with competitive pressure being another significant factor that cannot be ignored.

It is important to note that DJI not only competes head-on with Insta360 in the action camera market but has also quickly launched competing panoramic drones, putting significant pressure on Insta360's new business expansion. Additionally, DJI has attempted to use patent litigation to hinder Insta360. In March of this year, DJI sued Insta360 over the ownership of six patents involving core technologies such as flight control and image processing, directly targeting the underlying technological foundation of Insta360's drone business and introducing uncertainty for the company's future development.

Since the litigation outcome will directly impact Insta360's R&D investment, business layout, and brand reputation, among other aspects, significantly affecting its fundamental operating conditions, it is crucial. If Insta360 loses the lawsuit, not only will the substantial R&D investment become sunk costs due to infringement, but some businesses involving core areas such as flight control, structure, and image processing will also be affected. The final outcome remains to be seen—let's wait and see!

Overall, Insta360 is in a challenging growth phase, trading short-term pain for long-term barriers, accompanied by both risks and opportunities. Let's take a longer-term view and give Insta360 more opportunities to prove itself. Going forward, the outside world should focus on four key areas: the commercialization progress of new products, stabilization and rebound of gross profit margins, improvement in inventory turnover, and a return to positive cash flow. What do you think?

-

![]()

High-Speed Toll Collection via Mobile Phones & Cardless License Plate Recognition: Are License Plates at Risk of Misuse? Official Reply: Safeguarded by Domestic Encryption Algorithms

-

![]()

Insta360 Enters a Challenging Growth Phase Less Than a Year After Its IPO

-

![]()

The Real Race for Robotaxi Begins When the Steering Wheel Comes Off

-

![]()

China’s AI is Embroiled in a Token Price War, Leaving the U.S. Far Behind, with Prices at a Mere 0.6%

-

![]()

April Witnesses Major Shifts Among Emerging Automakers: Leapmotor Tops 70,000 Units, Xiaomi, Li Auto, and Xpeng Surpass 30,000 Units

-

![]()

OnePlus and realme Unite as OPPO Braces for Industry Challenges

-

![]()

2026 Beijing International Automotive Exhibition: Who Will Shape the Future of Cars?

-

Who Will Succeed Gree’s Dong Mingzhu?