Samsung Outpaced by Local Competitors in China!

05/07 2026

05/07 2026

576

576

The global home appliance market has now firmly entered the 'China Era.'

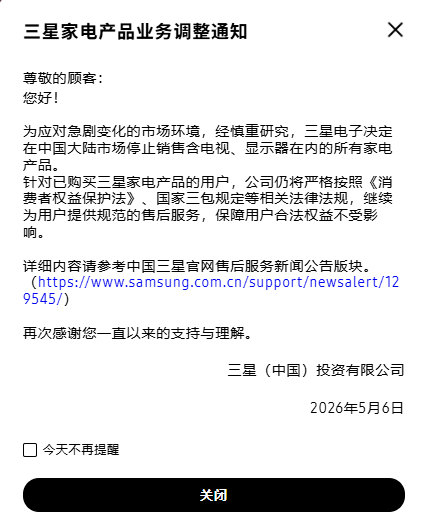

Samsung Electronics has officially announced its withdrawal from the Chinese home appliance market, stating: 'In response to rapidly evolving market conditions and after thorough deliberation, Samsung Electronics has decided to discontinue sales of all home appliance products, including televisions and monitors, in the Chinese mainland market.'

(Image source: Samsung China official website)

Samsung Electronics is making a complete exit from the Chinese home appliance sector, covering a wide range of products such as televisions, monitors, large commercial displays, air conditioners, refrigerators, washing machines, dryers, washer-dryer combos, garment care systems, audio equipment, projectors, vacuum cleaners, air purifiers, and more. However, this withdrawal does not affect its semiconductor business (including memory), mobile terminals (smartphones), or medical equipment divisions.

On the same day, Samsung Electronics' market capitalization surpassed one trillion US dollars, making it the second Asian company—after TSMC—to join this elite club.

The juxtaposition of these two events offers fascinating insights.

Memory Chips Generate Wealth, While Home Appliances Become a Liability

The decision to abandon home appliances—a category that once helped Samsung establish a premium brand image among Chinese consumers—may seem challenging. Since entering the Chinese market in 1992 and investing in manufacturing facilities in Huizhou, Tianjin, and Dongguan, Samsung has operated in China for 34 years. Its exit now reflects a highly rational capitalist strategy: when a company's stock price and market value are primarily driven by its memory chip business, low-margin, fiercely competitive ventures like home appliances become financially unattractive.

In 2026, Samsung—the world's largest memory chip manufacturer—dominates one of the most profitable industries globally. High Bandwidth Memory (HBM) is in short supply, with NVIDIA's GPU orders fully booked through 2027. Samsung has captured the majority of the profits from this wave of AI infrastructure development.

Financial Report Analysis: In the first quarter of 2026, Samsung Electronics' sales reached KRW 133 trillion (approximately RMB 606.48 billion), with operating profit surging by 755% year-on-year. The chip business contributed nearly 90% of the profits in this quarter, while the home appliance division remained unprofitable. Losses in the previous quarter amounted to approximately KRW 600 billion (around RMB 2.79 billion). Although losses narrowed this quarter, the business still hovered on the brink of profitability.

Gross profit margins for home appliances typically range from single digits to low teens. The profit from selling a single television may not even match a fraction of the profit from selling a single memory chip. Moreover, the latter does not require an after-sales service team, extensive channel penetration into lower-tier markets, or price wars with local brands.

With Samsung holding the world's most profitable semiconductor business, competing fiercely in the home appliance market is akin to 'choosing unnecessary hardship.' Companies developing AI home appliances, large language models, or AI agents are all 'gold miners,' but selling 'shovels' (memory chips) is a consistently profitable business. As home appliance manufacturers go all-in on AI, they all need to purchase Samsung's memory chips, effectively paying Samsung a 'computing infrastructure tax' in various ways.

Furthermore, Samsung's presence in the Chinese home appliance market has become so negligible that its withdrawal barely caused a ripple. Data shows that Samsung's offline market share for color televisions in China dropped to just 3.62% by April this year, with even lower shares for refrigerators and washing machines at 0.41% and 0.38%, respectively.

Samsung's current situation closely resembles that of DuPont in the late 19th century. DuPont began with black powder, but after a paradigm shift in the foundational science of the chemical industry, it swiftly transformed into a materials science company, supplying nylon, Teflon, and Kevlar. These inventions defined 20th-century industrial civilization. DuPont no longer produced bullets and shells, but all arms manufacturers relied on its raw materials.

Samsung follows the same logic. It no longer needs to compete head-on with Chinese brands in end-user categories like televisions and refrigerators. Instead, it can supply memory chips or OLED panels—a more sophisticated form of market control. You might think it has exited, but in reality, it has sunk deeper into the supply chain.

Slow Product Iteration: Samsung Home Appliances Outpaced by Chinese Brands

However, if more profits were achievable, no company would refuse them. Samsung's withdrawal from the Chinese home appliance market stems from its inability to compete with Chinese brands.

On the surface, Samsung's pricing appears aloof. For example, in televisions, TCL launched affordable MiniLED products in 2021, bringing a technology previously confined to high-end showrooms to ordinary consumers. Samsung only began large-scale promotion of MiniLED televisions in 2022, pricing them above RMB 15,000. While TCL democratized the technology, Samsung insisted its MiniLED was 'worth 15,000.'

(Image source: Samsung)

In the core dimension of AI home appliances, Samsung's component advantages have not translated into competitive end-user products.

Haier's AI Eye 2.0 system, unveiled at AWE 2026, has been mass-produced and applied to product lines including refrigerators, washing machines, and air conditioners. For instance, its AI refrigerator can identify ingredients, automatically sense storage conditions, and recommend recipes, truly integrating AI capabilities into daily user interactions.

(Image source: Leikeji AWE 2026 on-site footage)

Last year, Midea pioneered the world's first DeepSeek air conditioner. At AWE 2026, it showcased agent-based home appliances capable of autonomous perception, decision-making, and operation, along with household robots and whole-home air systems. Meanwhile, television—once a stronghold for Japanese and Korean manufacturers—has seen Chinese brands gain market share. TCL has made MiniLED mainstream, while Hisense's RGB-MiniLED outperforms traditional solutions in color reproduction.

(Image source: Leikeji AWE 2026 on-site footage)

Samsung's AI home appliances or MicroLED televisions displayed during the same period remained at the demo stage. Models like the R95H and R85H MicroLED televisions have yet to appear in the Chinese market, indicating Samsung's slower product cycle.

Exiting the Chinese market will not improve Samsung's home appliance business. Home appliances rely on economies of scale. Without Chinese market volume to support production costs for new technologies, a vicious cycle emerges: lower market share discourages aggressive new product launches, leading to conservative strategies and further shrinking market presence.

The Era of Human-Vehicle-Home 2.0: Home Appliances Are No Longer Standalone Businesses

More critically, the home appliance business is losing its independence in the AI era. At expos like AWE, CES, and IFA, as well as in press conferences by Chinese home appliance giants, the concept of 'human-vehicle-home' is frequently mentioned. As Leikeji reported at AWE 2026, the era of Human-Vehicle-Home 2.0 has arrived:

It's not just about connecting home appliances to the internet or enabling synergy between smartphones, cars, and home appliances. The future of whole-home intelligence lies in real-time collaboration among robots, vehicles, and home appliances, achieving true whole-home intelligence and even autonomous housework. Home appliances are no longer standalone products but nodes in an intelligent living ecosystem. Smartphones serve as control hubs, cars as mobile extensions, robots as execution terminals, and home appliances as perception and response carriers. Data flow, AI collaboration, and user habit integration among these four elements form a genuine competitive advantage.

(Image source: Leikeji AWE 2026 on-site footage)

Within this framework, home appliance manufacturers must own or partner with automotive and robotics businesses to build a complete experience loop:

- Xiaomi has automobiles, robots, and smartphones;

- Haier and Midea are heavily investing in robotics and collaborating with automotive brands through ecosystem models;

- Huawei's HarmonyOS ecosystem integrates vehicles, home appliances, and smartphones;

- Honor, OPPO, and Vivo are expanding into the home appliance sector;

- Even Dreame has proposed a vision of 'Human-Vehicle-Home-Space-Star.'

(Image source: Midea)

Samsung is not lacking in AI or smart home ecosystems. Globally, it owns the SmartThings platform, Galaxy smartphones, Harman automotive solutions, and even AI products like the Ballie home robot. The issue lies in its near-absent ecosystem in China.

(Image source: Samsung)

Is Samsung incapable? Not necessarily. In Leikeji's view, this stems from willingness and organizational structure. Samsung is a highly centralized South Korean chaebol, with its China division lacking sufficient product definition authority. All localization efforts are 'compliance adaptations' within headquarters' frameworks rather than genuine redesigns for the Chinese market. This contrasts sharply with Haier, Midea, TCL, and Hisense, which adopt a 'Glocal' (Global + Local) approach to research and development, better meeting local demands. Samsung merely 'translates' global products for China, a strategy increasingly costly in a market with rapid iteration and localized needs.

Thus, Samsung has failed to stitch together a 'human-vehicle-home' ecosystem in China. Its smartphone business collapsed after the Note 7 explosion scandal, maintaining a market share below 1%. While it won't exit the Chinese smartphone market soon, its presence is negligible. Its automotive business is virtually nonexistent, and its robotics布局 (layout) is unimpressive.

The world has changed. Home appliances no longer compete as standalone products but as entry points to ecosystems. Without the necessary infrastructure, Samsung's withdrawal from the home appliance market amounts to leaving the table.

Fleeing Competition: The Chinese Home Appliance Market Is Now in 'Hard Mode'

A more pressing issue is the brutal competitiveness of the Chinese home appliance market, which has left many international brands gasping for air.

Established giants like Haier, Midea, Hisense, TCL, Changhong, and Skyworth have fortified their positions with technology, product strength, omnichannel distribution (online and offline), supply chains, and brand recognition. Meanwhile, new players continue to enter the fray.

Yu Hao's ambition to build a trillion-dollar company may seem audacious, but Dreame's first target in smart cleaning is home appliances. Founded in 2017, Dreame adopts a 'premium feature democratization' strategy, packing suction power and cleaning performance previously exclusive to Dyson into more affordable products. By Q3 2025, its revenue reached RMB 12.07 billion, up 72.2% year-on-year, with a 12.4% global market share in robotic vacuum cleaners. It ranks first in 22 countries and regions, even outperforming Dyson in its home market (the UK) and the EU. Dreame matches Samsung in functionality, undercuts it in pricing, and iterates faster.

At Dreame's recent Silicon Valley product launch, it unveiled a full lineup of home appliances, including refrigerators, air conditioners, floor washers, televisions, and personal care devices. Leikeji's on-site coverage highlighted the global influence of Chinese brands.

(Image source: Dreame)

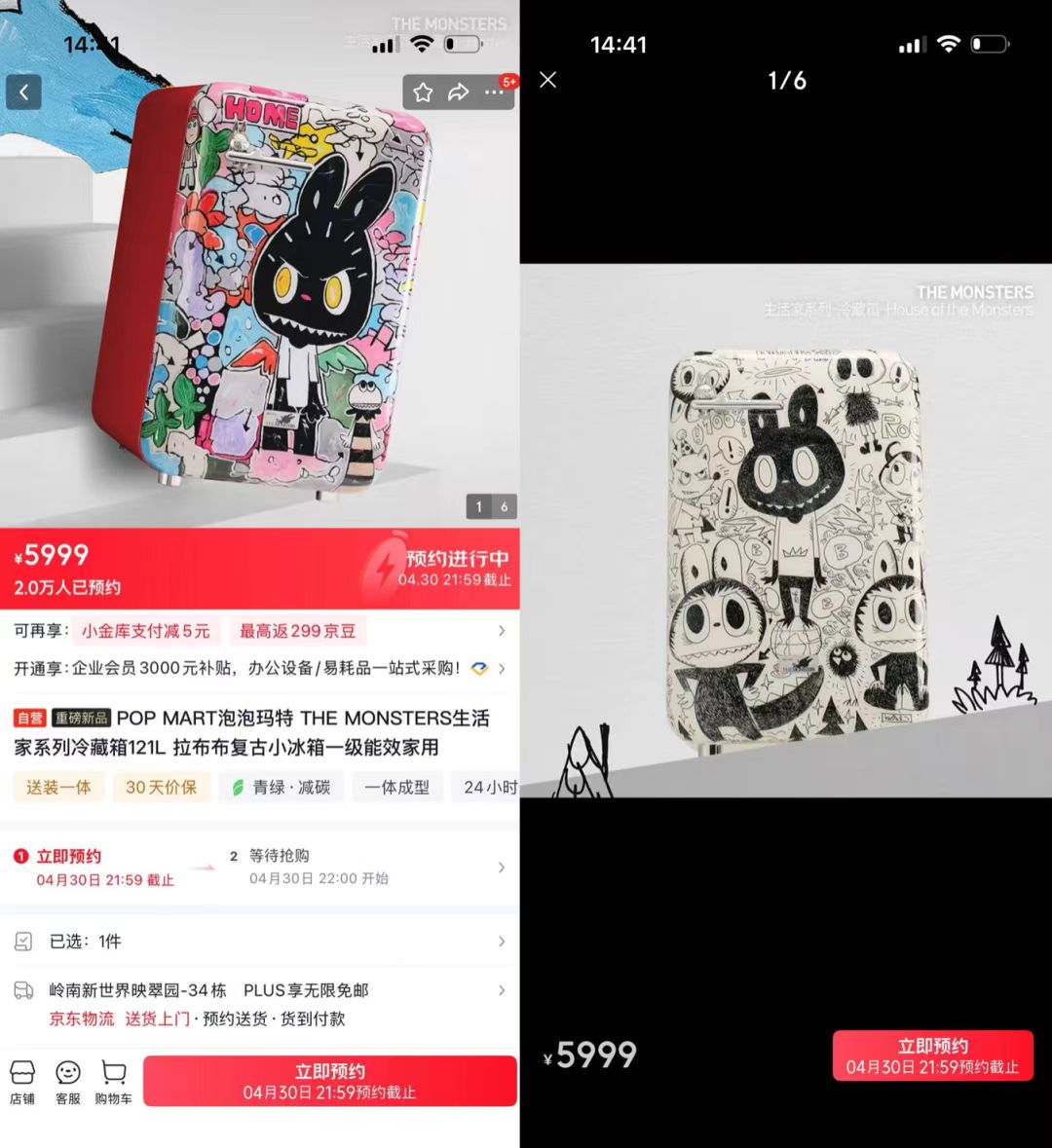

Not to mention Xiaomi, a 'price disruptor' that drags industry profit margins downward with every product launch. Even Pop Mart, a company unrelated to home appliances, has launched Labubu-themed refrigerators.

(Image source: JD.com)

It's hard to imagine how Samsung could compete against such relentless, rule-breaking, and imaginative rivals. The reality is that it cannot.

There is nothing new under the sun. Before 2016, Samsung smartphones commanded a premium market share in China, rivaling Apple. After the Note 7 explosion scandal, its Chinese smartphone business collapsed in freefall. Many assumed China would suffer greatly without Samsung phones, but the opposite happened: Huawei, OPPO, Vivo, Xiaomi, and Honor swiftly filled the void across high-end to mid-range and low-end segments. China also nurtured HarmonyOS, an ecosystem comparable to Android and iOS, and spearheaded the most aggressive foldable smartphone innovation.

The home appliance market may follow the same script: without Samsung televisions, Chinese living rooms will see further breakthroughs from TCL MiniLED and Hisense MicroLED. Haier and Midea will push the boundaries of AI home appliances even further.

Samsung's Exit: The Global Home Appliance Market Enters the 'China Era'

When we zoom out to the global stage, Samsung's withdrawal from the Chinese market is just the initial move in its broader global retreat. In recent years, based on my observations at CES and IFA, it's evident that Samsung's exhibition space has been shrinking, its advertising presence is waning, and the buzz around its new products is fading. In stark contrast, Chinese brands are expanding their presence with larger and more prominent booths. For instance, Dreame has reportedly secured the largest venue for CES 2027, taking over the spot that once belonged to Samsung. In 2026, Hisense sponsored the FIFA World Cup in the U.S., Mexico, and Canada, while TCL's international marketing budget has been growing annually, with a series of impactful sports and entertainment campaigns. The overseas growth curves of Dreame and Roborock are impressively steep.

Before Samsung's retreat, Japanese brands had already thrown in the towel. Sony and Panasonic's global TV businesses were respectively handed over to TCL and Skyworth. Toshiba sold its home appliance business to Midea in 2016, and its TV division went to Hisense.

In the German market, Bosch and Siemens still maintain their showcases in JD MALL and Suning, but their pace of new product updates and price competitiveness have significantly diminished. These once-dominant global home appliance giants are now being outperformed by Chinese brands in direct competition, either clinging to a niche market or exiting entirely. Samsung's withdrawal is just one manifestation of a decade-long transformation in the home appliance brand landscape—a shift that may seem sudden but was, in fact, inevitable.

This is not self-aggrandizement; the facts speak for themselves. Chinese home appliance manufacturers are emerging as the protagonists of the AI era. With the world's strongest home appliance supply chain, the broadest AI application scenarios, and the most aggressive AI hardware and software technology application system, Chinese home appliance brands are breaking free from the narrative of "cost-effectiveness" and stepping into a new realm of "redefining smart living." Chinese home appliance brands are exploring ways to equip appliances with eyes (vision), brains (AI), and hands (robotic arms), while collaborating with vehicles, robots, and more, with the vision of "hands-free housework" that liberates human labor.

Indeed, "a small boat has sailed through countless mountains."

Samsung Home Appliances, Haier, TCL, Dreame

Source: Leikeji

Images in this article are from the 123RF licensed image library. Source: Leikeji

-

![]()

Ultra Pure Inc. Bets Nearly 350 Million Yuan on Optics After Formal IPO Approval

-

![]()

No Surprises, Just Unforeseen Turns in This Year's May Day Home Appliance Market

-

![]()

Half Step Away: Bridging AI and the Hearing Impaired

-

![]()

A Trillion-Dollar Horizon: Crafting a New Narrative

-

![]()

Can Zhao Ming Enjoy the Thrill of Qianli Technology?

-

![]()

Lending My Face to an AI Short Film: A One-Way Journey

-

![]()

The "Midlife Crisis" of Long-Form Videos: Can AI Win Back Users?

-

![]()

The AI Industry Outlook Post-DeepSeek-V4 Launch