Stock Price Halved, Net Profit Plummets: Is Insta360 (688775.SH) Facing Its Own 'GoPro Moment'? | A-Share Lightning Rod

05/07 2026

05/07 2026

521

521

May 2026 may prove to be a chilly early summer for Insta360.

On one hand, its revenue in 2025 is approaching the RMB 10 billion mark; on the other, its stock price has been halved, gross margins are continuously declining, net profits have plummeted, and it faces relentless all-round competition from industry giant DJI.

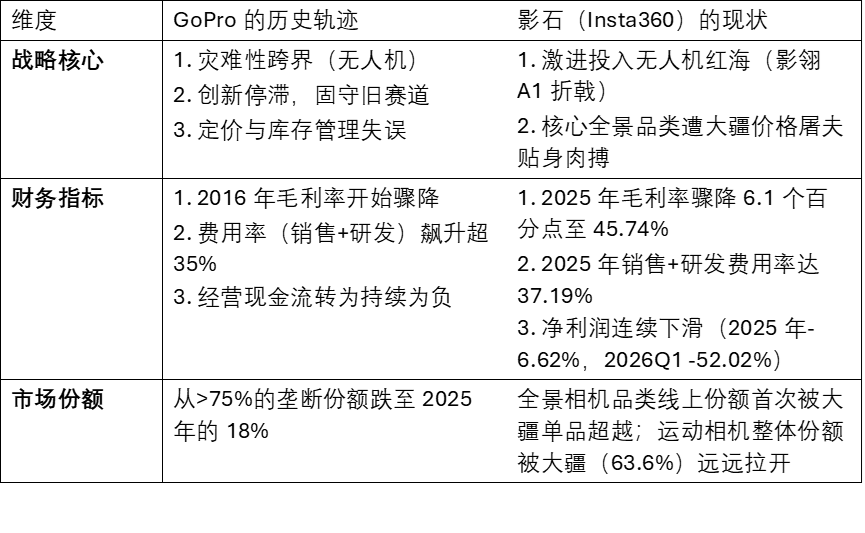

In the mirror of commercial history, Insta360's trajectory eerily mirrors that of GoPro a decade ago. The once-dominant force that defined the action camera era and saw its market value soar past $13 billion, the 'darling of Silicon Valley,' has now become a forgotten 'Meme Stock' among young consumers, its market value having crashed by 99% and teetering on the brink of bankruptcy.

As DJI's war machine rolls forward, will Insta360 follow in GoPro's footsteps and become the next 'old wave' eliminate (eliminated) by the times? To answer this question, we must look beyond the layers of fog in the financial reports, elevate our perspective to the macro dimension of business competition, and examine a life-or-death strategic choice.

01

Echoes of History: How Did GoPro Squander a Winning Hand?

Before analyzing Insta360, we must first dissect GoPro, this 'dead butterfly.' Its downfall was not due to a single product failure but rather a comprehensive strategic 'stroke.'

GoPro's greatness lay in creating an entire category single-handedly. Yet, its tragedy also stemmed from this—it became a victim of its own success. As the market shifted from professional extreme athletes to mainstream vloggers and content creators, GoPro remained aloof, intoxicated (intoxicated) in its self-image as the exclusive domain of extreme sports. On the product front, faced with rapidly evolving image stabilization algorithms and AI editing demands, GoPro's response was to milk its 'Hero' series with incremental updates. This attachment to its comfort zone quickly left it behind competitors with deeper local insights.

In 2016, seeking new growth, GoPro hastily entered the drone market with the Karma. However, 'crash' incidents due to battery failures forced a full recall just 16 days after launch, resulting in a staggering $376 million loss. This fiasco not only devastated GoPro's financials but, more critically, diverted management's attention from its core camera business. By the time Karma returned, DJI had already dominated the market, leaving GoPro to retreat in defeat. Ultimately, GoPro remained a traditional hardware assembler. Amid the 'hardware + algorithm + software + community' intelligence wave, its attempt to pivot into a media company failed miserably, with even basic mobile editing experiences poorly executed.

Reviewing GoPro's fall from a $13 billion market cap to a 'penny stock' worth less than $200 million, we see a classic collapse model of strategic missteps, financial deterioration, and market share erosion across three dimensions.

02

Insta360's Rise: Systemic Innovation Through Software-Defined Imaging

Insta360's success lies in taking a path starkly different from GoPro's.

Founded in 2015, Insta360 was born with a 'software gene.' Its founder, Liu Jingkang, a software engineering major dubbed the 'Tech Emperor of Nanjing University,' shaped Insta360's product philosophy: users buy not hardware but the experience of effortlessly creating and sharing content.

Insta360 redefined handheld imaging devices with its 'shoot first, frame later' approach, solving the traditional action camera's biggest pain point: composition and framing limitations. In the panoramic camera realm, Insta360 established a near-monopoly through technologies like multi-lens synchronous real-time stitching and distortion correction. Latest IDC data shows that in 2025, Insta360 maintained global leadership in two core original categories—panoramic and thumb cameras—with market shares of 66% and 57%, respectively.

More importantly, Insta360 built an AI-centric software ecosystem. Features like AI smart tracking, auto-editing, creative templates, and AI selfie stick removal enable ordinary users to generate professional-grade videos with one click. In 2025, Insta360 launched the 'Insta360+' cloud service, integrating cloud storage, sharing, playback, editing, and exporting to further enhance user stickiness.

Product iteration speed is another Insta360 advantage. With 3-5 new products annually, it far outpaces GoPro's 1 and rivals DJI's 2-3. From 2023 to the first half of 2025, Insta360 launched 3, 5, and 2 new products, respectively, rapidly translating technological innovation into market advantage.

From 2017 to 2024, Insta360's revenue CAGR reached 66%, while its Deducting non parent net profit (non-recurring profit and loss adjusted net profit) CAGR soared to 106%. In 2024, its revenue hit RMB 5.574 billion, surpassing GoPro for the first time.

03

DJI's Dimensional Strike: Hardware Empire's Ecosystem Expansion

If Insta360 represents 'software-defined imaging,' DJI embodies 'hardware + ecosystem' excellence.

DJI's core strength lies in its deep technological accumulation and complete supply chain system. Starting with drone flight control technology, DJI replicated its core competencies across action cameras, gimbal cameras, and other product lines, forming a 'drone + action camera + panoramic camera' trifecta.

In July 2025, DJI released its first panoramic camera, the Osmo 360. With 8K resolution, AI algorithms, and high cost-performance, it captured 49% of China's e-commerce market and 43% globally within three months, setting an industry record and directly challenging Insta360's panoramic camera monopoly.

In the action camera market, DJI's dominance is even stronger. In Q3 2025, DJI claimed 66% of the global market, surpassing GoPro to become the new global leader. In Japan, DJI broke GoPro's decade-long sales monopoly, claiming annual sales championships in both 'digital camcorders' and 'action cameras.'

DJI's success stems from its unique 'platform-based' strategy. Unlike Insta360's 'vertical deep dive,' DJI emphasizes product line breadth and ecosystem synergy. From drones to action cameras, handheld gimbals to intelligent driving systems, DJI's technologies and capabilities are reusable across multiple scenarios, creating powerful economies of scale.

As drone giant DJI enters Insta360's core territory with panoramic and action cameras, a full-scale war spanning patents, products, supply chains, channels, and talent has erupted—an asymmetric duel between a 'niche champion' and a 'full-industry-chain empire.'

First, the war's underlying logic is resources. In this dimension, the power imbalance is staggering.

Revenue and Profit Scale: In 2025, Insta360 achieved peak performance with nearly RMB 10 billion in revenue (RMB 9.741 billion) and RMB 929 million in net profit. Yet, these figures pale next to DJI's estimated RMB 85-90 billion annual revenue—nearly nine times Insta360's. This means DJI can deploy far greater financial resources and sustain losses longer in market battles.

Profitability and Strategic Flexibility: Insta360's 2025 net profit fell 6.62% YoY, with a net margin of just 9.10%. In Q1 2026, net profit plunged another 52.02% YoY. Its 37.19% expense ratio (R&D + sales exceeding RMB 3.2 billion) has pushed profits to the brink. DJI, with its massive base and diversified businesses, enjoys thicker profit cushions and strategic room. When DJI priced the Osmo 360 at RMB 2,999 (RMB 800 below Insta360's equivalent) and plans to launch the Avata 360 panoramic drone at RMB 2,788, it initiates a price war Insta360 cannot match. Insta360 has little room for further price cuts, while DJI, through vertical supply chain integration and scale effects, can use thin profits as a long-term competitive weapon.

Deeper still, this competition is a clash between two technological philosophies and product paths.

DJI's two-decade accumulation has forged vertical integration across flight control, gimbals, image transmission, batteries, and motors. Its strength lies in hardware reliability and parameter leadership. Insta360's success stems from 'software-defined hardware,' with core strengths in panoramic stitching algorithms, AI editing, and user experience design, aiming to lower creation barriers.

This path divergence leaves Insta360 vulnerable in a full-scale price war. DJI can swiftly launch competitive products (like the Osmo 360) using hardware cost advantages, while Insta360's algorithm- and experience-driven innovations require longer user education cycles and struggle to showcase 'cost-performance' on spec sheets.

As the giant awakens, wielding tenfold scale, full-industry-chain cost advantages, channel and supply chain clout, and patent legal weapons, Insta360's limited profits and cash flow emit sharp warnings amid this high-intensity war of attrition.

04

Financial Report Dissection: Bleeding Points and Profit 'Meat Grinder'

In business, crises ultimately reflect in financial statements. Insta360's 2025 annual report and Q1 2026 results paint a stark picture of 'revenue soaring, profits bleeding.'

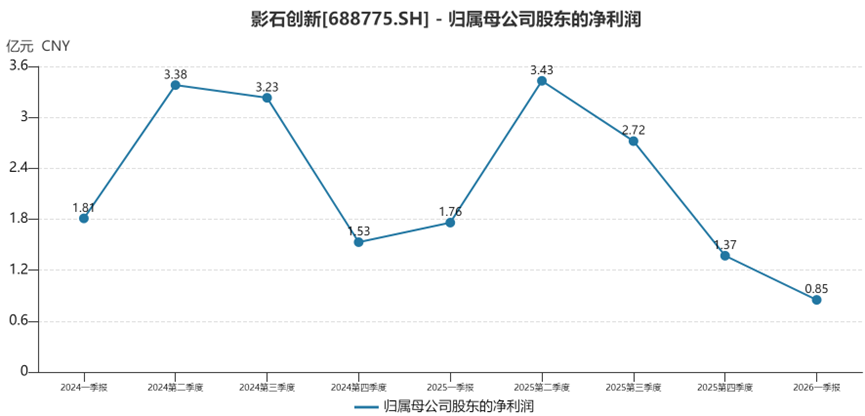

Data shows Insta360's 2025 revenue hit RMB 9.741 billion, up 74.76% YoY; in Q1 2026, revenue surged to RMB 2.481 billion, up 83.11% YoY. Superficially, this is high growth. But the profit statement tells another story: 2025 net profit was RMB 929 million, down 6.62% YoY; in Q1 2026, net profit collapsed to RMB 84.62 million, down 52.02% YoY.

Gross margins also face significant pressure. In 2025, Insta360's gross margin fell from 52.20% in 2024 to 45.74%, and in Q1 2026, it further declined to 45.20% (well below 52.93% in Q1 2025). This reflects the profit squeeze amid rising component costs and DJI's price war.

Meanwhile, to counter DJI's offensive and open new fronts, Insta360 is gambling heavily on spending. In 2025, R&D investment reached RMB 1.53 billion, up 97% YoY; in Q1 2026, R&D spending hit RMB 465 million, up 101% YoY. These funds are allocated to two drone projects (including the Yingling A1), the Luna gimbal camera, three undisclosed new categories, and three custom chip developments.

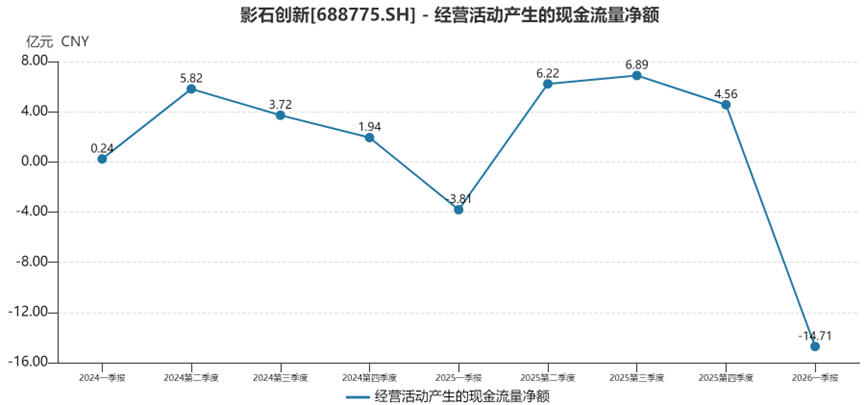

Accompanying profit declines is worsening cash flow. In Q1 2026, Insta360's net cash flow from operating activities plummeted. For a hard-tech company requiring constant R&D investment and risk resilience, weakened self-financing capabilities sound alarms.

05

Historical Lessons: Choices at the Crossroads

Facing profit table pain and fierce battles with giants, Insta360's management admits this is a strategic loss by choice. Yet history warns that the line between 'strategic losses' and 'sliding into the abyss' is thin.

GoPro's ghost does not predict Insta360's inevitable doom, but it clearly outlines a failure path: 'strategic overreach → financial deterioration → market loss.' Standing at the dawn of 2026, an unavoidable question arises: Is Insta360 at its own 'GoPro moment'?

In business, there are no eternal kings. GoPro once believed it held the key to the future, only to forget the commercial axiom: 'even disruptors can be disrupted.'

For Insta360, reaching RMB 10 billion in revenue is a milestone—and a dangerous crossroads.

- END -

-

![]()

Ultra Pure Inc. Bets Nearly 350 Million Yuan on Optics After Formal IPO Approval

-

![]()

No Surprises, Just Unforeseen Turns in This Year's May Day Home Appliance Market

-

![]()

Half Step Away: Bridging AI and the Hearing Impaired

-

![]()

A Trillion-Dollar Horizon: Crafting a New Narrative

-

![]()

Can Zhao Ming Enjoy the Thrill of Qianli Technology?

-

![]()

Lending My Face to an AI Short Film: A One-Way Journey

-

![]()

The "Midlife Crisis" of Long-Form Videos: Can AI Win Back Users?

-

![]()

The AI Industry Outlook Post-DeepSeek-V4 Launch